- Food Packaging

- Tray Liners Market

Tray Liners Market Size, Share, and Growth Forecast, 2026 – 2033

Tray Liners Market by Product Type (Standard Tray Liners, Custom Printed Tray Liners, Others), Material Type (Paper, Plastic, Foil, Others), End-use Industry (Food Service Industry, Retail Industry, Healthcare Industry, Household Use), and Regional Analysis for 2026 – 2033

Tray Liners Market Size and Trends Analysis

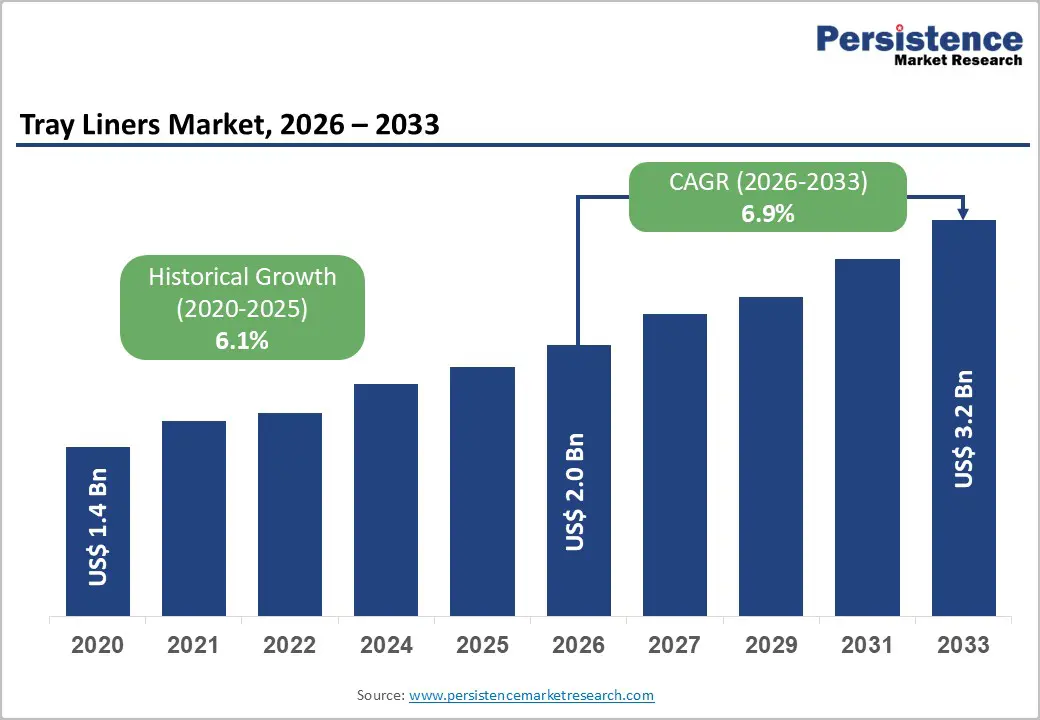

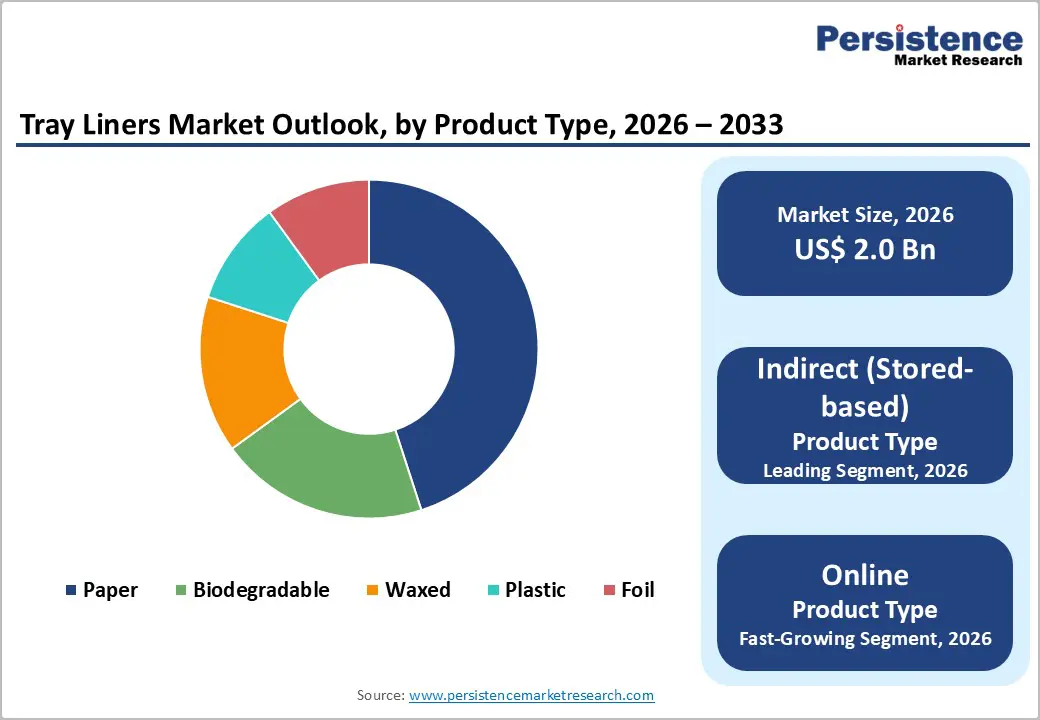

The global tray liners market size is likely to be valued at US$2.0 billion in 2026, and is expected to reach US$3.2 billion by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 to 2033, driven by the increasing prevalence of food safety and hygiene standards, rising demand for convenient disposable tray protection in food service and healthcare, and growing preference for biodegradable and custom-printed tray liners in retail and household applications.

The growing demand for high-absorbency, biodegradable, and paper-based tray liners in food service and healthcare is driving market growth. Innovations in grease-resistant coatings, compostable materials, and custom printing are enhancing performance and brand visibility. Tray liners are increasingly recognized for preventing contamination, protecting trays, improving food presentation, and reducing waste, fueling their adoption in emerging markets.

Key Industry Highlights:

