- Specialty & Fine Chemicals

- Conductive Carbon Black Market

Conductive Carbon Black Market Size, Share, and Growth Forecast 2026–2033

Conductive Carbon Black Market by Grade (Standard Conductive Carbon Black, Specialty Conductive Carbon Black), Product Type (Furnace Black, Acetylene Black, Channel Black, Thermal Black), Application (Plastics & Polymers, Batteries & Energy Storage, Coatings, Paints & Inks, Electronics & Cables, Rubber & Tire Compounds, Others), End-Use (Industrial, Electrical & Electronics, Automotive, Packaging, Others), and Regional Analysis, 2026–2033

Global Conductive Carbon Black Market Size and Trend Analysis

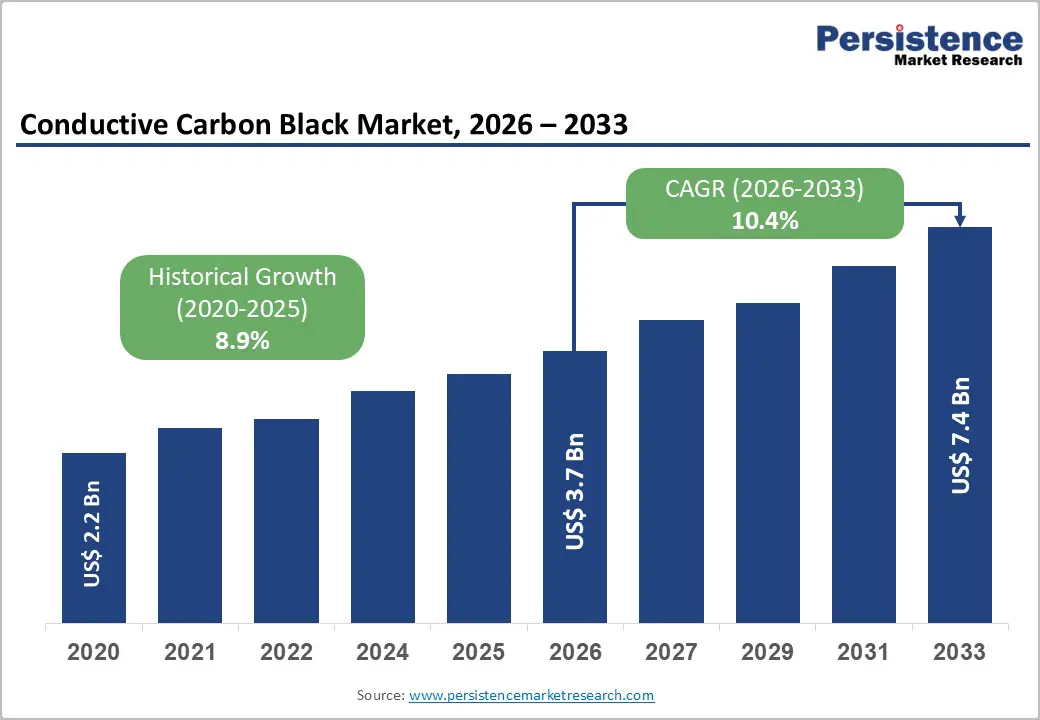

The global conductive carbon black market size is expected to be valued at US$ 3.70 billion in 2026 and is projected to reach US$ 7.40 billion by 2033, growing at a CAGR of 10.4% between 2026 and 2033. The conductive carbon black market is experiencing a sustained and expansion, driven by converging demand signals from electrification, advanced materials, and energy storage industries. This robust trajectory reflects intensifying adoption of conductive carbon black across lithium-ion batteries, electric vehicles (EVs), antistatic plastics and polymers, and EMI shielding applications.

