- Medical Devices

- Medical Adhesive Tape Market

Medical Adhesive Tape Market Size, Share, and Growth Forecast, 2026 - 2033

Medical Adhesive Tape Market by Product Type (Fabric Tapes, Paper Tapes, Plastic Tapes, Silicone Tapes, Others), Adhesive Type (Acrylic-Based Adhesive Tapes, Others), Adhesive (Surgery, Wound Dressing, Orthopedic Adhesives, Others), and Regional Analysis for 2026 - 2033

Medical Adhesive Tape Market Share and Trends Analysis

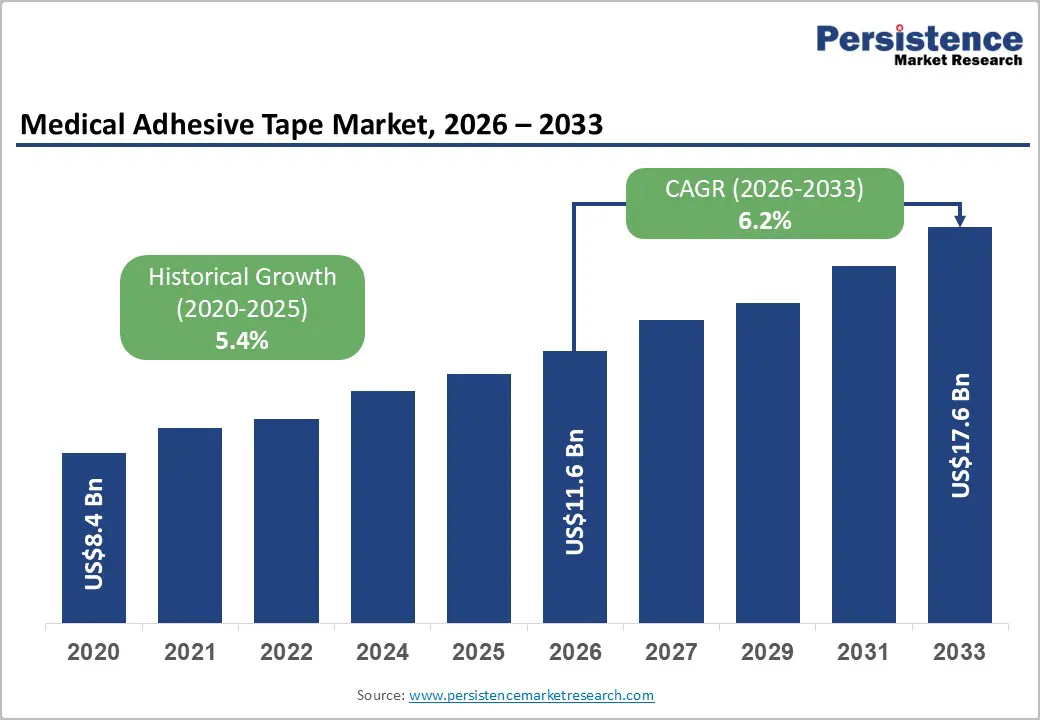

The global medical adhesive tape market size is likely to be valued at US$11.6 billion in 2026 and is estimated to reach US$17.6 billion by 2033, growing at a CAGR of 6.2% during the forecast period 2026 - 2033, driven by rising surgical procedures, expanding chronic wound management requirements, and increasing adoption of advanced skin-friendly fixation materials.

Growth momentum remains supported by aging population trends and rising hospitalization rates, creating sustained demand for wound closure and securement products across healthcare systems. Regulatory emphasis on infection prevention and patient safety is accelerating the transition toward hypoallergenic and silicone-based tapes with enhanced skin compatibility.