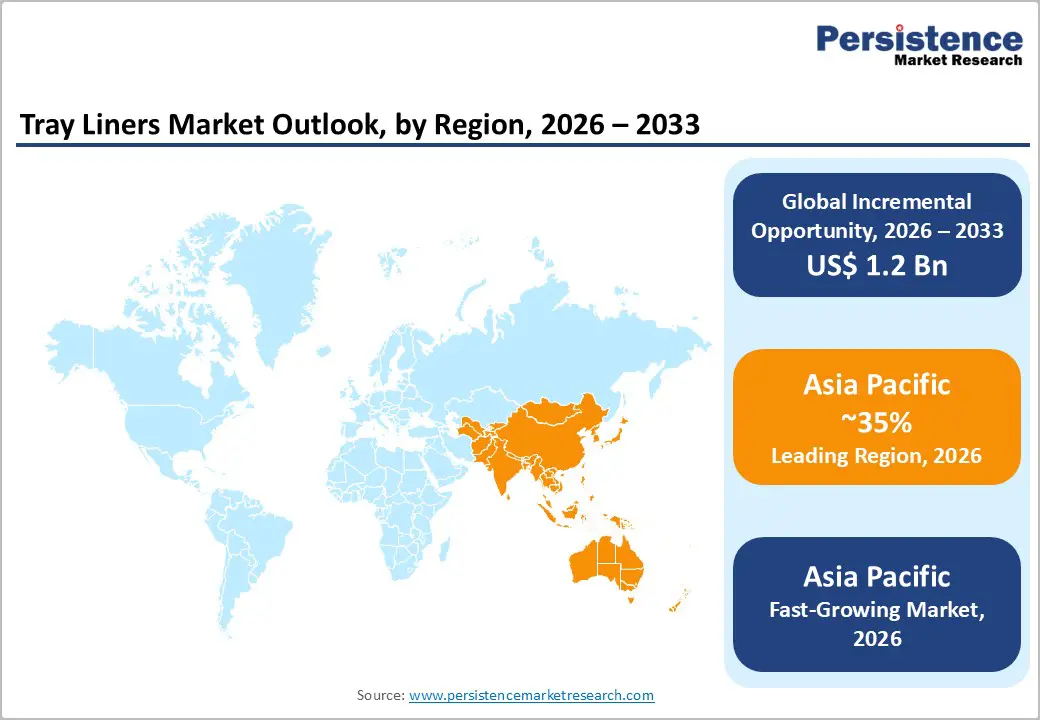

- Leading Region: Asia Pacific is expected to hold a 35% market share in 2026, driven by technological advancements in tray liners that offer stability, effectiveness, ease of use, and resistance to challenging climates, reducing contamination risks.

- Fastest-growing Region: Asia Pacific, fueled by the rapid expansion of organized food service, increasing healthcare infrastructure, and rising disposable income in China and India.

- Dominant Product Type: Standard tray liners, to hold approximately 48% of the market share, as they remain the most widely used format for cost-efficiency.

- Leading Material Type: Paper, to contribute nearly 52% of the market revenue, due to superior absorbency and sustainability appeal.

| Key Insights | Details |

|---|---|

| Tray Liners Market Size (2026E) | US$ 2.0 Bn |

| Market Value Forecast (2033F) | US$ 3.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Demand for Food Service and Healthcare Hygiene Requirements

Safe practices in food service environments have a measurable impact on public health, as shown by government data on the burden of unsafe food handling. The U.S. Centers for Disease Control and Prevention (CDC) estimates that 48 million people in the U.S. get sick from foodborne illnesses every year, leading to 128,000 hospitalizations and about 3,000 deaths annually. These illnesses are often linked to contamination occurring during food preparation, handling, or service, underscoring the importance of strict hygiene measures in restaurants, cafeterias, and other food service facilities to reduce contamination risks. Regular cleaning of surfaces, proper storage and handling, and minimizing contact with contaminants directly contribute to reducing these large numbers of annual foodborne illnesses and severe outcomes.

In healthcare settings, maintaining hygiene is crucial for patient safety and to prevent infections acquired during medical care. According to the World Health Organization (WHO), health care-associated infections (HAIs) are among the most frequent adverse events occurring during the delivery of health care, and on average, about 1 in 10 patients is affected by these infections in health care facilities worldwide. These infections not only cause additional suffering but also increase hospital stays and strain health systems. Rigorous hygiene protocols, including surface cleanliness, proper use of protective equipment, and adherence to sanitation standards, are essential to limit the spread of pathogens in clinical environments and support recovery.

Increasing Preference for Biodegradable and Custom-Printed Solutions

Consumer and business shifts toward biodegradable tray liners are rooted in growing awareness of the environmental burden created by traditional packaging. According to the U.S. Environmental Protection Agency (EPA), containers and packaging accounted for 82.2 million tons of municipal solid waste in 2018, representing a significant portion of overall waste streams, much of which ends up in landfills rather than being recycled or composted. As governments and environmental authorities highlight the limitations of conventional plastics, manufacturers and end-users are increasingly interested in materials that can break down through biological processes, reducing long-term waste accumulation and supporting composting programs that help divert organic waste from disposal pathways. Biodegradable options made from plant-derived polymers or other renewable materials require less reliance on finite fossil resources and can support more sustainable end-of-life outcomes for single-use products such as tray liners.

Alongside environmental motivations, the custom-printed biodegradable liner trend caters to brands looking to communicate sustainability commitments directly on packaging. Custom printing on biodegradable products allows food service companies and healthcare providers to combine functional waste reduction with clear messaging that aligns with regulatory trends and consumer preferences for sustainability. Clear on-product branding helps businesses signal engagement with environmental stewardship goals and meet increasing public demand for transparency in materials and disposal instructions.

