- Food Packaging

- Compostable Pouch Market

Compostable Pouch Market Size, Share, and Growth Forecast, 2026 - 2033

Compostable Pouch Market by Product Type (Stand-Up Pouches, Flat Pouches, Others), Closure Type (Zipper, Tear Notch, Others), Application (Food & Beverages, Personal Care, Healthcare/Industrial), and Regional Analysis 2026 - 2033

Compostable Pouch Market Size and Trends Analysis

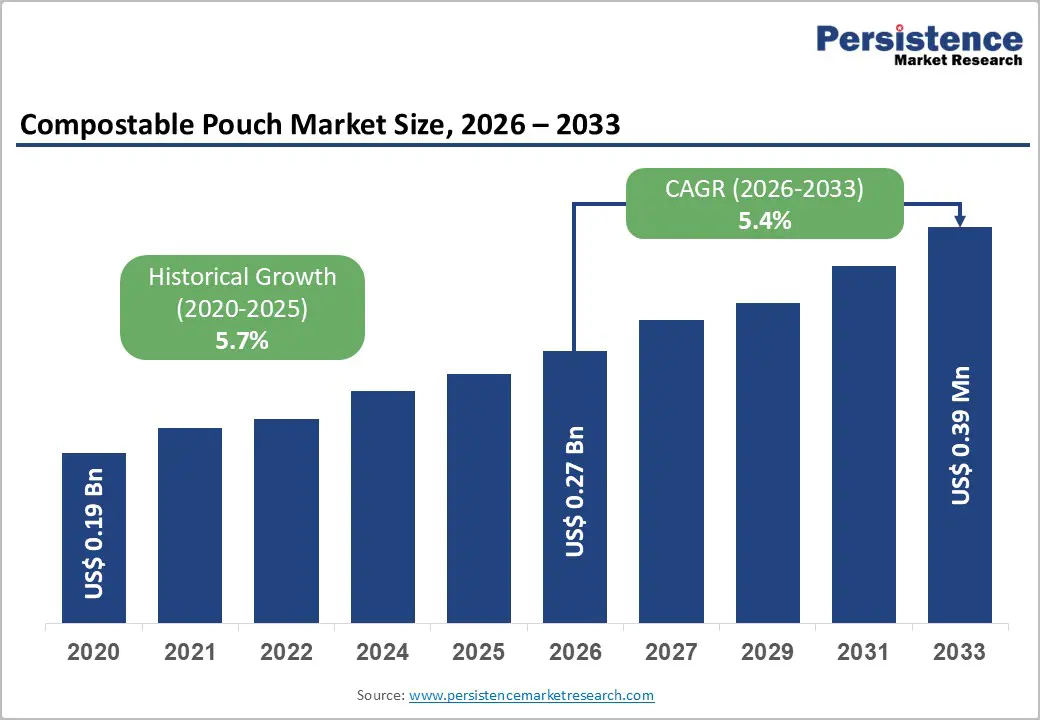

The global compostable pouch market size is likely to be valued at US$0.27 billion in 2026 and is expected to reach US$0.39 billion by 2033, growing at a CAGR of 5.4% during the forecast period from 2026 to 2033, driven by the rising demand for sustainable packaging amid plastic bans and consumer eco-preferences.

Regulatory pressures from governments accelerate adoption in food sectors. Rising environmental regulations and consumer demand for sustainable alternatives to single-use plastics drive steady market expansion, supported by advancements in bio-based materials that enhance. Projections indicate balanced growth, with emerging economies contributing significantly through manufacturing efficiencies and policy incentives.

Key Industry Highlights:

