- Specialty & Fine Chemicals

- Chitosan Market

Chitosan Market Size, Share, and Growth Forecast 2026 - 2033

Chitosan Market by Source (Shrimp, Crab, Prawns, Squid/Krill, Others), by Grade (Industrial Grade, Food Grade, Pharmaceutical Grade), Application (Water Treatment, Healthcare & Pharmaceuticals, Food & Beverages, Construction Industry, Agriculture, Others), by Regional Analysis, 2026 - 2033

Chitosan Market Size and Trend Analysis

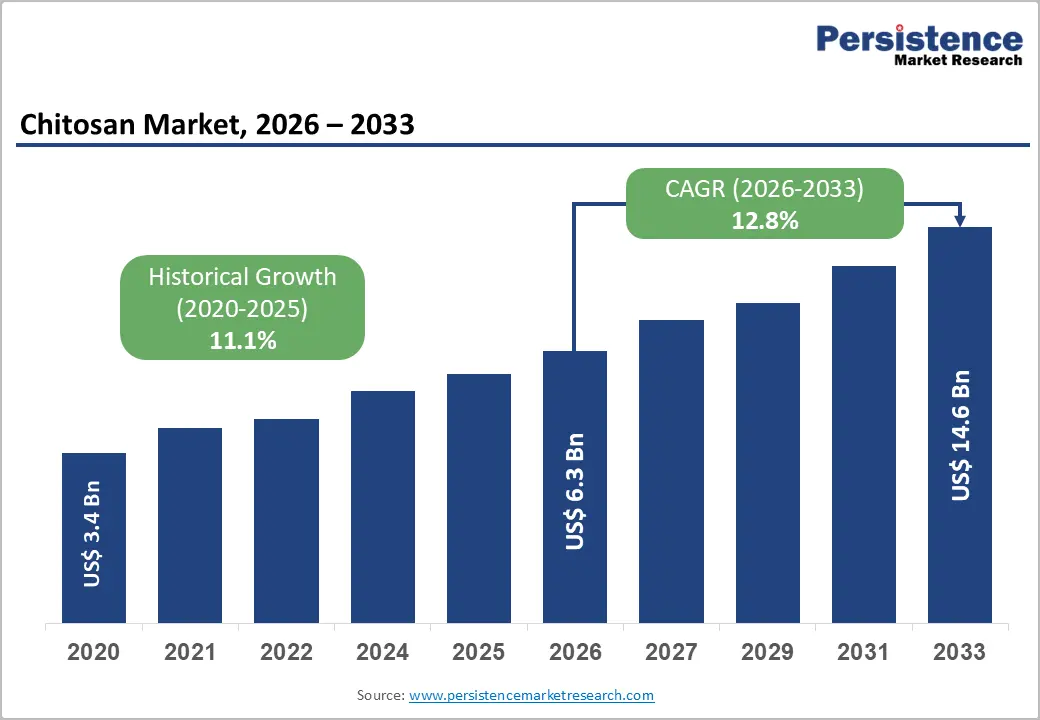

The global chitosan market is expected to be valued at US$6.30 billion in 2026 and is projected to reach US$14.64 billion by 2033, growing at a CAGR of 12.8% between 2026 and 2033.

The stringent restrictions on synthetic polymer use in food packaging and water treatment, most notably the European Union's Single-Use Plastics Directive (2019/904), now fully enforced across member states, are redirecting industrial procurement toward biodegradable natural polymers such as chitosan, fundamentally restructuring demand across multiple end-use verticals.

Key Industry Highlights:

- Leading Region: Asia Pacific's 39% revenue leadership in the global chitosan market rests on China and India's combined crustacean processing capacity, but the region's long-term competitive position will increasingly depend on how effectively producers upgrade from commodity industrial-grade output to pharmaceutical-grade supply, a transition that Panvo Organics Pvt. Ltd. and KIMICA Corporation are already executing with measurable export impact.

