- Transportation & Logistics

- Dozer Market

Dozer Market Size, Share, and Growth Forecast 2026 - 2033

Dozer Market by Product Type (Crawler Bulldozers, Wheeled Bulldozers), Engine Capacity (Up to 250 HP, 250-500 HP), Propulsion (Electric, Internal Combustion Engine), End-use Industry (Construction), and Regional Analysis, 2026 - 2033

Dozer Market Size and Trends Analysis

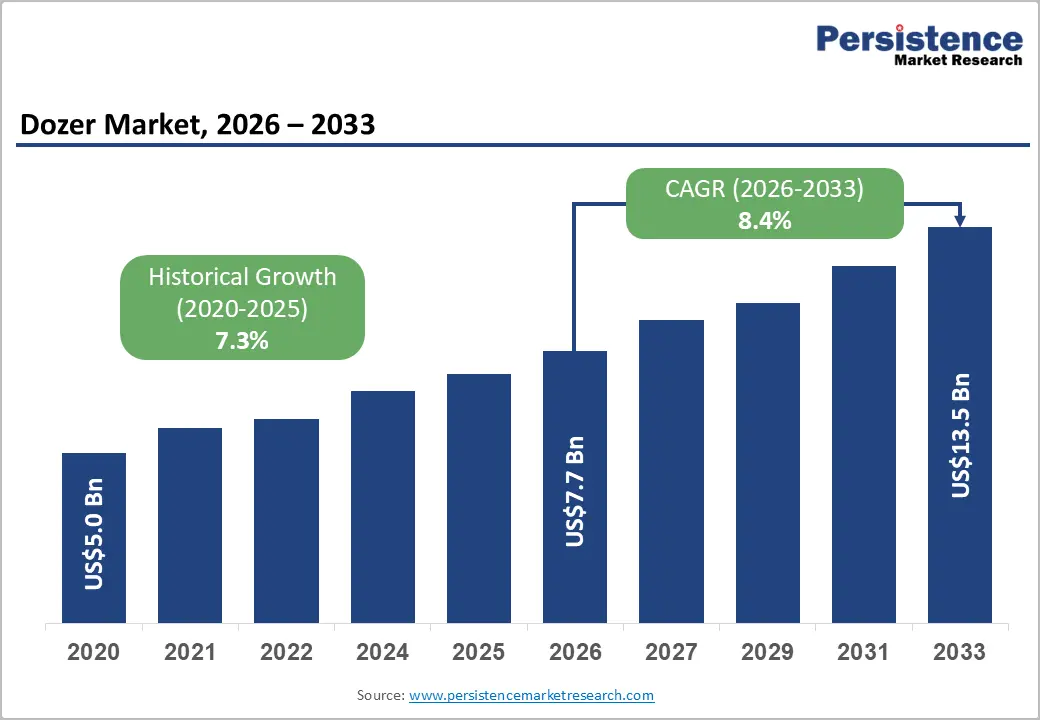

The global dozer market size is likely to be valued at US$7.7 billion in 2026 and is predicted to reach US$13.5 billion by 2033, surging at a CAGR of 8.4% between 2026 and 2033, driven by rising infrastructure development projects and increasing mining activities.

Surging government investments in road construction and urban development led by agencies such as the Ministry of Road Transport and Highways are further projected to boost growth.

Key Industry Highlights:

