- Medical Devices

- Electrophysiology Ablation Market

Electrophysiology Ablation Market Size, Share, and Growth Forecast, 2026 - 2033

Electrophysiology Ablation Market by Product Type (Ablation Catheters, Mapping & Navigation Systems, Others), Procedure Type (Catheter-based Ablation, Surgical/Hybrid Ablation), Indication, Technology, and Regional Analysis for 2026 - 2033

Electrophysiology Ablation Market Size and Trends Analysis

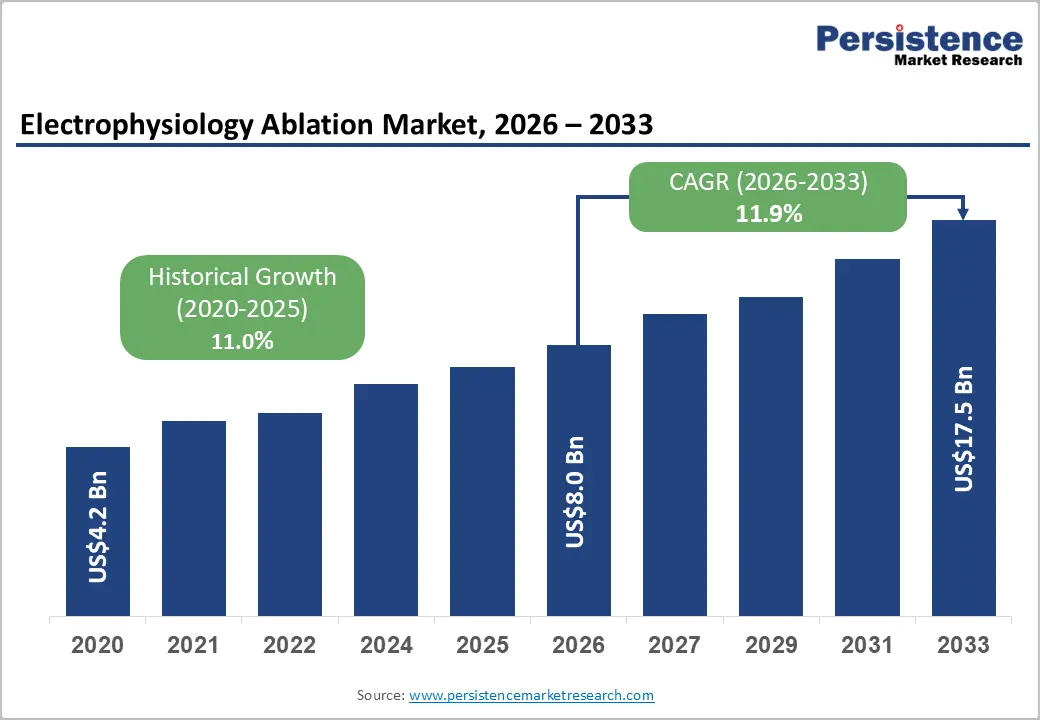

The global electrophysiology ablation market size is likely to be valued at US$ 8.0 billion in 2026, and is expected to reach US$ 17.5 billion by 2033, growing at a CAGR of 11.9% during the forecast period from 2026 to 2033, driven by the rising global incidence of atrial fibrillation, significant technological advancements in pulsed field ablation, increasing endorsement of catheter-based rhythm control strategies by leading cardiology associations, and the ongoing expansion of catheterization laboratory infrastructure across rapidly developing emerging economies.

Key Industry Highlights:

