- Industrial Goods & Service

- Collapsible Fuel Tank Market

Collapsible Fuel Tank Market Size, Share, Trends, Growth Analysis, 2026 - 2033

Collapsible Fuel Tank Market by Capacity (25-100 gallons, 3,000 gallons, 10,000 gallons, 50,000 gallons, 200,000 gallons), Fabric Material (Polyurethane, Composite Material), End-user (Agricultural Equipment, Construction Equipment, Military Vehicles, Commercial Vehicles, Marine Vessels, Mining Operations), and Region Analysis for 2026 to 2033

Collapsible Fuel Tank Market Trends & Analysis

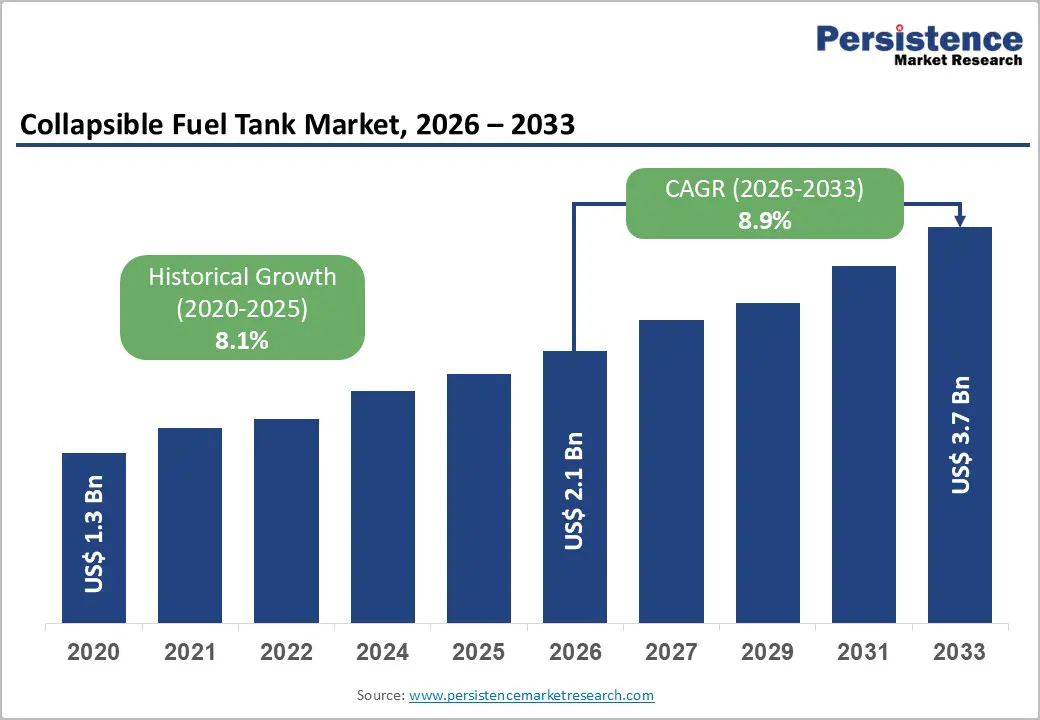

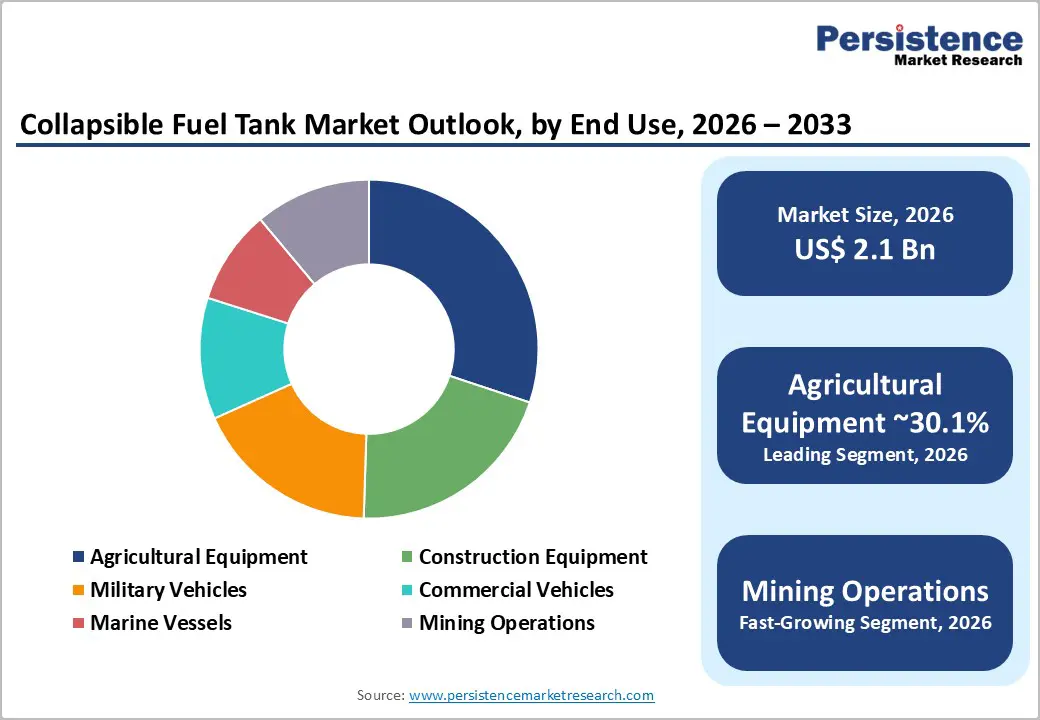

The global collapsible fuel tank market size is likely to be US$2.1 billion in 2026 and is projected to reach US$ 3.7 billion by 2033, growing at a CAGR of 8.9% between 2026 and 2033. The collapsible fuel tanks are redefining mobile energy logistics across every off-grid operational sector globally.

Expanding defense logistics modernization programs mandating portable fuel storage infrastructure, rapid agricultural mechanization in emerging economies increasing remote fuel storage demand, and advancement in high-strength polyurethane and composite fabric materials extending tank service life and chemical resistance are the primary drivers. The mining and construction sector expansion in the Asia Pacific and Africa is driving new large-capacity collapsible tank procurement for off-grid fuel logistics applications through 2033.

Key Industry Highlights:

- Leading Capacity Segment: 25-100 gallon tanks lead at 43.2% share; 200,000-gallon tanks grow fastest at 10.0% CAGR, driven by military forward base fuel farm and large-scale remote mining site bulk diesel pre-positioning procurement.

- Leading Fabric Material: Polyurethane leads at 62.4% share; composite material grows fastest at 9.6% CAGR, driven by aramid fiber-reinforced laminate adoption for extreme temperature military and mining deployment applications.

- Leading End-user: Agricultural equipment leads at 30.1% share; mining operations is likely to grow fast at 10.1% CAGR, supported by remote mine site greenfield diesel logistics infrastructure buildout across Africa, Central Asia, and Australia.

