- Medical Devices

- Endocrine Testing Market

Endocrine Testing Market Size, Share, and Growth Forecast, 2026 - 2033

Endocrine Testing Market by Test Type (Testosterone Test, Estradiol Test, Thyroid Stimulating Hormone (TSH) Test, Prolactin Test, Others), Technology (Tandem Mass Spectrometry, Immunoassay, Others), End-User (Hospitals, Diagnostic Laboratories, Others), and Regional Analysis for 2026 - 2033

Endocrine Testing Market Size and Trends Analysis

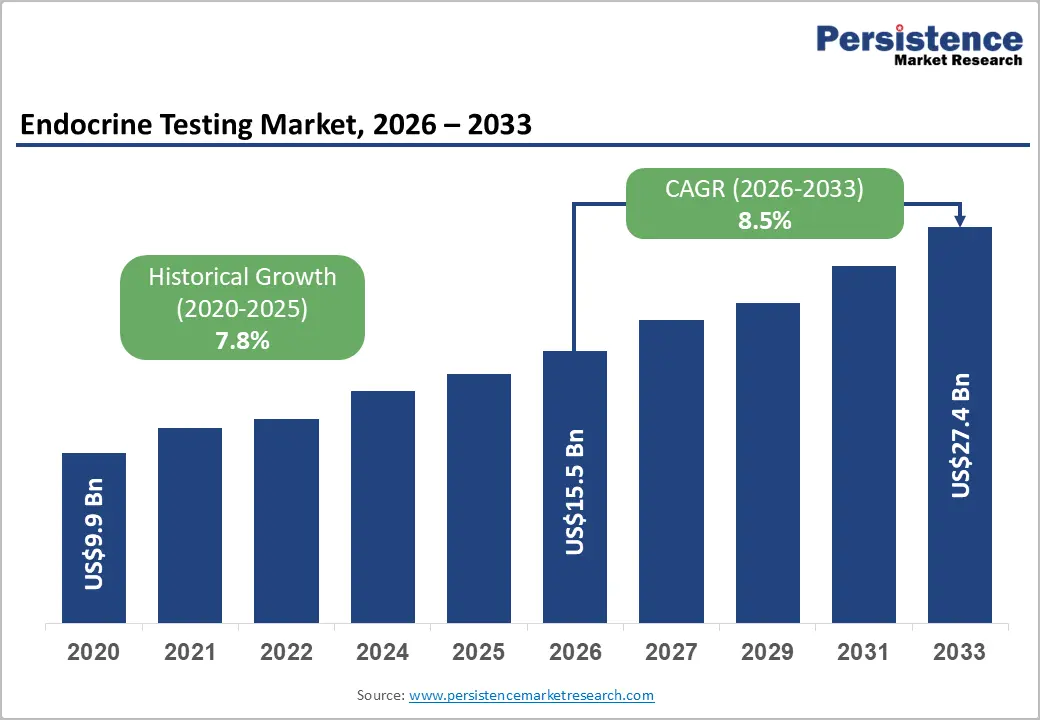

The global endocrine testing market size is likely to be valued at US$15.5 billion in 2026 and is estimated to reach US$27.4 billion by 2033, growing at a CAGR of 8.5% during the forecast period 2026 - 2033, driven by demographic expansion of aging populations, rising burden of metabolic disorders, increasing regulatory focus on early disease detection, wider adoption of automated laboratory platforms, and expansion of diagnostic infrastructure in emerging economies.

Growth momentum is supported by higher clinical demand for hormone profiling linked to thyroid disorders, fertility evaluation, and diabetes monitoring. Regulatory screening programs are expanding testing frequency across primary care settings. Technology adoption is improving assay sensitivity and turnaround time.

Key Industry Highlights:

- Leading Test Type: The TSH test is set to hold around 28% revenue share in 2026, driven by the integration of thyroid screening into routine preventive health checkup protocols across hospital and primary care settings.

- Fastest-Growing Test Type: The human chorionic gonadotropin (hCG) hormone test is projected as the fastest-growing segment, supported by rising global IVF procedure volumes and expanded fertility clinic infrastructure.

