- Specialty & Fine Chemicals

- Bitumen Additives Market

Bitumen Additives Market Size, Share, and Growth Forecast 2026 - 2033

Bitumen Additives Market by Additive Type (Polymeric Modifiers, Anti-Strip Agents/Adhesion Promoters, Bitumen Emulsifiers, Warm Mix Additives, Chemical Modifiers, Antioxidants, Fiber Additives, Fillers), by Application (Road Construction, Roofing, Paints & Coatings, Industrial Flooring & Waterproofing, Others), by Regional Analysis, 2026 - 2033

Bitumen Additives Market Size and Trend Analysis

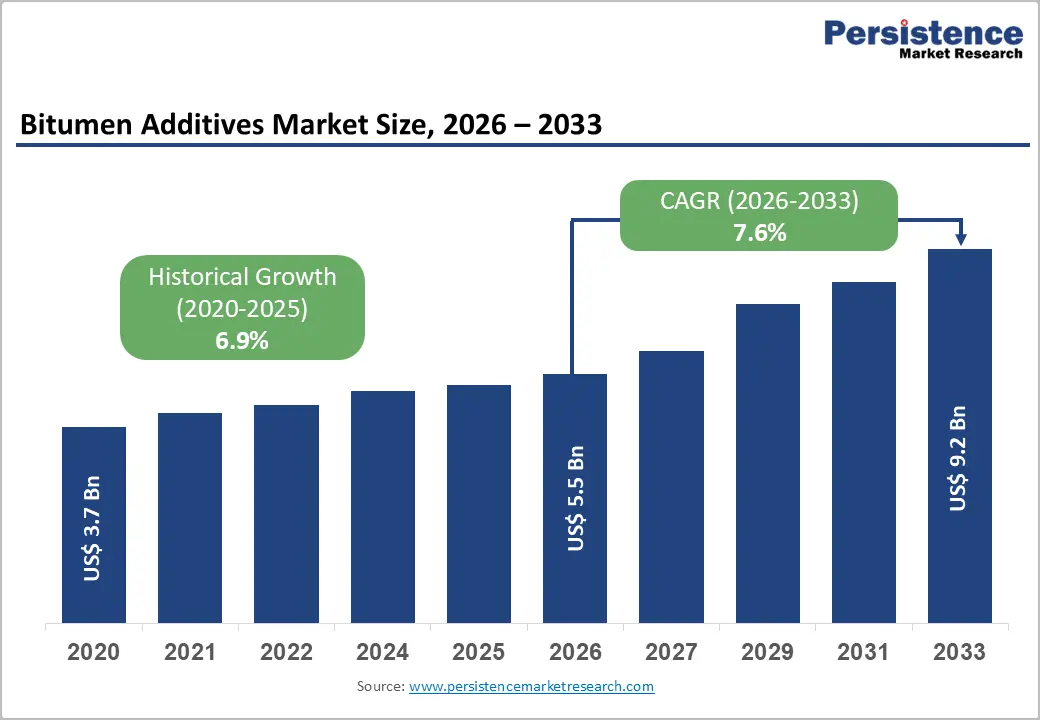

The global bitumen additives market size is expected to be valued at US$ 5.5 billion in 2026 and is projected to reach US$ 9.2 billion by 2033, growing at a CAGR of 7.6% between 2026 and 2033. This sustained growth is primarily driven by accelerating road construction and maintenance investments across emerging and developed economies, combined with tightening performance specifications for asphalt pavements.

The Asian Development Bank (ADB) estimates infrastructure investment needs in Asia alone at USD 1.7 trillion annually through 2030, directly fueling demand for performance-enhancing bitumen additives. Concurrently, the global transition toward low-energy paving technologies, particularly warm mix asphalt, is unlocking new additive chemistries and expanding the addressable market across construction, roofing, and waterproofing applications worldwide.