Key Industry Highlights:

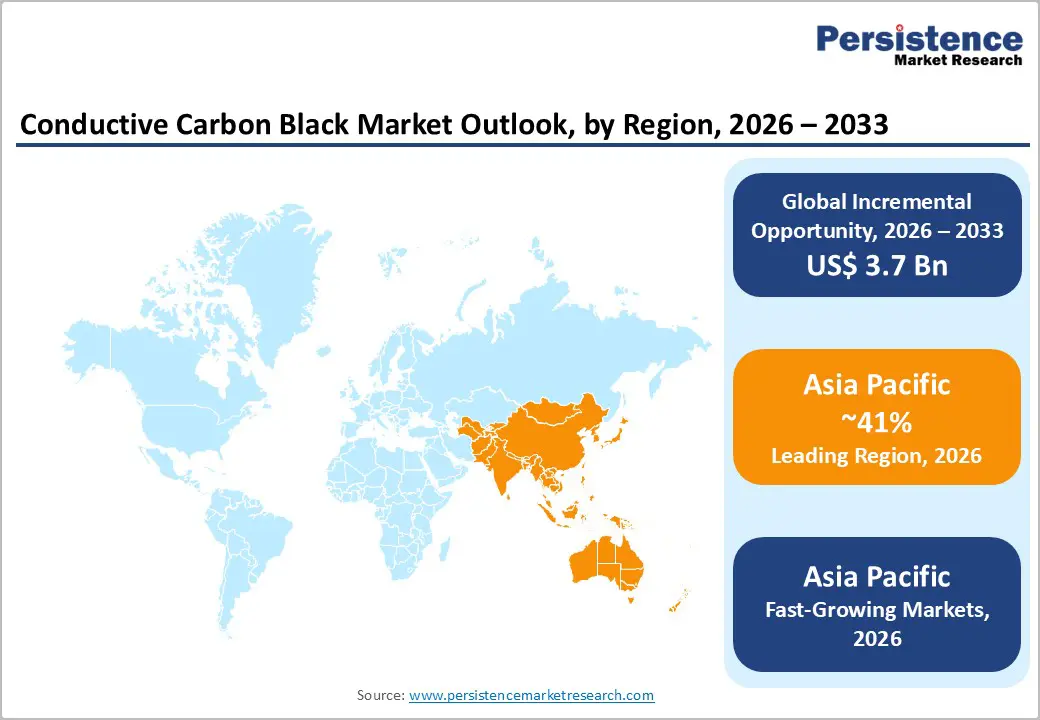

- Leading Region: Asia Pacific leads the global market with a 41.0% share in 2026, equivalent to US$ 1.52 Billion, driven by its concentration of EV manufacturing, battery gigafactories, and expanding industrial polymer compounding capacity across China, India, Japan, and South Korea.

- Fast-Growing Regional Market: Asia Pacific is also the fast-growing market projected at a CAGR of 13.9 in the forecast period with the primary growth catalyst as the unparalleled pace of lithium-ion battery capacity expansion and government-mandated EV adoption targets creating sustained, multi-year demand pull for specialty and standard conductive carbon black grades.