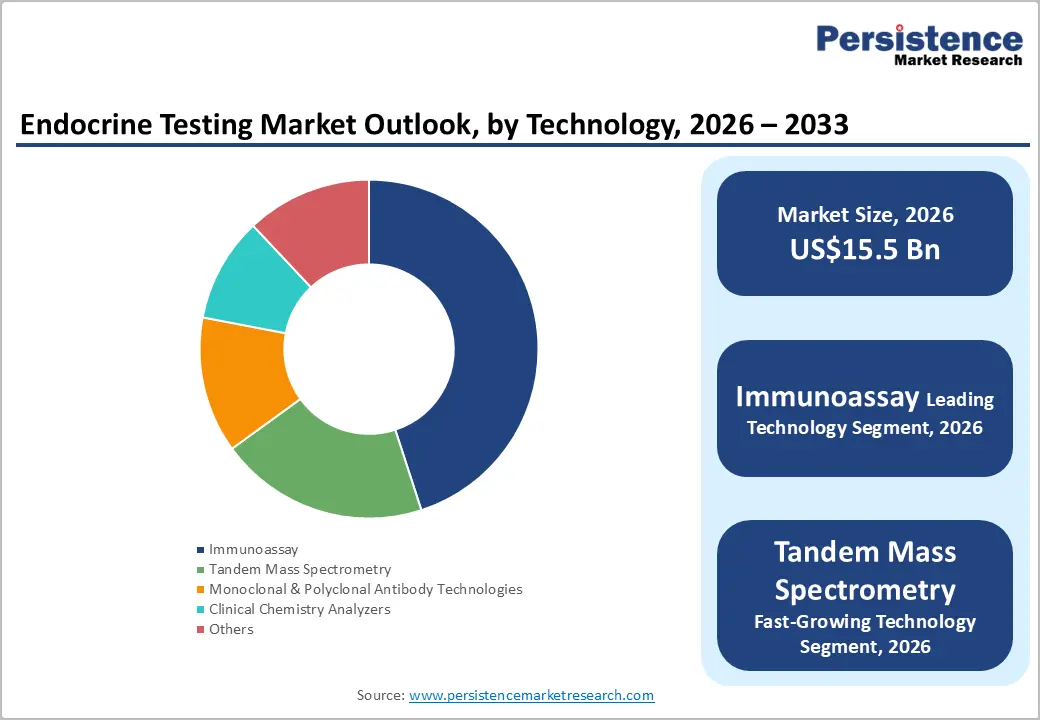

- Leading Technology: Immunoassay is estimated to hold roughly a 45% revenue share in 2026, due to broad clinical validation, high-throughput analyzer compatibility, and established reimbursement coverage across major markets.

- Fastest-growing Technology: Tandem mass spectrometry is forecast to record the fastest growth, driven by superior analytical specificity for steroid hormone quantification in pediatric, female, and complex clinical populations.