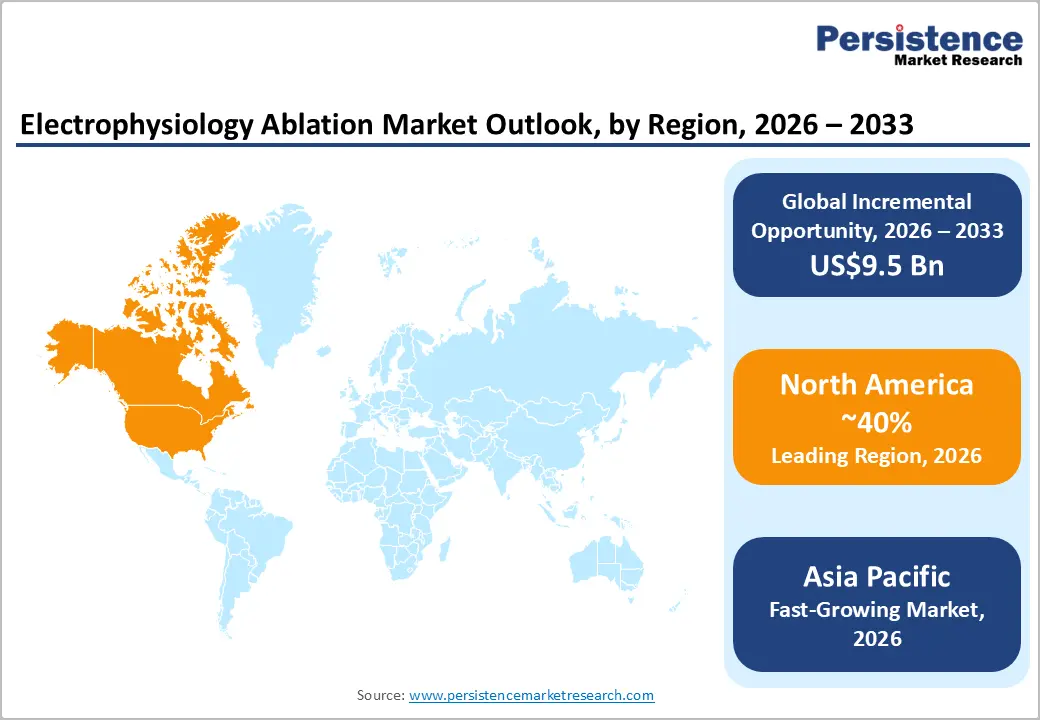

- Dominant Region: North America is projected to dominate with 40% revenue share, supported by high procedural volumes, premium reimbursement, and headquarters concentration of leading EP device companies.

- Fastest-growing Region: Asia Pacific is expected to be the fastest-growing, driven by Atrial fibrillation (AF) burden growth in China and India, expanding cath lab infrastructure, and government-backed cardiac care programs.

- Leading Product Type: Ablation catheters are the leading product segment, holding approximately 42% of the global market revenue, driven by rising AF ablation procedure volumes and next-generation catheter innovation.

