- Industrial Goods & Service

- Automatic Fireball Extinguisher Market

Automatic Fireball Extinguisher Market Size, Share, and Growth Forecast 2026 - 2033

Automatic Fireball Extinguisher Market by Agent Type (Dry Powder, Carbon Dioxide, Foam, Others), Weight (Up to 2 Kg, 2.1-10 Kg, Above 10 Kg), Fire Type (Class A, Class B, Class C, Class D, Class K), Application (Residential, Commercial, Industrial, Automotive, Others), and Regional Analysis for 2026 - 2033

Automatic Fireball Extinguisher Market Size and Trend Analysis

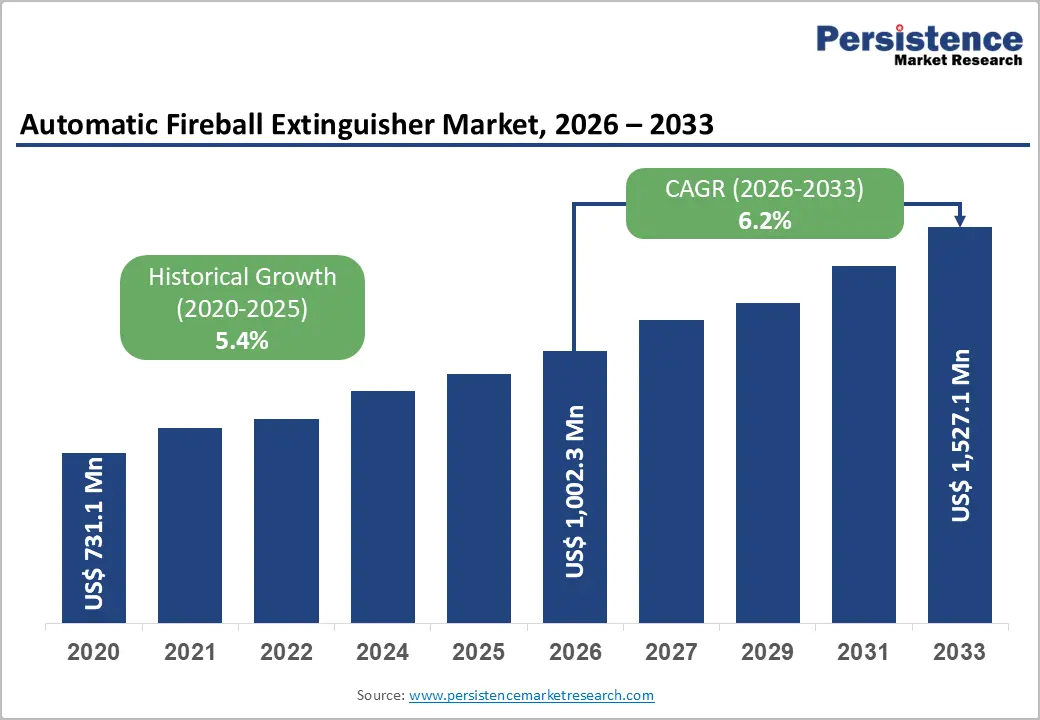

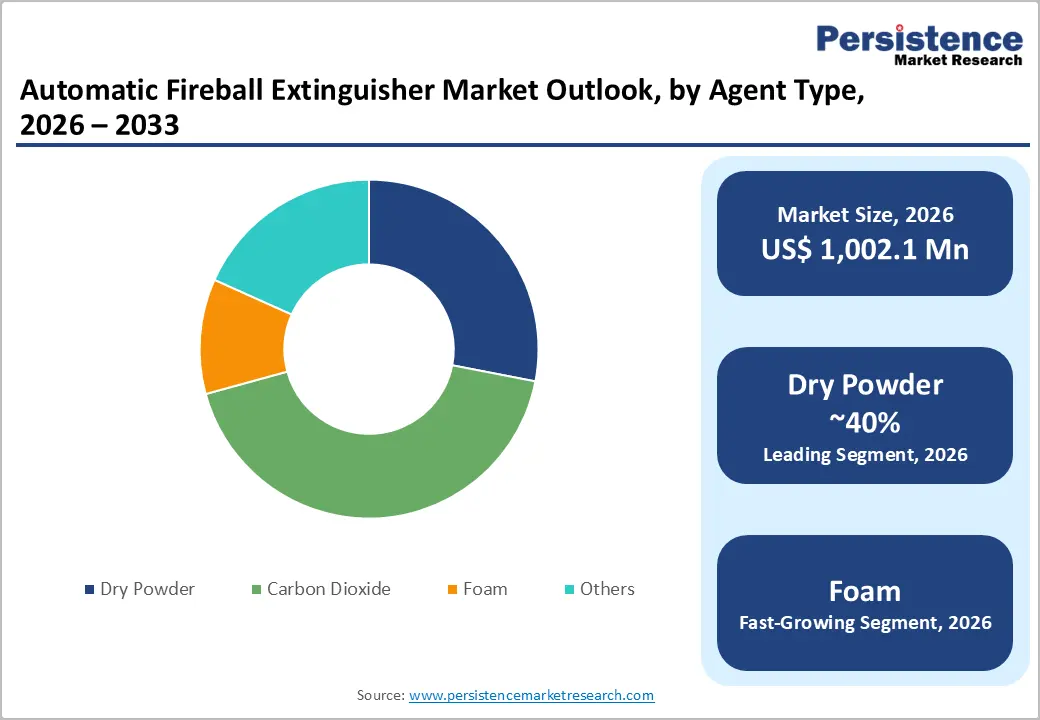

The global automatic fireball extinguisher market is valued at US$ 1002.3 Mn in 2026 and is projected to reach US$ 1,527.1 Mn by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

Rising incidences of industrial fires, increasingly stringent fire safety regulations enforced by governments worldwide, and growing adoption of automatic fire suppression systems across residential and commercial sectors are the primary drivers of this market. The U.S. Fire Administration (USFA) reported over 1.3 million fire incidents annually in the United States alone, reinforcing the urgent need for proactive fire suppression solutions.

Key Industry Highlights:

- Leading Region - North America holds approximately 34% of global market revenue, supported by robust regulatory mandates from NFPA and OSHA, extensive industrial activity, and rising EV infrastructure fire safety requirements.

- Fast-Growing Market - Asia Pacific is the fast-growing region, projected at a CAGR of 7.5%+ through 2033, driven by urbanization, industrial growth, and strengthening fire safety regulations in China and India.

- Dominant Segment - The industrial application segment leads with approximately 38% market share, propelled by high fire risk environments in manufacturing, chemical, and power generation facilities requiring mandatory automatic suppression systems.

- Fastest Growing Segment - The automotive segment is the fastest-growing application, fueled by surging EV adoption and the critical need for automatic lithium-ion battery fire suppression in vehicles and charging infrastructure globally.