Key Industry Highlights

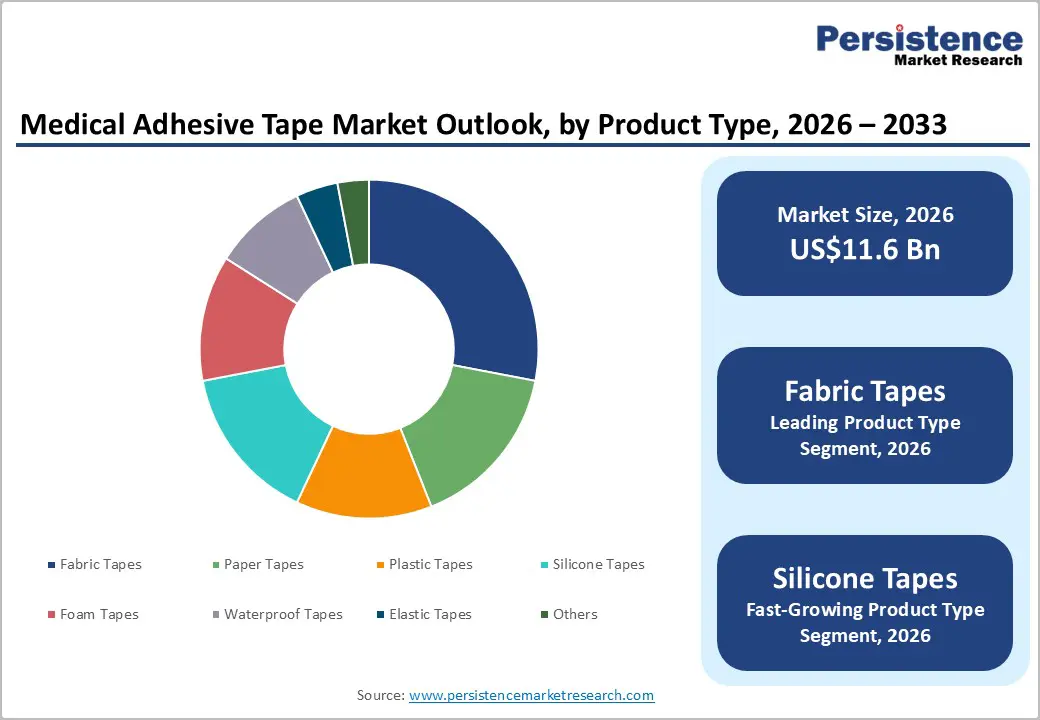

- Leading Product Type: Fabric tapes are set to hold around 28% revenue share in 2026, driven by strong clinical preference in wound dressing and post-surgical fixation adhesives.

- Fastest-Growing Product Type: Silicone tapes are projected as the fastest-growing segment, supported by clinical adoption of gentle adhesion technologies that minimize epidermal trauma.

- Leading Adhesive: Wound dressing is estimated to hold roughly a 35% revenue share in 2026, due to the structural dependence of wound care protocols on adhesive tape across acute and chronic management.

- Fastest-Growing Adhesive: Diagnostic and monitoring Adhesives are forecast to record the fastest growth, driven by the rising adoption of wearable continuous monitoring devices requiring medical-grade skin attachment.