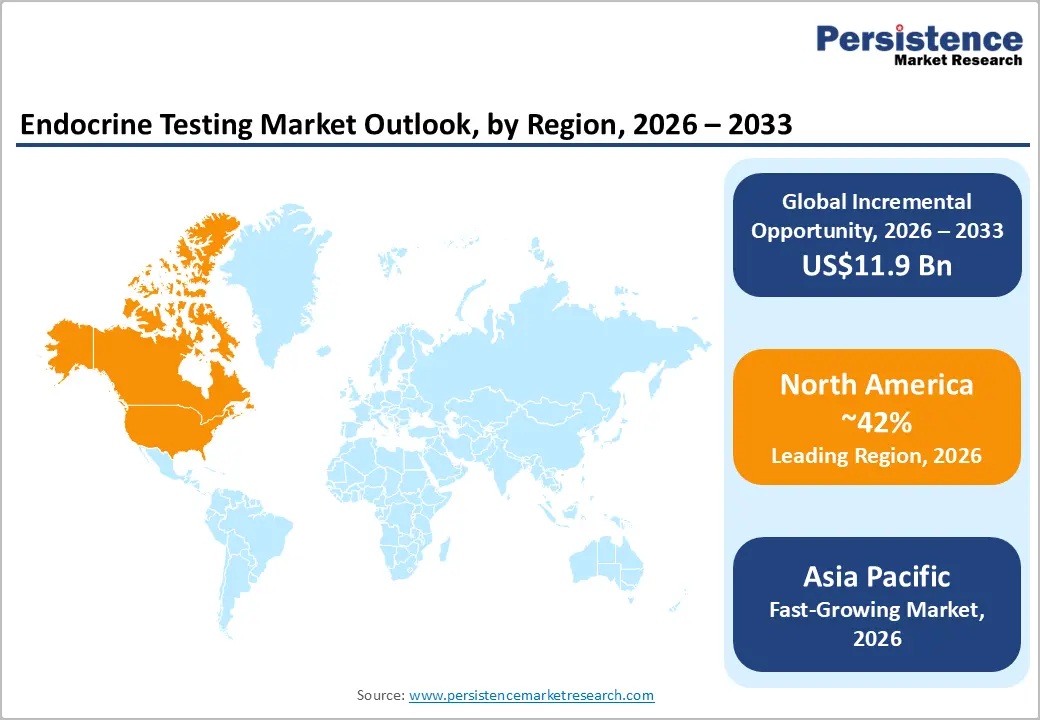

- Regional Leadership: North America is projected to capture roughly 42% of the market share by 2026, while Asia Pacific is forecast to record the fastest growth due to expanding private hospital networks.

- Competitive Environment: The market reflects a moderately consolidated structure, with key players such as Abbott Laboratories and Roche Diagnostics leveraging broad product portfolios, regulatory certifications, and global distribution infrastructure to maintain competitive positioning.

- Innovation Trends: Advancements in high-sensitivity immunoassay formats, AI-integrated hormonal biomarker interpretation platforms, and the commercialization of direct-to-consumer home testing kits are shaping long-term market evolution and attracting sustained investment toward precision endocrine diagnostics.

DRO Analysis

Driver- Rising Prevalence of Endocrine and Metabolic Disorders

The increasing incidence of diabetes, thyroid dysfunction, and reproductive hormone imbalance is expanding clinical testing volume across hospitals and diagnostic laboratories. Rising awareness of early detection protocols is strengthening demand for hormone-based diagnostic panels. Integration of screening guidelines in primary care is increasing test penetration across routine health evaluations.

According to CDC 2025 data, More than 40 million individuals in the United States are affected by diabetes, increasing demand for insulin and related hormone testing workflows in clinical diagnostics. Higher disease burden is increasing longitudinal monitoring requirements across patient populations. Hospitals are expanding endocrine panels to support chronic disease management programs and preventive screening frameworks.

Restraint - High Dependency on Skilled Laboratory Infrastructure

The market shows constrained scalability due to reliance on skilled laboratory infrastructure. Advanced diagnostic platforms, calibrated instrumentation, and specialized technical workforce define entry barriers for new facilities. Limited availability of trained laboratory professionals reduces processing capacity and slows diagnostic workflows. Complex hormonal assays require strict quality control, increasing operational burden and restricting expansion across decentralized healthcare settings.

Operational reliance on highly skilled laboratory environments constrains the scalability of diagnostic services and limits regional access to hormone analysis workflows. Complex assay procedures demand continuous calibration, maintenance, and stringent quality oversight by trained specialists. Workforce constraints reduce testing frequency and extend turnaround cycles for endocrine evaluation processes.

Opportunity - Expansion of Point-of-Care Endocrine Testing

Development of portable immunoassay systems is enabling decentralized hormone testing in outpatient and home-based environments. Integration of microfluidic technologies is reducing dependency on centralized laboratories. Diagnostic accessibility is improving across rural healthcare networks.

Point-of-care adoption is increasing the early detection of thyroid and fertility disorders. Healthcare providers are integrating rapid endocrine panels into primary care workflows to reduce diagnostic delays. Policy support for decentralized diagnostics is encouraging the adoption of compact analyzers. Manufacturers are investing in cartridge-based systems to enable scalable testing across non-laboratory environments.