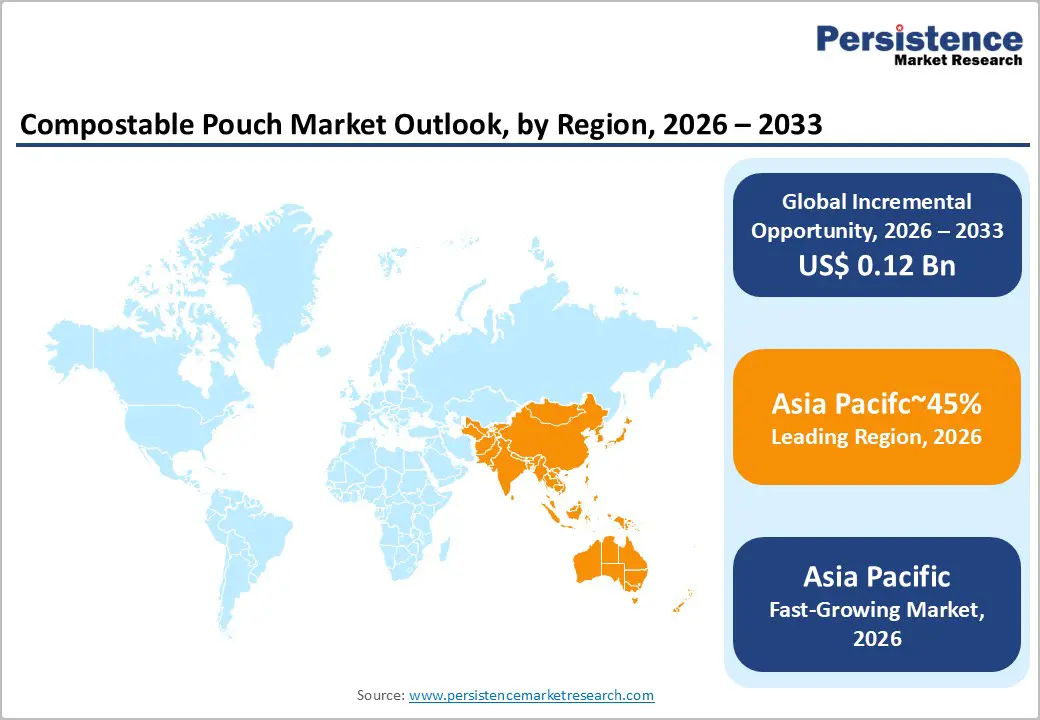

- Leading Region: Asia Pacific is projected to lead due to structural manufacturing dominance, regulatory acceleration, and integrated biopolymer supply chains, accounting for approximately 45% share in 2026, supported by large-scale PLA production, cost-optimized conversion clusters, and strong ecosystem alignment between polymer producers and pouch manufacturers.

- Fastest Growing Region: Asia Pacific is anticipated to grow the fastest due to rapid industrial expansion, aggressive plastic reduction policies, and accelerating adoption across food delivery, retail, and personal care sectors.

- Leading Product Type: Stand-up pouches are expected to lead, accounting for approximately 60% share in 2026, through strong retail adoption, high production throughput, superior shelf visibility, and suitability for premium and high-value food applications.