Key Industry Highlights

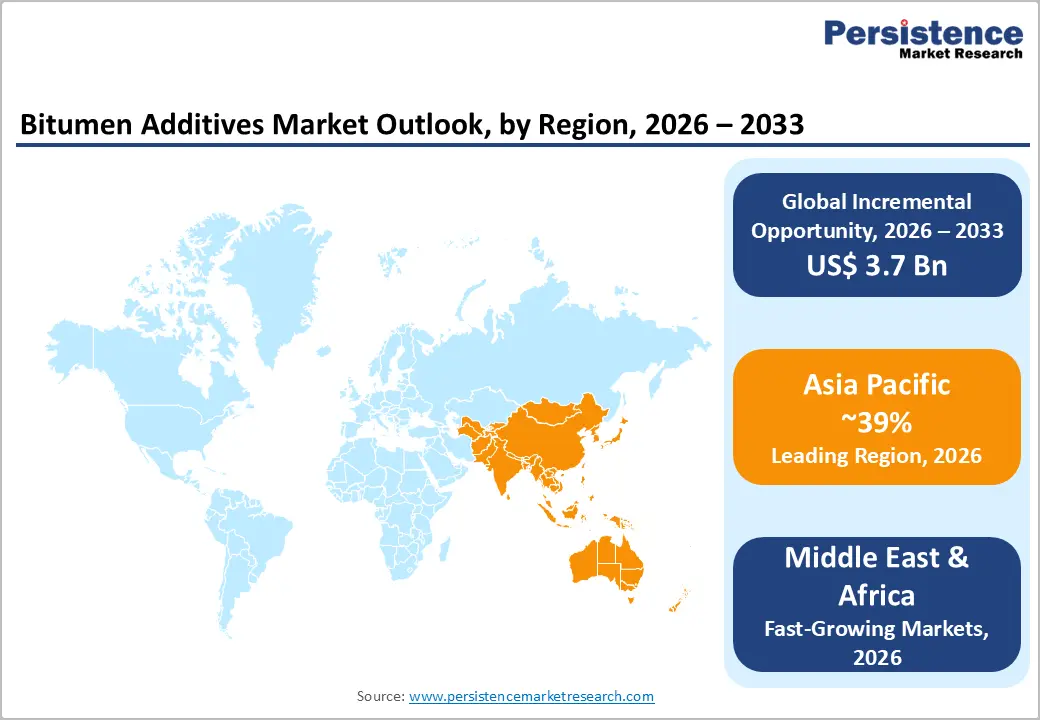

- Leading Region: Asia Pacific holds 39% of the global Bitumen Additives market in 2026, driven by China's 5.3 million km road network, India's Bharatmala Pariyojana highway program, and large-scale ASEAN infrastructure investment plans backed by ADB and World Bank financing.

- Fastest Growing Region: The Middle East & Africa region is the fastest growing market, propelled by Saudi Arabia's Vision 2030 infrastructure investments exceeding USD 1 trillion and the African Development Bank's USD 68–108 billion annual infrastructure gap mobilization across sub-Saharan road networks.

