- Food Ingredients & Additives

- Dairy Ingredients Market

Dairy Ingredients Market Size, Share, and Growth Forecast, 2026 - 2033

Dairy Ingredients Market by Product Type (Milk Protein Concentrate & Isolate, Whey Ingredients, Others), Source (Milk, Whey, Others), Form, Application, and Regional Analysis for 2026 - 2033

Dairy Ingredients Market Size and Trends Analysis

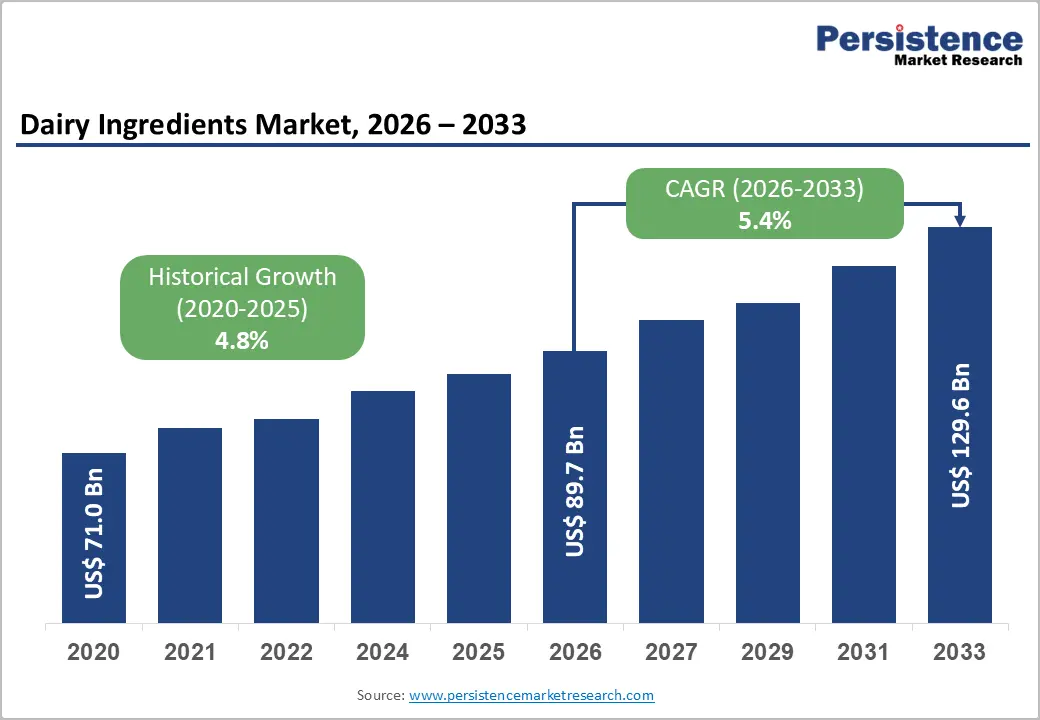

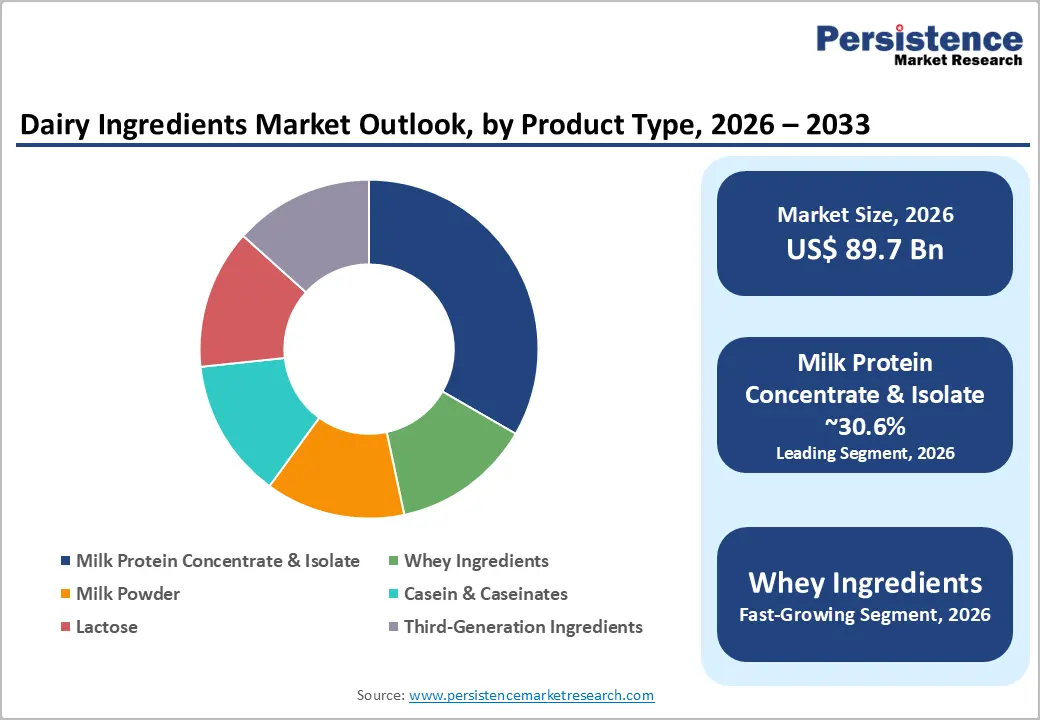

The global dairy ingredients market size is likely to be valued at US$ 89.7 billion in 2026 and is expected to reach US$129.6 billion by 2033, growing at a CAGR of 5.4% during forecast period from 2026 to 2033, driven by rising demand for protein-enriched foods, clean-label dairy formulations, and functional nutrition products across bakery, sports nutrition, infant formula, and convenience food applications.