Barrier Analysis – Environmental Restrictions on Single-Use Materials

Government mandates restricting single-use plastic items, including those used for packaging and food service applications, are limiting the traditional tray liners market by reducing the legal availability of certain materials that have historically been used in these products. For example, under the Plastic Waste Management (Amendment) Rules, 2021 in India, the manufacture, import, stocking, distribution, sale, and use of a wide category of single-use plastics such as cups, plates, cutlery, straws, and trays has been prohibited since 1 July 2022; the law also raised minimum plastic bag thickness standards to promote reuse. In this regulatory environment, product forms that rely on thin plastic liners face compliance challenges unless reformulated to fit permitted materials, increasing the complexity of maintaining previous product portfolios.

Similar regulatory trends are seen internationally, such as Europe’s Single-use Plastics Directive, which restricts placement on the market of specific items, including plates, cutlery, straws, and stirrers, and introduces measures to reduce the consumption of food containers by 2026. These policy frameworks force food service providers and manufacturers to transition away from conventional single-use plastic components toward alternatives or reusable systems to avoid fines and prohibitions.

Competition from Alternative Solutions

Tray liners compete directly with alternative packaging and containment solutions that can serve similar functions without requiring an additional disposable liner. For example, reusable trays made from rigid plastics, metals, or silicone can be washed and sanitized for repeated cycles in institutional kitchens, hospitals, and cafeterias. These products eliminate the need for a separate liner and lower ongoing procurement costs for facilities that have sufficient infrastructure for cleaning and sterilization. Steel or aluminum trays used in healthcare settings are designed to withstand repeated autoclaving or high-temperature washes, shifting demand away from single-use liners when organizations prioritize long-term cost efficiency and waste reduction.

Another common substitute in food service is rigid or molded fiber tray packaging that integrates a moisture-resistant coating or barrier layer. These integrated formats can provide containment and spill prevention without an added disposable liner sheet, streamlining workflows in high-volume environments such as quick-service restaurants or catering operations. Users may choose these alternatives when they simplify handling or reduce the number of SKUs needed in inventory.

Opportunity Analysis – Innovation in Biodegradable and Custom-Printed Tray Liners

Shifts toward biodegradable tray liners align with broader environmental objectives supported by government data on waste management. U.S. EPA statistics show that packaging waste constitutes a large part of municipal solid waste, and increasing recycling and composting rates over time have helped reduce landfill reliance and greenhouse gas emissions. For example, recycling and composting of municipal waste in the U.S. grew from just over 6 % in 1960 to about 35 % in 2017, contributing to significant environmental benefits such as reduced carbon dioxide emissions and conservation of resources. These figures highlight the value of materials that can re-enter ecological cycles and reduce conventional waste streams.

Government environmental programs also emphasize the benefits of composting organic materials, which can include biodegradable packaging components, to reduce methane emissions from landfills and recover nutrients via composting. Such recovery enhances soil health and supports sustainable resource use in agricultural settings, demonstrating an added ecological benefit when disposable liners can be processed in composting systems instead of persisting as waste.

Expansion in Online and Modern Retail Channels

Retail buying behavior has shifted significantly in recent years as consumers increasingly prefer online and modern retail channels for convenience, wider choice, and competitive pricing. E-commerce platforms and organized retail formats such as supermarkets, hypermarkets, and large grocery chains now serve as major purchase points for both household buyers and institutional customers such as restaurants, hotels, and catering services. In online marketplaces, buyers can easily compare different tray liner types, materials, and prices while accessing customer reviews that build trust in quality and performance. Retailers listed on e-commerce sites often offer bulk order options, subscription services, and prompt delivery, which help streamline procurement for businesses that regularly use disposable liner products. The convenience of doorstep delivery also encourages small and medium food service operators to adopt products they might not otherwise source through traditional local suppliers.

Modern retail stores further contribute to market expansion by offering visibility and accessibility to tray liner products alongside complementary packaging supplies. In physical retail environments, buyers can assess product features such as thickness, absorbency, and fit before purchase, enhancing buying confidence. Shelf placement in high-traffic store formats increases product exposure to a broader audience, including home cooks and small food businesses exploring new packaging solutions.

