- Nutraceuticals & Functional Foods

- Meal Replacement Products Market

Meal Replacement Products Market Size, Share, and Growth Forecast 2026 - 2033

Meal Replacement Products Market by Product Type (Powder, Ready-to-Drink, Protein Bar), by Source (Animal-Based, Plant-Based), Distribution Channel (Business to Business, Business to Consumer), and Regional Analysis, 2026 - 2033

Meal Replacement Products Market Size and Trend Analysis

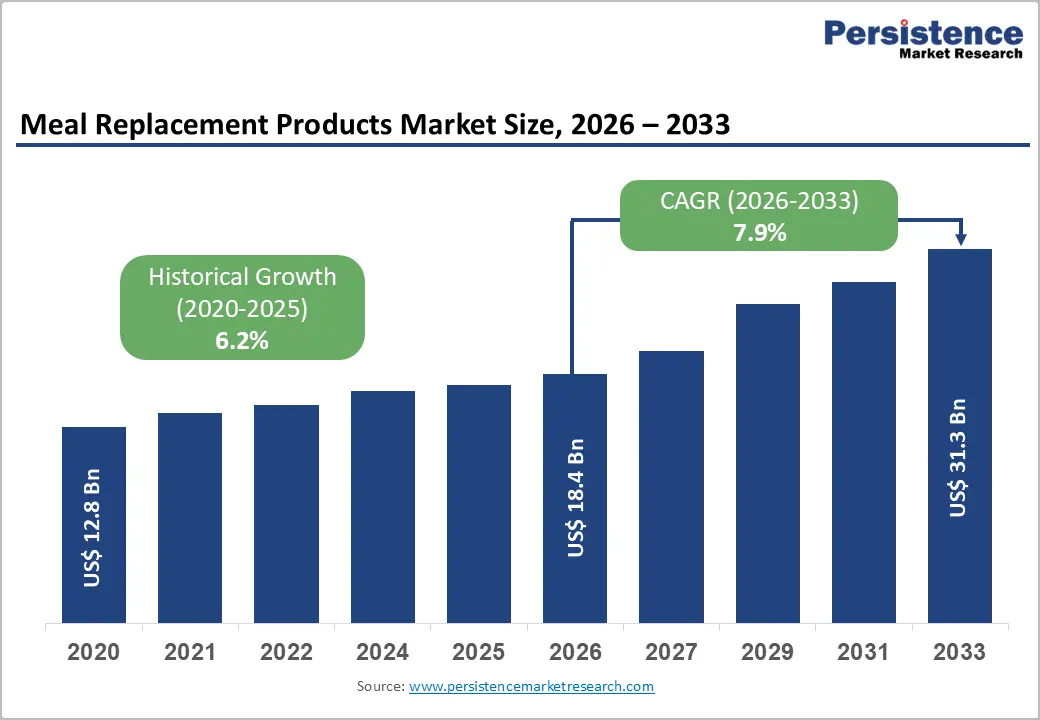

The global meal replacement products market size is expected to be valued at US$ 18.4 billion in 2026 and projected to reach US$ 31.3 billion by 2033, growing at a CAGR of 7.9% between 2026 and 2033. This robust growth trajectory is primarily driven by escalating global obesity rates and lifestyle-related diseases.

According to the World Health Organization (WHO), obesity has nearly tripled worldwide since 1975, with over 1 billion adults currently classified as obese, compelling consumers to adopt structured dietary interventions, including meal replacement solutions. The increasing prevalence of diabetes and cardiovascular conditions, combined with rising health consciousness among millennials and Gen Z consumers, is accelerating product adoption across both developed and emerging economies.