- Regional Leadership: North America is likely to reach a prominent 8.4% CAGR with the U.S. at US$ 421.7 Mn.

- Strategic Developments: ATL's U.S. Defense Logistics Agency contract (February 2025) and Continental AG's launch of the composite military bladder series (June 2024) are defining next-generation defense-grade collapsible fuel tank materials and procurement standards globally.

Market Dynamics Analysis

Drivers - Defense Sector Modernization Programs Driving Portable Fuel Storage Infrastructure Procurement

Global defense expenditure reached a record US$ 2.44 trillion in 2023 (Stockholm International Peace Research Institute), with NATO member states committing to 2% GDP defense spending targets generating sustained military logistics equipment procurement waves across North America and Europe. Collapsible fuel tanks meeting MIL-PRF-32233B military performance specifications, mandated for U.S. Army, Marine Corps, and NATO forward operating base fuel pre-positioning programs, represent a structurally non-discretionary procurement category directly linked to defense budget expansion cycles. The U.S. Defense Logistics Agency's bulk fuel storage modernization program allocated over US$340 Mn to portable fuel infrastructure in FY2024.

Military collapsible fuel tanks are deployed in helicopter forward arming and refueling points (FARPs), expeditionary airfield fuel systems, and disaster relief pre-positioning operations, each requiring rapid deployment, low transport cube, and chemical compatibility across JP-8, diesel, and AVGAS fuel types. Since 2022, NATO's Enhanced Forward Presence in Eastern Europe has materially increased demand for forward-deployable, collapsible fuel storage systems among Allied member defense logistics commands. Continental AG's military-certified collapsible tank division and Aero Tec Laboratories' aviation fuel bladder programs are directly scaling production capacity to meet intensifying defense and sector procurement demand through 2033.