Category-wise Analysis

Test Type Insights

The thyroid-stimulating hormone (TSH) test is anticipated to secure around 28% of the endocrine testing market share in 2026, reflecting the high global burden of thyroid disorders and the routine inclusion of TSH screening in annual health checkup panels. Quest Diagnostics in the United States processes millions of TSH tests annually as part of both clinical referral and preventive screening protocols. The clinical necessity of thyroid monitoring in pregnant women, elderly patients, and those on thyroid replacement therapy sustains consistent demand across all end-user categories.

The human chorionic gonadotropin (hCG) hormone test is expected to be the fastest-growing segment, propelled by rising demand for pregnancy confirmation, fertility treatment monitoring, and early gestational complication detection. Roche Diagnostics has expanded its Elecsys hCG assay portfolio to include ultrasensitive variants suited for assisted reproductive technology (ART) protocols.

Technology Insights

Immunoassay platforms are poised to dominate with a forecast market share of over 45% in 2026, powered by their established clinical validation, broad analyzer compatibility, and cost-effectiveness relative to chromatography-based alternatives. Abbott Laboratories offers its ARCHITECT immunoassay platform across a comprehensive endocrine panel that includes thyroid, reproductive, and metabolic hormones. The scalability of immunoassay systems for high-throughput laboratory environments reinforces their dominant position within hospital and reference laboratory settings.

Tandem mass spectrometry is estimated to be the fastest-growing segment, fueled by its superior analytical specificity in measuring steroids, thyroid hormones, and catecholamines at low concentrations where immunoassay cross-reactivity presents clinical limitations. ARUP Laboratories has deployed LC-MS/MS platforms as the reference methodology for testosterone quantification in pediatric and female patient populations. Increasing clinical awareness of immunoassay interference issues, combined with declining instrument costs, is accelerating the transition to mass spectrometry in specialized endocrine testing workflows.

End-user Insights

Hospitals are likely to be the leading segment with a projected 38% of the endocrine testing market share in 2026 due to their role as the primary diagnostic and treatment hub for complex endocrine conditions requiring integrated testing and specialist consultation. Cleveland Clinic operates dedicated endocrine testing pathways within its laboratory medicine division, processing thyroid, adrenal, and reproductive hormone panels for both inpatient and outpatient populations. The availability of advanced analyzer infrastructure within hospital laboratory settings enables high-volume testing with rapid turnaround times.

Home-based tests are anticipated to be the fastest-growing segment, fueled by accelerating consumer demand for accessible hormonal health monitoring, supported by direct-to-consumer regulatory approvals and the expansion of digital health ecosystems. LetsGetChecked and Everlywell have commercially deployed home-based thyroid and reproductive hormone test kits in the United States and European markets. Increasing consumer health awareness and the normalization of self-directed diagnostics within the broader telehealth framework are structurally expanding the home-based testing addressable market.

Regional Insights

North America Endocrine Testing Market Trends

North America is expected to lead with an estimated 42% of the market share in 2026, supported by high healthcare spending, comprehensive reimbursement frameworks, and a dense concentration of reference laboratories. Advanced clinical testing infrastructure across the region allows rapid adoption of newly cleared diagnostic systems.

U.S. Endocrine Testing Market Insights

The U.S. is anticipated to secure approximately 84% of the regional market share in 2026, driven by rising clinical tracking of chronic metabolic conditions. Healthcare providers focus heavily on early identification of pre-diabetic states, utilizing automated testing systems to manage heavy daily testing volumes across commercial laboratory networks such as Labcorp and Quest Diagnostics.

Canada Endocrine Testing Market Insights

Canada is forecast to account for around 16% of the regional market share in 2026, stimulated by sustained demand from provincial health insurance expansions for senior wellness screenings. Institutional focus on universal preventative care models prompts consistent provincial laboratory investments in high-throughput clinical chemistry analyzers, reducing wait times for diagnostic results.

Europe Endocrine Testing Market Trends

Europe is projected to hold roughly 28% of the market share in 2026, driven by structured national healthcare systems and centralized laboratory models. National health frameworks prioritize long-term preventative health, forcing large-scale implementation of automated hormone screening protocols across public networks.