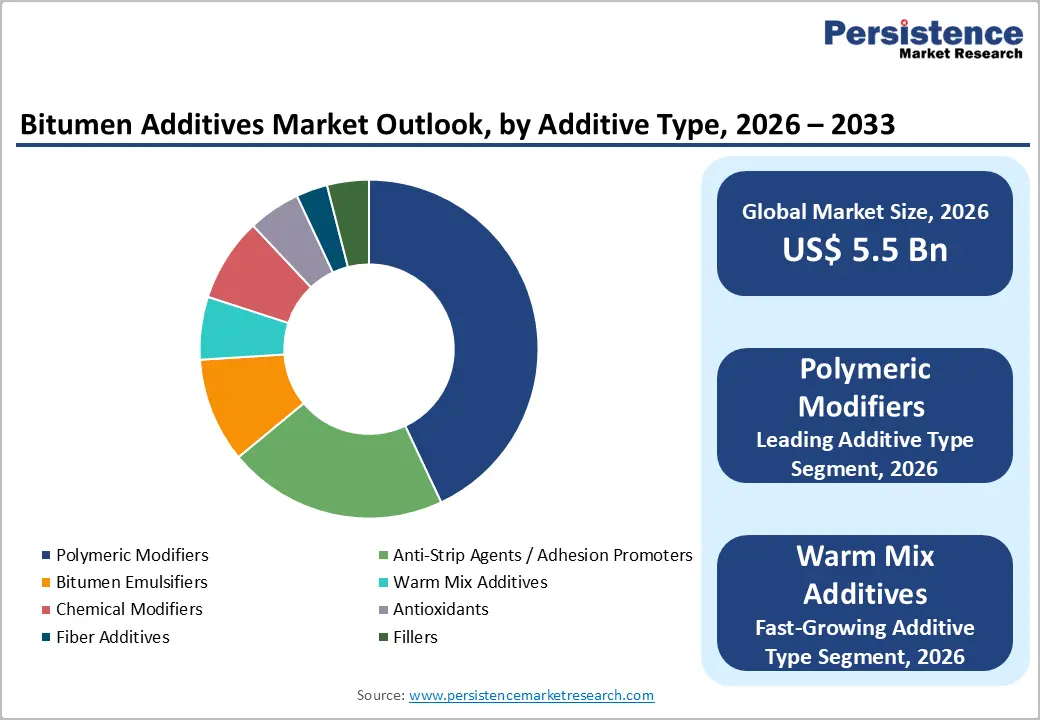

- Dominant Segment: Polymeric Modifiers command 43% of the Additive Type market in 2026, underpinned by AASHTO performance grade specifications and PIARC-documented 40–50% service life extensions for SBS and SBR-modified pavements versus unmodified bitumen on high-traffic corridors.

- Fastest Growing Segment: Warm Mix Additives are forecast at a 9% CAGR, driven by carbon-reduction procurement mandates, FHWA promotion of WMA technology in the U.S., and European asphalt producers targeting lower-energy, lower-emission paving processes under EU Green Deal sustainability requirements.

- Key Opportunity: Tightening REACH regulations and sustainability procurement criteria are creating a structural shift toward bio-based and low-VOC bitumen additives, with companies such as Kraton, Ingevity, and Arkema investing in next-generation sustainable modifier platforms to capture premium-priced green infrastructure contracts.

Market Dynamics

Driver - Sustained Infrastructure Investment and Road Construction Programs Worldwide

Global government commitments to road infrastructure upgrades are the most powerful demand catalyst for bitumen additives. In the United States, the Infrastructure Investment and Jobs Act (IIJA) allocated USD 110 billion specifically for roads, bridges, and major transportation projects, creating a decade-long procurement pipeline for modified and enhanced asphalt systems.

India's National Infrastructure Pipeline (NIP) earmarks over INR 111 trillion for infrastructure development through 2025, with road and highway construction constituting the largest single segment. The European Commission's TEN-T (Trans-European Transport Network) regulation mandates network completion by 2030 and 2050, generating sustained asphalt pavement demand. These structural investment cycles make polymer-modified bitumen and adhesion promoters indispensable for meeting durability, load-bearing, and performance lifecycle requirements.

Tightening Pavement Performance Standards Driving Adoption of Modified Bitumen Systems

Regulatory and engineering standards bodies worldwide are progressively mandating higher-performance bitumen specifications, directly benefiting the additives market. The American Association of State Highway and Transportation Officials (AASHTO) Performance Grade (PG) binder system and ASTM International standards increasingly specify polymer-modified bitumen for high-traffic and climate-stressed corridors.