Agricultural Mechanization Expansion in Emerging Economies Generating Remote Diesel Storage Demand

The United Nations Food and Agriculture Organization (FAO) estimates that global agricultural machinery stock must expand by 30% by 2030 to meet projected food production requirements, with mechanization investment concentrated in Sub-Saharan Africa, South Asia, and Southeast Asia, where farm electrification infrastructure remains limited and diesel-powered tractors, irrigation pumps, and harvesting equipment operations require on-site portable fuel storage solutions. India's PM-KISAN agricultural mechanization scheme and Brazil's MODERFROTA equipment financing program are driving rapid tractor fleet growth across large-scale farming operations, where collapsible fuel bladders provide the optimal solution for remote fuel management.

Collapsible fuel tanks deployed in agricultural settings offer critical operational advantages over rigid fixed tanks, roll-up portability enabling repositioning across seasonal field operations, zero residual fuel waste through complete collapse on emptying, and compliance with EPA Spill Prevention, Control, and Countermeasure (SPCC) regulations governing on-farm fuel storage in the U.S. The global agricultural equipment market is projected to exceed US$ 280 Bn by 2033 (FAO/OECD Agricultural Outlook), with collapsible fuel tank addressable procurement scaling proportionally as mechanized farming penetration expands into remote and semi-arid agricultural zones across Asia Pacific, Latin America, and Africa, sustaining Agricultural Equipment as the leading end-use segment through 2033.

Restraints - Stringent Regulatory Compliance Requirements for Fuel Storage Certification Across Multiple Jurisdictions

Collapsible fuel tanks deployed across military, commercial, and industrial end-users must comply with overlapping certification frameworks, including MIL-PRF-32233B (U.S. military fuel bladders), EPA SPCC rules (on-site fuel storage over 1,320 gallons), UN ADR dangerous goods transport regulations (Europe), and AS/NZS 1940 flammable liquids storage standards (Australia).

Each jurisdiction imposes distinct material testing, seam strength, chemical permeability, and installation documentation requirements, adding 6-18 months to certification timelines per new product configuration. Non-compliance with applicable fuel storage regulations exposes operators to fines quantified at US$ 25,000-US$ 70,000 per violation per day under EPA SPCC enforcement, constraining adoption velocity among cost-sensitive agricultural and construction operators globally.

Competition from Rigid Intermediate Bulk Containers (IBCs) and Modular Steel Tank Systems

Collapsible fuel tanks compete structurally with rigid intermediate bulk containers (IBCs), ISO-certified modular steel tank systems, and skid-mounted diesel storage units, which retain operational preference among fixed-site industrial operators prioritizing long-term durability, secondary containment integration, and established regulatory compliance documentation over collapsible system portability advantages. Steel modular tank systems, offered by Western Global, Fuel Proof, and Harlequin, are deeply embedded in construction site fuel management procurement specifications across the U.K., Australia, and the Middle East, where contract-standard fuel storage requirements reference rigid tank configurations. This competitive substitution risk is estimated to constrain collapsible tank penetration in fixed industrial site applications by 20-25% of the addressable market through the forecast period.

Opportunities - Large-Capacity Mining Sector Collapsible Tank Deployment in Remote African and Asian Operations

Expanding mineral extraction operations across Sub-Saharan Africa, Central Asia, and remote Australian territories, where rigid fixed fuel infrastructure is impractical and diesel supply chain logistics require flexible bulk storage solutions, are creating substantial greenfield procurement demand for large-capacity (10,000-50,000 gallon) collapsible fuel tanks.

The International Council on Mining & Metals (ICMM) documented a 14% increase in new mine development project approvals in 2023, with the majority located in regions lacking permanent fuel infrastructure. Each new remote mine site requires 50,000-200,000 gallons of on-site diesel capacity, which directly translates into multi-unit, large-capacity collapsible tank procurement events.

Mining operations are the fastest-growing end-use segment at 10.1% CAGR, with BHP, Rio Tinto, and Glencore mining contractors increasingly specifying collapsible fuel bladder systems for remote exploration camp fuel management under environmental containment compliance requirements. The global mining equipment fuel logistics market is estimated at US$ 4.5 Bn by 2030, with collapsible tank addressable penetration representing an estimated US$ 0.6-0.8 Bn incremental opportunity as mining operators transition from rigid IBC to portable bladder systems for enhanced operational flexibility and reduced infrastructure establishment costs across geographically constrained remote mine development programs.