Growth is also supported by advancements in whey processing, increasing dairy trade flows, and expanding industrial applications for milk-derived proteins and lactose-based ingredients. Manufacturers are prioritizing high-value specialty dairy ingredients to improve margins, strengthen product differentiation, and address evolving consumer nutrition preferences.

Key Industry Highlights:

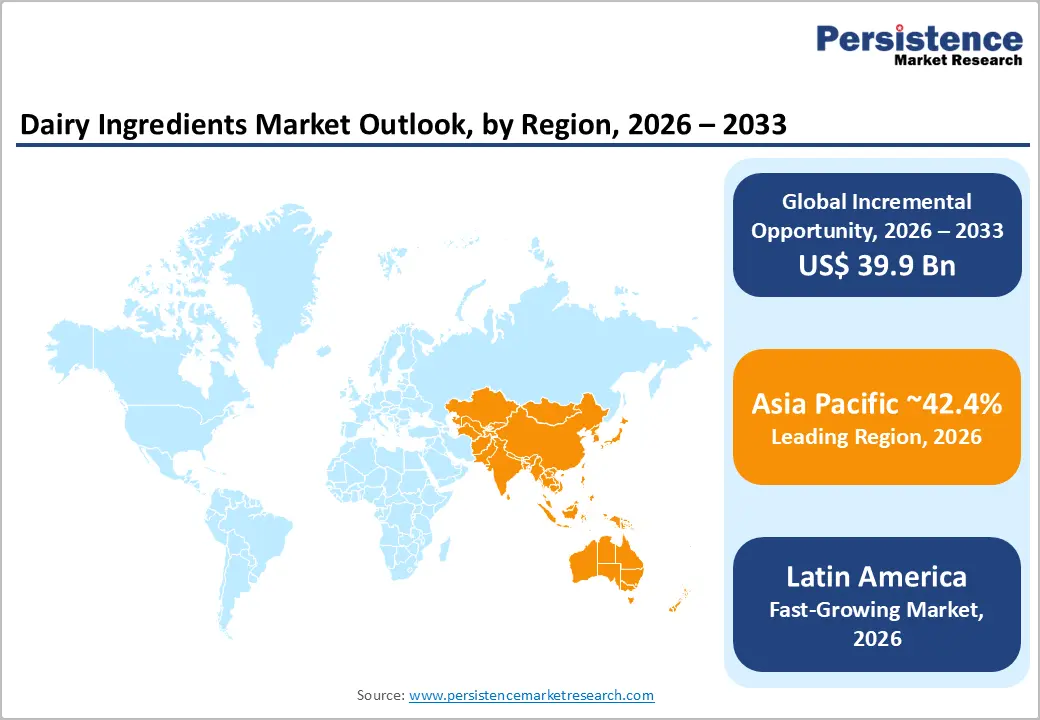

- Leading Region: Asia Pacific is projected to account for approximately 42.4% of the market share in 2026, supported by strong demand from China, India, Japan, and ASEAN countries for infant nutrition, dairy beverages, and protein-enriched foods.

- Fastest-growing Region: Latin America is projected to expand, driven by rising consumption of fortified foods, dairy beverages, and affordable protein nutrition products across Brazil and Mexico.