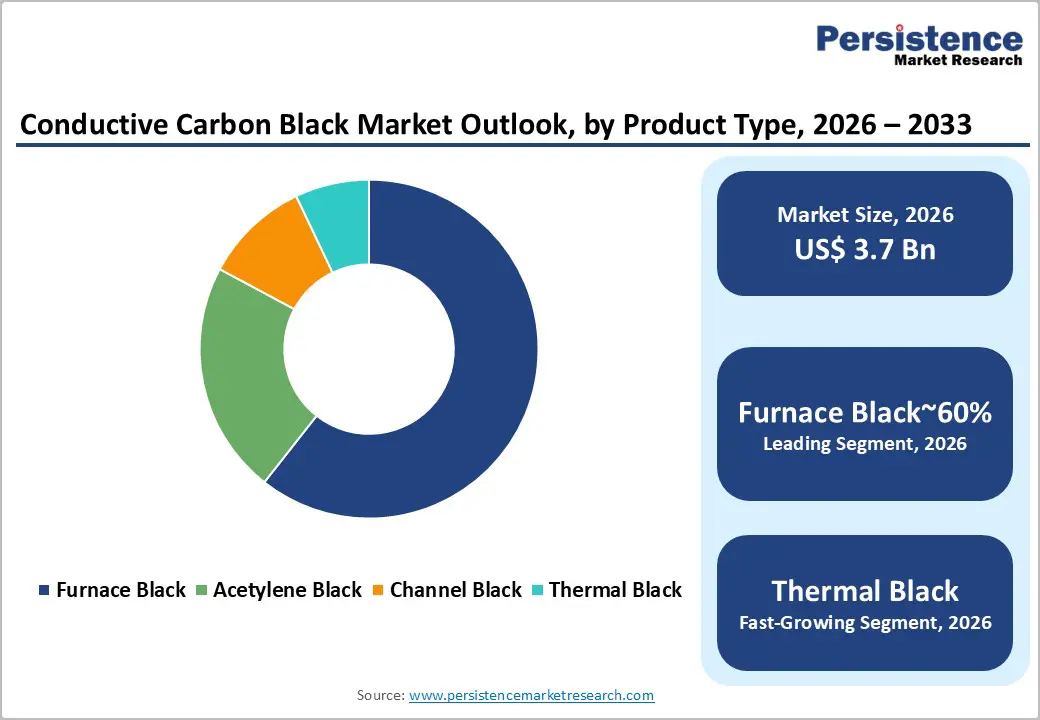

- Leading Grade Segment: Standard conductive carbon black dominates the grade segmentation with a 65.0% share in 2026, equivalent to US$ 2.40 Billion, justified by its cost-effective conductivity delivery across the broadest range of antistatic polymer, rubber, coatings and inks, and industrial applications where specialty grade performance is not required.

- Fast-Growing Application: Batteries & Energy Storage is the fast-growing application segment, propelled by global lithium-ion cell capacity additions projected to exceed 6,500 GWh annually by 2030, creating the single most consequential incremental demand opportunity for high-structure acetylene black and specialty conductive carbon black grades through the forecast period.

- Key Opportunity: Development of battery-grade specialty conductive carbon black for solid-state and next-generation cell architectures, where qualification lead times of 18–36 months make early-mover co-development partnerships with battery OEMs the highest-value strategic investment available to conductive carbon black producers before 2027 commercialisation windows open.

Market Dynamics

Drivers - Accelerating Electrification and Lithium-Ion Battery Demand Amplifying Conductive Carbon Black Consumption

The global transition toward electrified transportation and grid-scale energy storage systems. Conductive carbon black, particularly acetylene black and specialty grades, functions as a critical conductive additive in lithium-ion battery electrodes, lowering the percolation threshold and improving electron transport efficiency.

Global lithium-ion battery capacity additions are on track to exceed 6,500 GWh annually by 2030, based on authenticated market intelligence from energy transition tracking bodies, creating a durable, multi-decade demand runway. Manufacturers targeting battery-grade conductive carbon black must prioritise high purity and precisely controlled structure to meet tightening performance specifications from Tier 1 cell makers.

Rising Demand for Antistatic and EMI Shielding Solutions Across Plastics and Electronics

The irreplaceable role of conductive carbon black in imparting electrical conductivity to otherwise insulating plastics and polymers. Industries ranging from semiconductor packaging to automotive fuel systems require antistatic and EMI shielding performance that conductive carbon black delivers cost-effectively, at loading levels as low as 2 to 5% by weight, depending on the grade and dispersion technology employed.

The global electronics manufacturing output surpassed US$ 3 trillion in 2023, and a growing share of that output depends on conductive polymer compounds using furnace black or specialty high-structure carbon grades. As electronic miniaturisation intensifies, the precision of conductivity control offered by specialty conductive carbon black grades becomes increasingly non-negotiable for materials formulators.

Restraints - Volatile Feedstock Costs and Supply Chain Sensitivity Constraining Margin Stability

The inherent dependence on petroleum-derived feedstock, particularly coal tar distillates and heavy aromatic oils, whose prices move in lockstep with crude oil and refinery output cycles. When feedstock costs spike, as seen during the 2021–2022 energy price surge, where heavy oil prices increased by over 60%, producers face a margin compression dilemma: absorb the increase or risk customer attrition through price pass-through.

Smaller and mid-tier producers operating with limited hedging capability bear disproportionate exposure, which can force capacity rationalisation precisely when demand is accelerating. This dynamic introduces cyclical volatility into what is fundamentally a growth-oriented conductive carbon black industry, complicating long-term capital planning for both producers and downstream compounders.

Stringent Environmental Regulations and Emissions Standards Increasing Compliance Complexity

Regulatory tightening around carbon black manufacturing emissions, particularly particulate matter, polycyclic aromatic hydrocarbon (PAH) outputs, and carbon dioxide emissions from the furnace black process, represents a meaningful operational and capital expenditure burden for market participants. Regulatory bodies across the European Union, United States, and China have progressively tightened permissible emission thresholds, with the EU's Industrial Emissions Directive mandating best available techniques (BAT) compliance across chemical manufacturing by 2025–2026.

