- Beverages

- Fluid Milk Market

Fluid Milk Market Size, Share, and Growth Forecast 2026 – 2033

Fluid Milk Market by Product Type (Whole, Reduced Fat, Low Fat), Packaging Material (Paper, Plastic, Glass), Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores), and Regional Analysis, 2026 – 2033

Fluid Milk Market Size and Trends Analysis

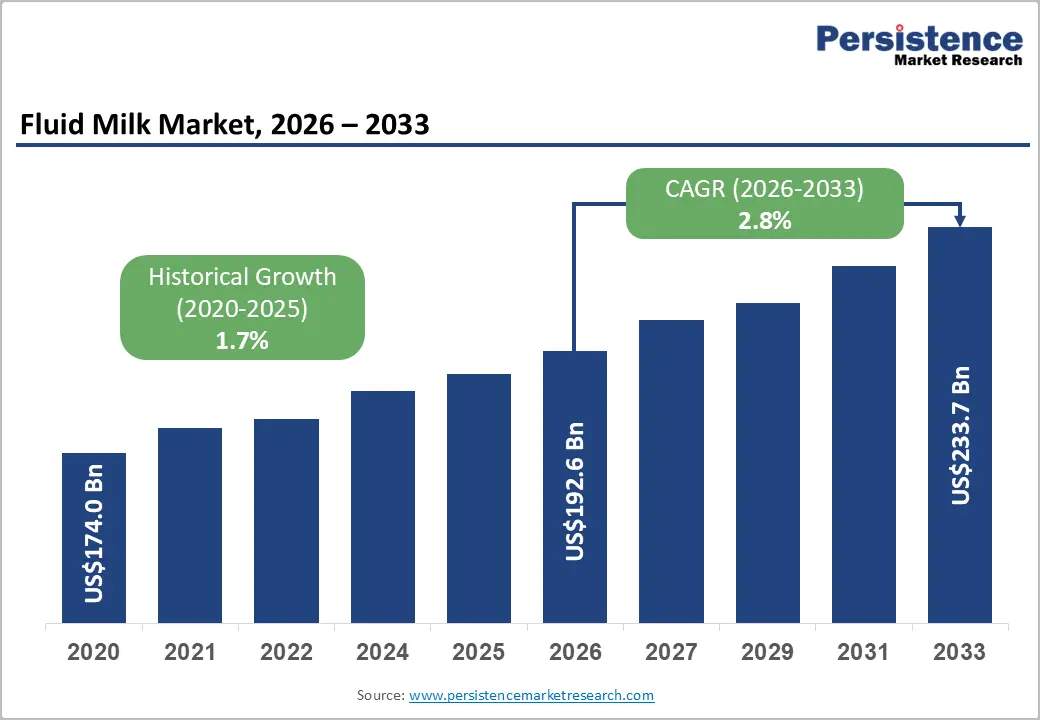

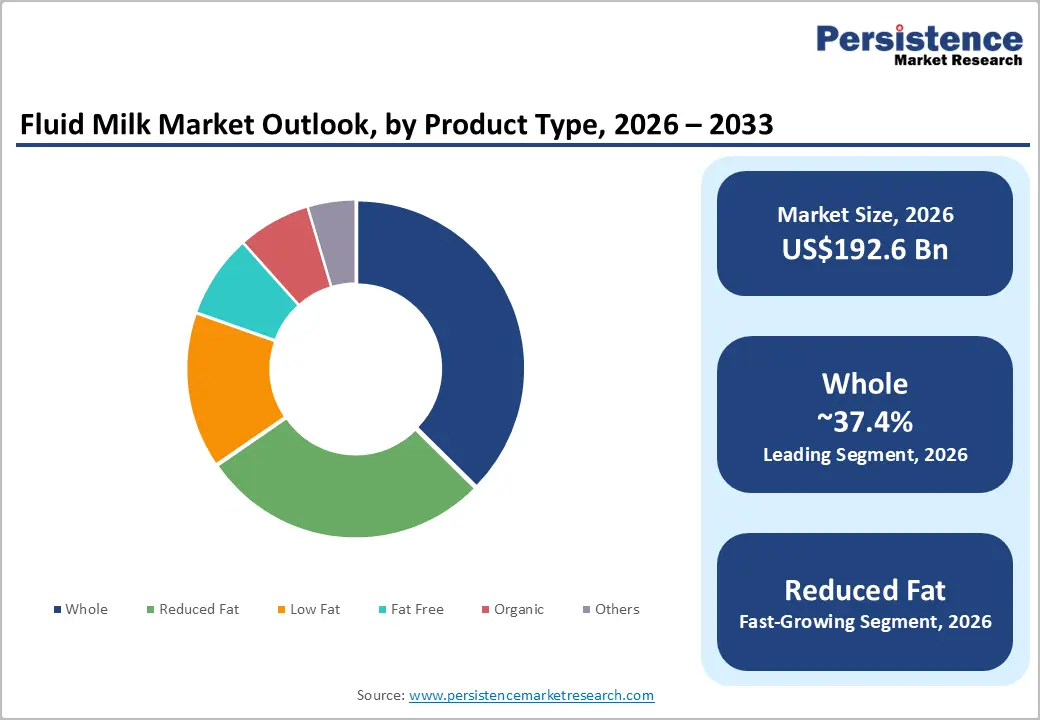

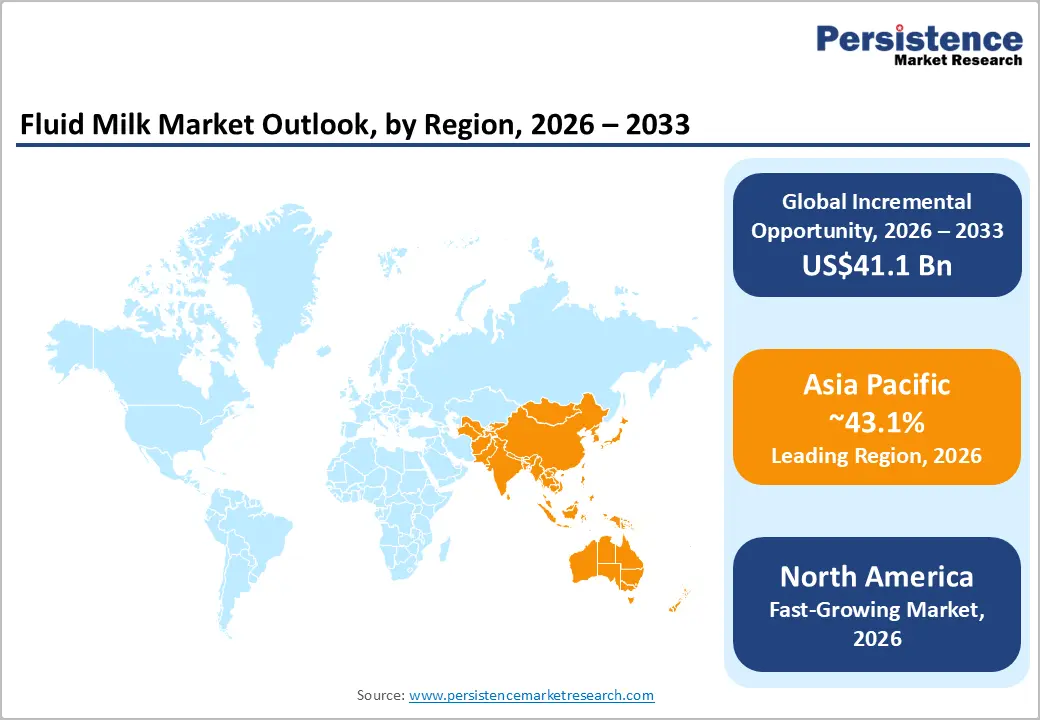

The global fluid milk market size is likely to be valued at US$192.6 billion in 2026 and is expected to reach US$233.7 billion by 2033, growing at a CAGR of 2.8% during the forecast period from 2026 to 2033, driven by rising demand for protein-rich and nutrient-dense beverages across both developed and emerging markets.

Increasing consumer preference for natural and minimally processed dairy products is also supporting the growth of fluid milk consumption.

Key Industry Highlights:

- Leading Product Type: Whole milk, approximately 37.4% share in 2026, as consumers now perceive whole milk as a natural and less processed dairy option.

- Dominant Packaging Material: Paper, nearly 42.1% in 2026, as it provides excellent product protection and supports long shelf life.

- Leading Region: Asia Pacific, with about a 43.1% share in 2026, due to superior dairy consumption traditions in countries such as India and China.

- Fast-growing Region: North America, owing to rising consumer preference for high-protein, lactose-free, organic, and value-added milk products.

- Packaging Innovation: In June 2026, Mother Dairy launched India’s first naturally degradable milk pouches for its cow milk variant. The degradable pouches decompose naturally in soil without leaving behind microplastics.