Key Industry Highlights

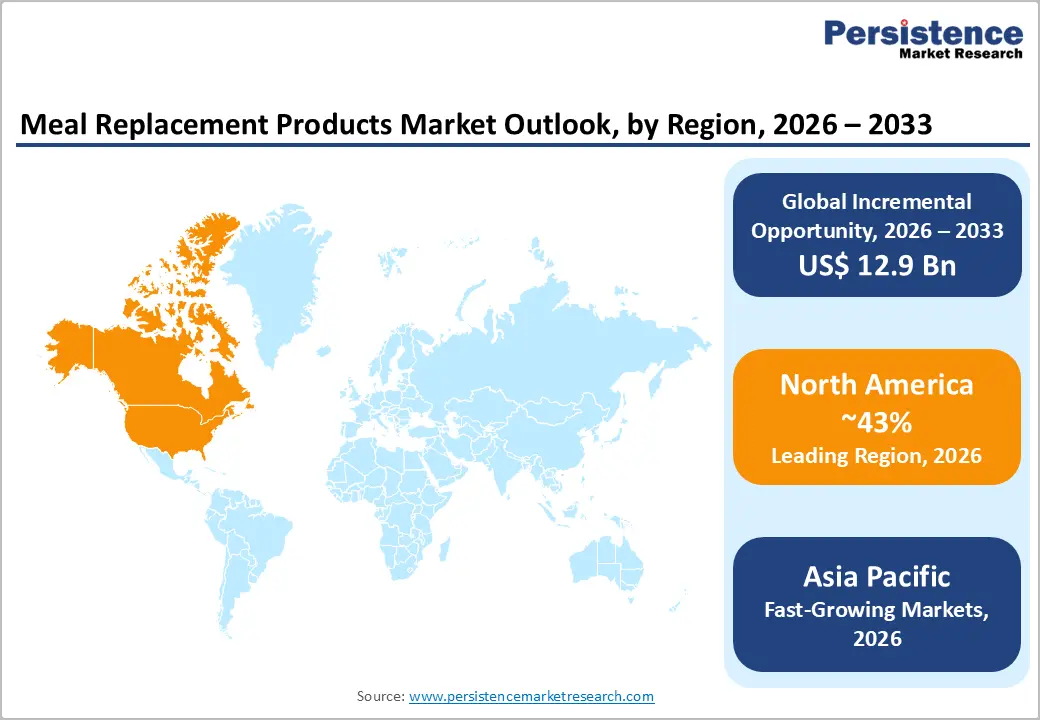

- Leading Region: North America dominates the Meal Replacement Products market with a 43% share (2025), supported by high obesity prevalence, strong consumer awareness, a mature supplement ecosystem, and stringent regulatory oversight ensuring product quality and trust.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by rapid urbanization, rising disposable incomes, increasing obesity awareness, expanding e-commerce penetration, and supportive regulatory developments across major economies.

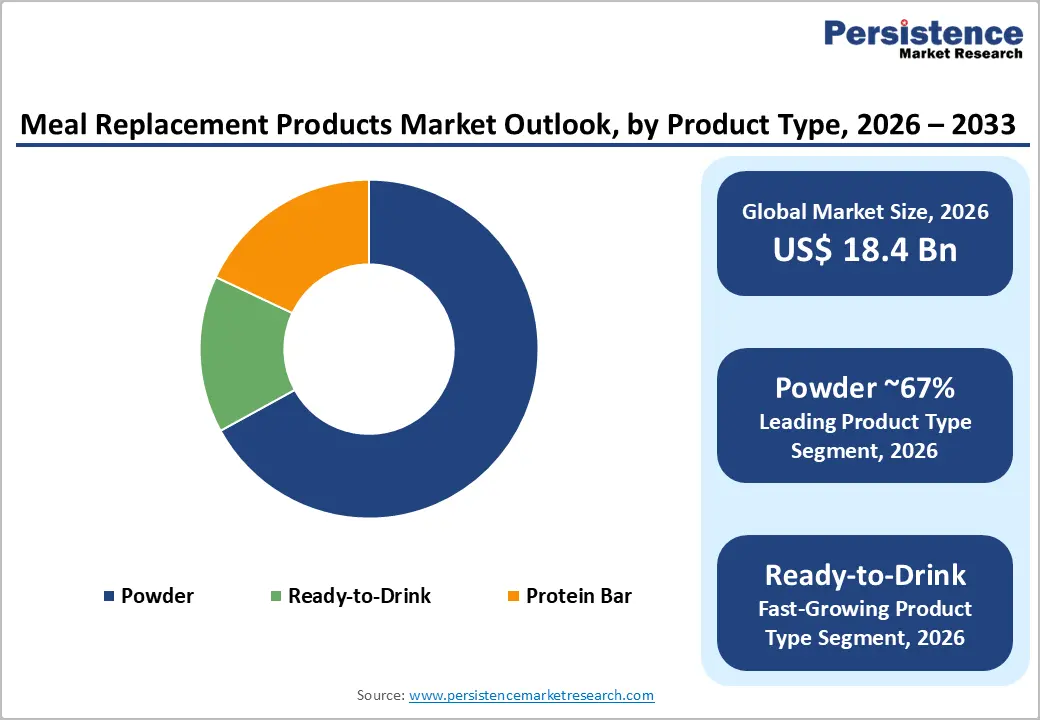

- Leading Product Segment: Powder-based meal replacements lead with approximately 67% share (2025), owing to their versatility, cost-effectiveness, longer shelf life, and ability to offer precise macronutrient customization for weight management.

