- Marine

- Cable Laying Vessel Market

Cable Laying Vessel Market Size, Share, and Growth Forecast 2026 - 2033

Cable Laying Vessel Market by Cable Type (Power Cable, Communication Cable), End-User (Oil and Gas, Wind Farms, Telecommunications, Others), Capacity (Below 1000 Tons, 1000-3000 Tons, 3001-5000 Tons, 5001-7000 Tons, above 7000 Tons), and Regional Analysis for 2026 - 2033

Cable Laying Vessel Market Size and Trend Analysis

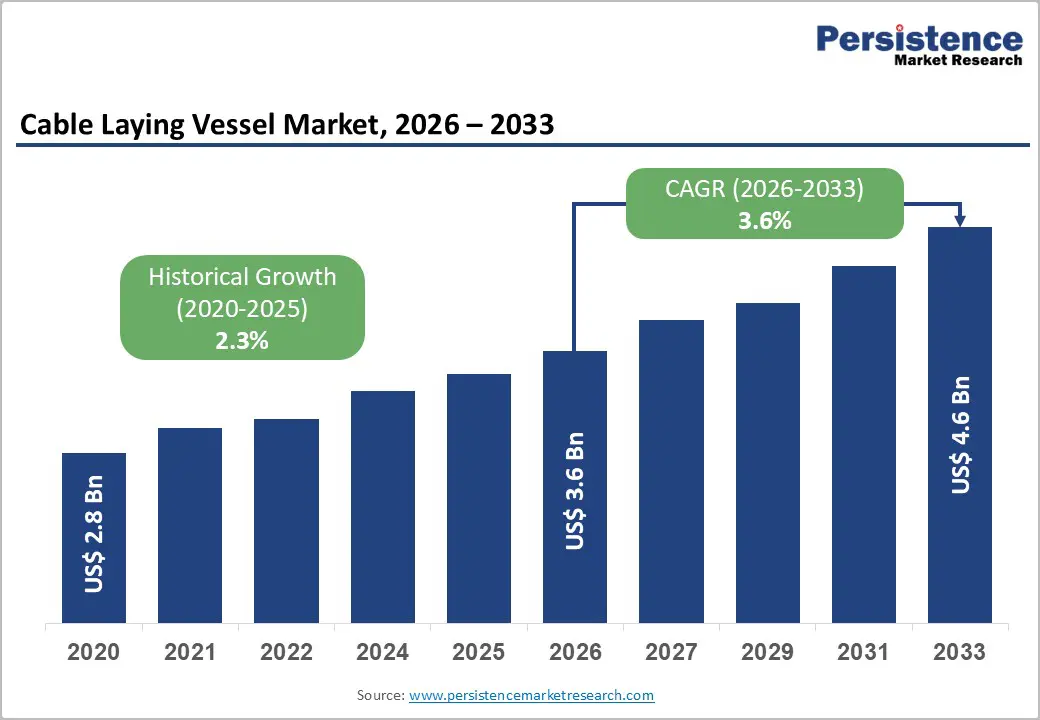

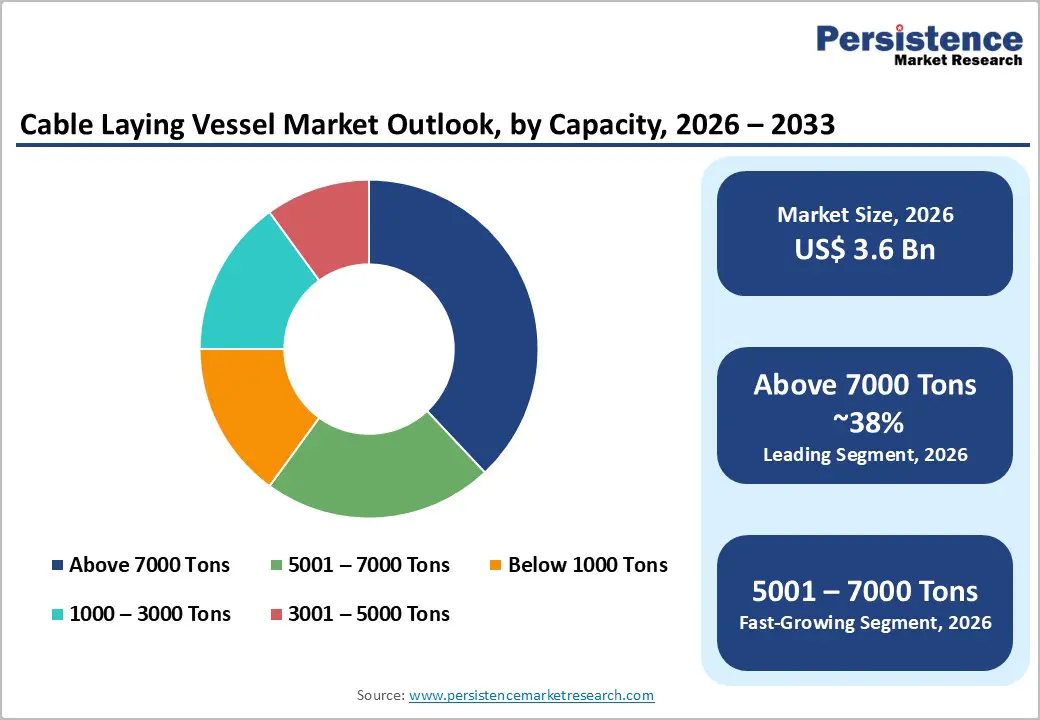

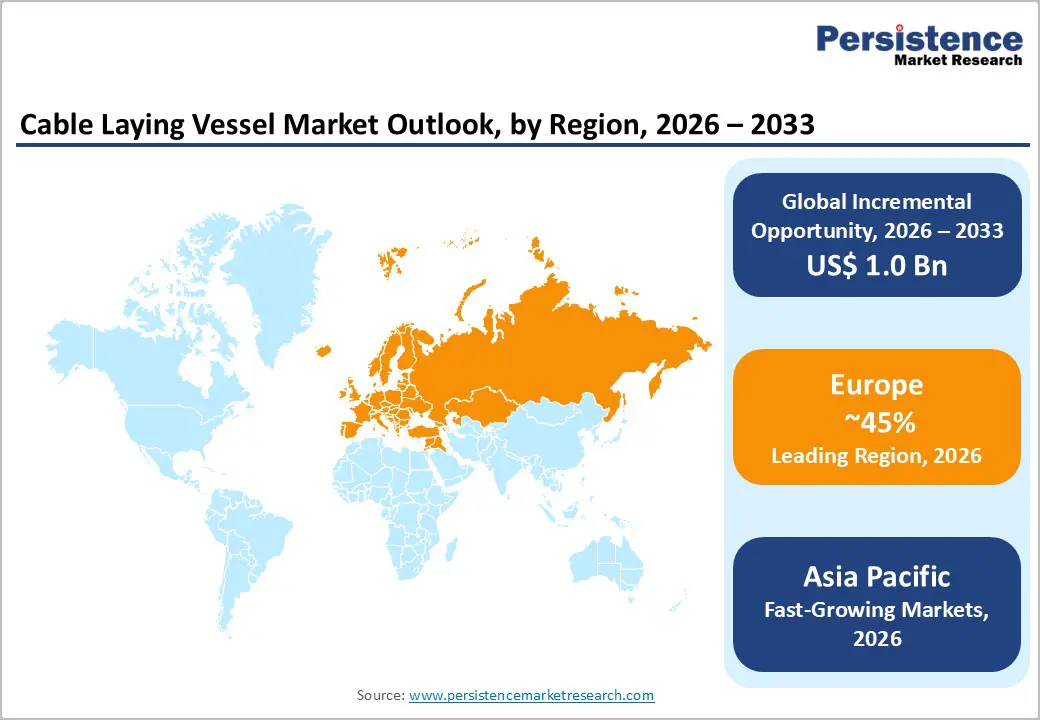

The global cable laying vessel market size is valued at US$ 3.6 Bn in 2026 and is projected to reach US$ 4.6 Bn by 2033, growing at a CAGR of 3.6% between 2026 and 2033.