Compliance investments required to retrofit or upgrade furnace black facilities run into the tens of millions of dollars per plant, creating a barrier that disproportionately disadvantages smaller regional producers. The net effect is a gradual consolidation pressure within the conductive carbon black space, as only well-capitalised incumbents can absorb these costs without disrupting competitive pricing.

Opportunities - Capitalising on Next-Generation Battery Technologies and Solid-State Cell Development

The transition from conventional lithium-ion to solid-state battery architectures creates a high-value opportunity for conductive carbon black manufacturers capable of delivering ultra-pure, ultra-fine specialty grades suited to next-generation electrolyte and cathode formulations. Manufacturers and formulators who invest now in R&D partnerships with battery cell developers stand to lock in long-term supply agreements before the technology inflection point arrives. Industry data suggests solid-state battery commercial production will scale meaningfully between 2027 and 2030.

Specialty conductive carbon black grades optimised for solid-state systems command premium pricing, with margin profiles estimated at 20% above standard furnace black equivalents. Analysts advise producers to initiate co-development programmes with leading battery OEMs, as qualification cycles for new materials in battery applications typically span 18 to 36 months, making early engagement strategically critical. This opportunity is particularly time-sensitive given the pace of EV platform commitments already announced by major automotive manufacturers through 2030.

Expanding Applications in Sustainable Packaging and Conductive Coatings and Inks

The global push toward smart and active packaging, including antistatic film, conductive barrier coatings, and printed electronics substrates, opens a substantial and underserved application corridor for the Conductive Carbon Black Market. Brand owners and packaging converters across the food, pharmaceutical, and consumer electronics industries increasingly specify conductive carbon black-loaded films and coatings to meet electrostatic discharge (ESD) protection and traceability requirements.

The printed electronics market, which utilises conductive carbon black in inks and coatings for flexible circuits, RFID antennas, and sensors, is expanding at a CAGR exceeding 12% according to regulatory and standards body documentation. Analysts recommend that conductive carbon black suppliers develop application-specific technical service capabilities and pre-formulated dispersion masterbatches to reduce the barrier for coatings and packaging formulators to switch from metal-based conductive additives. The cost-performance advantage of conductive carbon black over silver and copper-based alternatives in these applications is compelling and increasingly recognised by procurement decision-makers.

Category-wise Analysis

Grade Insights

Standard conductive carbon black holds 65.0% of the global share in 2026, equivalent to US$ 2.40 billion, making it the clear volume leader in market segmentation. This segment dominates because it offers a dependable balance between cost and conductivity, meeting the needs of a wide range of applications such as antistatic plastics, rubber compounds, tires, coatings, and inks without the higher cost of specialty grades. Industry data suggests that standard grades are used in over 70% of global antistatic polymer formulations, highlighting their strong and stable demand base.

The fastest-growing segment is Specialty Conductive Carbon Black, driven by rising demand from lithium-ion batteries and advanced EMI shielding applications that require higher purity and performance. While standard grades will continue to dominate core applications, specialty grades are attracting more investment and innovation. Companies should treat specialty grades as a key growth driver while relying on standard grades for steady revenue generation.

Product Type Insights

Furnace black accounts for 60.0% of the global share in 2026, reaching US$ 2.22 billion and maintaining its position as the leading product type. Its dominance is due to its highly scalable production process, flexible raw material use, and ability to control particle size and structure across various applications. Furnace black is widely used in both commodity and mid-range conductive grades, supported by the fact that it represents over 95% of global carbon black production.

The fast-growing segment is thermal black, which is gaining traction due to its high purity, larger particle size, and low surface area. These properties make it ideal for wire, cable insulation, and high-voltage applications requiring stable resistivity. While furnace black will continue to dominate in volume, thermal black is capturing niche, high-value applications.