- Leading Segment: Pharmaceutical grade's 42.0% revenue share reflects the structural pricing advantage, estimated at 3-5x over industrial grades by the International Pharmaceutical Excipients Council, that certified producers extract from regulated buyer relationships, creating a durable revenue moat that insulates market leaders from commodity price competition and makes pharmaceutical segment certification the highest-return investment thesis in the chitosan value chain.

- Fast-Growing Segment: Crab-derived chitosan's acceleration as the fastest growing source segment opens a commercially significant niche for North American shell waste processors, with Clearwater Seafoods' Nova Scotia facility exemplifying how sustainable materials valorisation can create integrated feedstock-to-biopolymer business models that command premium pricing in construction and biomedical applications where molecular weight consistency is a primary purchasing criterion.

- Key Opportunity: Chitosan-based drug delivery systems represent the highest-conviction strategic opportunity for producers targeting value accretion by 2033. Pharmaceutical buyers financing oncology nanoparticle platforms through programmes supported by the U.S. National Cancer Institute are establishing multi-year procurement agreements that will require producers to invest in nanomedicine-grade purity validation infrastructure now to participate in what will be a rapidly scaling, contract-locked revenue segment by 2027.

Market Dynamics

Drivers - Regulatory Phase-Out of Synthetic Flocculants in Municipal Water Treatment

Municipal water utilities across North America and Europe face mounting compliance costs as the U.S. Environmental Protection Agency's revised National Primary Drinking Water Regulations, updated in 2024 to lower maximum contaminant levels for PFAS compounds, accelerate the substitution of polyacrylamide-based flocculants with biopolymer alternatives including chitosan.

Veolia Water Technologies piloted chitosan-based coagulation systems across three French municipal treatment facilities in 2023, reporting a 30% reduction in residual sludge volume compared to conventional aluminium sulfate treatment. Over the next two to three years, utilities seeking to demonstrate compliance with tightening effluent standards will scale biopolymer procurement, positioning chitosan suppliers with validated wastewater purification credentials as preferred vendors in long-term municipal contracts.

Pharmaceutical Grade Chitosan Adoption in Advanced Drug Delivery Systems

The rapid expansion of mucosal and transdermal drug delivery platforms, where chitosan's mucoadhesive and permeation-enhancing properties are irreplaceable, creates durable demand from biomedical applications procurement teams inside major generic and specialty pharma manufacturers. Lubrizol Life Science launched its chitosan-based oral thin-film excipient platform in 2022, supplying contract development organisations developing buccal drug delivery systems for diabetes and cardiovascular indications.

As the European Medicines Agency continues expanding its approval framework for biopolymer excipients under the Guideline on Excipients in the Dossier for Application for Marketing Authorisation (EMA/CHMP/QWP/396951/2006, revised 2023), pharmaceutical-grade chitosan demand will compound at above-market rates, rewarding producers who invest in cGMP-certified manufacturing capacity now.

Restraints - Raw Material Supply Concentration and Seasonal Feedstock Volatility

Chitosan production depends almost entirely on chitin extracted from crustacean shells, a byproduct stream whose availability fluctuates with global seafood harvest cycles and is geographically concentrated in China, India, and Southeast Asia, creating supply chain fragility for downstream processors in North America and Europe.

The World Trade Organization's 2023 trade policy review flagged China's export licensing regime for processed marine biopolymers as a non-tariff barrier, with lead times for certified pharmaceutical-grade chitosan from Chinese suppliers extending to 14 to 18 weeks during peak demand periods. For new entrants lacking multi-source procurement infrastructure, this feedstock dependency translates directly into margin compression and an inability to honour supply commitments to regulated-industry customers.

Stringent Purity Standards Elevating Production Costs for Pharmaceutical Applications

Achieving the deacetylation degrees and molecular weight consistency demanded by the United States Pharmacopeia (USP) and European Pharmacopoeia monographs for pharmaceutical-grade chitosan requires capital-intensive multi-stage purification and analytical validation processes that can add a 40% cost premium over industrial-grade production.