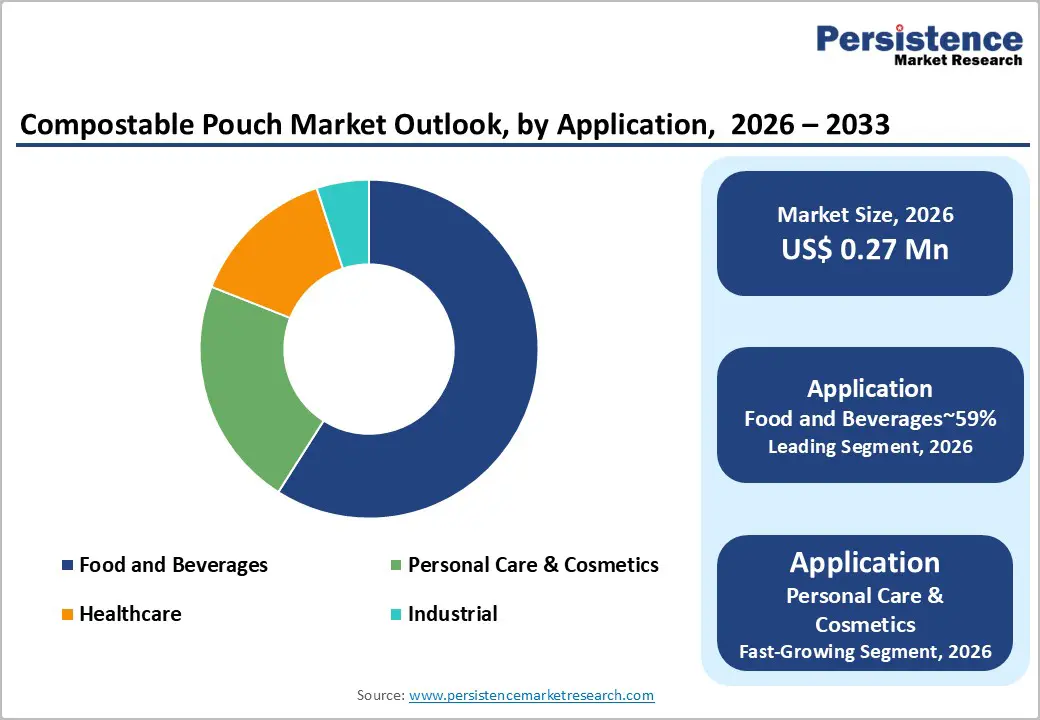

- Leading Application: The food & beverages segment is projected to dominate for functional simplicity, cost-efficiency, high-volume consumption cycles, and broad adoption across organized retail, holding approximately 59% share in 2026.

| Key Insights | Details |

|---|---|

| Compostable Pouch Market Size (2026E) | US$0.27 Bn |

| Market Value Forecast (2033F) | US$0.39 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Technological Advancements in Biopolymers

Advancements in biopolymer engineering are materially strengthening compostable pouch performance across applications. Innovations in Polylactic Acid and Polyhydroxyalkanoates have enhanced barrier resistance against moisture and oxygen transmission. These improvements address historical shelf life limitations that constrained broader adoption. Expanded global research investments are accelerating polymer refinement and processing optimization. Production scale expansions, including initiatives by BASF, signal structural capacity enhancement across supply chains. Cost compression achieved through process efficiency is narrowing the pricing gap with conventional plastics. Enhanced mechanical strength and sealing integrity improve compatibility with existing filling lines.

The improved polymer functionality reduces material redundancy and multilayer complexity. This streamlining lowers conversion waste and improves yield efficiency for flexible packaging converters. Enhanced barrier stability enables penetration into moisture-sensitive food and personal care categories. Regulatory alignment with compostability standards further supports procurement integration across sustainability mandates. Performance parity reduces retailer resistance linked to durability and storage risk concerns. Margin structures gradually stabilize as input variability declines and throughput increases.

Regulatory Mandates on Plastic Reduction

Escalating regulatory intervention targeting single-use plastics is reshaping packaging demand structures. Governments across major economies are implementing phased bans, usage restrictions, and extended producer responsibility frameworks. These measures directly constrain conventional polymer consumption within flexible packaging applications. Compliance obligations compel brand owners to reassess material selection and lifecycle impacts. Compostable pouches increasingly align with regulatory criteria governing biodegradability and waste diversion. Certification standards embedded within policy instruments formalize acceptance of industrial compostable materials. Public procurement policies further reinforce substitution toward environmentally compliant packaging formats.

Heightened enforcement intensity alters cost allocation throughout packaging and waste management systems. Producers internalize disposal liabilities through eco-modulation fees and compliance reporting burdens. Conventional plastic formats face rising fiscal disincentives linked to landfill diversion targets. Compostable pouch manufacturers benefit from improved competitive positioning within regulated retail channels. Waste infrastructure modernization encourages compatibility with certified compostable material streams. These structural shifts embed policy compliance into procurement decisions, accelerating institutional demand reconfiguration.

Barrier Analysis - Inadequate Infrastructure and Shelf Life Constraints

Limited access to industrial composting infrastructure restricts effective end-of-life realization. Only a fraction of households have access to certified composting facilities. This gap undermines environmental claims and increases contamination within conventional waste streams. Municipal collection systems often lack segregation protocols for certified compostable materials. Misclassification risks reduce recovery efficiency and weaken circularity outcomes. Retailers face reputational exposure when disposal pathways remain unclear to consumers. Policy frameworks frequently mandate compostability without parallel investment in processing capacity. Consequently, infrastructure asymmetry constrains the functional scalability of compostable pouch adoption.

Material performance limitations further compound commercialization challenges across sensitive product categories. Compostable laminates exhibit shorter shelf life under elevated humidity conditions. Liquids and perishable goods face higher spoilage exposure relative to multilayer plastics. Barrier instability influences inventory turnover, logistics planning, and retailer stocking policies. Certification processes introduce procedural complexity and extended approval timelines across jurisdictions. Compliance documentation elevates administrative burdens for converters and brand owners. Concurrently, recyclable flexible packaging alternatives compete on durability and established recovery systems. These combined pressures suppress margin stability and moderate procurement acceleration.