- Dominant Product Type: Milk protein concentrate & isolate is anticipated to account for nearly 30.6% of the market share in 2026, due to strong demand from sports nutrition, dairy beverages, and functional food applications.

- Leading Source: Milk is estimated to contribute approximately 72.5% of the market share in 2026, owing to its widespread use in milk powders, protein concentrates, lactose derivatives, and infant nutrition ingredients.

DRO Analysis

Driver - Rising Demand for Protein-Enriched Nutrition Products

Protein-focused nutrition trends continue to accelerate global demand for dairy ingredients. Dairy proteins such as whey protein, casein, milk protein concentrate, and milk protein isolate are increasingly used in sports nutrition, medical nutrition, high-protein snacks, and fortified dairy beverages as they provide complete amino acid profiles and strong digestibility characteristics. The growing consumer preference for high-protein diets, weight-management products, and functional foods has increased the use of whey proteins in ready-to-drink beverages, protein bars, and clinical nutrition products.

Food manufacturers are also using dairy proteins to improve texture, emulsification, stability, and nutritional density in processed foods. The expansion of health-conscious consumer demographics across North America, Europe, and Asia Pacific is strengthening long-term demand for value-added dairy ingredients rather than commodity milk powders. This shift is increasing investments in whey fractionation, protein concentration technologies, and specialized dairy formulations designed for premium nutrition applications.

Expansion of Global Dairy Trade and Ingredient Specialization

The growing international trade of dairy proteins, whey powders, lactose derivatives, and specialty milk ingredients is expanding the commercial scope of the dairy ingredients market. Major exporting regions such as Europe, Oceania, and North America continue to increase production of high-value whey and milk protein products to support demand from Asia Pacific, Latin America, and the Middle East.

Ingredient specialization is also improving profitability for dairy processors by enabling fuller utilization of raw milk streams. Companies are increasingly monetizing whey proteins, lactose, permeates, and casein derivatives that were previously treated as lower-value outputs. This transformation is supported by technological advancements in membrane filtration, drying systems, and dairy fractionation technologies.

The expansion of dairy ingredients into applications such as infant formula, clinical nutrition, bakery systems, confectionery, and animal nutrition is increasing market diversification and reducing dependence on traditional fluid dairy consumption. As a result, processors are shifting their investment priorities toward higher-margin specialty dairy ingredients with stronger export potential and greater pricing resilience.

Restraint - Volatility in Milk Prices and Dairy Supply Chains

Milk-price fluctuations remain one of the most significant structural challenges for dairy ingredient manufacturers. Dairy ingredient production depends heavily on raw milk availability, feed costs, transportation expenses, energy pricing, and seasonal supply conditions. Volatility in these factors can significantly affect manufacturing margins, especially when downstream pricing adjustments lag behind input cost increases.

Trade restrictions and regulatory barriers also create uncertainty in cross-border dairy ingredient movement. Import certification requirements, food safety regulations, and changing trade policies can disrupt whey protein, lactose, and milk powder exports into key consumption markets. Supply chain instability further affects inventory planning, long-term procurement contracts, and capital investment decisions related to drying and protein-processing infrastructure.

These risks are particularly relevant for companies operating in export-oriented markets where dairy ingredient pricing is closely tied to global commodity trends and international demand cycles.

Opportunity - Specialty Dairy Proteins Creating Premium Revenue Opportunities

The development of specialty dairy proteins is generating substantial opportunities for dairy ingredient manufacturers. Companies are increasingly introducing advanced whey proteins, lactoferrin ingredients, bioactive milk fractions, and heat-stable dairy proteins for use in medical nutrition, infant formula, active nutrition, and ready-to-drink beverages. Specialty proteins command significantly higher margins than standard milk powders because they address targeted nutritional and functional requirements. Heat-resistant whey proteins, high-purity lactoferrin, and milk fat globule membrane ingredients are becoming increasingly important in premium nutrition categories where manufacturers prioritize functionality, digestibility, and clinical positioning.

Regulatory approvals for specialized dairy ingredients across major international markets are also accelerating commercialization opportunities. This trend is encouraging dairy processors to invest in advanced filtration systems, protein-isolation technologies, and scientific validation programs to strengthen product differentiation and long-term customer partnerships.

Emerging Markets and Localized Dairy Processing Investments

Emerging economies across Asia Pacific and Latin America are creating long-term growth opportunities for dairy ingredient suppliers. Rising disposable incomes, urbanization, changing dietary patterns, and increasing processed-food consumption are strengthening demand for dairy-based nutritional products.