Category-wise Analysis

Product Type Insights

Standard tray liners are anticipated to dominate the market, accounting for approximately 48% of the market share in 2026. Their dominance is driven by their cost-effectiveness, wide availability, and suitability across diverse foodservice and packaging applications. These liners offer reliable grease absorption, moisture resistance, and hygiene support, making them a preferred choice for quick-service restaurants, bakeries, and institutional catering. Their compatibility with standard tray sizes simplifies procurement and inventory management for large operators. Growing demand from high-volume food outlets, expansion of takeaway and delivery formats, and rising emphasis on food safety and presentation further reinforce adoption. Heavy Duty, Grease-Resistant 3-Lb Paper Food Tray & Deli Liner Combo. This disposable grease-resistant tray liner from Avant Grub is widely used by quick-service restaurants, food trucks, and concession stands to line food trays and baskets.

Custom printed tray liners represent the fastest-growing product type, as foodservice brands increasingly use packaging as a low-cost marketing and customer engagement tool. Printed liners enhance brand visibility at the point of consumption, reinforcing logos, messages, and promotions directly in front of customers. The growth of social media sharing and visual food presentation has amplified demand for aesthetically appealing, branded tray liners that improve the dine-in and takeaway experience. Advancements in digital printing have reduced minimum order quantities and turnaround time, making customization affordable for small and mid-sized outlets. Custom printed meal tray sleeves (pack of 1,000) are designed to fit food trays and serve containers, showcasing branding or logos directly on the liner. Businesses such as cafés, cloud kitchens, and quick-service restaurants are increasingly using these branded liners to strengthen brand recognition, improve customer recall, and elevate the presentation of meals for takeaway or dine-in.

Material Type Insights

The paper segment is expected to dominate the market, contributing nearly 52% of revenue in 2026, fueled by a strong balance of cost, functionality, and sustainability. Paper tray liners offer effective grease absorption, breathability, and food-safe contact, making them ideal for high-volume foodservice applications such as quick-service restaurants, bakeries, and cafeterias. Growing regulatory and consumer pressure to reduce plastic use is accelerating the shift toward paper-based packaging. Paper liners are lightweight, easy to dispose of, and increasingly available in recyclable and compostable formats. Heavy Duty, Grease Resistant 3Lb Paper Food Tray and Deli Liner, this paper tray and deli liner is widely used in restaurants, bakeries, and food trucks as a disposable paper liner that absorbs grease and moisture while providing a sanitary surface for serving food.

The biodegradable segment is the fastest-growing material type, driven by increasing environmental awareness and stricter regulations on single-use plastics. Consumers and foodservice operators are increasingly opting for materials that naturally decompose after disposal, reducing landfill waste and environmental impact. Advancements in biodegradable polymers and plant-based fibers have enhanced performance, offering strong, moisture-resistant alternatives for trays, liners, and packaging. With many cities and countries imposing bans or taxes on traditional plastics, the shift to biodegradable options is accelerating. The 1000-piece Biodegradable 5.5-inch Square Tray is made from eco-friendly materials and is widely used by restaurants, cafés, and catering services as a sustainable alternative to plastic or paper trays. Its compostable nature meets the growing demand for environmentally responsible packaging that reduces waste and supports sustainability efforts.

Regional Insights

North America Tray Liners Market Trends

North America stands out due to its high food-service volumes, strict hygiene regulations, and strong public awareness of the benefits of disposable convenience. The distribution networks in the United States and Canada offer comprehensive support for tray liner programs, making them easily accessible across various sectors, including standard, paper, and food service industries. The growing demand for sustainable, user-friendly solutions is driving the adoption of these products, as they enhance hygiene and eliminate the challenges posed by cloth liners.

Innovation in tray liners technology, including stable biodegradable, improved custom-printed delivery, and targeted healthcare enhancement, is attracting significant investment from both public and private sectors. Government initiatives and FDA/CDC campaigns continue to promote use against contamination risks, sustainability concerns, and emerging green threats, creating sustained market demand. The growing focus on pre-cut grades and specialty uses, particularly for food service and others, is expanding the target applications for tray liners.