The market's consistent growth trajectory is underpinned by the global acceleration of offshore wind farm development and the surging demand for submarine power and communications cables, which require specialized cable-laying vessels for installation and maintenance. The European Union has set an offshore wind target of 300 GW by 2050, up from approximately 32 GW installed capacity in 2023, creating multi-decade procurement pipelines for cable-laying vessel operators.

Key Industry Highlights:

- Leading Region: Europe leads the global Cable Laying Vessel market with approximately 45% revenue share in 2024, anchored by the world's most active offshore wind sector, EUR 5.5 Bn TenneT HVDC contract awards, and mature CLV operator fleets in the North Sea.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by China's 40 GW offshore wind target by 2030, rapid Japanese CLV vessel commissioning, and ASEAN nations scaling submarine telecommunications and offshore energy cable infrastructure deployments.

- Dominant Segment: The Wind Farms end-user segment dominates the market with approximately 48% revenue share, driven by the global offshore wind build-out, which requires over 18,000 km of submarine cable to be laid in 2028 alone, creating firm multi-year vessel charter demand.

- Fastest Growing Segment: The above 7000-tonne cable capacity segment is the fastest-growing, driven by the adoption of next-generation HVDC CLVs such as NKT Eleonora (23,000 tonnes) and Prysmian's Monna Lisa (19,000 tonnes), capable of simultaneous multi-cable laying with fewer port calls.

- Key Opportunity: Jones Act-compliant CLV development for the U.S. offshore wind market, exemplified by Nexans' partnership with Crowley Wind Services and the commissioning of methanol/hybrid-propulsion vessels aligned with IMO 2030 mandates, represents the highest-value growth opportunities.

| Key Insights | Details |

|---|---|

| Cable Laying Vessel Market Size (2026E) | US$ 3.6 Bn |

| Market Value Forecast (2033F) | US$ 4.6 Bn |

| Projected Growth CAGR (2026 - 2033) | 3.6% |

| Historical Market Growth (2020 - 2025) | 2.3% |

Market Dynamics

Drivers - Offshore Wind Energy Expansion Driving Unprecedented Submarine Power Cable Demand

The rapid global build-out of offshore wind farms represents the most powerful structural demand driver for cable-laying vessels in the 2026-2033 forecast period. The European Union's target of 300 GW of offshore wind capacity by 2050 and 60 GW by 2030 is triggering an unparalleled wave of subsea export cable installations, each requiring specialized cable-laying vessels for deployment and burial. The scale of this demand is reflected in landmark contracts: in September 2023, TenneT awarded NKT, Nexans, and a consortium of Jan De Nul, LS Cable & System, and Denys with contracts totaling approximately EUR 5.5 Bn for 525 kV HVDC cable systems connecting ten offshore wind projects in the Netherlands and Germany.

Surging Demand for Submarine Telecommunications Cables Driven by Global Data Traffic Growth

Beyond offshore energy, the explosive growth in global data traffic driven by cloud computing, AI workloads, streaming media, and expanding digital economies is generating substantial incremental demand for submarine fibre-optic communications cables and the specialized vessels required to install and maintain them. As of early 2024, approximately 426 submarine cables were in service globally, spanning over 1.3 million kilometres of the world's ocean floors. Technology majors, including Google, Microsoft, Meta, and Amazon, are now among the most active commissioners of new transcontinental submarine cable systems, with Google alone accounting for ownership or co-investment in approximately 1.4% of global submarine cables by length.

Restraints - Extremely High Capital Expenditure Requirements for Newbuild Vessels

The cable laying vessel market is characterized by significant capital intensity, with newbuild specialized vessels costing between US$ 200 Mn and US$ 500 Mn per unit a procurement threshold accessible only to well-capitalized industry majors with long-term contract backlog visibility. Even Prysmian's January 2024 commitment of approximately €350 Mn (approximately US$ 381 Mn) for just two cable-laying vessels illustrates the extraordinary scale of the fleet investment required to maintain market relevance. Combined with typical project construction lead times of approximately two years, this cost structure effectively restricts market entry and constrains the pace of fleet expansion necessary to meet surging demand, contributing to the capacity bottlenecks currently extending project lead times across the industry.