The Ph. Eur. monograph 1774, governing chitosan hydrochloride specifications, imposes residual solvent and heavy metal limits that are difficult to meet consistently using shrimp shells sourced from regions with variable aquaculture practices. Incumbents with established cGMP facilities absorb these costs through volume, but smaller regional producers face disadvantages when competing for pharmaceutical supply agreements.

Opportunities

Chitosan-Based Bioactive Crop Protection in Regenerative Agriculture

Agrichemical formulators and specialty input distributors should accelerate investment in chitosan-based plant biostimulants and seed coating technologies, which activate systemic plant immunity without leaving synthetic pesticide residues, a capability directly aligned with the European Commission's Farm to Fork Strategy target of 50% reduction in chemical pesticide use by 2030.

Koppert Biological Systems expanded its chitosan-enriched crop protection line across Iberian Peninsula markets in 2024, targeting high-value horticultural crops where residue regulations are most stringent. Formulators with proprietary depolymerisation processes that produce oligomeric chitosan, which demonstrates superior crop absorption over high-molecular-weight variants, will capture a disproportionate share as the EU biostimulants regulation (EU) 2019/1009 mandates market entry criteria that effectively screen out synthetic alternatives.

Antimicrobial Chitosan Films for Active Food Packaging in Emerging Markets

Consumer packaged goods companies and flexible packaging converters operating in South and Southeast Asia should position chitosan-based antimicrobial films as a commercially viable alternative to petroleum-derived barrier packaging, leveraging both the cost competitiveness of regional crustacean shell supply and escalating retailer demands for sustainable materials.

Amcor plc disclosed active development of chitosan-laminate flexible packaging formats in its 2024 sustainability report, targeting fresh produce and processed meat applications where food preservation through natural antimicrobial mechanisms reduces cold-chain dependency. For this opportunity to fully materialise, regional governments must harmonise food-contact material standards with Codex Alimentarius Commission guidelines, a convergence already under negotiation in the ASEAN Food Safety Network's 2024-2026 regulatory alignment agenda.