Technical and Performance Limitations

Intrinsic material properties of compostable polymers constrain their barrier effectiveness. Biopolymers such as Polylactic Acid and starch-based blends exhibit hydrophilic behavior under humid conditions. Elevated oxygen and moisture transmission rates limit protection for oxidation-sensitive products. Applications, including roasted coffee and high-fat snacks, face reduced shelf stability. Conventional multilayer laminates derived from Polyethylene Terephthalate and polyethylene provide superior barrier consistency across climates. Performance gaps necessitate additional coatings or complex laminate structures. These adaptations increase formulation complexity and processing sensitivity.

Thermal and mechanical limitations further restrict seamless integration into established packaging lines. Compostable films demonstrate lower melting thresholds and reduced heat seal robustness. Vertical form fill seal operations experience slower throughput due to narrower sealing windows. Reduced line efficiency elevates operational expenditure beyond raw material cost differentials. High polylactic acid content also introduces brittleness and acoustic crackling during handling. Premium consumer brands assess tactile perception as integral to packaging quality signals. Material fragility and noise characteristics, therefore, influence brand acceptance criteria. Collectively, these performance barriers moderate conversion speed within demanding commercial applications.

Opportunity Analysis - Addressing Unmet Needs in Personal Care

Evolving sustainability expectations within personal care are expanding demand for compostable packaging formats. Cosmetics and liquid hygiene products require flexible solutions with credible environmental positioning. Compostable pouches offer lightweight, reduced material intensity alternatives to rigid plastics. Policy developments, including directives issued by the European Union, reinforce waste reduction mandates across member states. These frameworks incentivize substitution toward certified compostable material systems. Brand owners increasingly align product launches with zero-waste positioning and lifecycle transparency. Compatibility with liquid formulations remains central to unlocking adoption within premium skincare and refill categories. Targeted innovation, therefore centers on moisture resistance, seal integrity, and aesthetic performance.

Dedicated research efforts focus on improving laminate durability without compromising compostability standards. Advances in liquid-compatible barrier coatings reduce leakage risks in humid environments. Scalable pouch architectures enable flexible sizing tailored to cosmetics distribution channels. Sustainability compliance enhances retailer acceptance within environmentally regulated markets. Integrated branding strategies leverage compostability claims to strengthen consumer engagement narratives. Value chain participants invest in certification alignment to streamline cross-border commercialization. These developments collectively position personal care as a structurally attractive expansion corridor for compostable pouches.

Compostable Packaging for Sustainable Personal Care

Evolving sustainability expectations within personal care are expanding demand for compostable packaging formats. Cosmetics and liquid hygiene products require flexible solutions with credible environmental positioning. Compostable pouches offer lightweight, reduced material intensity alternatives to rigid plastics. Policy developments, including directives issued by the European Union, reinforce waste reduction mandates across member states. These frameworks incentivize substitution toward certified compostable material systems. Brand owners increasingly align product launches with zero-waste positioning and lifecycle transparency. Compatibility with liquid formulations remains central to unlocking adoption within premium skincare and refill categories.

Dedicated research efforts focus on improving laminate durability without compromising compostability standards. Advances in liquid-compatible barrier coatings reduce leakage risks in humid environments. Scalable pouch architectures enable flexible sizing tailored to cosmetics distribution channels. Sustainability compliance enhances retailer acceptance within environmentally regulated markets. Integrated branding strategies leverage compostability claims to strengthen consumer engagement narratives. Value chain participants invest in certification alignment to streamline cross-border commercialization.

Category-wise Analysis

Product Type Insights

Stand-Up pouches are projected to lead, accounting for approximately 60% share in 2026, supported by strong retail visibility and format engineering advantages. Their structural rigidity and printable surface area enhance shelf differentiation in premium food and beverage categories. Integration of resealable zippers and degassing valves improves functionality for snacks and coffee applications. Manufacturers such as Amcor Plc and Mondi Group are advancing mono-material compostable laminates to replicate multilayer stiffness. TIPA Corp and Coveris reinforce market presence through high-barrier home compostable structures. Compatibility upgrades by Mespack support high-speed processing without major throughput losses.

Stand-Up pouches are anticipated to be the fastest-growing segment, driven by rigid-to-flexible substitution across consumer goods categories. Brands are replacing glass jars and metal cans with lightweight compostable formats to optimize freight economics. Spouted and retort-capable variants extend applicability into liquids, soups, and baby nutrition segments. UFlex Limited and ProAmpac are expanding aseptic and high-barrier pouch portfolios to capture evolving demand. Digital printing scale-up, including investments linked to ePac Flexible Packaging, enhances short-run customization for emerging brands.