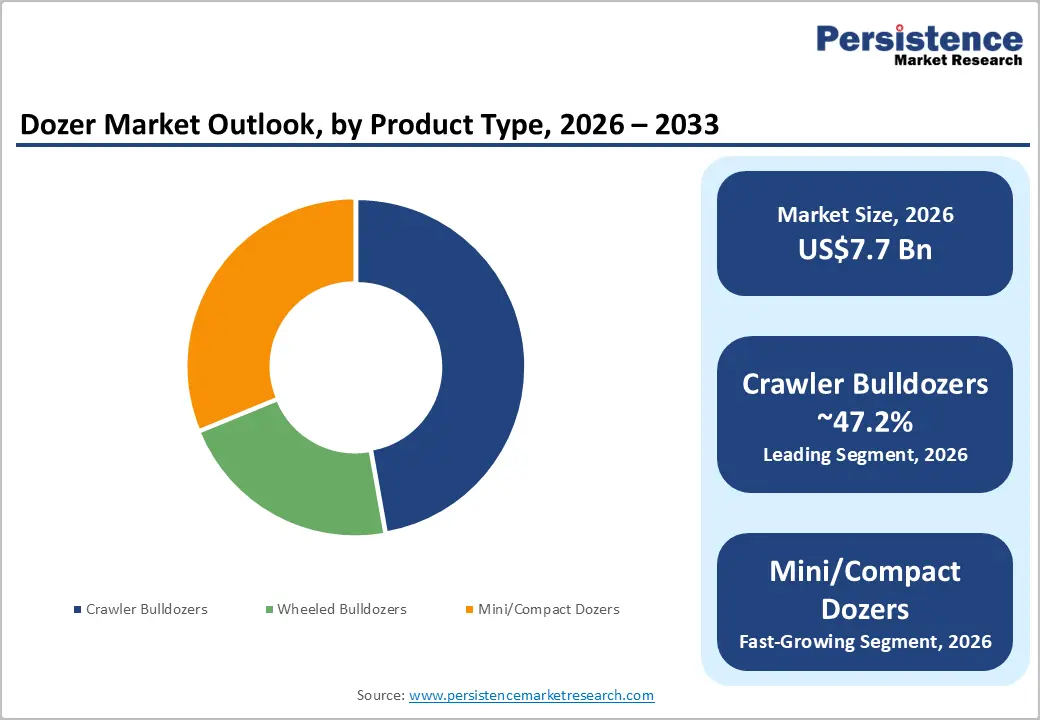

- Leading Product Type: Crawler bulldozers, approximately 47.2% share in 2026, as these provide superior traction and stability on soft, uneven, and muddy terrains.

- Dominant Propulsion: Internal Combustion Engine (ICE), nearly 78.9% in 2026, as it delivers high power output, long operating hours, and easy refueling.

- Product Launch: In March 2025, John Deere announced the launch of the all-new 850 X-Tier Dozer. It features dual-path electric drive technology to optimize torque delivery and simplify the drivetrain compared to conventional systems.

- Leading Region: Asia Pacific, with about 36.7% share in 2026, owing to ongoing infrastructure expansion and mining activities, especially in India and China.

- Fast-growing Region: Europe, fueled by strict emission regulations and government-backed green construction initiatives.

DRO Analysis

Driver - Large-Scale Public Infrastructure Programs

Governments are channeling unprecedented funds into roads, bridges, flood control systems, and energy infrastructure. All of these demand dozers at the site preparation and earthmoving stages. The U.S. federal government alone allocated around US$62 billion for infrastructure development in 2025, targeting public safety, sustainability, and economic growth.

Projects such as the 18.5-mile Lake Pontchartrain levee system in Louisiana and the Brent Spence Bridge corridor upgrade between Kentucky and Ohio are active examples. Road projects specifically require excavator and dozer operators. Nearly US$454 billion in infrastructure work is currently generating demand for qualified machine operators. This sustained pipeline of earthwork ensures dozer demand remains high well beyond 2026.

Ongoing Expansion of Mining Activities

The global shift toward Electric Vehicles (EVs) and clean energy has intensified pressure on mining operations to extract more lithium, cobalt, copper, and rare earth materials. According to World Mining Data 2024, global mineral production reached 18.5 billion metric tons in 2023, marking a year-on-year rise of nearly 5%, boosted mainly by high demand for iron ore, coal, copper, and rare earth elements.

Large crawler dozers are central to overburden removal and haul road construction in surface mines. In September 2024, Fortescue and Liebherr signed a US$2.8 billion agreement to deploy 475 zero-emission mining machines, including battery-powered PR 776 dozers, for fossil-free autonomous mining operations. It is a key signal that mining is expanding and upgrading simultaneously.