- Fastest Growing Product Segment: Ready-to-Drink (RTD) meal replacements are witnessing the fastest growth, fueled by convenience, on-the-go consumption trends, wider retail availability, and ongoing product innovation.

- Key Market Opportunity: Plant-based formulations and AI-driven personalized nutrition platforms present significant growth potential, aligning with sustainability trends, evolving dietary preferences, and increasing demand for customized, science-backed nutrition solutions.

Market Dynamics

Drivers - Rising Prevalence of Obesity and Lifestyle Diseases Fueling Demand

The accelerating global burden of obesity and metabolic disorders represents the most powerful demand driver for the meal replacement products market. The World Health Organization (WHO) reports that over 650 million adults worldwide were classified as obese as of 2023, with projections indicating a continued rise through the next decade. Meal replacement products offer clinically structured, calorie-controlled dietary support that isincreasingly recommended by dietitians and healthcare providers as part of weight management protocols.

The U.S. Centers for Disease Control and Prevention (CDC) highlights that approximately 42.4% of U.S. adults are obese, creating a massive domestic consumer base. In addition, the International Diabetes Federation (IDF) estimates over 537 million adults globally were living with diabetes in 2023, further amplifying the need for nutritionally complete, portion-controlled meal alternatives that support glycemic management.

Shifting Consumer Lifestyles and Growing Demand for Convenient Nutrition

Rapid urbanization has extended working hours, and the proliferation of on-the-go lifestyles is significantly reshaping dietary patterns across developed and emerging markets alike. According to the Food and Agriculture Organization (FAO) of the United Nations, the global urban population is expected to reach 68% by 2050, intensifying demand for quick, nutritionally balanced food solutions. Meal replacement products, including powders, ready-to-drink beverages, and protein bars, address this need directly by providing complete macronutrient profiles in convenient formats.

The growing influence of fitness culture, endorsed by medical professionals and wellness influencers alike, is also accelerating consumer uptake, particularly among individuals aged 18–45 who prioritize health optimization alongside time efficiency. The convergence of busy lifestyles with rising nutritional awareness is expected to sustain strong demand momentum throughout the forecast period.

Restraints - High Product Costs Limiting Accessibility in Price-Sensitive Markets

Despite growing awareness, the relatively high retail price of quality meal replacement products remains a significant barrier to mass adoption, particularly in low- and middle-income countries. Premium formulations featuring organic, non-GMO, or clinically validated ingredients command substantially higher price points compared to conventional food alternatives. According to the World Bank, approximately 3.5 billion people globally subsist on less than USD 5.50 per day, making specialized nutritional products economically inaccessible.

Even in developed markets, consumer price sensitivity during inflationary periods, as evidenced by rising Consumer Price Index (CPI) figures reported by the U.S. Bureau of Labor Statistics (BLS) can dampen discretionary health product spending, constraining market penetration among middle-income segments.

Regulatory Complexity and Labelling Compliance Challenges

The meal replacement products sector is subject to stringent and often varying regulatory frameworks across geographies, creating compliance challenges for manufacturers seeking global distribution. In the European Union, products must comply with Regulation (EU) No. 609/2013 on foods intended for specific groups, which imposes detailed compositional and labeling requirements. Similarly, the U.S. Food and Drug Administration (FDA) regulates meal replacements under dietary supplement and food guidelines, requiring precise nutrient disclosures and health claim substantiation.

Divergent standards across the Asia Pacific region, governed by bodies such as FSSAI (India), FSANZ (Australia/New Zealand), and CFDA (China), further complicate multi-market product launches, increasing time-to-market and compliance costs for international players.

Opportunities - Expansion of Plant-Based Meal Replacement Formulations

The global surge in plant-based dietary preferences presents a compelling growth opportunity for meal replacement product manufacturers. According to the Good Food Institute (GFI), global plant-based food retail sales have grown consistently year-over-year, reflecting a structural shift in consumer dietary philosophy rather than a transient trend. The United Nations Environment Programme (UNEP) has also highlighted plant-rich diets as critical to achieving sustainability goals, providing tailwinds for plant-based meal replacement innovation. Formulations incorporating pea protein, brown rice protein, hemp, and quinoa are gaining significant traction, especially among vegan, flexitarian, and environmentally conscious consumers.

Companies investing in improved taste profiles, enhanced amino acid completeness through protein blending, and superior digestibility of plant-based meal replacements are well-positioned to capture a rapidly expanding consumer cohort that prioritizes both personal health and ecological responsibility.