Disaster Relief and Emergency Response Pre-Positioning Programs as an Institutional Procurement Channel

National emergency management agencies, humanitarian organizations, and military rapid-response units are progressively mandating collapsible fuel tank pre-positioning within disaster preparedness inventories, recognizing that post-disaster infrastructure collapse renders fixed fuel systems inoperable while collapsible bladder systems enable first-responder generator, vehicle, and aviation fuel supply continuity within hours of deployment. FEMA's National Response Framework identifies portable fuel storage as a Tier-1 critical infrastructure resilience requirement, with U.S. state emergency management offices procuring pre-positioned collapsible tank inventories for hurricane, earthquake, and wildfire response scenarios.

The UNHCR, World Food Program, and International Federation of Red Cross societies collectively operate humanitarian response programs across 60+ active emergency settings annually, each requiring deployable fuel storage for generator power, vehicle fleets, and water pumping infrastructure. This institutional emergency response procurement channel represents an estimated US$ 0.3-0.5 Bn addressable market by 2030, growing at approximately 9% CAGR as climate-driven disaster frequency increases and international humanitarian organizations systematically expand pre-positioned emergency logistics equipment stockpiles under UN Office for the Coordination of Humanitarian Affairs preparedness frameworks.

Category-wise Analysis

Capacity Insights

25-100 gallon tanks lead the capacity segment with a 43.2% share in 2026. Small-capacity collapsible tanks dominate through their universal applicability across the broadest and most frequent-purchase end-use scenarios, agricultural field operations requiring portable tractor diesel storage, military forward patrol unit fuel pre-positioning, construction equipment site refueling, and recreational marine and off-road vehicle applications. The 25-100 gallon range's low unit weight when empty, ease of single-operator deployment, and compatibility with standard pump and nozzle fuel dispensing equipment make them the most accessible entry point across all buyer segments. While large-capacity 10,000-200,000 gallon systems are growing by value, unit volume leadership firmly positions the 25-100 gallon range as the dominant capacity segment through 2033.

200,000-gallon tanks are the fastest-growing capacity segment at 10.0% CAGR through 2033. Military forward operating base fuel farm pre-positioning programs, large-scale mining camp bulk diesel storage contracts, and disaster relief strategic fuel reserve procurement by national emergency management agencies are driving demand for very large-capacity collapsible fuel storage systems across defense and industrial sectors.

Fabric Material Insights

Polyurethane is likely to lead the fabric material segment with a 62.4% share in 2026. Polyurethane's segment dominance reflects its proven performance characteristics across collapsible fuel tank applications, including superior hydrocarbon resistance across diesel, gasoline, JP-8, and AVGAS fuel types, high tensile strength-to-weight ratio enabling large-capacity configurations without structural failure risk, and extended UV and abrasion resistance supporting multi-year field deployment cycles. Polyurethane tanks meeting MIL-PRF-32233B military specifications and EPA SPCC regulatory compliance requirements represent the established procurement standard across defense, agricultural, and industrial end-users. Composite Material tanks are gaining share through enhanced chemical resistance and weight optimization, but polyurethane's regulatory approval depth and supply chain maturity sustain its leadership through 2033.

Composite Material is the fastest-growing fabric material at 9.6% CAGR through 2033. Advanced fiber-reinforced composite fabric architectures delivering enhanced tensile strength, reduced permeability, and improved temperature resistance for extreme environment deployments, particularly mining and aerospace applications, are driving composite material collapsible tank adoption across premium specification end-users globally.

End-user Insights

Agricultural equipment is likely to lead the end-user segment with a 30.1% market share in 2026. Agricultural equipment's segment leadership reflects the global agricultural machinery fleet's structurally continuous diesel consumption requirements across remote field operations where fixed infrastructure fueling is impractical, generating the highest unit-volume procurement frequency across all collapsible tank end-use categories. FAO data confirms 600+ million agricultural holdings globally consume diesel as the primary farm mechanization energy source, with collapsible tanks serving as the optimal portable fuel management solution across large-format farms in developing economies. Construction, military, and marine segments occupy significant complementary shares, but agricultural procurement volume frequency sustains the segment's leading position through 2033.