Application Insights

Food & beverages are projected to lead, accounting for approximately 59% share in 2026, driven by high-volume ready meal and snack packaging demand. Rapid consumption cycles and contamination tolerance make compostable formats operationally suitable for food applications. Advanced barrier solutions and modified atmosphere integration improve shelf stability for perishables and fresh produce. Manufacturers such as TIPA Corp and Futamura are expanding high-barrier cellulose and multilayer compostable films. Parkside Flexibles and Eco-Products strengthen foodservice and retail deployment ecosystems. Migration compliance under authorities such as the Food Safety and Standards Authority of India reinforces qualification thresholds.

Personal care & cosmetics are anticipated to be the fastest-growing segment in the Compostable Pouch market, propelled by refill-based packaging transformation and premium sustainability positioning. Brands are replacing rigid plastic bottles with lightweight, compostable refill pouches to reduce material intensity. Innovations in oil-resistant linings and compostable spouts expand suitability for lotions and liquid cleansers. Companies including L'Oréal and Estée Lauder are piloting high-end compostable refill systems. Material advancements from Sulapac and cellulose technologies by Futamura enhance aesthetic and moisture resistance performance. E-commerce shipping efficiency and microplastic avoidance narratives further accelerate adoption.

Regional Insights

Asia Pacific Compostable Pouch Market Trends

Asia Pacific is expected to remain both the leading regional as well as fastest growing regional market, accounting for approximately 45% of global share in 2026, supported by structural manufacturing dominance and regulatory acceleration. The region is positioned to set global pricing benchmarks due to integrated biopolymer supply chains, large-scale PLA and starch-blend resin production, and cost-optimized pouch conversion clusters. Aggressive single-use plastic restrictions across major economies are anticipated to create a legally enforced demand floor, particularly in food delivery, snacks, and quick-service packaging. Rapid urbanization and middle-class expansion are projected to intensify the consumption of packaged goods, reinforcing volume scalability for compostable flexible formats. Harmonization efforts across ASEAN markets are expected to reduce regulatory fragmentation and facilitate cross-border trade in certified compostable materials.

China is anticipated to anchor regional expansion, commanding the largest share within Asia Pacific and shaping supply-demand equilibrium. National plastic reduction mandates and industrial modernization policies are expected to accelerate certified biodegradable pouch deployment across express logistics, catering, and retail ecosystems. Domestic manufacturers such as Mitsubishi Chemical Group are expected to intensify technology partnerships and barrier-material innovation across the region, strengthening film durability and heat-seal performance. Retailer competition is likely to remain fragmented and manufacturing-heavy, with strategic focus on cost leadership and rapid commercialization of starch-blend and PLA-based laminates.

North America Compostable Pouch Market Trends

North America is expected to remain a mature and structurally stable market in the compostable pouch industry, approximating 20% of global share, supported by compliance-driven upgrades and brand-led sustainability commitments. Regional expansion is projected to be anchored in replacement cycles across food retail, specialty beverages, and e-commerce fulfillment rather than greenfield manufacturing scale. Policy alignment through federal environmental frameworks and state-level single-use plastic restrictions is anticipated to reinforce institutional demand for certified compostable formats, particularly in organized retail and foodservice chains. High consumer sustainability awareness and retailer participation in voluntary packaging compacts are likely to sustain premiumization trends in bio-based laminates. The competitive landscape is set to remain consolidated, with multinational converters such as Amcor and Sealed Air reinforcing enterprise-grade supply contracts and technology-driven differentiation.

The U.S. is anticipated to function as the regional anchor, accounting for the dominant share within North America and shaping regulatory and innovation trajectories. State-level compostability mandates and retail compliance targets are expected to accelerate adoption in grocery, meal-kit, and direct-to-consumer packaging channels. Participation in initiatives such as the U.S. Plastics Pact is projected to influence procurement strategies toward certified reusable or compostable flexible formats. The compliance-oriented and innovation-led ecosystem is expected to preserve North America’s stable yet premium-focused compostable pouch trajectory.