Restraint - High Equipment Acquisition Costs

The purchase price of a dozer remains a significant barrier, especially for small and mid-sized contractors. New standard dozers typically range from US$30,000 to US$200,000, with mid-range models around US$75,000 to US$175,000, while large or high-capacity machines can reach up to US$900,000. Novel electric or semi-autonomous models, such as Caterpillar's D7E hybrid, have been listed at around US$600,000, which is potentially double the cost of a conventional unit.

Specialized mining and quarry dozers can exceed US$1 million. Even used equipment demands substantial capital. Without subsidies, financing solutions, or technological cost reductions, small-scale firms struggle to justify the upfront investment, slowing the adoption of next-generation dozer technology across several markets. This cost gap between operational requirement and financial capacity continues to restrict fleet expansion among small operators.

Opportunity - Precision Grade Control through Integrated Technology

GPS and sensor-based blade control systems have shifted dozer operation from manual estimation to data-driven precision. Today, nearly half of all dozers sold are equipped with autonomous grade control technology that uses GPS to complete jobs fast and with high accuracy, eliminating the requirement for costly rework.

Caterpillar's CAT GRADE with 3D and Komatsu's Intelligent Machine Control (IMC) are now factory-installed options. CAT 3D dozers require 80% fewer operator inputs than traditional machines. New operators can see a 200 to 300% improvement in productivity compared to conventional grading. This further reduces labor dependency and the time spent correcting grade errors on large earthmoving projects.

Developments in Semi-Autonomous Operation

Beyond assisted grading, manufacturers are now delivering systems that allow dozers to autonomously plan and execute multi-pass operations across a job site. Komatsu's Proactive Dozing Control, available on the D51EXi-24 and D61EXi-24 models, scans the surrounding terrain in real time, stores data from each pass, and uses that information to drive the blade to precise grade.

Traditionally, GPS machine control was used only during finish grading, around 10 to 20% of total operating time. Proactive Dozing Control extends automation to routine tasks such as site clean-up and trench backfilling, dramatically increasing technology utilization. Komatsu also demonstrated non-line-of-sight teleremote dozer operation at MINExpo in September 2024, broadening the scope of autonomous deployment to hazardous or remote sites.

Category-wise Analysis

Product Type Insights

Crawler bulldozers are predicted to lead with a share of approximately 47.2% in 2026, as these use continuous tracks instead of wheels. This helps them spread weight evenly and avoid sinking in soft soil, sand, or mud. They are widely used in mining, road construction, and large infrastructure projects where ground conditions are uneven. For example, the U.S. Army Corps of Engineers highlights the use of tracked bulldozers in flood control and dam construction due to their ability to operate on wet and unstable ground. In India, crawler dozers are commonly deployed in coal mining projects by Coal India Limited, where overburden removal requires high traction and pushing power.

Mini/compact dozers are estimated to be the fastest-growing segment in the forecast period, as these are designed for tight spaces where large machines cannot operate. Their small size allows easy movement in urban infrastructure projects, landscaping, and utility work. This trend is visible in smart city projects and metro rail expansions across India. The Ministry of Housing and Urban Affairs has emphasized compact equipment in urban redevelopment projects to reduce disruption in densely populated areas. In the U.S., contractors prefer renting these machines as they reduce transport costs and improve project flexibility.

Propulsion Insights

The Internal Combustion Engine (ICE) segment is anticipated to dominate with a share of nearly 78.9% in 2026. Dozers are often used in remote locations such as mines, forests, and large construction sites. These areas lack charging infrastructure, making diesel engines more practical. ICE dozers can run continuously for long hours and can be refueled quickly. According to the U.S. Department of Energy, diesel engines still provide higher energy density compared to current battery systems, which is important for heavy equipment. In mining operations, companies such as BHP continue to rely on diesel-powered fleets because downtime can disrupt production.

The electric segment is expected to remain in the second position in 2026. Governments and contractors are under pressure to reduce carbon emissions. Electric dozers produce zero on-site emissions and low noise, making them suitable for urban and indoor projects.

The European Commission has introduced strict emission norms for construction equipment, encouraging OEMs to develop electric alternatives. For example, Caterpillar showcased battery-powered prototypes as part of its sustainability roadmap, while Komatsu is working on electrified construction machinery under its Green Equipment initiative. In Norway, pilot projects supported by public agencies have already tested electric construction equipment at zero-emission construction sites.