Mining operations is the fastest-growing end-user at 10.1% CAGR through 2033. Remote mine site greenfield development in Africa, Central Asia, and Australia, driving large-capacity diesel pre-positioning requirements, environmental containment compliance mandates compelling replacement of uncontained rigid fuel storage, and BHP, Rio Tinto, and Glencore contractor specification adoption are collectively accelerating mining segment collapsible tank procurement.

Regional Market Insights

North America Collapsible Fuel Tank Market Insights

North America is growing at a prominent 8.4% CAGR through 2033, anchored by the U.S.'s deep defense sector collapsible fuel tank procurement base, large-format agricultural operation remote fuel storage demand, and EPA SPCC regulatory compliance investment driving systematic fuel bladder adoption across commercial and industrial operators. Defense Logistics Agency forward fuel infrastructure modernization, FEMA disaster preparedness pre-positioning programs, and U.S. Army Corps of Engineers construction project portable fuel management requirements collectively sustain high-frequency procurement across all capacity categories.

U.S. Collapsible Fuel Tank Market: Defense Procurement Leadership and Agricultural Scale Demand

The U.S. market is estimated at US$ 421.7 Mn in 2026, driven by Aero Tec Laboratories' and GTA Containers' military-grade bladder system contracts, SEI Industries' agricultural and wildfire response tank deployments, and EPA SPCC compliance upgrade investment across Midwest grain farming operations. Canada contributes oil sands and remote mining camp portable fuel storage procurement across Alberta and British Columbia through 2033.

Europe Collapsible Fuel Tank Market Insights

Europe held a 21.4% share of the global collapsible fuel tank market in 2025, supported by NATO defense logistics modernization programs across Eastern European member states, EU ATEX-compliant portable fuel storage regulatory enforcement, and Continental AG's and Meggitt's specialty military and aviation fuel bladder production sustaining European manufacturing leadership in premium specification collapsible tank systems.

Germany Collapsible Fuel Tank Market: NATO Procurement and Industrial Compliance Investment

Germany's market is estimated at US$ 108.3 Mn in 2026, anchored by Bundeswehr logistics modernization, collapsible fuel tank procurement, and Continental AG's military-certified bladder tank manufacturing programs. The U.K. contributes to Avon Engineered Fabrications' defense and marine fuel bladder production and North Sea offshore support vessel portable tank deployments. France sustains Foreign Legion and NATO logistics collapsible fuel infrastructure investment, while Spain contributes agricultural sector demand across Castile and Andalusia large-format farming operations through 2033.