Category-wise Analysis

Source Insights

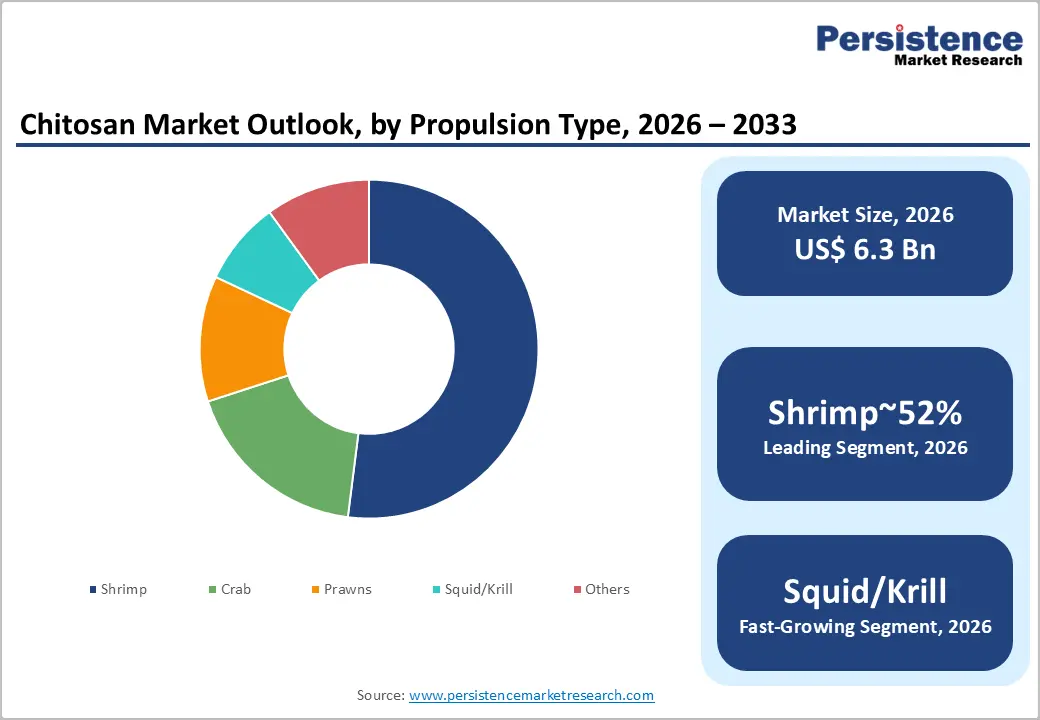

Shrimp dominates the global chitosan market at 52.0% in 2026, worth US$ 3.28 billion. This lead comes from abundant shell supply, high chitin content, and strong processing hubs in Asia's aquaculture centers. Pharmaceutical and water treatment buyers snap up shrimp shell chitin for its reliable molecular weight and low ash content. Wound care makers, like HemCon Medical Technologies, love it for haemostatic dressings; its cationic charge speeds platelet aggregation at injury sites. NOAA reports U.S. shrimp processing alone yields over 200,000 tonnes of shells yearly, shielding buyers from import risks. This cost edge cements shrimp's top spot through 2033.

Crab chitosan grows fastest, fueled by expanding blue crab and snow crab fisheries in North America and Canada. Stricter waste rules push processors to turn shells into value. Clearwater Seafoods boosted capacity in Nova Scotia in 2022, feeding biopolymer makers with high-molecular-weight chitosan for construction. This viscous crab variant acts as a rheology modifier and antimicrobial in concrete, backed by ASTM's new biopolymer standards.

Grade Insights

Pharmaceutical grade claims 42% of the global chitosan market in 2026. Premium prices and big contracts from drug makers boost its revenue share beyond volume alone. CDMO buyers use it as a mucoadhesive in nasal vaccines, boosted by post-COVID mucosal tech such as Bharat Biotech's iNCOVACC, approved in India in 2022. IPEC notes it costs 3-5x more than food grade, locking in revenue for certified players. It also grows fastest by value, thanks to oncology firms adopting chitosan nanoparticles for targeted delivery. Nanobiotix and ETH Zürich's 2023 studies prove it works, with NIH funding more research.

Application Insights

Water treatment leads applications at 34% of the global chitosan market in 2026, valued at US$ 2.14 billion. It shines as a coagulant in municipal drinking water and industrial wastewater across Asia, North America, and Europe. Pulp mills, textile dyers, and food plants rely on it to remove solids, metals, and dyes, required by India's 2023 effluent rules. WHO's 2022 guidelines promote it for low-resource areas, building tough demand.

Healthcare and pharmaceuticals grows fastest, driven by orthopaedics and tissue engineering. Chitosan scaffolds support bone and cartilage repair. Integra LifeSciences rolled out chitosan-collagen composites in 2023 for U.S. and German surgeries, covered by CMS and G-DRG reimbursements. EU's 2017 MDR rules confirmed its biocompatibility, easing med-tech sourcing and spurring big orders.

Regional Insights

North America Chitosan Market Trends and Insights

North America accounts for 24.0% of the global chitosan market in 2026, representing US$ 1.51 Billion, with demand concentrated in pharmaceutical excipient supply chains and water infrastructure modernisation programmes funded through the U.S. Infrastructure Investment and Jobs Act (2021), which allocated US$ 55 billion for water system upgrades, a portion of which is channelled toward green chemistry procurement mandates. As federal agencies increasingly require biopolymer-based treatment chemicals in publicly funded infrastructure, North American chitosan demand will expand beyond its current pharmaceutical concentration into mainstream municipal utilities over 2026-2029.

- United States Chitosan Market Size

The United States contributes an estimated 80% of North America's chitosan market revenue, driven by the country's concentration of pharmaceutical CDMOs and the FDA's regulatory infrastructure that makes U.S.-sourced pharmaceutical-grade chitosan the preferred specification for global drug filings. Expanding aquaculture waste valorisation programmes under the USDA Agricultural Research Service are beginning to develop domestic chitosan extraction capacity, which should reduce import dependency and compress pharmaceutical buyer lead times through 2028.

