- Specialty & Fine Chemicals

- Functional Fibers Market

Functional Fibers Market Size, Share, and Growth Forecast 2026 - 2033

Functional Fibers Market by Product Type (Soluble Fibers, Insoluble Fibers, Others), Source (Cereals & Grains, Fruits & Vegetables, Legumes & Pulses, Seaweed & Marine Sources, Synthetic/Modified Fibers, Others), Nature (Organic, Conventional), Application (Food & Beverages, Dietary Supplements, Pharmaceuticals, Clinical Nutrition, Animal Feed & Pet Nutrition, Personal Care & Cosmetics, Others), and Regional Analysis, 2026 - 2033

Functional Fibers Market Size and Trend Analysis

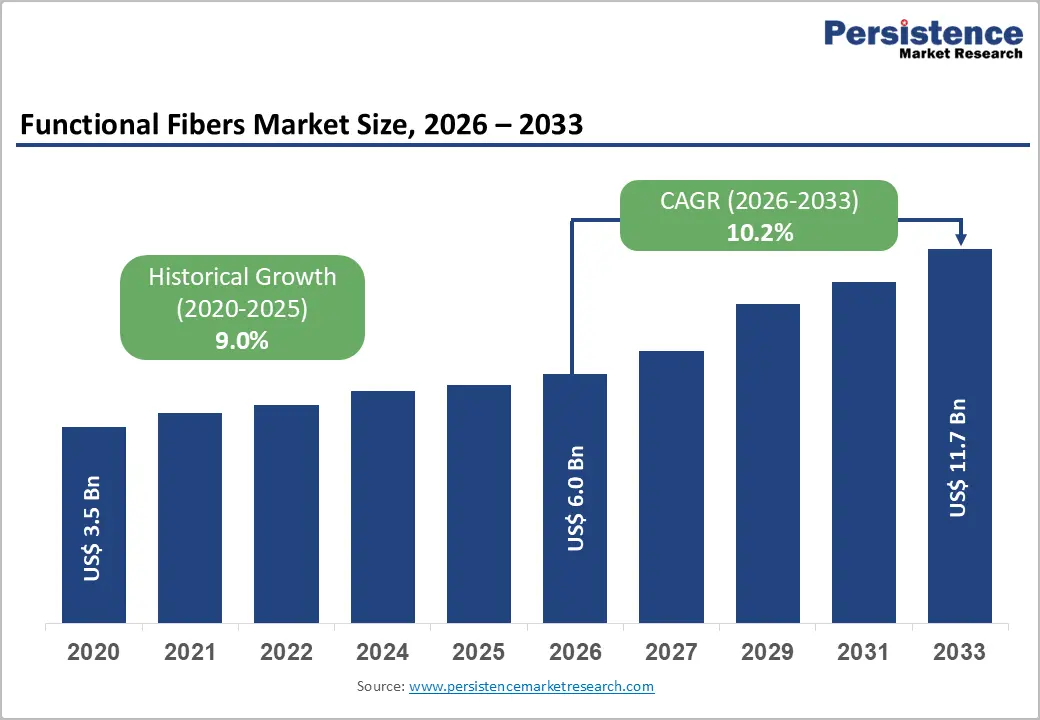

The global functional fibers market size is expected to be valued at US$ 6.0 billion in 2026 and projected to reach US$ 11.7 billion by 2033, growing at a CAGR of 10.2% between 2026 and 2033.

Rise in consumer awareness about gut health, chronic disease prevention, and clean-label nutrition continues to fuel robust demand for functional fibers across food, pharmaceutical, and nutraceutical sectors globally.

According to the World Health Organization (WHO), non-communicable diseases, including type 2 diabetes and cardiovascular conditions, both strongly linked to dietary fiber deficiency, account for 74% of all global deaths annually, prompting consumers and healthcare providers alike to prioritize high-fiber dietary ingredients. Additionally, the rapid expansion of the functional food and dietary supplement industries, alongside growing clinical evidence endorsing fiber supplementation for metabolic health, creates compelling long-term tailwinds for sustained market growth.