Regional Insights

Asia Pacific Dozer Market Trends

Asia Pacific is anticipated to dominate in 2026, with a share of nearly 36.7%, as it brings together the world's most active construction zones, largest mining operations, and fastest-urbanizing economies. Growth is mainly bolstered by ongoing infrastructure development, expanding mining activities, and increasing government investments in transportation, energy, and industrial projects across China, India, Australia, and Southeast Asia. Manufacturing is also concentrated here.

In 2024, global manufacturing capacity for medium-sized dozers grew by 9%, particularly in Asia Pacific hubs, enabling suppliers to meet rising equipment demand. This combination of demand pull and supply capability is difficult to replicate elsewhere.

China Dozer Market Trends

China's dominance comes from two simultaneous forces, namely, a massive domestic construction pipeline and an expanding global construction footprint through the Belt and Road Initiative (BRI). The country’s 14th Five-Year Plan aims to establish an advanced and globally competitive transport infrastructure system by 2035, emphasizing superhighways, railways, and airports. The mining sector also propels excavator and dozer demand through increased coal, gold, and copper extraction.

Externally, in the first half of 2025 alone, China-based companies signed BRI construction contracts worth US$66.2 billion and invested around US$57.1 billion in projects across Asia, Africa, Europe, and beyond. Local OEMs such as XCMG and LiuGong are also using these overseas projects as launchpads for domestic equipment exports, further deepening China's control over the dozer supply chain.

India Dozer Market Trends

India is one of the most compelling markets right now because government infrastructure spending is both large and long-term. Key government initiatives such as the US$1.4 trillion National Infrastructure Pipeline, PM GatiShakti scheme, and Industrial Corridors project are the backbone of the country's construction push. On the roads front, the Bharatmala program, targeting 34,800 km of optimized road corridors, had already completed 18,926 km by November 2024. It has pushed a 40% year-on-year increase in road construction equipment sales in FY 2023-24. Dozers and graders are important to highway sub-grade preparation under these programs.

Europe Dozer Market Trends

Europe is estimated to witness the fastest growth during the forecast period, boosted by decarbonization mandates, energy infrastructure buildout, and post-pandemic construction revival. Rising public works spending linked to the EU Green Deal, the European Central Bank's 2025 rate-cut cycle, and the ongoing rollout of Stage V emissions rules are the primary factors pushing demand. Equipment buyers are tilting toward battery-electric models for urban projects. Several countries have planned to reduce carbon emissions from construction machinery by 20% by 2025 and by 50% in public projects by 2030, augmenting the adoption of electric construction equipment.

Germany Dozer Market Trends

Germany's construction sector was in a prolonged slump, but the tide has turned due to a historic public investment package. The country launched a €500 billion special fund targeting civil protection, transport, digitalization, hospitals, energy infrastructure, and education, with total investments in 2025 reaching €37 billion (US$43.1 billion). With the Federal Government planning to increase infrastructure investments to over €120 billion (US$139.7 billion) in 2026, the demand for heavy earthmoving equipment, including dozers, is set to rise through the rest of the decade.

U.K. Dozer Market Trends

The U.K. market is on a recovery path, underpinned by large national infrastructure projects and a surging green energy pipeline. Key projects include the US$70 billion HS2 Phase 1 high-speed rail line, the US$40 billion Hinkley Point C nuclear power station, and the US$11 billion Lower Thames Crossing tunnel, initiated in 2024. However, the market is not without challenges. Equipment sales dipped in 2024 as high housebuilding volumes from 2023 normalized. The medium-term outlook remains solid as long-dated public infrastructure programs continue to unlock dozer-intensive earthmoving work.

North America Dozer Market Trends

North America's market is supported by a multi-year federal infrastructure agenda that has translated into concrete project activity. The Bipartisan Infrastructure Law (IIJA) authorizes US$1.2 trillion for infrastructure and transportation improvements, with US$550 billion directed toward new projects, facilitating the development of roads, bridges, and energy systems that require heavy-duty dozers.