- Key Opportunity - Expanding EV infrastructure and smart building construction present high-value opportunities for manufacturers offering IoT-enabled, battery-compatible automatic fireball extinguisher systems with remote monitoring capabilities.

DRO Analysis

Drivers - Stringent Fire Safety Regulations and Building Codes

Governments across North America, Europe, and Asia Pacific have significantly tightened fire safety mandates over the past decade, compelling building owners, industrial facility operators, and automotive manufacturers to install automated fire suppression systems. In the European Union, the Construction Products Regulation (CPR) and EN 3 standards mandate specific fire suppression capabilities across commercial and industrial buildings

In the United States, the National Fire Protection Association (NFPA) Standard 10 governs portable fire extinguishers and is updated regularly to incorporate automatic systems. Compliance requirements are now extending to logistics warehouses, data centres, and electric vehicle (EV) charging infrastructure, creating a sustained and legally backed demand pipeline for automatic fireball extinguisher manufacturers across the forecast period.

Rapid Growth of Industrial and Automotive Sectors

The expansion of heavy industry, oil & gas facilities, chemical manufacturing plants, and the automotive sector, particularly the electrification of fleets, has intensified the need for reliable, self-activating fire suppression devices. According to the International Energy Agency (IEA), the global electric vehicle fleet surpassed 40 million units in 2023, and lithium-ion battery fires present a unique and escalating challenge for traditional extinguishing methods.

Automatic fireball extinguishers, which activate upon heat or flame contact without human intervention, are increasingly being integrated into engine compartments, battery bays, and industrial control rooms. This trend is further reinforced by insurers mandating automatic suppression installations as a prerequisite for industrial facility coverage, directly stimulating procurement volumes across global markets.