Key Industry Highlights:

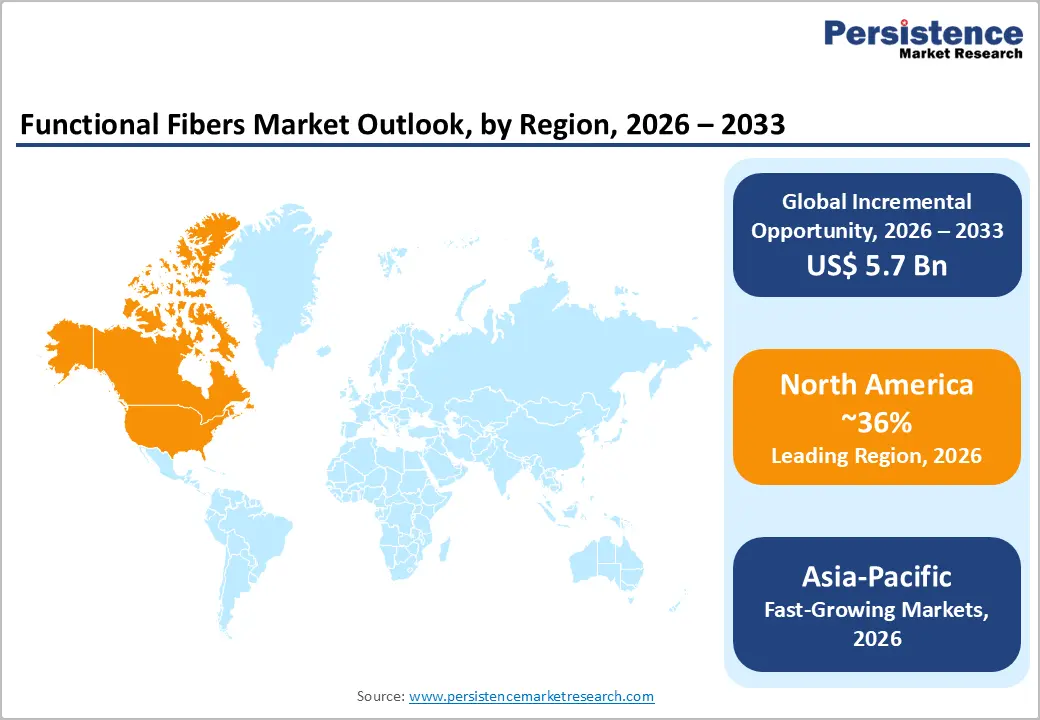

- Regional Leadership: North America leads the global functional fibers market with approximately 36% market share in 2025, driven by the persistent fiber gap in the U.S. population, strong regulatory support from the FDA, and a highly innovative functional food and dietary supplement industry ecosystem.

- Fast-growing Market: Asia Pacific is the fast-growing regional market for functional fibers, fueled by rapid urbanization, rising lifestyle disease prevalence, expanding functional food manufacturing capacity, and proactive government health initiatives across China, Japan, India, and ASEAN nations.