Vessel Supply Constraint and Aging Fleet Creating a Capacity Bottleneck

A structural mismatch between expanding cable-laying demand and available vessel supply is placing increasing strain on the global cable-laying vessel market. The global fleet of large, specialized cable-laying ships numbers approximately 60 vessels globally, and the average age of operational cable ships is approximately 25 years, indicating widespread vessel obsolescence risk. Industry analysis by Spinergie confirmed that approximately 18% of charter contracts in 2024 were delayed due to vessel supply-chain bottlenecks. While nine newbuilds are expected to expand the current fleet by the end of 2026, the outlook beyond that date becomes uncertain, as no significant additional vessel orders were visible, suggesting continued capacity pressure through much of the 2026-2033 forecast window.

Opportunities - High-Capacity HVDC Cable Installation Vessels and Jones Act-Compliant U.S. Fleet Development

The accelerating global transition to High Voltage Direct Current (HVDC) submarine power transmission is creating a compelling, specialized vessel opportunity for cable laying operators willing to invest in next-generation, large-capacity platforms. HVDC cables used for long-distance offshore wind export connections and intercontinental grid interconnectors are larger, heavier, and more technically complex to install than conventional HVAC cables, requiring vessels with carousel capacities exceeding 7,000 tonnes and advanced dynamic positioning systems. This is evidenced by Jan De Nul's Fleeming Jenkin and Nexans' Nexans Electra, two of the world's largest CLVs, both due for delivery in 2026, each capable of laying multiple cables simultaneously. In parallel, the U.S. Jones Act creates a protected market opportunity for domestically registered cable-laying vessels to serve the rapidly expanding U.S. offshore wind sector.

Hybrid and Methanol-Powered Vessels Aligned with IMO Decarbonization Mandates

The International Maritime Organization's (IMO) revised greenhouse gas strategy, which targets at least a 40% reduction in carbon intensity of international shipping by 2030 and net-zero emissions by 2050, is creating a structural opportunity for cable-laying vessel operators and shipbuilders that invest early in low-emission vessel technologies. Operators that commission hybrid-electric, LNG-ready, or methanol-fueled cable-laying vessels are well positioned to win long-term charter contracts from ESG-focused offshore wind developers and government procurement programs that increasingly mandate green vessel operations. NKT named its second cable laying vessel NKT Eleonora in 2024, designed to run on methanol, making it among the world's first CLVs with methanol dual-fuel capability.

Category-wise Analysis

Cable Type Insights

The power cable segment dominates the cable-laying vessel market's cable type category, accounting for approximately 62% of total market revenue and reflecting a wholesale shift in vessel utilization away from telecommunications toward offshore energy infrastructure. The primacy of power cable installation is structurally driven by the massive scaling of offshore wind, the proliferation of HVDC interconnectors linking national electricity grids, and the expansion of offshore oil and gas platforms requiring subsea power supply cables. Industry analysis confirms that more than 55% of new cable-laying vessel charter contracts as of 2023 were dedicated to power cable deployment, with over 40% of new vessel orders placed in 2024 specifically targeting high-voltage power cable installations.

End-user Insights

The Wind Farms end-user segment is the leading and fastest-growing application category in the cable-laying vessel market, commanding approximately 48% of total revenue in 2025. This dominance reflects the global transition to offshore renewable energy and the foundational role that subsea inter-array and export cables play in connecting turbines to onshore power grids. The scale of upcoming offshore wind cable demand is unprecedented: over 18,000 km of cable projected to be laid in 2028 alone (Spinergie), with global offshore wind capacity expected to add over 400 GW between 2024 and 2033. Cable contracts of this magnitude, including TenneT's EUR 5.5 Bn award and NKT and Prysmian's EUR 4.6 Bn contracts from 50Hertz, directly sustain multi-year vessel charter demand and reinforce wind farms as the structural demand anchor for cable laying vessel operators throughout the forecast period.

Capacity Insights

The Above 7000 Tons cable capacity segment commands the leading revenue share within the capacity category, accounting for approximately 38% of total market revenue, reflecting the industry's shift toward large-format vessels capable of handling heavy HVDC cables and reducing the number of offshore port calls required per installation project. High-capacity vessels directly translate into lower operational costs per kilometre of cable laid, making them the preferred choice for long-distance, high-value export cable projects. Vessels such as Prysmian's Leonardo da Vinci and its sister ship Monna Lisa feature three carousel systems with a combined cable capacity of approximately 19,000 tonnes, while NKT Eleonora will offer a cable-laying capacity of 23,000 tonnes. The mid-range 3001-5000 Ton segment remains strategically important for inter-array cable installation across established offshore wind markets, particularly in the North Sea and Baltic Sea.