Restraints - High Initial Installation and Maintenance Costs

Despite growing awareness of fire safety, the relatively high capital expenditure associated with automatic fireball extinguisher systems remains a significant deterrent, particularly for small and medium-sized enterprises (SMEs) and residential consumers in price-sensitive markets. Installation costs in commercial facilities can range from US$ 1,000 to US$ 5,000 per unit depending on agent type, system complexity, and site requirements.

Furthermore, recurring maintenance, inspection, and agent-refill obligations add to the total cost of ownership, limiting adoption in developing economies. This cost barrier is especially pronounced in rural infrastructure projects across Sub-Saharan Africa and Southeast Asia, where budget constraints restrict comprehensive fire safety investments.

Limited Awareness and Technical Expertise in Emerging Markets

In several emerging economies across Africa, South Asia, and Latin America, inadequate awareness of automatic fire suppression benefits, combined with a shortage of certified installation professionals, continues to constrain market penetration. The World Bank has noted that fire safety infrastructure deficits are significantly more pronounced in low- and middle-income countries.

Without sufficient technical training programs and regulatory enforcement, widespread adoption of automatic fireball extinguisher systems remains limited. Distributors face challenges in educating procurement decision-makers, and the lack of locally manufactured products further compounds affordability and availability issues, collectively dampening overall market expansion potential in these high-growth geographies.

Opportunities - Integration with Smart Building and IoT Fire Safety Ecosystems

The proliferation of smart buildings and connected infrastructure presents a compelling growth avenue for automatic fireball extinguisher manufacturers. Integration with Internet of Things (IoT) platforms enables real-time monitoring of extinguisher status, automated alerts, predictive maintenance scheduling, and seamless activation coordination with building management systems (BMS). According to online sources, the global smart building market is projected to exceed US$ 570 billion by 2030.

As green building certifications such as LEED and BREEAM increasingly incorporate fire safety automation as a scoring criterion, demand for IoT-compatible fireball extinguisher solutions is expected to accelerate. This opens significant opportunities for manufacturers willing to invest in connectivity-enabled product lines and partner with smart building technology integrators to offer bundled fire safety solutions.

Expansion into Electric Vehicle (EV) and Energy Storage Applications

The global transition toward electric mobility and battery energy storage systems (BESS) is creating a high-value, rapidly growing niche for specialized automatic fire suppression. Lithium-ion battery thermal runaway fires characterized by intense heat, toxic fume release, and re-ignition potential require purpose-designed suppression agents, making conventional extinguishers inadequate.

Department of Energy (DOE) and the European Battery Alliance (EBA) have both emphasized the need for dedicated suppression technologies within EV charging stations and grid-scale energy storage facilities. Companies developing automatic fireball extinguishers with Class D or next-generation electrolyte-compatible agents stand to capture premium pricing and long-term service contracts. Government incentive schemes for EV infrastructure under programs like the U.S. Bipartisan Infrastructure Law and the EU Green Deal further amplify this market opportunity.

Category-wise Analysis

Agent Type Insights

Among the various agent types, the Dry Powder segment commands the leading share of approximately 42% of the total automatic fireball extinguisher market. Dry powder agents particularly monoammonium phosphate and sodium bicarbonate-based formulations are widely favoured due to their broad-spectrum effectiveness against Class A, B, and C fires, cost-effectiveness, and non-conductivity, making them suitable for both industrial and residential applications.

The NFPA categorizes dry chemical agents among the most versatile suppression media. Their long shelf life, compatibility with harsh environmental conditions, and relative ease of handling further enhance their adoption in automotive, mining, and manufacturing sectors. Ongoing product enhancements focused on reducing post-fire cleanup challenges are expected to sustain the dominance of dry powder agents through the forecast period.

Weight Insights

The 2.1-10 Kg weight segment holds the largest market share at approximately 49%, reflecting its strong suitability across the widest range of use cases. Extinguishers in this weight category strike an optimal balance between suppression capacity and ease of deployment, making them the preferred choice for commercial establishments, light industrial settings, and automotive applications.

EN 3 European standards and NFPA 10 guidelines both recommend mid-weight extinguishers as the standard configuration for general hazard environments. The segment benefits from its versatility across Class A, B, and C fire types, broad retail availability, and compatibility with most automatic activation mechanisms. Growing commercial construction activity globally continues to generate consistent demand for this segment.