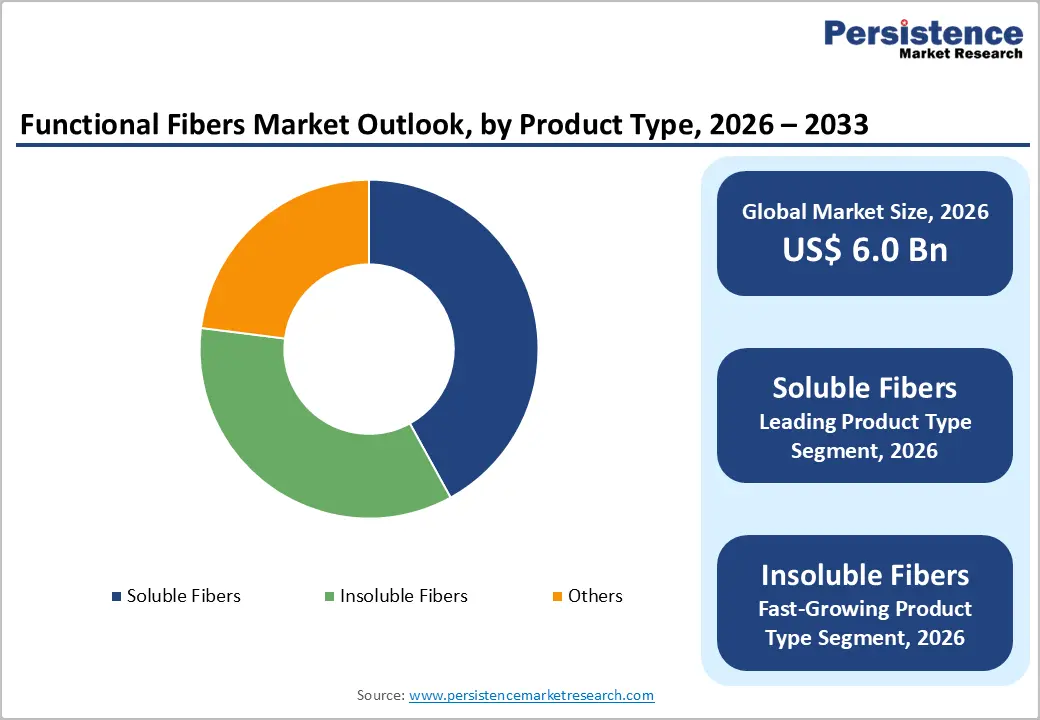

- Leading Source Fiber: Soluble fibers dominate the global market with approximately 42% product type share in 2025, backed by clinically validated health benefits for cardiovascular and metabolic health, regulatory health claim approvals from FDA and EFSA, and broad compatibility across food and beverage matrices.

- Fast-growing Source Fiber: Insoluble fibers represent the fastest-growing product type segment, driven by rising consumer demand for digestive health solutions, increasing adoption in high-fiber bakery and snack formulations, and growing clinical interest in their role in colorectal health management.

- Opportunity: The expansion of the clinical nutrition and medical foods segment presents a key market opportunity, with fiber-enriched formulations increasingly adopted in disease management protocols for IBS, metabolic syndrome, and post-surgical recovery nutrition, supported by favorable regulatory frameworks across the EU and North America.

Market Dynamics

How Does the Prevalence of Lifestyle-Related Diseases Fuel Fiber Fortification?

The global surge in lifestyle-related chronic conditions is one of the most potent demand drivers for the functional fibers market. The International Diabetes Federation (IDF) reported in its 2023 Diabetes Atlas that approximately 537 million adults worldwide are living with diabetes, a figure projected to rise to 643 million by 2030. Dietary fiber, particularly soluble varieties such as beta-glucan and inulin, is extensively clinically validated for its role in glycemic control, cholesterol reduction, and weight management.

The U.S. Food and Drug Administration (FDA) and the European Food Safety Authority (EFSA) have both issued health claims permitting manufacturers to highlight the association between soluble fiber intake and reduced risk of coronary heart disease. This regulatory backing has further encouraged food manufacturers to incorporate functional fibers into everyday food products, from breakfast cereals and breads to dairy analogs and fortified beverages, amplifying market demand consistently.

Growth of Functional Food & Beverage Industry Driving Ingredient Adoption

The rapid global expansion of the functional food and beverage sector is creating significant downstream demand for high-quality functional fiber ingredients. The Food and Agriculture Organization (FAO) has consistently underscored dietary fiber's role in preventing obesity, which now affects over 1 billion people globally according to the WHO's 2024 Global Obesity Report. Consumers, particularly in North America and Europe, increasingly seek products with verifiable health benefits, fueling demand for fiber-enriched formulations.

Major food and beverage companies are proactively reformulating products with prebiotic fibers, resistant starches, and pectin to align with this trend. The growing acceptance of high-fiber claims on packaging reinforced by FDA and EFSA approved qualified health claims has made functional fibers a key value-addition strategy for food manufacturers seeking competitive differentiation in premium product categories.

Does the Production Costs and Processing Complexity Limit Growth?

Despite strong demand signals, the high cost of extracting and processing certain premium functional fibers particularly those derived from seaweed, chicory, and specialty legumes poses a notable restraint. Extraction technologies such as enzymatic hydrolysis and membrane filtration require significant capital investment. U.S. Department of Agriculture (USDA) data indicates that specialty dietary ingredient sourcing costs have increased by approximately 15-20% over the past three years, partly due to supply chain disruptions and rising raw material prices. These elevated costs are often passed on to end-users, limiting adoption among price-sensitive consumer segments and smaller food manufacturers operating on thin margins, particularly in developing economies across Asia and Latin America.