Germany Endocrine Testing Market Insights

Germany is likely to command about 24% of the European market share in 2026, maintained through high integration of laboratory automation solutions. Large laboratory clusters utilize advanced liquid chromatography coupled with mass spectrometry to handle routine endocrine screening requests originating from primary care networks.

U.K. Endocrine Testing Market Insights

The U.K. is expected to capture nearly 19% of the Europe market share in 2026, propelled by volume growth from National Health Service (NHS) modernization initiatives. Centralized laboratory hub procurement strategies favor long-term reagent contract models, reducing individual testing costs while securing automated immunoassay platform installations.

Asia Pacific Endocrine Testing Market Trends

Asia Pacific is forecast to be the fastest-growing market for endocrine testing, stimulated by expanding private hospital networks, rising disposable incomes, and accelerating public health infrastructure spending. Urbanizing populations face shifting lifestyle profiles, resulting in rapid escalation of diabetes and thyroid disorder presentations.

China Endocrine Testing Market Insights

China is projected to secure around 35% of the regional market share in 2026, accelerated by government-led health access initiatives and localized manufacturing mandates. Regional healthcare expansions increase overall diagnostic equipment installation rates across rural township hospitals, boosting regular consumable test kit utilization.

Japan Endocrine Testing Market Insights

Japan is likely to represent approximately 22% of the regional market share in 2026, sustained by consistent volume expansion from a rapidly aging demographic profile. Increasing clinical focus on age-related endocrine imbalances, such as late-onset hypogonadism and postmenopausal osteoporosis, maintains high demand for specialized reproductive hormone assays.

Competitive Landscape

The global endocrine testing market is moderately consolidated, with a core group of multinational diagnostics companies controlling a majority of revenue through broad product portfolios, established distribution networks, and long-term supply agreements with hospital and laboratory systems. Abbott Laboratories, Roche Diagnostics, Siemens Healthineers, Becton Dickinson, and bioMérieux collectively hold a dominant share of global immunoassay-based endocrine testing revenue.

Market concentration is maintained through the high capital requirements associated with reagent manufacturing, analyzer development, and regulatory compliance, which create meaningful barriers to entry for new participants. Smaller specialized manufacturers compete in niche segments such as mass spectrometry consumables, fertility-focused panels, and direct-to-consumer testing formats, where differentiation based on clinical specificity or consumer accessibility can create sustainable competitive positions.

Key Industry Developments:

- In May 2026, Revvity received United States Food and Drug Administration clearance for its total testosterone assay, strengthening its automated endocrine testing portfolio and expanding comprehensive hormone testing capabilities in clinical diagnostics.

- In December 2025, bioMérieux highlighted its VIDAS Equine Insulin and ACTH assay portfolio, strengthening veterinary endocrine testing capabilities and improving diagnostic support for equine metabolic and adrenal disorders.

Companies Covered in Endocrine Testing Market

- Abbott Laboratories

- Roche Diagnostics

- Siemens Healthineers

- Becton, Dickinson and Company

- bioMérieux SA

- Thermo Fisher Scientific

- Ortho Clinical Diagnostics

- DiaSorin S.p.A.

- Randox Laboratories

- Mindray Medical International

- Snibe Diagnostics

- Transasia Bio-Medicals

- Tosoh Corporation

- Luminex Corporation (DiaSorin)

- Hologic Inc.

Frequently Asked Questions

The global endocrine testing market is projected to reach US$15.5 billion in 2026.

The endocrine testing market is driven by rising prevalence of hormonal disorders such as diabetes and thyroid diseases, increasing adoption of preventive screening programs, and rapid expansion of automated diagnostic laboratory infrastructure.

The endocrine testing market is poised to witness a CAGR of 8.5% from 2026 to 2033.

Key market opportunities include expansion of point-of-care endocrine diagnostics, adoption of precision hormone testing using mass spectrometry, and increasing integration of automated laboratory systems across emerging healthcare networks.

Some of the key market players include Abbott Laboratories, Roche Diagnostics, Siemens Healthineers, Becton Dickinson, and bioMérieux.