Countries such as India, China, Indonesia, Vietnam, and Brazil are witnessing increased investment in domestic dairy processing infrastructure, ingredient blending facilities, and nutritional food manufacturing. Localized processing improves supply-chain efficiency, reduces import dependency, and supports regional customization of dairy ingredient formulations.

Manufacturers are also exploring sustainability-focused processing models that improve raw-material utilization and reduce production waste. Investments in circular dairy processing systems and ingredient upcycling are expected to improve profitability while aligning with environmental and regulatory expectations. These developments are creating opportunities for multinational dairy ingredient companies to expand their regional manufacturing presence and strengthen market penetration.

Category-wise Analysis

Product Type Insights

Milk Protein Concentrate (MPC) and Milk Protein Isolate (MPI) are anticipated to account for nearly 30.6% of the market share in 2026, making them the leading product-type segment. These ingredients are widely used in high-protein yogurt, ready-to-drink dairy beverages, processed cheese, bakery products, and sports nutrition formulations because they provide high protein density, emulsification, and texture stability. Companies such as Fonterra and Idaho Milk Products continue expanding MPC and MPI offerings to meet growing demand for protein fortification in functional foods and nutritional beverages.

Whey ingredients are expected to witness the fastest growth during the forecast period due to rising demand for sports nutrition, meal replacements, and clinical nutrition products. Whey protein concentrates, isolates, and hydrolysates are increasingly used in protein bars, RTD beverages, and infant nutrition because of their rapid digestibility and strong amino acid profile. Manufacturers, including Arla Foods Ingredients and Glanbia Nutritionals, are investing in advanced whey-processing technologies to develop premium whey solutions with improved purity, taste, and functionality.

Source Insights

Milk is anticipated to hold approximately 72.5% of the market share in 2026, maintaining its position as the dominant source segment. Liquid milk serves as the primary raw material for milk powders, caseinates, lactose, protein concentrates, and specialized dairy blends. Large dairy processors such as Lactalis and FrieslandCampina benefit from integrated milk collection and processing networks that support efficient ingredient production across bakery, confectionery, infant formula, and dairy beverage applications.

Whey is projected to be the fastest-growing source category due to increased utilization of cheese-processing streams in high-value nutritional products. Advances in membrane filtration and protein isolation technologies are enabling manufacturers to produce whey protein concentrates, isolates, and lactose derivatives with higher functionality. Companies such as Hilmar Cheese Company and Agropur are expanding whey-processing capacity to support growing demand from sports nutrition, weight-management, and medical nutrition industries.

Regional Insights

Latin America Dairy Ingredients Market Trends

Latin America is projected to be the fastest-growing regional market, expanding at an estimated 7.5% CAGR during the forecast period. Rising demand for affordable protein nutrition, fortified dairy products, bakery applications, and infant nutrition continues to support market expansion across the region.

Brazil Dairy Ingredients Market Trends

Brazil represents the largest dairy ingredients market in Latin America due to its strong dairy-processing industry and large consumer base. Growing demand for whey proteins, milk powders, and dairy stabilizers in bakery products, flavored milk, and nutritional beverages is supporting market growth. Local manufacturers are increasingly investing in milk protein concentrates and sports nutrition ingredients to address rising health-conscious consumption trends.

Mexico Dairy Ingredients Market Trends

Mexico remains a major importer and processor of dairy ingredients, particularly whey proteins and lactose derivatives used in bakery, confectionery, and convenience foods. Expanding packaged-food consumption and strong demand for protein-enriched beverages are encouraging food manufacturers to incorporate functional dairy ingredients into mainstream product categories.

Argentina Dairy Ingredients Market Trends

Argentina benefits from a well-established dairy farming sector and strong milk availability, supporting domestic production of milk powders and whey ingredients. The country is increasingly focusing on export-oriented dairy ingredient manufacturing, particularly for milk protein concentrates and lactose-based products used in nutritional applications.

Europe Dairy Ingredients Market Trends

Europe remains one of the most strategically important dairy ingredients markets owing to its advanced dairy-processing infrastructure, strong export capabilities, and highly regulated food manufacturing environment. The region is a leading supplier of whey proteins, milk powders, lactose derivatives, and infant nutrition ingredients.

Germany Dairy Ingredients Market Trends

Germany is one of Europe’s largest dairy ingredient producers, supported by advanced dairy-processing technologies and strong industrial food manufacturing capabilities. The country has significant demand for whey proteins, milk protein concentrates, and specialty dairy ingredients used in sports nutrition, bakery products, and functional beverages.