What are the Expansions in the Clinical Nutrition and Medical Foods Segments?

The clinical nutrition segment represents a high-value, rapidly expanding opportunity for functional fiber manufacturers. With aging global populations and escalating hospitalization rates, healthcare providers are increasingly incorporating fiber-enriched medical foods into disease management protocols for conditions including irritable bowel syndrome (IBS), Crohn's disease, and metabolic syndrome.

The Global Burden of Disease Study estimates that digestive disorders affect over 40% of the global population at any given time. Regulatory frameworks such as the EU's Regulation (EU) No 609/2013 on foods for special medical purposes (FSMPs) are enabling manufacturers to develop targeted fiber-based clinical nutrition products with specific health claims. Companies like Roquette Frères and Kerry Group are actively investing in clinical-grade fiber grades designed for hospital and home care nutrition settings, signaling strong commercial potential.

Category-wise Analysis

Product Type Insights

Soluble fibers dominate the functional fibers market, accounting for approximately 42% of global market share in 2025. This leadership position is primarily driven by the extensive clinical evidence supporting the metabolic health benefits of soluble fiber types such as inulin, pectin, beta-glucan, and fructooligosaccharides (FOS). The FDA and EFSA have both approved qualified health claims linking beta-glucan consumption to reduced blood cholesterol levels, significantly boosting its incorporation in heart-healthy food and beverage formulations.

Furthermore, soluble fibers serve a dual functional role in food systems acting both as a health-enhancing ingredient and a functional additive for improving texture, viscosity, and shelf life. Their compatibility with a wide array of food matrices, including dairy, beverages, baked goods, and nutraceutical capsules, further underpins their dominant commercial position. Leading players, including Tate & Lyle PLC and Ingredion Incorporated, have invested heavily in expanding their soluble fiber portfolios to meet growing global demand.

Source Insights

Cereals & grains represent the leading source segment within the functional fibers market, commanding the largest share in 2026 owing to the widespread availability, cost-effectiveness, and consumer familiarity. Wheat bran, oat fiber, and corn-derived resistant starch are among the most commercially deployed fiber sources across food and beverage formulations. The U.S. Grains Council and USDA data consistently reflect oat fiber and wheat bran as the most consumed dietary fiber ingredients globally.

The functional and nutritional versatility of cereal-derived fibers, combined with established and scalable supply chains, makes them the preferred choice for mass-market food manufacturers. The global expansion of high-fiber bakery products and ready-to-eat cereals, especially in developed markets, continues to reinforce the leading position of the cereals & grains segment. ADM (Archer Daniels Midland Company) and Cargill, Incorporated are among the key suppliers benefiting most from the strong demand for cereal-derived functional fibers.

Regional Insights

North America Functional Fibers Market Trends and Insights

North America dominated the functional fibers market in 2026, accounting for nearly 36% of the global market valued at USD 6.0 billion. Strong consumer awareness regarding digestive health, obesity management, diabetes prevention, and clean-label nutrition significantly supported regional demand. The region also benefits from advanced functional food manufacturing, high dietary supplement consumption, and strong product innovation by companies such as Ingredion Incorporated and Cargill Incorporated.

According to the CDC, most U.S. adults consume only about half of the recommended fiber intake, increasing demand for fiber-fortified foods and beverages. Rising consumption of ultra-processed foods has further accelerated interest in functional fibers for gut and metabolic health applications.

U.S. Functional Fibers Market Trends and Insights

The United States led the North American market and was expected to reach nearly US$ 1.5 billion by 2026 due to strong demand for functional foods, dietary supplements, and digestive health ingredients. CDC and NHANES data showed average U.S. dietary fiber intake remained around 16 grams per day, significantly below recommended levels, encouraging manufacturers to launch fiber-enriched bakery, beverages, cereals, and snack products. The country also has high obesity and diabetes prevalence, increasing use of soluble fibers for blood sugar and cholesterol management.

Major ingredient suppliers, including ADM and Tate & Lyle PLC, expanded prebiotic and resistant starch portfolios to support rising demand for gut-health-focused nutrition solutions.