Europe Chitosan Market Trends and Insights

Europe accounts for 19% of the global chitosan market in 2026, representing US$ 1.20 billion, with the regulatory environment shaped most directly by the European Chemicals Agency (ECHA) REACH regulation and the Farm to Fork Strategy, both of which are actively channelling industrial procurement toward bio-based polymer alternatives in packaging, agriculture, and water treatment.

Germany, France, and the United Kingdom collectively represent the core demand centres, with pharmaceutical and food-grade chitosan consumption growing as the EU bioplastics industry targets, requiring 20% bio-based content in packaging by 2030 under the proposed Packaging and Packaging Waste Regulation (PPWR), begin reshaping procurement specifications.

- Germany Chitosan Market Size

Germany contributes an estimated 26% of European chitosan market revenue, reflecting the country's dense concentration of pharmaceutical manufacturers, including those operating under GMP Annex 11 digital compliance frameworks that require excipient traceability, a specification that chitosan suppliers meeting Ph. Eur. monograph 1774 can satisfy directly. BASF SE's ongoing investment in bio-based polymer R&D, including chitosan-compatible coating systems for agrochemical applications, signals that Germany's industrial chemistry sector will drive formulation-level demand growth through 2028.

- United Kingdom Chitosan Market Size

The United Kingdom represents approximately 20% of the European chitosan market revenue, with demand anchored in the NHS supply chain's procurement of wound care biopolymers and biomedical applications, particularly haemostatic and antimicrobial wound dressings that the Medicines and Healthcare products Regulatory Agency (MHRA) classifies under the UK Medical Devices Regulations 2002 (SI 2002/618), amended post-Brexit to maintain CE-equivalent certification pathways. Scotland's seafood processing sector, particularly salmon and langoustine processing, is emerging as a domestic chitosan feedstock source that could reduce UK pharmaceutical manufacturers' dependence on Asian imports by 2027.

- France Chitosan Market Size

France accounts for an estimated 17% of European chitosan market revenue, driven primarily by the country's advanced cosmetics and active food packaging industries, both subject to ANSM (Agence nationale de sécurité du médicament et des produits de santé) oversight, where chitosan's film-forming and antimicrobial properties are integrated into cosmetic preservative systems as the EU Cosmetics Regulation (EC) No 1223/2009 restricts synthetic preservative concentrations. L'Oréal's publicly disclosed R&D investment in biopolymer-based cosmetic delivery systems, announced at the 2023 In-Cosmetics Global trade show, specifically identified chitosan derivatives as priority ingredients for scalp treatment formulations.