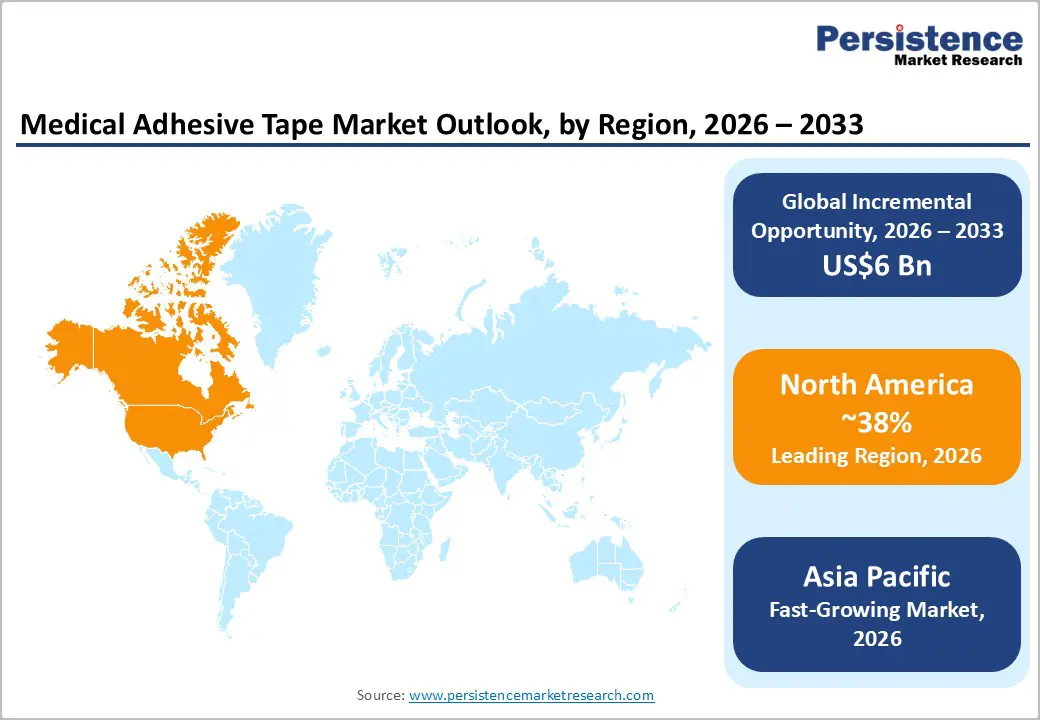

- Regional Leadership: North America is projected to capture roughly 38% of the market share in 2026, while Asia Pacific is forecast to record the fastest growth due to rapid clinical infrastructure modernization.

- Competitive Environment: The market reflects a moderately consolidated structure, with 3M Company and Mölnlycke Health Care leveraging proprietary adhesive technology and global distribution scale to maintain competitive positioning.

DRO Analysis

Driver - Rising Surgical Volumes and Chronic Wound Management Demand

The increasing prevalence of chronic diseases and trauma-related injuries is driving higher surgical procedure volumes, strengthening demand for secure wound fixation products. Medical adhesive tapes remain essential across pre-operative, intra-operative, and post-operative care environments due to their role in dressing stabilization and catheter fixation. The expanding elderly population groups are contributing to a greater incidence of diabetic ulcers, pressure injuries, and vascular wounds requiring long-duration dressing adhesives.

According to the U.S. Centers for Disease Control and Prevention (CDC), nearly 38.4 million individuals in the U.S. were living with diabetes in 2024, creating sustained wound management requirements across healthcare facilities. Growing diabetic patient populations are increasing demand for breathable and skin-sensitive adhesive products that reduce dressing displacement and minimize skin trauma. Healthcare providers are prioritizing tapes with improved adhesion durability to reduce infection risks and clinical intervention frequency.

Restraint - Volatility in Raw Material Supply Chains and Production Costs

Medical adhesive tape manufacturing depends heavily on petrochemical derivatives, specialty polymers, silicone compounds, and medical-grade substrates exposed to supply-chain disruptions and pricing volatility. Rising transportation costs and fluctuating resin availability are increasing operational expenditure for manufacturers. Margin pressure is intensifying among mid-sized producers lacking vertically integrated procurement capabilities or long-term supplier agreements.

Regulatory compliance requirements for biocompatibility testing and sterilization validation are extending product approval timelines and increasing manufacturing expenses. Cost escalation associated with high-performance silicone adhesives is limiting penetration across price-sensitive healthcare facilities. Procurement delays linked to fluctuating raw material availability are restricting scalability and reducing production flexibility during periods of elevated demand.

Opportunity - Growth in Home Healthcare and Wearable Medical Device Adoption

The expansion of home healthcare services and remote patient monitoring is increasing demand for easy-to-apply medical adhesive tapes suitable for non-clinical environments. Rising use of wearable glucose monitors, cardiac telemetry systems, and portable infusion devices is creating new Adhesive areas requiring durable yet skin-compatible fixation solutions. Manufacturers capable of developing lightweight and waterproof tapes are positioned for accelerated growth.