Europe Compostable Pouch Market Trends

Europe is expected to remain a mature and structurally stable market, supported by regulatory harmonization, advanced waste infrastructure, and high certification thresholds. The region is positioned as the global standard setter, where compliance under EN 13432 and evolving Packaging and Packaging Waste Regulation enforcement frameworks is anticipated to sustain premium-grade adoption rather than volume-driven expansion. Circular economy alignment and eco-modulated Extended Producer Responsibility fee systems are expected to reinforce the cost competitiveness of certified compostable laminates relative to non-recyclable multi-layer plastics. Technological differentiation in cellulose-based films, paper-polymer hybrids, and advanced oxygen and moisture barrier engineering is likely to define competitive positioning.

Germany is projected to function as the regional anchor, accounting for the largest share within Europe and reinforcing infrastructure-backed scalability. National enforcement of EU directives is anticipated to accelerate certified pouch penetration in supermarket supply chains, while domestic chemical and materials innovators such as BASF are likely to advance bio-based polymer refinement and barrier resin development. Retailer sustainability mandates are set to drive supplier realignment toward home-compostable and paper-look flexible formats, strengthening value-added positioning rather than commoditized competition.

Competitive Landscape

The global compostable pouch market is moderately fragmented, with leadership concentrated among global flexible packaging converters and specialty biopolymer developers such as Amcor, Mondi Group, and TIPA Corp. Market structure reflects a tiered ecosystem in which multinational packaging groups leverage scale, regulatory certification capabilities, and multinational procurement relationships, while regional specialists focus on material science innovation and niche application engineering. Leaders matter because compostable pouch adoption is specification-driven; qualification under industrial and home-compostability standards, food-contact compliance, and barrier validation directly influence retailer approval lists and multinational FMCG sourcing frameworks.

Competitive positioning is defined by differentiation across material platforms, integration depth, and end-market specialization. This creates a bifurcated landscape between scale-oriented contract manufacturers and innovation-led material developers. Industry behavior is expected to reflect gradual ecosystem consolidation through targeted acquisitions, joint development agreements, and co-investment in bio-polymer capacity. Service-led models integrating regulatory advisory, life-cycle assessment support, and end-of-life partnership networks are likely to expand, reinforcing platform-based competition rather than single-product sales.

Key Industry Developments:

- In November 2025, TIPA acquired SEALPAP to bolster its position in paper-based sustainable packaging solutions, enhancing TIPA's ability to deliver high-performance compostable and recyclable alternatives across diverse global markets.

- In July 2025, Amcor and Mediacor collaborated to launch a 2-liter spouted stand-up pouch for liquid products in Europe. The refillable, recycle-ready solution for home cleaning products reduces plastic consumption compared to traditional rigid containers.

- In July 2025, Huhtamaki launched new compostable ice cream cups that are both home and industrially compostable. The innovation utilizes bio-based material coatings to reduce fossil-based plastic content to less than 10% while maintaining product safety and appeal.

Companies Covered in Compostable Pouch Market

- Amcor

- Mondi Group

- BASF

- Smurfit Kappa

- Sealed Air

- Tetra Pak

- DS Smith

- Novamont

- TIPA

- NatureWorks

- BioBag International

- Klabin

- International Paper

- Elevate Packaging

- NPP Group

- The Compost Bag Company

Frequently Asked Questions

The global compostable pouch market is projected to be valued at US$0.27 billion in 2026 and is expected to reach US$0.39 billion by 2033, driven by accelerating plastic reduction mandates, sustainability-focused brand transitions, and expanding applications in food and personal care packaging.

Escalating bans on single-use plastics, Extended Producer Responsibility frameworks, and eco-modulated fee systems are compelling brand owners and retailers to transition toward certified compostable materials. Regulatory harmonization, particularly in Europe and parts of Asia Pacific, is embedding compostability standards into procurement policies, thereby structurally reshaping material selection strategies across flexible packaging value chains.

The compostable pouch market is forecast to grow at a CAGR of 5.4% from 2026 to 2033, reflecting steady adoption across regulated retail channels and performance improvements in biopolymer barrier technologies.

Asia Pacific is the leading regional market, accounting for approximately 45% share, supported by integrated biopolymer manufacturing clusters, aggressive plastic substitution policies, and expanding food delivery and e-commerce packaging demand in China and India.

The compostable pouch market is moderately fragmented, with leadership concentrated among global packaging and biopolymer innovators including Amcor, Mondi Group, BASF, TIPA, Novamont, NatureWorks, Sealed Air, Smurfit Kappa, DS Smith, and Tetra Pak. Competition is defined by material science expertise, certification capabilities, and vertically integrated supply partnerships spanning resin production to high-barrier pouch conversion.