Application Insights

Plastics & polymers represent 35.0% of the global conductive carbon black market share in 2026, valued at US$ 1.29 billion, making it the leading application segment. This dominance is driven by its widespread use in providing antistatic and conductive properties to thermoplastics and thermosets across industries such as automotive, packaging, electronics, and construction. Regulatory requirements for electrostatic discharge protection, especially in industrial environments, have further strengthened demand for conductive carbon black in polymer applications.

The fastest-growing segment is the batteries & energy storage, supported by the rapid expansion of global energy storage systems and electric vehicles. With installations expected to grow at over 25% annually through 2030, demand for conductive carbon black in battery electrodes is rising significantly. While plastics and polymers will remain the largest segment, batteries are expected to drive the highest growth. Companies should focus on advanced, high-purity grades to capture opportunities in next-generation energy storage technologies.

End-user Insights

The industrial segment holds 45.0% of the global conductive carbon black market in 2026, valued at US$ 1.67 billion, making it the largest end-use sector. Its leadership comes from its broad application base, including antistatic conveyor belts, fuel hoses, conductive flooring, and industrial piping systems. These applications rely on conductive carbon black to meet strict safety and operational standards across manufacturing and processing industries. Additionally, regular replacement and maintenance cycles ensure consistent demand in this segment.

The fastest-growing end-use sector is the electrical & electronics, driven by the rapid expansion of electric vehicles, consumer electronics, data centers, and 5G infrastructure. These applications require high-performance materials for EMI shielding, cable insulation, and semiconductor packaging. While the industrial segment will continue to lead in volume, electrical and electronics will grow at a faster pace. Companies should align their product development with the evolving requirements of this high-growth segment.

Regional Insights

North America Conductive Carbon Black Market Trends and Insights

North America holds 25.0% of the global conductive carbon black market in 2026, valued at US$ 0.93 billion. Growth is supported by EV expansion, reshoring policies like the Inflation Reduction Act, and rising use in batteries, aerospace, and antistatic plastics, strengthening long-term regional demand.

United States Conductive Carbon Black Market Size

The United States represents nearly 78% of the North American market, reaching about US$ 0.73 billion in 2026. Demand is driven by EV battery production, polymer compounding, and electronics manufacturing. Expansion of gigafactories and IRA incentives will continue reinforcing the country’s dominant regional position.

Europe Conductive Carbon Black Market Trends and Insights

Europe accounts for 20.0% of the global market in 2026, totaling US$ 0.74 billion. Growth is shaped by EU Green Deal regulations, battery sustainability requirements, and strong automotive demand. Producers with low-carbon manufacturing capabilities are increasingly favored across automotive, coatings, and electronics applications.

Germany Conductive Carbon Black Market Size

Germany contributes around 30% of Europe’s market, valued at US$ 0.22 billion in 2026. Demand is driven by automotive manufacturing, specialty chemicals, and EV battery applications. Increasing electrification of vehicles is expected to accelerate demand for high-performance conductive carbon black grades.

United Kingdom Conductive Carbon Black Market Size

The UK accounts for approximately 15% of the European market, reaching US$ 0.11 billion in 2026. Demand stems from aerospace, defence electronics, and 5G infrastructure. Increasing focus on EMI shielding and domestic battery investments is expected to support steady growth over the forecast period.

France Conductive Carbon Black Market Size

France holds nearly 18% of the European market, valued at US$ 0.13 billion in 2026. Demand is supported by automotive production, coatings, and printed electronics. National electrification targets and energy storage investments are expected to strengthen demand for specialty conductive carbon black applications.

Asia Pacific Conductive Carbon Black Market Trends and Insights

Asia Pacific dominates with 41.0% market share in 2026, reaching US$ 1.52 billion and growing at a 13.9% CAGR. Growth is fueled by EV production, battery manufacturing, and industrial expansion. The region remains central to global supply chains and future competitive positioning.

China Conductive Carbon Black Market Size

China leads the Asia Pacific market with 55% share, valued at US$ 0.84 billion in 2026. Demand is driven by EV manufacturing, battery production, and plastics. Domestic producers are scaling capacity and improving quality, intensifying competition while supporting overall market expansion.

India Conductive Carbon Black Market Size

India represents around 14% of the Asia Pacific market, totaling US$ 0.21 billion in 2026. Growth is supported by tire manufacturing, electronics, and EV initiatives like the PLI scheme. Expanding domestic battery production and electrification will drive sustained demand growth.