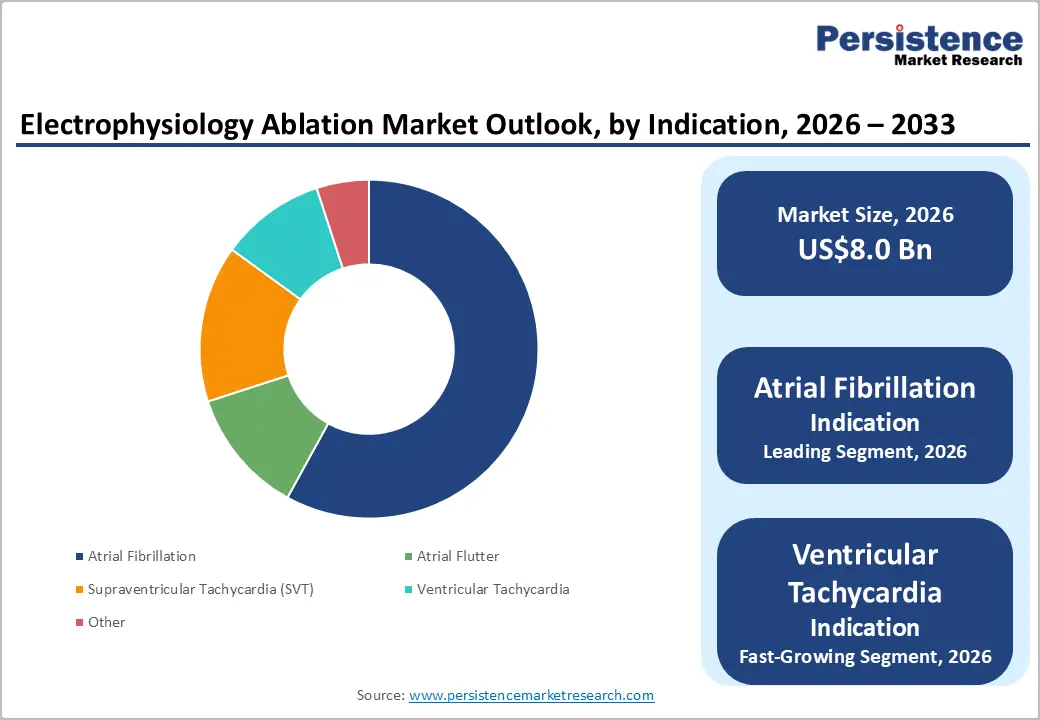

- Dominant Indication: Atrial fibrillation (AF) dominates by indication with 55% market share, underpinned by a global AF patient population exceeding 59 million and expanding rhythm-control guideline adoption

- In May 2023, Abbott got FDA approval of its TactiFlex Ablation Catheter, Sensor Enabled, and an atrial fibrillation treatment device. The device enhances safety in the procedures and saves time in treatment as compared to the previous models of the catheters.

DRO Analysis

Driver - Pulsed Field Ablation Technology Disruption

The commercial launch of pulsed field ablation (PFA) systems has fundamentally redefined the EP ablation technology landscape. PFA delivers ultra-rapid, high-voltage electrical pulses that cause irreversible electroporation of cardiomyocyte cell membranes, achieving durable pulmonary vein isolation (PVI) while sparing adjacent non-cardiac structures, including the oesophagus, phrenic nerve, and pulmonary veins from thermal injury. This tissue-selectivity profile directly addresses the most serious safety concerns associated with radiofrequency and cryoablation technologies.

The ADVENT trial, a landmark prospective randomized controlled trial published in the New England Journal of Medicine (2023), demonstrated non-inferiority of PFA versus conventional thermal ablation for AF freedom at 12 months, with a markedly improved safety profile. Boston Scientific's FARAPULSE system became the first PFA platform to receive FDA approval (January 2024) for the treatment of symptomatic paroxysmal AF, followed by Johnson & Johnson MedTech's VARIPULSE system.

Restraint - Workforce Bottleneck and Cath Lab Infrastructure Deficit

A significant challenge facing the electrophysiology (EP) ablation market is the shortage of trained electrophysiologists, EP nurses, technologists, and support staff required to perform complex cardiac ablation procedures. Training specialists takes several years, and growing patient demand for atrial fibrillation and other arrhythmia treatments is outpacing workforce expansion in many healthcare systems. This imbalance contributes to longer waiting times, scheduling delays, and reduced procedural capacity.

Many hospitals face limitations in the catheterization laboratory (cath lab) and dedicated EP lab infrastructure. Advanced ablation procedures require specialized imaging systems, 3D electroanatomical mapping platforms, and high-cost capital equipment, creating financial barriers for smaller hospitals and community healthcare centers. Limited procedure rooms and equipment availability can restrict the number of patients treated each day.

Opportunity - AI-Driven Mapping Integration and Robotic Ablation Systems

The convergence of artificial intelligence, high-density electroanatomical mapping, and robotic catheter navigation represents a transformational opportunity for the EP ablation market. AI-powered algorithms applied to ultra-high-density mapping data (from systems such as Abbott's EnSite X, Johnson & Johnson's CARTO 3, and Rhythmia HDx) are enabling automatic annotation of complex arrhythmia substrates, predictive ablation target identification, and real-time procedural guidance that reduces operator-dependent variability.

Robotic EP platforms, including Stereotaxis' Genesis RMN and Corindus' CorPath GRX (now Siemens Healthineers), are demonstrating reduced radiation exposure, improved catheter stability, and the potential for remote or semi-autonomous procedure execution. The global robotic EP market alone is forecast to grow at a CAGR exceeding 18% through 2033, presenting high-margin growth opportunities for established EP device manufacturers and digital health entrants alike.

Category-wise Analysis

Product Type Insights

Ablation catheters are expected to dominate the product type, representing approximately 42% of total market revenues. This dominance reflects the catheter's central role as the core consumable in every EP ablation procedure, driving recurring revenue per case combined with premium pricing for next-generation RF contact-force catheters, cryoballoon systems, and PFA single-shot devices.

Mapping & navigation systems represent the fastest-growing product segment. The transition from conventional fluoroscopy-guided ablation to real-time 3D electroanatomical mapping, which enables precise substrate characterization, rotor mapping, and ablation lesion confirmation, is driving system upgrades across established EP labs globally.