DRO Analysis

Driver - Increasing Demand for Minimally Processed Nutrient Sources

Fluid milk is regaining consumer attention as a clean and whole-food source of nutrition. Surveys from the International Food Information Council (IFIC) show that Americans are drinking more milk as they view it as an affordable protein powerhouse. Milk is minimally processed and inherently nutritious. Pasteurization makes it safe without affecting its natural nutrient profile, which includes 13 essential nutrients such as calcium and vitamin D. This perception complies well with the current ‘back to basics’ approach to food.

The U.S. Dietary Guidelines for Americans 2020 to 2025 recommend consuming 2 to 3 cup equivalents of dairy per day, depending on age, gender, and physical activity level. This official backing strengthens milk's credibility as a daily dietary staple. Research published in BMC Nutrition found that dairy consumers had calcium intakes 137.8% higher and vitamin D intakes 59.4% higher than non-consumers. It is a compelling data point that brands are actively utilizing in their marketing.

Rising Demand for Premium and Organic Beverages

Rather than a broad-based recovery, fluid milk's recent growth is concentrated in premium and organic segments. Total fluid milk sales increased in 2024 by 0.5% relative to 2023, according to the U.S. Department of Agriculture’s (USDA) Agricultural Marketing Service, the first category increase since 2009. The growth was augmented by organic, whole, and other fluid milk sales, as consumers moved away from low- and no-fat options.

Organic milk rose nearly 7% versus 2023, totaling 3 billion pounds. Whole milk, in particular, is changing the category. Whole milk's share of total fluid milk sales has grown to 37%, up from 28% a decade ago, while reduced-fat, low-fat, and non-fat varieties each lost about 5% of market share since 2015. This shift shows that consumers are choosing quality and fat content over calorie reduction. It is a trend that is actively sustaining the category against long-term volume declines.

Restraint - Lactose Intolerance to be a Key Barrier

The inability to digest lactose remains one of the most persistent biological barriers to fluid milk consumption. According to StatPearls (NCBI), 65% to 70% of the global population exhibits lactose intolerance, most commonly in its primary form, though not all individuals are symptomatic. The condition results from declining lactase enzyme activity after childhood, which is a natural biological process and not a disorder. Its prevalence is sharply uneven across ethnicities.

Rates range from less than 10% in Northern Europe to as high as 95% in parts of Asia and Africa. This creates a structural ceiling for fluid milk penetration in large and fast-growing markets across Asia Pacific and sub-Saharan Africa. Symptoms, including bloating, gas, and diarrhea, often push affected consumers toward plant-based alternatives. U.S. dairy processors have begun eliminating lactose from fluid milk after identifying lactose sensitivity as a key reason why several consumers left the dairy milk category. However, lactose-free options carry a price premium, limiting their reach in price-sensitive markets.

Opportunity - Brands to Enrich Fluid Milk with Functional Ingredients

Fluid milk's inherent nutrition gives brands a strong foundation to build on. Protein claims are now the key claim in recent dairy drink launches across North America, Latin America, Europe, and Asia Pacific. Other standout claims include digestive/gut health, probiotics, and vitamin/mineral fortification. Brands are responding with measurable product upgrades. Ultrafiltered milk, which packs 50% more protein and 50% less sugar than regular milk while being lactose-free, forms just 7% of the total milk dollars but is pushing steady growth, with dollar sales up 14.8% and unit sales up 5.5% in the last reported year, as per the latest report.

Coca-Cola's Fairlife brand is the most prominent example of this working at scale. Fairlife went from an estimated US$90 million in sales in 2015 to crossing the US$1 billion mark. A new factory in New York is under construction to support continued demand. In 2024, Danone also fortified 100% of its kids' dairy portfolio with vital nutrients, including vitamin D and B6.

Launch of Flavored and Specialty Variants to Attract Youngsters

Flavored and specialty milks are helping the category win back younger consumers and convenience-driven adults. The USDA sales data for November 2025 show flavored whole milk volumes up 13.4% from the prior year, significantly outpacing plain whole milk growth of 1.3% in the same period. For the first half of 2025, flavored whole milk was gaining traction, with whole milk representing 42% of all conventional fluid milk sales and 55% of organic fluid milk sales.

Fairlife's YUP! line, which is available in chocolate, vanilla, and strawberry, delivers 16g of protein with 25% less sugar than standard flavored milk, thereby targeting on-the-go nutrition. Beyond standard fortification, some brands are now featuring bioactives such as lactoferrin, immunoglobulins, and glycomacropeptides in unique dairy drinks targeting gut and brain health. These specialty formats allow producers to command premium price points while making fluid milk relevant to a wide and younger demographic.