E-Commerce Expansion and Personalized Nutrition Technology

The accelerating digitization of retail and the emergence of personalized nutrition technologies represent a transformational opportunity for the meal replacement products market. Global e-commerce penetration in the food and beverage sector has surged, with the International Trade Administration (ITA) reporting significant double-digit growth in online health product sales across major markets. Direct-to-consumer (DTC) business models enable brands to offer subscription services, personalized meal plans, and AI-driven dietary recommendations, significantly enhancing customer lifetime value.

Advances in nutrigenomics, the study of how individual genetic profiles interact with nutrition as highlighted by research published in the National Library of Medicine (NLM), are enabling companies to develop hyper-personalized meal replacement solutions tailored to specific metabolic profiles, health goals, and dietary restrictions. This intersection of digital commerce, data analytics, and nutritional science is expected to unlock significant revenue growth opportunities through 2033.

Category-wise Analysis

Product Type Insights

By product type, the meal replacement products market is segmented into powder, ready-to-drink, and protein bars. The powder segment held the largest revenue share of 67% in 2025 due to the convenience offered by the powdered meal replacements among health-conscious individuals. With intense job pressures leaving little time for meal planning and preparation, nutritional deficiencies have become rampant, thereby fueling the demand for on-the-go meal replacements.

Meal replacement products in powder form enable easy storage and have a longer shelf life. and enable simple preparation with water. Their minimal risk of contamination, along with the ability to customize portion sizes and ingredients, further enhances their appeal. The powdered form is also more cost-effective, especially when purchased in bulk, appealing to long-term users.

The ready-to-drink (RTD) segment is set to experience the fastest growth from 2026 to 2033 due to its convenience and immediate usability. RTD products require no preparation, making them ideal for on-the-go consumption, travel, pre-surgery nutrition, and weight loss. They offer better taste and satiety, effectively replacing calorie-dense meals with balanced nutrients. Innovations incorporating plant-based ingredients and specialized formulations, such as vegan, lactose-free, and keto-friendly options, are expanding their appeal. The RTD market is projected to nearly double by 2033, driven by rising health awareness, busy lifestyles, and product advancements.

Distribution Channel Insights

The online retail channel is rapidly emerging as the dominant and fastest-growing distribution channel in the meal replacement products market, propelled by the global acceleration of digital commerce. Hypermarkets and supermarkets continue to hold a significant share due to their broad geographic reach and consumer trust, particularly in North America and Europe, where organized retail infrastructure is well-developed. The U.S. Census Bureau reported sustained double-digit growth in e-commerce food and supplement sales in recent years.

Online platforms offer consumers access to a broader product range, detailed ingredient transparency, competitive pricing, and the convenience of subscription-based auto-delivery models factors particularly valued by health-conscious millennials and Gen Z shoppers. Business-to-Business (B2B) channels are also gaining traction, with gyms, corporate wellness programs, and clinical nutrition centers incorporating meal replacements into structured dietary offerings.

Regional Insights

North America Meal Replacement Products Market Trends and Insights

North America leads the global meal replacement products market, commanding approximately 43% of total market share in 2025. The region’s dominance is underpinned by high consumer health literacy, a well-established dietary supplement industry, and a robust regulatory framework governed by the U.S. Food and Drug Administration and Health Canada. The Centers for Disease Control and Prevention reports that over 70% of U.S. adults are classified as overweight or obese, creating a persistent demand for structured weight management solutions, including meal replacements. Strong pharmacy retail networks, led by CVS Health and Walgreens Boots Alliance, alongside advanced e-commerce infrastructure, ensure widespread product accessibility.

The U.S. dominates the regional market and is projected to reach approximately US$ 6.7 billion by 2026, driven by continuous product innovation and strong consumer demand. The country remains the epicentre of R&D, with companies focusing on clinically validated, clean-label formulations. Canada is witnessing steady growth, supported by regulatory clarity from Health Canada’s Natural Health Products Directorate. Additionally, increasing awareness of gut microbiome health, supported by institutions such as the National Institutes of Health, is further driving innovation and consumer engagement across the region.

Europe Meal Replacement Products Market Trends and Insights

Europe represents a significant, mature market for meal replacement products, characterized by stringent regulatory standards under EU Regulation No. 609/2013 governing foods for specific groups. Germany leads the regional market, driven by a strong culture of preventive healthcare, high consumer acceptance of functional nutrition, and a well-developed retail pharmacy network. The European Food Safety Authority (EFSA) plays a central role in validating health claims, thereby strengthening consumer trust in scientifically substantiated products. France and the UK follow as significant contributors, with France benefiting from strong functional dairy traditions and the UK witnessing growth supported by the National Health Service (NHS) endorsed dietary guidance on obesity management.