In Europe, EN 14023 standard governs polymer-modified bitumen, while EN 13108 specifies bituminous mix requirements, both driving additive consumption. The World Road Association (PIARC) technical reports document that polymer-modified asphalt pavements achieve 40–50% longer service lives than conventional mixes, providing a compelling cost-benefit case for agencies to specify SBS, SBR, and EVA-modified bitumen systems in new and rehabilitated road networks globally.

Restraints - Crude Oil Price Volatility Disrupting Bitumen and Additive Cost Structures

Bitumen is a refinery by-product of crude oil, meaning its price and availability are intrinsically linked to crude oil market dynamics. The International Energy Agency (IEA) has documented crude oil price swings exceeding 30–40% within single calendar years, creating significant uncertainty in bitumen feedstock costs.

Since polymeric and chemical modifiers are themselves petrochemical derivatives, feedstock cost inflation cascades through the entire additive value chain. This dual exposure, both in bitumen substrate and modifier chemistry, compresses contractor margins and can delay or downscale infrastructure project procurement, particularly in public-sector programs operating under fixed budget frameworks.

Environmental and Regulatory Pressures on Petrochemical-Based Additives

Mounting environmental scrutiny of volatile organic compound (VOC) emissions and polycyclic aromatic hydrocarbon (PAH) content in bitumen and its additives is creating compliance complexity for manufacturers. The European Chemicals Agency (ECHA) has classified certain bitumen components under REACH regulations, imposing reformulation requirements on manufacturers.

Worker health and safety directives across the EU and North America are tightening permissible exposure limits for bitumen fumes, adding testing and formulation costs. These regulatory pressures require continuous R&D investment in cleaner additive chemistries, raising barriers to entry and increasing operating expenditure for smaller market participants.

Opportunities - Warm Mix Asphalt Additives: A High-Growth Technology Redefining Sustainable Paving

Warm Mix Asphalt (WMA) technology represents the most dynamic growth opportunity in the bitumen additives sector, forecast at a 9% CAGR from 2026 to 2033, the highest among all additive type segments. WMA additives allow asphalt mixing and compaction temperatures to be reduced by 20–40°C compared to hot mix asphalt, delivering tangible benefits: reduced fuel consumption, lower greenhouse gas emissions, and improved worker safety by cutting bitumen fume exposure.

The U.S. Federal Highway Administration (FHWA) has actively promoted WMA adoption through technology deployment programs, while the European Asphalt Pavement Association (EAPA) reports WMA's share of European asphalt production has been on a consistent upward trajectory. As sustainability reporting requirements and carbon procurement criteria become embedded in public infrastructure tenders, WMA additive manufacturers are positioned to capture structurally growing demand from government agencies targeting net-zero construction supply chains.

Middle East & Africa: Infrastructure Expansion Creating a Structurally New Demand Pool

The Middle East & Africa region is emerging as the fastest-growing geographic opportunity in the global bitumen additives market. In the Middle East, Saudi Arabia's Vision 2030 program is investing over USD 1 trillion in infrastructure, with major road network expansions forming a core component. The African Development Bank (AfDB) estimates the continent's infrastructure financing gap at USD 68–108 billion annually, with road infrastructure representing the largest deficit.

Programs such as the Programme for Infrastructure Development in Africa (PIDA) and bilateral Chinese Belt and Road Initiative (BRI) investments are mobilizing large-scale road construction procurement. The extreme climate conditions across the region, high UV exposure, temperature cycling, and heavy rainfall in sub-Saharan zones, demand high-performance modified bitumen, creating structural demand for polymeric modifiers, adhesion promoters, and antioxidant additives specifically engineered for harsh environmental conditions.

Category-wise Analysis

Additive Type Insights

Polymeric modifiers constitute the dominant segment within the additive type, likely to command 43% share in 2026. This leadership position is anchored in the unmatched performance improvements that polymer modification, primarily using Styrene-Butadiene-Styrene (SBS), Styrene-Butadiene-Rubber (SBR), and Ethylene-Vinyl-Acetate (EVA), delivers to asphalt binders: superior elasticity recovery, resistance to rutting and fatigue cracking, and extended pavement service life.