Category-wise Analysis

Product Type Insights

Whole milk is predicted to lead with a share of approximately 37.4% in 2026, as consumer attitudes toward dairy fat have changed significantly over the past decade. Earlier, many consumers preferred low-fat or skim milk due to concerns about saturated fat. However, new nutrition research has questioned whether full-fat dairy is as harmful as previously believed. Studies have shown that whole milk can improve satiety, helping people feel full for longer periods. Hence, several consumers now view whole milk as a less processed and more natural option.

Reduced-fat milk is estimated to be the fastest-growing segment over the forecast period, as it provides a middle ground between nutrition and calorie management. Several consumers still want to limit fat intake but are unwilling to sacrifice taste completely by switching to skim milk. Reduced-fat milk provides a balance, making it attractive to families, older adults, and health-conscious consumers. The product is also benefiting from increasing awareness of lifestyle diseases such as obesity, diabetes, and cardiovascular disorders.

Packaging Material Insights

The paper segment is anticipated to dominate with a share of nearly 42.1% in 2026, as they provide an effective combination of product protection, sustainability, and cost-efficiency. Beverage cartons are widely used for both fresh and UHT milk as they protect milk from light and oxygen, helping preserve taste and nutritional quality while extending shelf life. This is mainly important for long-life milk products distributed across large geographic regions.

The plastic segment is expected to remain in the second position in 2026, as it delivers practical advantages that remain difficult to replace in multiple milk distribution systems. High-density polyethylene (HDPE) bottles and plastic pouches are lightweight, durable, and resistant to breakage. These features reduce transportation losses and make handling easier throughout the dairy supply chain. Plastic is particularly important in emerging economies where affordability is a prominent purchasing factor.

Regional Insights

Asia Pacific Fluid Milk Market Trends

Asia Pacific is anticipated to dominate in 2026 with a share of nearly 43.1%, owing to India's high liquid milk consumption and China's stronghold on UHT processing. The region benefits from a mix of structural factors, including a large and youthful population, rising disposable income, ongoing urbanization, and surging awareness of dairy's nutritional value. Government-backed dairy programs in both India and China have further strengthened supply chains and processing infrastructure.

India Fluid Milk Market Trends

In 2026, India is predicted to remain at the forefront with a share of around 36.9%, fueled by rising population and economic growth. For a largely vegetarian population, milk is one of the most important protein sources, which makes demand relatively inelastic. The National Dairy Development Board (NDDB) emphasizes milk as a key component for fighting malnutrition, and reports show milk remains a prominent source of nutrition for over 800 million local households.

The government's National Dairy Plan and National Program for Dairy Development (NPDD) are actively modernizing cold chain and processing infrastructure. Milk production is projected to see superior growth of 3.6% per annum between 2025 and 2034 as the national herd surges and efficiencies improve, the highest production growth rate globally, as per the Organization for Economic Co-operation and Development (OECD).

China Fluid Milk Market Trends

China is estimated to account for approximately 23.2% in 2026. Data from the country’s National Bureau of Statistics show that raw milk production in 2024 increased by 31.6% compared to 2018, while per capita dairy consumption grew by only 3.3% over the same period. It created a situation of oversupply in the industry. Despite this, premiumization is providing a floor for value growth. The UHT milk market is stable, especially in big cities.

In 2024, although raw milk prices tumbled, UHT milk prices remained stable. High-end UHT milk, including A2 or organic milk, continues to remain popular. The market is also shifting from volume to value. The China dairy market is transitioning from basic UHT milk toward value-added products such as lactose-free milk, high-protein Greek yogurts, and grass-fed organic products.

North America Fluid Milk Market Trends

North America is predicted to be the fastest-growing region in 2026 with a share of approximately 22.6%. This is attributed to a protein culture that has fully penetrated mainstream dairy. Increasing consumer sophistication in health and wellness, high demand for functional food and sports nutrition products, and a booming market for clean-label and natural ingredients are also spurring growth. Protein has moved from being an athlete's concern to a mainstream dietary priority. Fluid milk is benefiting directly. Brands such as Fairlife and Darigold's ‘Fit’ have captured this shift.

U.S. Fluid Milk Market Trends

The U.S. will likely see steady growth over the forecast period and account for a share of approximately 55.2% in 2026. Whole milk, which once seemed in permanent decline, has firmly re-established itself in the country. According to the USDA Economic Research Service, whole milk accounted for 39% of U.S. fluid milk sales in 2024, up from just 26% in 2012. This shift showcases changing consumer perceptions regarding dairy fat. The market is also benefiting from surging interest in protein-rich foods and beverages. Milk is now being positioned as an affordable source of complete protein, calcium, vitamin D, and other nutrients.