Healthcare systems are promoting decentralized patient care models to reduce hospitalization costs and improve treatment accessibility. This transition is increasing the procurement of adhesive products compatible with long-duration monitoring and home-based wound management. Strategic collaboration with wearable device manufacturers can create integrated fixation ecosystems supporting recurring product utilization and broader distribution penetration.

Category-wise Analysis

Product Type Insights

Fabric tapes are anticipated to secure around 28% of the medical adhesive tape market share in 2026, reflecting strong clinical preference for conformable, breathable textile substrates in wound care. 3M Health Care supplies fabric tape systems across surgical suites globally. The breathable structure reduces maceration risk in long-wear clinical Adhesives.

Silicone tapes are expected to be the fastest-growing segment, propelled by widespread clinical adoption of gentle adhesion technologies. Smith+Nephew introduced silicone fixation solutions supporting delicate wound care adhesives in intensive care environments. Rising wearable device utilization and long-duration monitoring procedures continue accelerating commercial demand substantially.

Adhesive Type Insights

Acrylic-based adhesive tapes are poised to dominate with a forecast market share of over 38% in 2026, powered by broad chemical versatility across low-, medium-, and high-tack performance tiers. Avery Dennison Medical supplies acrylic adhesive substrates used in branded tape products across North America and Europe. Compatibility with sterilization processes supports deployment in sterile wound care adhesives.

Silicone-based adhesive tapes are estimated to be the fastest-growing segment, fueled by the global transition toward skin-safe medical device attachment protocols. Mölnlycke Health Care has commercialized silicone adhesive systems for negative pressure wound therapy device attachment. ISO 10993 biocompatibility recognition is reducing clinical hesitancy and accelerating formulary adoption.

End-user Insights

Wound dressing is likely to be the leading segment with a projected 35% of the medical adhesive tape market share in 2026, due to the structural dependence of wound care protocols on adhesive tape for dressing fixation and periwound skin protection. Hartmann Group incorporates adhesive tape in wound dressing systems used across European hospital networks. The chronic wound epidemic sustains consistent per-patient tape consumption across multi-week cycles.

Diagnostic and monitoring Adhesives are anticipated to be the fastest-growing segment, fueled by the proliferation of wearable devices, including cardiac patches, glucose sensors, and respiratory monitors. Abbott Laboratories integrates medical adhesive tape into the FreeStyle Libre CGM system worn by millions globally. Growing telehealth adoption is sustaining demand for skin-worn diagnostic device attachment solutions.

Regional Insights

North America Medical Adhesive Tape Market Trends

North America is expected to lead with an estimated 38% of the medical adhesive tape market share in 2026, supported by a mature healthcare infrastructure and high per-capita healthcare expenditure. 3M, Cardinal Health, and Medline maintain strong distribution networks across acute care and ambulatory settings.

U.S. Medical Adhesive Tape Market Insights

The U.S. is projected to account for approximately 82% of the North American market in 2026, underpinned by a large chronic disease patient base and well-established CMS reimbursement frameworks. 3M Health Care and Medline capacity expansions are forecast to reinforce domestic supply chain resilience.

Canada Medical Adhesive Tape Market Insights

Canada is forecast to represent around 18% of the North America market in 2026, driven by federal and provincial hospital modernization investments. Progressive alignment with international harmonization standards is expected to reduce market access timelines for innovative products. McKesson Canada is forecast to expand medical consumable portfolios to serve growing community care settings.

Europe Medical Adhesive Tape Market Trends

Europe is likely to secure a 28% market share in 2026, driven by robust public healthcare infrastructure and strict implementation of regional medical device safety regulations. European manufacturing entities focus heavily on compliance with the updated European Medical Device Regulation (MDR), ensuring all adhesive chemical compositions undergo meticulous toxicological profiling.