Japan Conductive Carbon Black Market Size

Japan accounts for approximately 12% of the Asia Pacific market, valued at US$ 0.18 billion in 2026. Demand is driven by advanced electronics, battery R&D, and specialty materials. Leadership in solid-state battery innovation positions Japan as a key market for high-performance conductive carbon black.

Competitive Landscape

The global conductive carbon black market operates as a moderately consolidated competitive landscape, with a small group of globally integrated producers, led by Cabot Corporation, Orion Engineered Carbons, and Birla Carbon, commanding significant scale advantages through integrated feedstock access, global production networks, and deep technical service capabilities. These incumbents compete primarily on the basis of product performance differentiation, application engineering support, and supply chain reliability rather than price alone.

Mid-tier and regional players, including Tokai Carbon, Mitsubishi Chemical Corporation, and Himadri Speciality Chemical, compete effectively in regional markets and niche specialty grades by leveraging proximity, process expertise, and faster customisation cycles. The most consequential emerging competitive dynamic is the rise of Chinese domestic producers, including Jiangxi Blackcat Carbon Black and Longxing Chemical, who are rapidly closing the quality gap on specialty grades while maintaining cost advantages. Strategic investment in dispersion technology, battery-grade purity certification, and low-carbon manufacturing credentials increasingly defines competitive differentiation in the premium segment of this market.

Key Developments

- January, 2025: Cabot Corporation announced a multi-year capacity expansion programme at its Cilegon, Indonesia facility to increase specialty conductive carbon black output, targeting growing demand from Asia Pacific battery and electronics manufacturers and reinforcing its regional supply chain position.

- September, 2024: Orion Engineered Carbons S.A. launched a new product line of ultra-high purity acetylene black grades specifically engineered for next-generation lithium-ion and solid-state battery electrode applications, marking a significant product development milestone in the conductive carbon black industry analysis landscape.

- March, 2024: Birla Carbon completed the commissioning of a debottlenecking project at its Renukoot, India facility, increasing specialty conductive carbon black capacity by approximately 15%, directly targeting the growing domestic EV and electronics manufacturing demand base under India's PLI incentive framework.

Companies Covered in Conductive Carbon Black Market

- Cabot Corporation

- Orion Engineered Carbons S.A.

- Birla Carbon

- Tokai Carbon Co., Ltd.

- Mitsubishi Chemical Corporation

- Denka Company Limited

- Imerys Graphite & Carbon

- Phillips Carbon Black Limited (PCBL)

- Omsk Carbon Group

- Himadri Speciality Chemical Ltd.

- China Synthetic Rubber Corporation (CSRC)

- Jiangxi Blackcat Carbon Black Inc., Ltd.

- Longxing Chemical Stock Co., Ltd.

- Sid Richardson Carbon & Energy Co.

- Asbury Carbons

- Continental Carbon Company

- Shanxi Fulihua Chemical Materials Co., Ltd.

- Shandong Huibaichuan New Materials Co., Ltd.

- Cancarb Limited

Frequently Asked Questions

The conductive carbon black market is valued at US$ 3.70 billion in 2026 and projected to reach US$ 7.40 billion by 2033, growing at a CAGR of 10.4%.

Growth is driven by rising EV production increasing battery demand, and regulatory requirements for antistatic and EMI shielding across plastics, electronics, and industrial sectors, ensuring consistent and diversified market expansion.

Standard Conductive Carbon Black leads with 65.0% share in 2026 due to its cost-effective conductivity across multiple applications, while specialty grades are gradually gaining share from advanced battery and electronics demand.

Asia Pacific dominates with 41.0% share in 2026, supported by strong EV, battery, electronics, and polymer industries, and remains the fastest-growing region due to expanding manufacturing and industrial infrastructure.

Key opportunity lies in developing ultra-pure conductive carbon black for next-generation batteries, especially solid-state, where early partnerships with battery manufacturers enable premium pricing, long-term contracts, and strong competitive advantage.

The leading companies in the Conductive Carbon Black Market include Cabot Corporation, Orion Engineered Carbons S.A., Birla Carbon, Tokai Carbon Co., Ltd., Mitsubishi Chemical Corporation, Denka Company Limited, and Phillips Carbon Black Limited (PCBL), among others.