Europe Tray Liners Market Trends

Market growth in Europe is propelled by increasing awareness of sustainability and hygiene benefits, strong regulatory systems, and government-led circular economy programs. Countries such as Germany, France, the U.K., and Italy have well-established food-service and healthcare frameworks that support routine tray liners and encourage the adoption of innovative biodegradable delivery methods. These high-compliance formulations are particularly appealing for food service populations, regulation-conscious operators, and retail users, improving absorbency and coverage rates.

Technological advancements in tray liner development, such as enhanced compostable coatings, application-targeted delivery, and improved custom-printed grades, are further boosting market potential. European authorities are increasingly supporting research and trials for liners against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, eco-friendly options is aligned with the region’s focus on preventive waste reduction and food safety. Public awareness campaigns and promotion drives are expanding reach in both food service and healthcare segments, while suppliers are investing in sustainable substrates and novel variants to increase efficacy.

Asia Pacific Tray Liners Market Trends

Asia Pacific is expected to dominate and be the fastest-growing market, capturing 35% revenue in 2026, driven by rising hygiene awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Indonesia, and Thailand are actively promoting tray liner campaigns to address food-service growth and emerging healthcare needs. Tray liners are particularly attractive in these regions due to their cost-effective administration, ease of adoption, and suitability for large-scale food service and retail drives in both urban and semi-urban populations.

Technological advancements are supporting the development of stable, effective, and easy-to-use tray liners, which can withstand challenging climatic conditions and minimize contamination dependence. These innovations are critical for reaching domestic operators and improving overall hygiene coverage. Growing demand for standard, paper, and food service applications is contributing to market expansion. Public-private partnerships, increased food-service expenditure, and rising investment in tray liners research and production capacity are further accelerating growth. The convenience of liner delivery, combined with improved hygiene and reduced risk of cross-contamination, positions it as a preferred choice.

Competitive Landscape

The global tray liners market is shaped by competition between established medical and food-service packaging leaders and a growing set of sustainability-focused specialists. In North America and Europe, companies such as Medline Industries and Sirane leverage strong R&D capabilities, wide distribution networks, and deep relationships with hospitals and foodservice operators to drive adoption. Their portfolios increasingly emphasize biodegradable materials and custom-printed liners, helping customers meet hygiene, branding, and sustainability goals simultaneously.

In Asia Pacific, regional manufacturers gain traction with cost-competitive offerings, improving accessibility for small and mid-sized food outlets and institutional buyers. Paper-based delivery formats remain central to growth, as they enhance absorbency, reduce contamination risks, and integrate easily across standardized trays in healthcare and foodservice settings. Meanwhile, strategic partnerships, collaborations, and targeted acquisitions are accelerating innovation cycles, expanding product portfolios, and shortening time-to-market.

Key Industry Developments:

- In January 2026, Ranpak partnered with Medline Industries to replace plastic protective packaging with paper-based alternatives across Medline’s high-volume distribution centers. The move reduced plastic waste, improved packing efficiency, and strengthened supply-chain sustainability across Medline’s U.S. and Europe operations.

Companies Covered in Tray Liners Market

- Medline Industries

- HASTI MEDIC

- SafMed

- Sirane

- Clinipak Limited

- NOVIPAX LLC

- Pactiv LLC

- Weifang Sunshine Packaging

- Healthmark Industries Company

- Flexipol Packaging Limited

- Kimberly-Clark Corporation

- Owens & Minor Inc.

- Cardinal Health

- Shenzhen Snowdent Healthcare

Frequently Asked Questions

The global tray liners market is projected to reach US$2.0 billion in 2026.

Rising regulatory pressure and customer demand to replace plastic with paper-based and biodegradable packaging in healthcare and foodservice.

The tray liners market is poised to witness a CAGR of 6.9% from 2026 to 2033.

Increasing adoption of custom-printed tray liners as low-cost branding tools in foodservice and institutional catering.

Medline Industries, Sirane, NOVIPAX LLC, Pactiv LLC, and Kimberly-Clark Corporation are the key players.