Asia Pacific Chitosan Market Trends and Insights

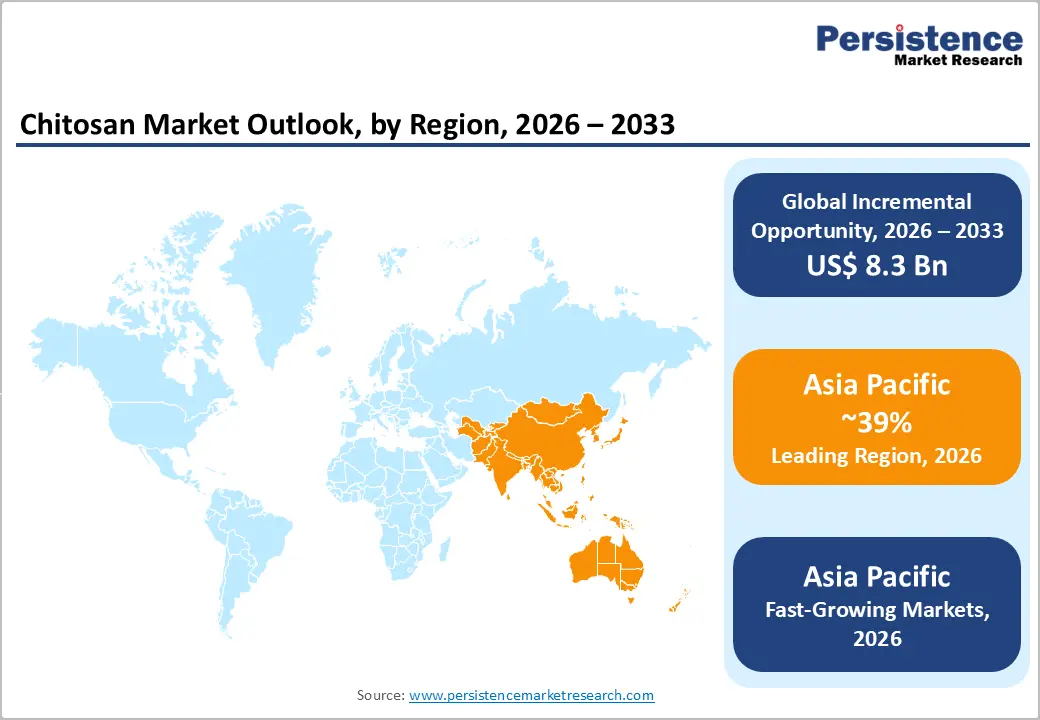

Asia Pacific accounts for 39% of the global chitosan market in 2026, representing US$ 2.46 billion, a position built on the region's structural command of global crustacean production. China alone contributes over 60% of global shrimp aquaculture output, per FAO's State of World Fisheries and Aquaculture 2022 report, and is reinforced by integrated supply chains linking shell waste generators directly to chitosan extraction facilities.

- China Chitosan Market Size

China commands an estimated 55% of Asia Pacific's chitosan market revenue, anchored by the country's globally dominant position as both the largest producer and largest domestic consumer of chitosan across water treatment, agriculture, and food preservation applications. Qingdao Yunzhou Biochemistry Co., Ltd., one of China's largest vertically integrated chitosan producers, has expanded extraction capacity since 2022 in response to domestic demand from China's 14th Five-Year Plan (2021-2025) wastewater treatment investment mandate, which allocated CNY 1.06 trillion to environmental infrastructure.

- India Chitosan Market Size

India represents approximately 20% of Asia Pacific's chitosan market revenue, with pharmaceutical-grade demand growing sharply as India's CDMO sector, ranked second globally in generic drug API manufacturing by the Pharmaceuticals Export Promotion Council of India (Pharmexcil), integrates chitosan excipients into export-oriented drug filings targeting FDA and EMA markets. Panvo Organics Pvt. Ltd., a Gujarat-based speciality chitosan producer, has expanded its pharmaceutical-grade output to serve both domestic formulators and European import buyers, positioning India to capture a greater share of global pharmaceutical chitosan demand by 2028.

- Japan Chitosan Market Size

Japan accounts for an estimated 12% of Asia Pacific's chitosan market revenue, supported by the country's sophisticated functional food and nutraceutical industry, where chitosan's cholesterol-binding properties have been validated under the Consumer Affairs Agency's Foods with Function Claims (FFC) system, which had registered over 6,800 functional food claims by early 2024. KIMICA Corporation, Japan's leading chitosan producer, continues to supply high-deacetylation pharmaceutical and nutraceutical grades to both domestic health supplement manufacturers and export clients in South Korea and Taiwan, maintaining Japan's position as a technology-leader in high-purity chitosan processing.

Competitive Landscape

The global chitosan market operates as a moderately fragmented competitive landscape with Primex ehf, KitoZyme S.A., and Heppe Medical Chitosan GmbH holding the strongest positions in pharmaceutical-grade supply to regulated Western markets, while Golden-Shell Pharmaceutical Co. Ltd. and Qingdao Yunzhou Biochemistry Co., Ltd. dominate on production scale and cost competitiveness across industrial and food-grade segments.