The American Road and Transportation Builders Association projected US$203.5 billion in total transportation construction activity for 2026, up from US$203 billion in 2024, with growth expected across bridges and transit. Rental models are also gaining traction, reducing the barrier to fleet access and accelerating equipment upgrades across both the U.S. and Canada.

U.S. Dozer Market Trends

The U.S. remains the anchor of North America’s market, augmented by heavy investments in large-scale infrastructure upgrades across transport, energy, and urban development. Rising adoption of GPS, telematics, and autonomous systems, as well as surging earthmoving requirements in road expansion and utility installation, are also likely to propel growth. However, the policy environment has introduced some turbulence. On January 20, 2025, funding under the IIJA and IRA was temporarily halted, including 400 cancelled grants worth US$1.7 billion.

Subsequent legislative actions compressed project timelines and diverted some funds from climate resilience toward fossil fuel infrastructure. Despite this, private capital is stepping in to fill gaps, and the structural demand for dozers remains strong heading into the second half of the decade.

Competitive Landscape

The global dozer market is moderately consolidated, with a handful of multinational OEMs dominating premium and mining-grade equipment. The leading companies, including Caterpillar, Komatsu, John Deere, Liebherr, and XCMG, collectively control over 40% of the global market. OEMs are constantly striving to differentiate through automation, telematics, autonomous grading systems, fuel-efficiency technologies, and lifecycle service contracts. Caterpillar continues to dominate because of its unmatched dealer network, financing arm, and integration of smart construction technologies.

Komatsu remains the most prominent challenger, especially in mining and large infrastructure projects. The company is investing heavily in autonomous equipment and intelligent machine control. China-based manufacturers such as SANY Group, Shantui, and XCMG are changing the competitive environment by providing low-cost machines with increasingly improved technology stacks. These companies are gaining traction in Africa, Southeast Asia, Latin America, and parts of the Middle East, where affordability matters more than brand legacy.

Key Industry Developments

- In March 2026, Komatsu gave CONEXPO-CON/AGG 2026 attendees an exclusive preview of two next-generation crawler dozers, the D61PXi-25 and the D175AX-10. The D61PXi-25 features IMC 3.0 with a new 10-inch intelligent control touchscreen and auto steering. The D175AX-10 replaces the D155AX-8 and delivers up to 26% more horsepower at 450 hp and up to 25% more material moved per hour.

- In March 2026, Caterpillar announced the Cat D8 XE at CONEXPO-CON/AGG 2026 in Las Vegas, expanding its Next Generation dozer electric drive lineup. The D8 XE uses an electric drive powertrain instead of a conventional torque converter.

- In April 2025, Liebherr-Canada delivered four PR 776 dozers to Taseko Mines at the Gibraltar mine in British Columbia. The PR 776 G8 features updated electronic architecture compatible with Liebherr Mining's Operator Assistance Systems, which give operators greater precision when controlling the blade and ripper.

Companies Covered in Dozer Market

- Caterpillar Inc.

- Komatsu Ltd.

- XCMG Construction Machinery Co., Ltd.

- Deere & Company

- SANY Group (Sany Heavy Industry Co., Ltd.)

- Volvo Construction Equipment AB

- Liebherr Machines Bulle S.A.

- Hitachi Construction Machinery Co., Ltd.

- Shantui Construction Machinery Co., Ltd.

- Guangxi LiuGong Machinery Co., Ltd.

- Others

Frequently Asked Questions

The global dozer market is projected to be valued at US$7.7 billion in 2026.

The dozer market is expected to reach US$13.5 billion by 2033.

Key market trends include rising adoption of automation, telematics, and electric equipment, with leading companies focusing on smart and sustainable construction solutions.

Crawler bulldozers are expected to be the leading product type with a share of nearly 47.2% in 2026, as their track-based design distributes weight evenly, enabling efficient operation.

The market is expected to grow at a CAGR of 8.4% from 2026 to 2033.

Caterpillar Inc., Komatsu Ltd., XCMG Construction Machinery Co., Ltd., and Deere & Company are a few key market players.