The World Road Association (PIARC) has documented service life extensions of 40–50% for polymer-modified pavements versus unmodified alternatives. As global infrastructure agencies increasingly mandate PG-graded binder specifications for high-traffic routes, the systemic adoption of SBS-modified bitumen for expressways, highways, and bridge decks continues to drive polymeric modifier consumption at above-market rates.

Application Insights

Road construction is the dominant application segment, accounting for approximately 60% market share in 2026. The primacy of this segment is directly tied to global public infrastructure investment cycles: road networks represent the single largest end-use for bitumen globally, with the International Road Federation (IRF) estimating over 64 million kilometers of paved roads worldwide requiring ongoing maintenance and expansion.

Performance demands on modern road networks, driven by heavier axle loads, climate stress, and extended design lives, mandate the systematic use of polymeric modifiers, adhesion promoters, and anti-stripping agents. Roofing represents the second-largest application, benefiting from construction activity and waterproofing standards across North America and Europe, where modified bitumen membrane systems are specified for commercial and industrial roofing applications under standards including ASTM D6163 and EN 13707.

Regional Analysis

North America Bitumen Additives Market Trends and Insights

North America holds approximately 23% of the global Bitumen Additives market in 2026, driven by the multi-year pipeline of road rehabilitation and construction investment unlocked by the U.S. Infrastructure Investment and Jobs Act (IIJA). Demand is further reinforced by stringent AASHTO performance grade binder specifications, high adoption of warm mix asphalt technology promoted by the FHWA, and a mature roofing waterproofing segment that systematically specifies modified bitumen membranes.

U.S. Bitumen Additives Market Size

The U.S. Bitumen Additives market is estimated at approximately US$ 1.0–1.1 billion in 2026, representing roughly 80% of North American demand. The IIJA's USD 110 billion road and bridge allocation is driving multi-year asphalt procurement, while the FHWA's Every Day Counts (EDC) program accelerates WMA technology adoption across state departments of transportation, directly benefiting warm mix additive and polymer modifier suppliers.

Europe Bitumen Additives Market Trends and Insights

Europe accounts for approximately 20% of global Bitumen Additives market share in 2026. The region is characterized by stringent EN 14023 and EN 13108 standards mandating performance-graded binders, a mature polymer-modified bitumen market, and growing adoption of low-temperature paving solutions in line with EU Green Deal decarbonization objectives. The rehabilitation backlog across European road networks, documented by PIARC, sustains steady baseline demand for adhesion promoters and antioxidants.

Germany Bitumen Additives Market Size

Germany represents the largest European market for bitumen additives, estimated at approximately US$ 380–420 million in 2026, accounting for around 35–37% of European demand. Germany's Bundesfernstraßen (Federal Trunk Roads) network, over 13,000 km of Autobahn, and large-scale federal road rehabilitation programs generate consistent premium demand for SBS-modified bitumen and high-performance adhesion promoters.

U.K. Bitumen Additives Market Size

The U.K. Bitumen Additives market is estimated at approximately US$ 200–230 million in 2026. The UK National Roads Fund and Highways England's Road Investment Strategy (RIS2) earmark over £27 billion for strategic road improvements through 2025, sustaining demand for modified binders. The UK's Warm Mix Asphalt adoption rate, promoted through Highways England specifications, is among the highest in Europe, driving warm mix additive consumption.

France Bitumen Additives Market Size

France represents approximately 15–17% of European Bitumen Additives demand, with a market estimated at US$ 180 million in 2026. USIRF (Union des Syndicats de l'Industrie Routière Française) data confirms France as one of Europe's most active road maintenance markets, with the National Road Maintenance Plan and departmental network rehabilitation driving systematic use of anti-strip agents and polymer modifiers to address aging infrastructure.