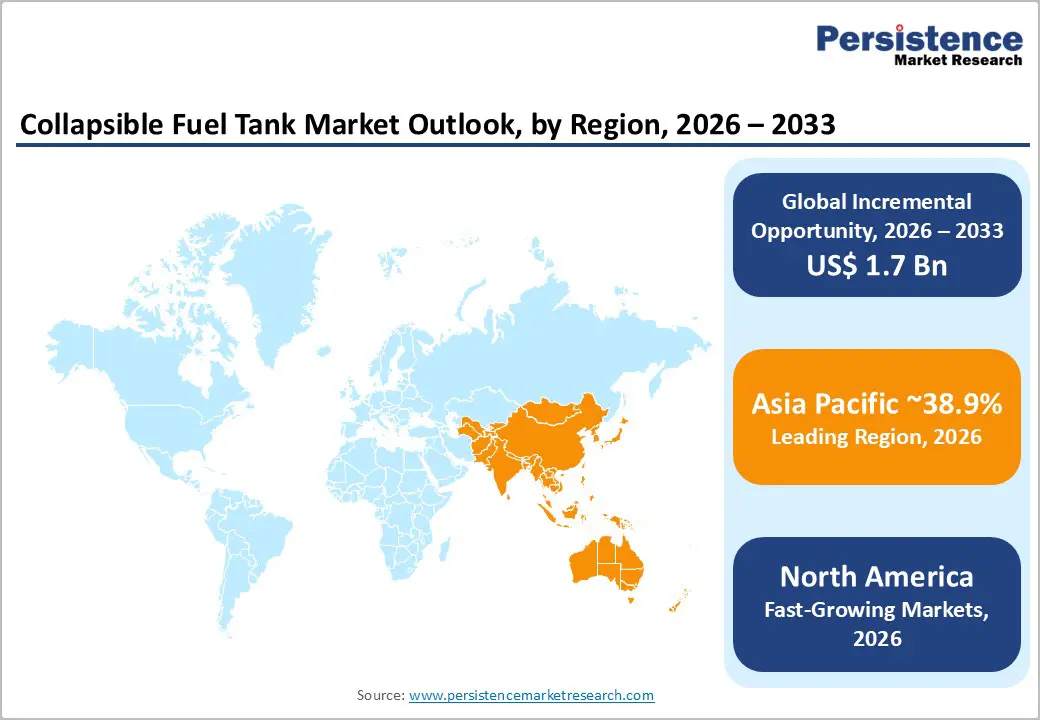

Asia Pacific Collapsible Fuel Tank Market Insights

Asia Pacific is the fastest-growing regional market at 9.6% CAGR through 2033, driven by rapid agricultural mechanization in India and Southeast Asia, generating portable diesel storage demand, expanding remote mining operations across Australia, Indonesia, and Mongolia requiring large-capacity fuel pre-positioning, and People's Liberation Army logistics modernization programs driving Chinese military collapsible fuel tank procurement at scale.

China Collapsible Fuel Tank Market: Agricultural Mechanization and Mining Logistics Driving Volume

China's market is estimated at US$ 331 Mn in 2026, driven by PLA logistics fuel bladder procurement, SINOPEC remote oilfield fuel management deployments, and rapidly expanding agricultural mechanization under China's Rural Revitalization Strategy. India's market at US$ 110 Mn is growing through PM-KISAN farm mechanization, diesel storage demand, and Indian Army forward fuel pre-positioning programs. Australia sustains BHP and Rio Tinto's remote mining site large-capacity collapsible tank procurement through 2033.

Competitive Landscape

The global collapsible fuel tank Market is moderately fragmented, with Aero Tec Laboratories, SEI Industries, and GTA Containers collectively holding an estimated 35-40% combined revenue share, differentiating through MIL-PRF-32233B military certification depth, proprietary RF-welded polyurethane seam technology, and application-engineered large-capacity configuration portfolios. Custom-engineered tank programs and defense framework contracts are emerging as primary business model differentiators beyond standard catalogue product supply.

Military-grade certification advancement, composite fabric material R&D investment for extreme environment applications, geographic expansion into Asia Pacific mining and agricultural markets, and strategic emergency response agency supply agreement development define the dominant competitive strategic themes shaping the global collapsible fuel tank market through 2033.

Key Developments:

- In February 2025, Aero Tec Laboratories secured a multi-year U.S. Defense Logistics Agency contract to supply MIL-PRF-32233B certified 50,000-gallon collapsible fuel bladder systems for NATO forward operating base fuel farm pre-positioning programs across Eastern European Allied defense logistics infrastructure.

- In October 2024, SEI Industries expanded its collapsible fuel tank product portfolio with a new agricultural-series diesel bladder system incorporating integrated secondary containment bunding and EPA SPCC-compliant quick-connect dispensing fittings, targeting large-format U.S. Midwest grain and livestock farming operations requiring remote diesel management.

Companies Covered in Collapsible Fuel Tank Market

- Aero Tec Laboratories (ATL)

- SEI Industries Ltd.

- GTA Containers Inc.

- Continental AG

- Meggitt PLC

- Avon Engineered Fabrications

- AMUFUEL

- Texas Boom Company

- Husky Portable Containment

- DOOWIN (Qingdao) Technology

- Shanghai BGO Industries Ltd.

- Flixtank

- Western Global

- SO.C.A.P

- Fleximake

Frequently Asked Questions

The collapsible fuel tank market is valued at US$ 2.05 Bn in 2026, projected to reach US$ 3.73 Bn by 2033.

Defense sector logistics modernization mandating portable fuel pre-positioning infrastructure and agricultural mechanization expansion across emerging economies, generating remote diesel storage demand, are the primary growth drivers.

The collapsible fuel tank market is projected to grow at a CAGR of 8.9% from 2026 to 2033.

Large-capacity collapsible tank deployment across remote mining operations in Africa and Asia Pacific and disaster relief emergency response institutional pre-positioning procurement programs represent the most actionable near-term growth opportunities.

Aero Tec Laboratories, SEI Industries, GTA Containers, Continental AG (ContiTech), Meggitt PLC, Avon Engineered Fabrications, AMUFUEL, Texas Boom Company, Husky Portable Containment, and DOOWIN Technology are the leading global participants.