Across the region, Spain is showing promising growth driven by increasing obesity awareness campaigns led by the Spanish Agency for Food Safety and Nutrition (AESAN). Clean-label and organic formulations are strongly preferred by European consumers, with EU organic certification standards serving as important purchasing signals.

Asia Pacific Meal Replacement Products Market Trends and Insights

Asia Pacific is projected to be the fastest-growing region in the meal replacement products market during the forecast period, driven by rapid urbanization, rising disposable incomes, and growing health awareness across key economies. China represents the largest market within the region, with the National Health Commission of China reporting that overweight and obese adults now exceed 50% of the population, creating strong demand for weight management solutions. The Chinese market is further expected to expand at a CAGR of approximately 9.3% during the forecast period, supported by rapid e-commerce growth and shifting dietary preferences among urban consumers.

In India, the Food Safety and Standards Authority of India is strengthening regulatory frameworks for nutraceuticals, boosting market confidence. Japan benefits from its established FOSHU system under the Consumer Affairs Agency. ASEAN countries such as Indonesia and Vietnam are also witnessing rising demand due to growing middle-class populations and increasing fitness awareness.

Competitive Landscape

The global meal replacement products market exhibits a moderately consolidated competitive structure, with a handful of multinational corporations commanding significant market share alongside a vibrant ecosystem of regional and specialty brands. Leading players such as Nestle SA, Abbott Laboratories, Herbalife International, and Unilever Plc leverage extensive R&D capabilities, global distribution networks, and strong brand equity as key differentiators. Strategic initiatives, including product line extensions into plant-based formulations, clinical partnerships with healthcare institutions, and aggressive digital marketing strategies, are reshaping competitive dynamics. Mergers, acquisitions, and licensing agreements are increasingly common as companies seek to rapidly expand their nutritional science capabilities and geographic reach in high-growth markets.

Key Developments:

- In January 2026: Danone introduced Alpro Meal To Go, a plant-based meal replacement drink range in Europe, targeting the growing demand for convenient, on-the-go nutrition. The product focuses on delivering balanced nutrition with improved texture and satiety benefits.

- In November 2025: Zantus Lifesciences launched a low-carbohydrate meal replacement product designed to support individuals at risk of pre-diabetes, addressing rising metabolic health concerns in India.

- In May 2024, Nestlé launched Vital Pursuit, a new food line tailored for individuals using weight-loss drugs such as Ozempic and Wegovy. The brand rolled out 12 frozen meal options, including protein pasta, sandwich melts, and pizzas, formulated with higher protein content and essential nutrients such as iron, vitamin A, and potassium.

- In February 2024, Herbalife launched the GLP-1 Nutrition Companion, a product range combining food and supplements to support users of GLP-1 weight-loss medications. Featuring Classic and Vegan options it debuted in various flavors across the U.S. and Puerto Rico.

Global Meal Replacement Products Market Report – Key Insights

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 12.8 billion |

|

Current Market Value (2026) |

US$ 18.4 billion |

|

Projected Market Value (2033) |

US$ 31.3 billion |

|

CAGR (2026-2033) |

7.9% |

|

Leading Region |

North America, 43% share |

|

Dominant Product Type |

Powder, 67% share |

|

Top-ranking Source |

Plant Based, 65% |

|

Incremental Opportunity |

US$ 12.9 Bn |

Companies Covered in Meal Replacement Products Market

- Abbott Laboratories

- Blue Diamond Global Ingredients Division

- Bob's Red Mill Natural Foods

- General Mills

- Glanbia Plc

- Healthy 'N Fit International Inc.

- Herbalife International of America Inc.

- Kellogg Company

- Nestle SA

- Nutrisystem Inc.

- Unilever Plc

- KSF Acquisition Corporation

- Others

Frequently Asked Questions

The global market is estimated to be valued at US$ 18.4 billion in 2026.

The meal replacement products market is primarily driven by the rise in global prevalence of obesity and lifestyle-related diseases, as highlighted by the WHO and CDC, alongside the growing consumer preference for convenient, on-the-go nutritional solutions.

North America leads the market with a 43% share in 2025.

The key market opportunities include a significant demand for plant-based and vegan options, appealing to a wider consumer base seeking alternatives.

Major players in the meal replacement products industry include Abbott Laboratories, Blue Diamond Global Ingredients Division, Bob's Red Mill Natural Foods, and General Mills.