Germany Medical Adhesive Tape Market Insights

Germany is projected to hold approximately 22% of the Europe market in 2026, driven by a high density of advanced wound care centers and robust public healthcare funding. Paul Hartmann AG maintains a strong domestic manufacturing presence supporting supply to German healthcare providers.

U.K. Medical Adhesive Tape Market Insights

The U.K. is forecast to account for approximately 16% of the European market in 2026. National Health Service (NHS) procurement frameworks are expected to prioritize cost-effective wound care tape solutions. Smith+Nephew's established clinical networks are likely to sustain penetration of advanced silicone tape systems.

Asia Pacific Medical Adhesive Tape Market Trends

Asia Pacific is forecast to be the fastest-growing market for medical adhesive tape, stimulated by rapid healthcare infrastructure modernization and expanding universal health coverage policies. Rising disposable incomes across developing population centers accelerate the volume of elective surgical interventions, directly elevating baseline utilization of essential clinical consumables.

China Medical Adhesive Tape Market Insights

China is projected to account for approximately 22% of the Asia Pacific market in 2026. The Made in China 2025 strategy is driving domestic medical tape manufacturing investment and reducing import dependency. The National Medical Products Administration (NMPA) regulatory approval pathway expansion is expected to accelerate domestic product submissions and distribution scale-up across national hospital procurement programs.

India Medical Adhesive Tape Market Insights

India is forecast to account for approximately 18% of the Asia Pacific market in 2026, with among the fastest regional growth rates. The Pradhan Mantri Jan Arogya Yojana (PM-JAY) scheme is expanding surgical access across tier-two and tier-three cities. Production-linked incentive schemes are attracting manufacturing investment and reducing supply chain dependence on imports.

Competitive Landscape

The global medical adhesive tape market is moderately consolidated, with a limited number of multinational manufacturers commanding substantial share through diversified product portfolios and global distribution networks. 3M Company, Mölnlycke Health Care, Smith+Nephew, Paul Hartmann AG, and Nitto Denko form the core competitive tier.

Mid-tier and regional manufacturers compete on price competitiveness and local product customization, particularly in Asia Pacific and Latin America. Private label manufacturing for retail pharmacy chains and group purchasing organizations places cost efficiency at the center of supplier qualification.

Key Industry Developments:

- In May 2026, Smith+Nephew launched ALLEVYN COMPLETE CARE Dressing and RENASYS EDGE wound management solutions at EWMA 2026, reinforcing innovation in advanced wound care and skin-friendly medical adhesive technologies for chronic wound treatment adhesives.

- In February 2026, Ahlstrom launched recyclable Acti-V® RRF Natural release liners for pressure-sensitive adhesive medical tapes, reinforcing sustainability and circular-material adoption across advanced healthcare adhesive applications.

Companies Covered in Medical Adhesive Tape Market

- 3M

- Mölnlycke Health Care AB

- Smith+Nephew plc

- Paul Hartmann AG

- Nitto Denko Corporation

- Cardinal Health Inc.

- Medline Industries LP

- BSN Medical GmbH

- Nichiban Co. Ltd.

- Toray Industries Inc.

- Avery Dennison Corporation

- Lohmann GmbH & Co. KG

- Invacare Corporation

- Hollister Incorporated

- Scapa Group plc

Frequently Asked Questions

The global medical adhesive tape market is projected to reach US$11.6 billion in 2026.

Increasing surgical procedures, rising chronic wound management demand, and expanding adoption of wearable medical devices are driving growth in the medical adhesive tape market.

The medical adhesive tape market is poised to witness a CAGR of 6.2% from 2026 to 2033.

Growing demand for silicone-based skin-friendly adhesives and expanding utilization of wearable healthcare monitoring devices are creating key opportunities in the medical adhesive tape market.

Some of the key market players include 3M Company, Mölnlycke Health Care, Smith+Nephew, Paul Hartmann AG, and Nitto Denko.