Fire Type Insights

The Class B fire type segment holds the largest market share, estimated at approximately 35%, driven by the prevalence of flammable liquid and gas fire risks across oil & gas, chemical processing, and transportation sectors. Class B fires involving substances such as gasoline, diesel, solvents, and liquefied petroleum gas are among the most frequent and destructive in industrial environments.

According to the U.S. Bureau of Labor Statistics, flammable liquid fires account for a significant proportion of workplace fire fatalities. Automatic fireball extinguishers engineered for Class B suppression are standard requirements in fuel storage facilities, refineries, and commercial vehicle fleets, ensuring consistent procurement demand. Regulatory requirements across the EU ATEX Directive and OSHA 29 CFR 1910.157 further mandate Class B-rated systems in applicable facilities.

Application Insights

Industrial application accounts for the largest revenue contribution, representing approximately 38% of the market. Industrial facilities encompassing manufacturing plants, chemical storage sites, power generation units, warehouses, and mining operations face elevated fire risks due to the presence of flammable materials, high-voltage equipment, and continuous operations. According to OSHA, industrial fires and explosions account for billions of dollars in property losses annually in the United States alone.

Automatic fireball extinguishers provide critical first-response suppression in environments where human intervention may be delayed or dangerous. The increasing complexity of industrial processes, combined with tightening occupational safety mandates from bodies such as the International Labour Organization (ILO), continues to drive widespread procurement across the industrial application segment.

Regional Insights

North America Automatic Fireball Extinguisher Market Trends & Analysis

North America remains the dominant regional market, accounting for approximately 34% of global revenue, underpinned by mature fire safety regulatory frameworks, high industrial activity, and substantial commercial and residential construction investment. The NFPA and the Occupational Safety and Health Administration (OSHA) enforce stringent compliance standards that necessitate regular installation and maintenance of fire suppression systems. The region's growing adoption of automatic fire suppression in EV charging stations, data centres, and smart commercial buildings further supports market expansion.

U.S. Automatic Fireball Extinguisher Market Size

The United States occupies a large share within North America, contributing over 82% of regional revenue. With more than 1.3 million fire incidents recorded annually by the USFA, demand for proactive automatic suppression remains consistently high across commercial, industrial, and automotive segments. The country's large fleet of industrial facilities, expanding EV infrastructure, and robust building permit activity collectively sustain strong procurement volumes.

Europe Automatic Fireball Extinguisher Market Trends, Drivers, & Insights

Europe is the fast-growing market, driven by harmonized fire safety standards under EN 3 and EN 1869, as well as active enforcement by national fire safety authorities. The European Union's ambitious Green Deal and Energy Performance of Buildings Directive (EPBD) are accelerating smart building retrofits, indirectly spurring demand for integrated fire suppression systems. Germany, the U.K., and France collectively account for most European market revenue, supported by dense industrial bases and advanced construction sectors.

Germany Automatic Fireball Extinguisher Market Size

Germany, as Europe's largest industrial economy, drives significant demand through its automotive manufacturing, chemical processing, and engineering sectors. Strict compliance with DIN EN 3 standards and the country's leadership in EV adoption, with over 2.5 million registered EVs as of 2023 (Kraftfahrtbundesamt)creates a growing niche for battery-specific automatic suppression solutions.

U.K. Automatic Fireball Extinguisher Market Size

The United Kingdom benefits from robust regulatory oversight by the Health and Safety Executive (HSE) and requirements stemming from the Regulatory Reform (Fire Safety) Order 2005. Post-Brexit updates to fire safety guidance have maintained high compliance standards across commercial and residential buildings, sustaining steady market demand.

France Automatic Fireball Extinguisher Market Size

France's market is supported by AFNOR NF EN 3 standards and growing industrial modernization investments. The French government's commitment to net-zero buildings and industrial decarbonization, backed by France Relance stimulus programs, is driving smart building upgrades that incorporate automatic fire suppression as a core safety feature.

Asia Pacific Automatic Fireball Extinguisher Market Drivers & Analysis

Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR exceeding 7.5% through 2033, fueled by rapid urbanization, industrial expansion, and strengthening national fire safety regulations across China, India, and Southeast Asia. The Asian Development Bank (ADB) projects infrastructure investment needs in the region to reach US$ 26 trillion by 2030, creating a vast addressable market for fire safety equipment.