Europe Fluid Milk Market Trends

Europe will likely see decent growth over the forecast period, with a share of nearly 14.3% in 2026. According to the European Commission, the EU School Scheme allocated funding exclusively for milk distribution during the 2023 to 2024 academic year, serving millions of children across the bloc. The U.K. continues its independent School Milk Scheme, reaching hundreds of thousands of children daily, based on data from the Department for Environment, Food and Rural Affairs. These programs create a stable consumption baseline from childhood. On the innovation side, fortified and functional dairy is gaining momentum.

Germany Fluid Milk Market Trends

Germany, being the most prominent milk producer in Europe, is estimated to record a share of nearly 37.6% in 2026. One of the key growth drivers is the country's surging preference for organic and locally sourced dairy. Germany has a well-established organic dairy network, with approximately 12,000 certified organic dairy farms supplying most of the domestic demand. Consumers increasingly associate organic milk with animal welfare, sustainability, and product quality. This trend is encouraging retailers such as Aldi, Lidl, Edeka, and Rewe to extend their organic milk portfolios, creating new opportunities for fluid milk manufacturers.

U.K. Fluid Milk Market Trends

In 2026, the U.K. is expected to account for a share of around 15.2%, as it is entering a period of quality-focused growth. This is attributed to increasing consumer demand for protein-rich, functional, and lactose-free dairy products. Although traditional milk consumption remains relatively mature, dairy milk has recently regained momentum as consumers seek natural and nutrient-dense beverages. The rising focus on protein intake, weight management, and healthy aging is creating new opportunities for premium milk products across the country.

Competitive Landscape

The global fluid milk market is moderately fragmented, with a mix of multinational dairy processors, regional cooperatives, and local fresh milk suppliers competing across different geographies. Key players such as Lactalis, Danone, Nestlé, Arla Foods, Fonterra, Yili Group, and Mengniu Dairy hold dominant positions. Regional brands continue to command substantial market share due to consumers' preference for locally sourced fresh milk and established dairy distribution networks. The top ten companies collectively account for less than half of the global market, preventing excessive concentration.

Competition is now shifting from commodity milk toward value-added fluid milk products such as lactose-free milk, A2 milk, fortified milk, high-protein milk, and organic milk. Companies are investing heavily in product differentiation, traceability systems, and premium positioning rather than competing solely on price. In markets such as China and India, local players continue to challenge multinational firms by using extensive procurement networks and adapting products to regional tastes.

Key Industry Developments:

- In June 2026, Purabi Dairy, one of the most prominent dairy cooperatives in Assam, India, unveiled Purabi Gold, a full cream variant of milk, just ahead of Rongali Bihu. The one-liter pack contains 6% fat and 9% Solids-Not-Fat (SNF).

- In May 2026, Maola Local Dairies launched Strawberry Whole Milk, broadening its flavored dairy portfolio to capture high consumer demand for indulgent yet authentic products. The launch points to a broad trend toward value-added milk products that combine taste, nutrition, and familiarity.

- In March 2026, regulators approved Fonterra's sale of its consumer and associated businesses, collectively known as Mainland Group, to Lactalis, in a deal valued at approximately US$2.5 billion. The deal strengthened Lactalis' position as the dominant global dairy company by turnover and marked a strategic pivot for Fonterra toward its core B2B ingredients business.

Companies Covered in Fluid Milk Market

- Amul (GCMMF)

- Arla Foods amba

Dairy Farmers of America, Inc. - Fonterra Co-operative Group Limited

- Lactalis International, Landliebe (Theo Müller Group)

- Meiji Holdings Co., Ltd.

- Nestle S.A.

- Saputo Inc.

- Yili Group

- Others

Frequently Asked Questions

The global fluid milk market is projected to be valued at US$192.6 billion in 2026.

The fluid milk market is expected to reach US$233.7 billion by 2033.

Key market trends include rising demand for lactose-free milk and the launch of premium value-added milk.

Whole milk is expected to be the leading product type with a share of nearly 37.4% in 2026, as recent nutritional research has improved consumer confidence in dairy fat.

The fluid milk market is expected to grow at a CAGR of 2.8% from 2026 to 2033.

Amul (GCMMF), Arla Foods amba, and Dairy Farmers of America, Inc. are a few key market players.