Canada Functional Fibers Market Trends and Insights

Canada emerged as the fast-growing market in North America and was expected to reach nearly 10.6% CAGR in the forecast period. The growth parameters in these regions are based on increasing consumer preference for clean-label, plant-based, and high-fiber foods. Canadian consumers increasingly adopted oat fiber, barley beta-glucan, and prebiotic ingredients in breakfast cereals, dairy alternatives, and nutritional supplements.

Government-backed healthy eating guidelines promoting whole grains and fiber-rich diets also supported market expansion. Demand for functional fibers further increased across sports nutrition and weight-management products due to rising health awareness and preventive healthcare spending. Food manufacturers focused heavily on sugar reduction and digestive wellness formulations, accelerating innovation in soluble and resistant fiber applications across packaged foods and beverages.

Europe Functional Fibers Market Trends and Insights

Europe represented nearly 29% of the global Functional Fibers Market in 2026 due to strong regulatory support for nutritional labeling, growing clean-label demand, and increasing consumer awareness regarding gut microbiome health. The region has high adoption of prebiotic fibers, resistant starches, and cereal-based fibers across bakery, dairy, and functional beverage applications. Organizations such as the European Food Safety Authority actively promoted fiber-related health claims, encouraging manufacturers to innovate in digestive wellness products.

Europe also benefits from strong demand for plant-based and sustainable ingredients. Countries across the region are increasingly focused on reducing sugar and fat consumption, boosting the utilization of functional fibers as texture improvers and calorie-reduction ingredients in processed foods.

Germany Functional Fibers Market Trends and Insights

Germany dominated the European market and was expected to reach around US$ 620 million by 2026 due to high consumption of functional bakery products, cereals, and dietary supplements. German consumers increasingly preferred clean-label and digestive-health-focused foods containing inulin, beta-glucan, and resistant starch ingredients.

The country also has a strong organic and plant-based food industry supporting demand for natural fiber sources. Major European ingredient manufacturers expanded investments in chicory root fibers and cereal-derived ingredients to support growing food reformulation activities. Rising demand for sugar reduction in confectionery and dairy products further accelerated the use of soluble fibers as multifunctional ingredients for texture enhancement and calorie reduction in packaged foods.

United Kingdom Functional Fibers Market Trends and Insights

The United Kingdom is likely to reach approximately 10.4% CAGR during the forecast period due to increasing awareness regarding obesity, digestive disorders, and gut microbiome health. Consumers increasingly adopted fiber-fortified snacks, beverages, and nutritional supplements as preventive health products. Demand for vegan and plant-based functional foods significantly accelerated the use of oat fiber, pea fiber, and prebiotic ingredients across retail food categories.

The country also witnessed strong expansion in personalized nutrition and sports nutrition products containing functional fibers for satiety and metabolic health benefits. Government initiatives encouraging healthier diets and reduced sugar intake further supported fiber ingredient adoption across processed foods and ready-to-eat product categories.

Asia Pacific Functional Fibers Market Trends and Insights

Asia-Pacific was projected to register the fast-growth in the functional fibers market and is likely to experience 12.8% CAGR in the forecast period. Rapid urbanization, rising disposable incomes, growing awareness regarding digestive wellness, and increasing consumption of fortified foods significantly supported regional growth. Countries such as China, India, and Japan witnessed strong expansion in functional beverages, dietary supplements, and prebiotic-enriched foods.

The rising prevalence of obesity, diabetes, and gastrointestinal disorders also accelerated demand for soluble and insoluble fiber ingredients. According to regional dietary fiber studies, consumers increasingly adopted functional foods for weight management and immunity support. Manufacturers expanded investments in cereal-based fibers, resistant starch, and clean-label formulations to meet evolving consumer preferences across developing economies.

China Functional Fibers Market Trends and Insights

China led the Asia-Pacific market and was expected to reach approximately US$ 850 million by 2026. The country’s strong packaged food industry, rising middle-class population, and growing health awareness significantly boosted demand for dietary fibers. Government initiatives promoting whole-grain consumption and healthier eating habits further supported market expansion. China also remained a major producer and consumer of cereal fibers, resistant starches, and prebiotic ingredients used in beverages, dairy products, and infant nutrition.