Asia Pacific Bitumen Additives Market Trends and Insights

Asia Pacific is the dominant region, holding a 39% share of the global Bitumen Additives market in 2026. China, the world's largest road construction market with over 5.3 million km of paved roads per National Bureau of Statistics of China, accounts for the single largest national demand pool, driving SBS modifier and emulsifier consumption at scale. India and Southeast Asian economies are rapidly scaling road infrastructure under national development plans, while Japan's market is characterized by mature quality standards and maintenance-driven demand for high-performance bitumen systems.

India Bitumen Additives Market Size

India's Bitumen Additives market is estimated at approximately US$ 320 million in 2026, supported by the Ministry of Road Transport and Highways (MoRTH) target of constructing 50 km of national highways per day. The National Highways Authority of India (NHAI) and Bharatmala Pariyojana program, targeting 34,800 km of highway development, are creating sustained long-term demand for polymer-modified bitumen and anti-stripping adhesion promoters suitable for India's diverse climate conditions.

Japan Bitumen Additives Market Size

Japan's Bitumen Additives market is estimated at approximately US$ 190 million in 2026, representing approximately 11–13% of Asia Pacific demand. Japan's market is mature and maintenance-driven, with the Ministry of Land, Infrastructure, Transport and Tourism (MLIT) overseeing a 1.3 million km road network that demands premium modified bitumen for seismic resilience, freeze-thaw durability, and high-traffic performance on the densely loaded expressway network.

Southeast Asia Bitumen Additives Market Size

Southeast Asia represents one of the most dynamic sub-regional growth pockets, with the market estimated at approximately US$ 170 million in 2026. ASEAN member states, particularly Vietnam, Indonesia, the Philippines, and Thailand, are executing large-scale national road development programs under their respective medium-term development plans and with support from ADB and World Bank project financing. High temperatures and tropical rainfall demand thermally stable, moisture-resistant bitumen formulations, creating targeted demand for adhesion promoters and antioxidant additives.

Competitive Landscape

The global Bitumen Additives market exhibits a moderately consolidated structure, with multinational specialty chemicals players, Kraton, Arkema, BASF, Evonik, Dow, Nouryon, and Ingevity, holding significant shares through proprietary polymer and chemical modifier technologies. Key differentiators include polymer architecture (SBS block structure, molecular weight distribution), application-specific formulation expertise, and technical service networks embedded with road authorities.

Strategies center on capacity expansions in Asia Pacific, bio-based feedstock integration for ESG alignment, and digital formulation tools. Vertically integrated bitumen majors, Shell Bitumen, TotalEnergies, Nynas, and Sinopec, compete by offering pre-modified binder systems directly to contractors, bypassing the standalone additive value chain in certain markets.

Key Developments

- In January 2025, Ingevity Corporation launched its next-generation Evotherm warm mix asphalt additive formulation, offering enhanced compaction performance at reduced temperatures, targeting adoption across U.S. state DOTs and European national road agencies pursuing carbon-reduction procurement criteria.

- In March 2024, Kraton Corporation announced expanded production capacity for its SYLVAROAD performance additives at its Berre-l'Étang, France facility, targeting growing European demand for bio-based warm mix and adhesion promoter solutions for sustainable road construction.

- In September 2024, Arkema S.A. announced strategic investment in bio-sourced polymer modifier R&D, aligning its bitumen additive portfolio with EU Green Deal sustainability mandates and positioning the company to address tightening VOC and PAH regulatory requirements in European road construction markets.

Companies Covered in Bitumen Additives Market

- Kraton Corporation

- Arkema S.A.

- Ingevity Corporation

- Nouryon

- BASF SE

- Evonik Industries AG

- Dow Inc.

- Sinopec

- TotalEnergies SE

- Shell Bitumen

- Nynas AB

- Huntsman Corporation

- Sasol Limited

- Colas Group

- AkzoNobel