Procedure Type Insights

Catheter-based ablation is estimated to dominate the procedure type segment, accounting for 40% market share. Its dominance is driven by its minimally invasive nature, shorter hospital stays, lower complication rates compared to open-heart surgery, and strong clinical effectiveness in treating atrial fibrillation, atrial flutter, and other cardiac arrhythmias.

Surgical/Hybrid ablation represents the fastest-growing segment, due to its increasing use in patients with persistent or long-standing atrial fibrillation who may not achieve optimal outcomes with catheter ablation alone. Hybrid approaches combine the strengths of surgical epicardial ablation and catheter-based endocardial ablation, improving long-term rhythm control and procedural success rates.

Technology Insights

Radiofrequency (RF) ablation is anticipated to dominate technology, commanding approximately 52% of the market in 2026. RF ablation's leadership reflects decades of clinical evidence, widespread operator familiarity, a mature device ecosystem, and broad regulatory approvals across AF, AFL, SVT, and VT indications.

Pulsed Field Ablation (PFA) is expected to emerge as the fastest-growing technology segment, expanding at a rate more than twice that of the overall market. Rapid adoption is being driven by regulatory approvals across the U.S. and Europe, the publication of several landmark randomized controlled trials (RCTs), and strong commercialization efforts by major industry players such as Boston Scientific, Johnson & Johnson MedTech, and Medtronic.

Indication Insights

Atrial Fibrillation (AF) is anticipated to remain the leading indication in the global electrophysiology (EP) ablation market, contributing nearly 55% of total market revenue. The large and growing disease burden, estimated at around 59 million patients worldwide, with approximately 5 million new cases diagnosed annually, along with updated clinical guidelines from organizations such as the European Society of Cardiology, Heart Rhythm Society, and American College of Cardiology/American Heart Association recommending catheter ablation as a first-line rhythm control therapy for eligible patients, continues to reinforce AF’s dominant market position.

Ventricular Tachycardia (VT) ablation is projected to be the fastest-growing indication segment. Increasing clinical evidence from randomized trials supporting catheter ablation as an effective rhythm-control strategy for patients with structural heart disease and recurrent VT is significantly broadening the eligible patient base. This expansion extends beyond the historically treated ischemic VT population to include patients with non-ischemic cardiomyopathy substrates, thereby accelerating market growth.

Regional Insights

North America Electrophysiology Ablation Market Trends

North America is projected to dominate the market, accounting for 40% of the total market share in 2026, driven by the increasing prevalence of atrial fibrillation and other cardiac arrhythmias across the region. Rapid adoption of advanced technologies, including pulsed field ablation (PFA), AI-enabled mapping systems, and robotic-assisted navigation, is enhancing procedural efficiency and patient outcomes.

U.S. Electrophysiology Ablation Market Insights

The U.S. market remains the largest in North America, commanding 68% of the share in 2026, fueled by the high prevalence of atrial fibrillation and other cardiac arrhythmias, increasing adoption of minimally invasive procedures, and strong reimbursement support. The country is at the forefront of adopting advanced technologies such as pulsed field ablation (PFA), 3D electroanatomical mapping, and robotic-assisted navigation systems. A large network of specialized electrophysiology centers and continued investment in cardiac care infrastructure further support market growth.

Canada Electrophysiology Ablation Market Insights

Canada's electrophysiology ablation market is growing steadily due to the increasing prevalence of atrial fibrillation and other cardiac arrhythmias, particularly among the aging population. Rising adoption of catheter-based ablation procedures, supported by a well-established public healthcare system and expanding electrophysiology centers, is driving market growth. Healthcare providers are increasingly utilizing advanced mapping and ablation technologies to improve procedural outcomes and reduce hospitalizations.

Europe Electrophysiology Ablation Market Trends

Europe accounts for approximately 27% of the EP ablation market revenue, propelled by a well-established interventional cardiology infrastructure, universal healthcare coverage across major economies, and strong regulatory approval pathways through the European CE marking system. Germany, the U.K., and France are the three dominant country-level markets in Europe.