Increasing demand for gut-health-focused foods and nutritional supplements encouraged food manufacturers to incorporate soluble fibers and functional ingredients into mainstream food categories. Expanding sports nutrition and weight-management sectors also contributed to rising fiber ingredient adoption.

India Functional Fibers Market Trends and Insights

India's functional fibers market growth is anticipated at nearly 13.5% CAGR during the forecast period due to rising health-conscious consumers, expanding processed food consumption, and increasing preventive healthcare awareness. The country’s large vegetarian population and growing preference for plant-based nutrition accelerated demand for cereal fibers, fruit fibers, and pulse-derived ingredients. Functional beverages, fortified snacks, and digestive health supplements witnessed strong adoption among urban consumers.

Rising diabetes and obesity prevalence has also increased interest in low-calorie and high-fiber food products. Domestic food manufacturers are increasingly focused on clean-label and gut-health formulations using prebiotic and resistant fiber ingredients to meet changing dietary preferences among middle-income consumers.

Competitive Landscape

The global functional fibers market exhibits a moderately consolidated structure, with a mix of large multinational ingredient companies and specialized niche players. Leading participants such as Ingredion Incorporated, Tate & Lyle PLC, Cargill, Incorporated, ADM, and Roquette Frères collectively account for a significant share of global revenues, leveraging their extensive R&D capabilities, global distribution networks, and diversified product portfolios as key differentiators.

Market leaders are increasingly focused on clean-label fiber innovation, sustainability-driven sourcing, and expanding clinical substantiation for their fiber ingredients. Strategic acquisitions, joint ventures with biotechnology firms, and investment in novel fermentation and enzymatic processing technologies are emerging as the primary growth strategies among top-tier players. Smaller specialized companies such as Fiberstar, Inc., and Sensus are carving out competitive niches through proprietary fiber technologies and targeted application development services.

Key Developments

- March 2026: Roquette Frères strengthened its cosmetics and health ingredient portfolio after acquiring the pharmaceutical solutions business of IFF Pharma Solutions. The acquisition expanded Roquette’s expertise in plant-based excipients, functional ingredients, and formulation technologies used across pharmaceuticals, nutraceuticals, and cosmetic applications.

- December 2025: The food and beverage industry witnessed rising innovation in fiber-enriched products targeting gut microbiome health and broader wellness benefits. Companies including Ingredion Incorporated, Comet Bio, Tate & Lyle PLC and Nexira highlighted growing consumer demand for functional fibers linked to digestive health, weight management, mental wellness, and metabolic support.

- July 2024: Ingredion Incorporated launched its VERSAFIBE dietary fiber series to help food manufacturers increase fiber content and reduce calories in bakery, pasta, snack, and extruded food products. The company introduced VERSAFIBE 2470 and VERSAFIBE 1490 as insoluble resistant starch ingredients designed to deliver fiber fortification with minimal impact on texture, flavor, and color.

Functional Fibers Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 3.5 Billion |

| Projected Market Value (2026) | US$ 6.0 Billion |

| Projected Market Value (2033) | US$ 11.7 Billion |

| CAGR (2026 - 2033) | 10.2% |

| Leading Region | North America, 36% share |

| Dominant Product Type | Soluble Fibers, 42% share |

| Top-ranking Source | Cereals & Grains, 34% share |

| Incremental Opportunity | US$ 5.8 Billion |

Companies Covered in Functional Fibers Market

- Ingredion Incorporated

- Roquette Frères

- Cargill, Incorporated

- Fiberstar, Inc.

- Tate & Lyle PLC

- Royal DSM

- ADM (Archer Daniels Midland Company)

- Sensus

- Kerry Group

- DuPont de Nemours, Inc.

- Others

Frequently Asked Questions

The global functional fibers market is estimated to be valued at US$ 6.0 billion in 2026.

Rising digestive health awareness, growing functional food consumption, prebiotic demand, clean-label trends, and obesity concerns.

North America is the leading region, holding approximately 36% market share in 2025.

Expanding demand for prebiotic, clean-label, and fiber-fortified foods in emerging health-conscious consumer markets.

Leading companies in the global functional fibers market include Ingredion Incorporated, Roquette Frères, Cargill, Incorporated, Tate & Lyle PLC, ADM (Archer Daniels Midland Company), Royal DSM.