China Automatic Fireball Extinguisher Market Size

China dominates the Asia Pacific market, underpinned by the Ministry of Emergency Management's active enforcement of the Fire Protection Law (2021 amendment). The country's massive industrial base, extensive high-rise construction activity, and the world's largest EV market with over 20 million new EVs sold in 2023 (China Association of Automobile Manufacturers) collectively make China the single largest national market in the Asia Pacific for automatic fireball extinguishers.

India Automatic Fireball Extinguisher Market Size

India represents a high-growth opportunity, supported by the National Building Code of India (NBC 2016) and government initiatives like Make in India and Smart Cities Mission. Industrial corridors such as the Delhi-Mumbai Industrial Corridor (DMIC) are generating significant demand for fire safety systems across new manufacturing and logistics facilities.

Japan Automatic Fireball Extinguisher Market Size

Japan's market is shaped by rigorous fire prevention standards enforced under the Fire Service Act and regulations administered by the Fire and Disaster Management Agency (FDMA). The country's aging industrial infrastructure and active seismic risk profile necessitate advanced automatic fire suppression in factories, warehouses, and commercial districts, sustaining steady procurement across the forecast period.

Competitive Landscape

The global automatic fireball extinguisher market exhibits a moderately fragmented structure, with a mix of established multinational corporations and regional specialists competing on product innovation, regulatory compliance, and distribution reach. Market leaders differentiate through proprietary agent formulations, broad product portfolios spanning multiple fire classes and deployment environments, and global service networks.

Key strategic moves include geographic expansion into high-growth Asia Pacific and Middle East markets, R&D investment in IoT-enabled smart suppression systems, and acquisitions of regional distributors to strengthen last-mile capabilities.

Key Developments:

- March 2025: Amerex Corporation announced the expansion of its automatic suppression product line with a new series of dry powder fireball extinguishers specifically engineered for lithium-ion battery fire suppression in EV charging stations across North America.

- November 2024: Firetrace International launched an upgraded automatic fire detection and suppression system for industrial machinery cabinets, integrating wireless IoT connectivity for real-time monitoring and remote diagnostics in manufacturing environments.

Companies Covered in Automatic Fireball Extinguisher Market

- UFI Filters

- Amerex Corporation

- Firetrace International

- Hochiki Corporation

- Minimax Viking GmbH

- Kidde (Carrier Global)

- Tyco Fire Protection Products

- Ansul (Johnson Controls)

Frequently Asked Questions

The global Automatic Fireball Extinguisher market is estimated at US$ 1002.3 Mn in 2026 and is projected to reach US$ 1,527.1 Mn by 2033, registering a CAGR of 6.2% during the forecast period. The market recorded a historical CAGR of 5.4% between 2020 and 2025.

The primary demand drivers include stringent fire safety regulations enforced by bodies such as the NFPA, OSHA, and the EU CPR; rising fire incidents across industrial and automotive sectors; and the rapid global expansion of electric vehicle infrastructure, which creates specialized demand for battery fire suppression solutions.

The Industrial application segment is the market leader, accounting for approximately 38% of global revenue. This dominance is driven by mandatory fire suppression requirements in manufacturing plants, chemical storage facilities, warehouses, and power generation units, as governed by international occupational safety standards.

North America is the leading regional market, contributing approximately 34% of global revenue. The region's leadership is attributed to mature regulatory frameworks, high industrial activity, significant commercial and residential construction investment, and rising adoption of automatic suppression in EV and smart building applications.

The integration of automatic fireball extinguishers with IoT-enabled smart building systems and the development of specialized suppression agents for lithium-ion battery and EV applications represent the most significant growth opportunities. Government-backed EV infrastructure programs and green building certifications are expected to generate sustained premium-priced demand for next-generation fire suppression solutions.

Prominent companies operating in the market include UFI Filters, Amerex Corporation, Firetrace International, Hochiki Corporation, Minimax Viking GmbH, Kidde (Carrier Global Corporation), Tyco Fire Protection Products (Johnson Controls), and Ansul (Johnson Controls), among others. These players compete on the basis of product innovation, regulatory compliance, distribution strength, and specialized application expertise.