U.K. Dairy Ingredients Market Trends

The U.K. continues to experience rising demand for high-protein dairy beverages, clinical nutrition products, and clean-label food formulations. Food manufacturers are increasingly incorporating whey proteins and milk-based stabilizers into convenience foods and nutritional snacks to meet changing dietary preferences.

Spain Dairy Ingredients Market Trends

Spain is witnessing increasing use of dairy ingredients in bakery, confectionery, and ready-to-drink beverage applications. Investments in sustainable dairy processing and advanced whey fractionation technologies are supporting regional manufacturing growth and export competitiveness.

European manufacturers are shifting toward higher-value specialty ingredients rather than commodity dairy powders alone. Regulatory harmonization across the European Union supports consistent quality standards and cross-border trade, although strict labeling and food safety regulations continue to increase operational complexity.

Asia Pacific Dairy Ingredients Market Trends

Asia Pacific represents the largest regional market, accounting for approximately 42.4% of market share, and is projected to expand at a 6.2% CAGR during the forecast period. Rising disposable incomes, urbanization, and increasing demand for protein-rich foods continue to strengthen regional market growth.

China Dairy Ingredients Market Trends

China remains one of the largest importers of whey proteins, milk powders, and specialized dairy ingredients for infant nutrition and functional food applications. Growing health awareness and increasing demand for high-protein beverages, yogurt products, and sports nutrition continue to support dairy ingredient imports and domestic processing investments.

India Dairy Ingredients Market Trends

India is strengthening its position as a major dairy-processing hub due to expanding milk production and government support for food-processing modernization. Demand for milk powders, dairy proteins, and lactose ingredients is increasing across bakery products, flavored milk, infant nutrition, and convenience foods. Domestic dairy cooperatives and private processors are investing heavily in ingredient manufacturing infrastructure.

Competitive Landscape

The global dairy ingredients market is moderately fragmented, consisting of a combination of multinational dairy processors and regional specialty ingredient suppliers. Competitive leadership is concentrated among companies with strong whey-processing capabilities, advanced protein technologies, extensive milk collection networks, and global distribution infrastructure.

Leading companies are prioritizing innovation-driven premiumization, whey-processing expansion, and geographic market penetration. Manufacturers are investing in specialty proteins, infant nutrition ingredients, and advanced filtration technologies to strengthen product differentiation. Strategic partnerships, regional processing expansion, and customer-focused formulation support are becoming increasingly important competitive strategies across the global dairy ingredients industry.

Key Industry Developments

- In January 2025, FrieslandCampina Ingredients announced that its Vivinal® Lactoferrin ingredient achieved GRAS status for use in U.S. infant nutrition products, strengthening the company’s position in premium early-life nutrition and specialty dairy proteins.

- In February 2026, Milky Mist Dairy Food Ltd. announced expansion plans tied to its upcoming IPO, including investments in premium dairy products such as Greek yogurt and protein-enhanced cottage cheese to strengthen its high-protein dairy segment.

Companies Covered in Dairy Ingredients Market

- Arla Foods Ingredients

- Fonterra Co-operative Group

- FrieslandCampina Ingredients

- Groupe Lactalis

- Saputo Inc.

- Kerry Group

- Glanbia Nutritionals

- Dairy Farmers of America

- Agropur Cooperative

- Hilmar Cheese Company

- Idaho Milk Products

- Valio Ltd.

- Ingredia SA

- Sodiaal International

- Lactoprot Deutschland GmbH

- Carbery Group

Frequently Asked Questions

The global dairy ingredients market is projected to be valued at US$89.7 billion in 2026.

The dairy ingredients market is expected to reach approximately US$129.6 billion by 2033.

Major trends include rising demand for protein-enriched foods, growing adoption of whey proteins in sports nutrition, expansion of ready-to-drink dairy beverages, increasing use of dairy ingredients in infant nutrition, and investments in specialty dairy proteins and advanced whey-processing technologies.

Milk protein concentrate & isolate is the leading segment, accounting for nearly 30.6% of the market share due to strong demand in functional foods, sports nutrition, and dairy beverages.

The dairy ingredients market is projected to grow at a CAGR of 5.4% between 2026 and 2033.

Some of the key companies include Arla Foods Ingredients, Fonterra Co-operative Group, FrieslandCampina Ingredients, Glanbia Nutritionals, and Kerry Group.