Germany Electrophysiology Ablation Market Trends

Germany is one of the leading markets in Europe, accounting for 22% of the market share in 2026, supported by its advanced healthcare infrastructure, high adoption of innovative cardiac technologies, and strong presence of specialized cardiac centers. The rising prevalence of atrial fibrillation and other arrhythmias, coupled with an aging population, is driving demand for catheter-based ablation procedures.

U.K. Electrophysiology Ablation Market Trends

The U.K. market is expected to grow steadily and holding 15% share in 2026, due to the increasing prevalence of atrial fibrillation and other cardiac arrhythmias, coupled with rising demand for minimally invasive treatment options. Expansion of electrophysiology services within the public healthcare system and investments in advanced cardiac care infrastructure are supporting procedure growth.

Asia Pacific Electrophysiology Ablation Market Trends

Asia Pacific is likely to be the fastest-growing regional market, driven by the rising prevalence of cardiac arrhythmias, the expanding elderly population, and increasing awareness of advanced cardiac treatments. Growing healthcare investments, improving access to specialized electrophysiology centers, and the expansion of catheter-based ablation services are driving market development across the region.

China Electrophysiology Ablation Market Trends

China is projected to hold the 32% of the Asia Pacific market share, and is the fastest-growing in Asia Pacific, powered by the increasing prevalence of atrial fibrillation, a rapidly aging population, and expanding access to advanced cardiac care. The country is investing heavily in healthcare infrastructure, including specialized electrophysiology centers and catheterization laboratories.

Japan Electrophysiology Ablation Market Trends

Japan is projected to account for approximately 20% of the Asia Pacific electrophysiology ablation market in 2026, supported by its rapidly aging population and the rising incidence of atrial fibrillation and other cardiac arrhythmias. The country benefits from a highly developed healthcare infrastructure and strong adoption of advanced electrophysiology technologies, including 3D mapping systems, contact-force sensing catheters, and emerging pulsed field ablation (PFA) platforms.

Competitive Landscape

The global electrophysiology ablation market is moderately concentrated, with a handful of multinational medical device companies controlling a significant portion of market revenue through extensive product portfolios, strong clinical evidence, and broad geographic reach. Competition is centered on technological innovation, particularly in pulsed field ablation (PFA), advanced 3D mapping systems, contact-force sensing catheters, and robotic navigation platforms.

Leading players are focusing on product launches, regulatory approvals, strategic acquisitions, and collaborations with hospitals and electrophysiology centers to strengthen their market positions. The rapid commercialization of next-generation PFA technologies has intensified competition, as manufacturers seek to improve procedural safety, efficiency, and clinical outcomes for atrial fibrillation treatment.

Key Industry Developments:

- In May 2025, Abbott introduced the TactiFlex sensor-enabled ablation catheter, which is a flexible-tipped device that incorporates contact force technology. This innovation improves the accuracy and safety of the procedure when ablating the heart.

- In August 2023, Biosense Webster received regulatory clearance for more advanced atrial fibrillation ablation products that would allow them to be operated as fluoroscopy-free. This decreases the radiation dose to the patient and promotes minimally invasive cardiac operations.

Companies Covered in Electrophysiology Ablation Market

- Medtronic plc

- Abbott Laboratories

- Boston Scientific Corporation

- Johnson & Johnson

- Philips Healthcare

- Siemens Healthineers

- Biotronik SE & Co. KG

- MicroPort Scientific Corporation

- Acutus Medical, Inc.

- AtriCure, Inc.

- CardioFocus, Inc.

- Stereotaxis, Inc.

- CathRx Ltd.

- Imricor Medical Systems, Inc.

- Lepu Medical Technology Co., Ltd.

- Baylis Medical Company, Inc.

Frequently Asked Questions

The global electrophysiology ablation market is projected to reach US$8.0 billion in 2026.

The rising prevalence of atrial fibrillation and other cardiac arrhythmias is driving increased demand for minimally invasive electrophysiology ablation procedures worldwide.

The electrophysiology ablation market is poised to witness a CAGR of 11.9% from 2026 to 2033.

Expanding adoption of pulsed field ablation (PFA) technology offers significant opportunities to improve procedural safety, efficiency, and treatment outcomes in cardiac arrhythmia management.

Key players include Medtronic plc, Abbott Laboratories, Boston Scientific Corporation, Johnson & Johnson MedTech, and Philips Healthcare.