The disruptive force entering the landscape is fungal chitosan extraction, notably advanced by KitoZyme S.A., which sources chitin from *Aspergillus niger* fermentation byproducts, entirely sidestepping seafood supply chain volatility and enabling vegan-certified pharmaceutical-grade chitosan that commands significant pricing premiums with health-conscious nutraceutical buyers.

Key Market Developments

- January, 2025: KitoZyme S.A. secured a supply agreement with a major European CDMO to provide pharmaceutical-grade fungal chitosan for oral drug delivery applications, marking the first large-scale commercial contract for non-crustacean chitosan in a regulated pharmaceutical supply chain.

- March, 2024: FMC Corporation divested its chitosan and biopolymer specialty chemicals portfolio to focus on core crop protection and lithium businesses, creating an acquisition opportunity that Advanced Biopolymers AS and regional Asian producers moved to evaluate for capacity consolidation.

- September, 2024: Heppe Medical Chitosan GmbH received ISO 13485:2016 certification renewal for its pharmaceutical-grade chitosan manufacturing facility in Halle, Germany, reinforcing its position as the preferred European supplier for medical device-grade biopolymer procurement under the EU MDR 2017/745 framework.

Companies Covered in Chitosan Market

- Primex ehf

- KitoZyme S.A.

- Heppe Medical Chitosan GmbH

- Panvo Organics Pvt. Ltd.

- Qingdao Yunzhou Biochemistry Co., Ltd.

- Advanced Biopolymers AS

- Golden-Shell Pharmaceutical Co. Ltd.

- FMC Corporation

- BIO21 Co., Ltd.

- Meron Biopolymers

- G.T.C. Bio Corporation

- Foodchem International Corporation

- Dainichiseika Color & Chemicals Mfg. Co. Ltd.

- KIMICA Corporation

- Chitinor AS

- Chibio Biotech Co., Ltd.

- Vietnam Food JSC

- Agratech International Inc.

- Mahtani Chitosan Pvt. Ltd.

- Bio Synectics Inc.

Frequently Asked Questions

The global chitosan market is valued at US$6.30 billion in 2026 and is forecast to reach US$14.64 billion by 2033, expanding at a CAGR of 12.8%. The primary growth catalyst is convergent regulatory pressure across water treatment, pharmaceutical, and agriculture sectors mandating biopolymer substitution for synthetic chemical inputs, mostly through the EU Single-Use Plastics Directive and the U.S. EPA's updated PFAS-linked water treatment standards.

Growing demand for eco-friendly wastewater treatment and pharmaceutical applications is driving the chitosan market. Stricter environmental regulations are encouraging the use of chitosan-based flocculants, while its increasing adoption as a drug delivery excipient in the pharmaceutical industry is further supporting market growth.

Pharmaceutical grade accounts for the largest revenue share at 42% of the global chitosan market in 2026, driven by its commanding price premium, certified manufacturers extract multiples of industrial-grade pricing per kilogram from CDMO, and pharma manufacturer buyers locked into specification-compliant supply agreements.

Competitive stability is reinforced by the high capital and regulatory cost of entry, though producers who fail to maintain USP and Ph. Eur. monograph compliance face rapid contract loss to alternative certified suppliers, making quality system investment a non-negotiable competitive requirement.

Asia Pacific dominates the global chitosan market with a 39% share, underpinned by the region's control over global crustacean aquaculture output, according to FAO. Asia accounts for over 85% of global aquaculture production by volume, and by large-scale domestic water treatment infrastructure investment mandated under national environmental plans such as China's 14th Five-Year Plan.

The fungal chitosan production for pharmaceutical and vegan-certified nutraceutical applications is where KitoZyme S.A.'s fermentation-derived chitosan has demonstrated commercial viability outside the crustacean supply chain.

Primex ehf, KitoZyme S.A., Heppe Medical Chitosan GmbH, Golden-Shell Pharmaceutical Co. Ltd., and KIMICA Corporation are the leading companies in the chitosan market, competing primarily on purity grade certification, molecular weight consistency, and supply reliability, factors that matter more to pharmaceutical and biomedical buyers than unit price alone.