Regional Insights

North America Cable Laying Vessel Market Trends

North America accounted for approximately 42% of the global cable laying vessel market share in 2025, driven primarily by expanding offshore wind development along the U.S. East Coast and sustained investment in submarine telecommunications cable infrastructure. The U.S. Bureau of Ocean Energy Management (BOEM) reports that over 150 km of new subsea power cable projects were awarded in U.S. waters in 2023. The U.S. Inflation Reduction Act (IRA) has significantly amplified capital flows into domestic clean energy infrastructure, creating incentive structures that are accelerating offshore wind farm development timelines and associated cable installation requirements.

A defining characteristic of the North American market is the Jones Act, U.S. maritime legislation mandating that cargo transported between U.S. ports be carried on U.S.-built, -owned, and -operated vessels. This creates a structural demand for domestically registered cable-laying vessels that do not yet exist in adequate numbers.

Europe Cable Laying Vessel Market Trends

Europe holds the largest operational market share for cable-laying vessels by revenue, accounting for approximately 45% of global revenue in 2024, supported by the world's most mature offshore wind industry and an increasingly dense network of cross-border submarine power interconnectors. The United Kingdom, Germany, the Netherlands, and Denmark are the four dominant demand centres, collectively commissioning billions of euros in HVDC cable system contracts annually. In February 2024, TenneT and TransnetBW awarded NKT and Prysmian contracts worth approximately EUR 2 Bn for the SuedLink HVDC underground cable connection spanning 750 km across Germany.

European cable-laying operators are simultaneously leaders in green vessel technology, aligning with the EU Green Deal and IMO decarbonization standards. NKT's Eleonora, designed to run on methanol, and Prysmian's Monna, equipped with battery-hybrid propulsion, represent European-led innovation in sustainable CLV design.

Asia Pacific Cable Laying Vessel Market Trends

Asia Pacific is the fastest-growing regional market for cable-laying vessels, propelled by China's ambitious offshore wind capacity target of 40 GW by 2030, Japan's accelerating offshore wind build-out, and India's expanding submarine cable infrastructure programs. China increased its defense and energy infrastructure spending by 7.0% in 2024 (SIPRI), and its domestic CLV shipbuilding capacity is growing accordingly: LS Cable & System (South Korea) secured a contract for South Korea's largest 8,000-tonne submarine cable vessel, the GL2030, reflecting the region's expanding vessel construction capabilities.

Japan-based companies are increasingly building operational capacity for domestic and regional offshore wind markets: Toyo Construction contracted Vard in late 2023 for a hybrid-power cable-lay and construction vessel of the Vard 9 15 design, valued at over US$ 200 Mn, specifically developed for the Japanese offshore wind market. Penta-Ocean Construction has also signed a shipbuilding contract with PaxOcean Group for a self-propelled large-scale CLV, expanding its capabilities for Japan's offshore wind sector.

Competitive Landscape

The global cable laying vessel market is highly consolidated, with Prysmian, Nexans, NKT, and Jan De Nul collectively accounting for an estimated 60% of global revenue. This concentration is structurally reinforced by the capital intensity of vessel ownership each unit costing US$ 200-500 Mn and the importance of EPCI (Engineering, Procurement, Construction, and Installation) contract capabilities that integrate cable manufacturing, logistics, and marine installation. Competitive differentiation centers on cable carousel capacity, dynamic positioning (DP2/DP3) systems, HVDC technical certification, green propulsion technology, and fleet availability in target regions.

Key Developments:

- January 2024: Prysmian Group confirmed an investment of approximately €350 Mn (US$ 381 Mn) in two new cable-laying vessels, including the Monna Lisa (185 m, three carousels, total capacity 19,000 tonnes), with battery-hybrid propulsion and biodiesel-compatible generators, reflecting the company's expanding EPCI offshore commitments.

- 2024: NKT named its second cable laying vessel NKT Eleonora, designed to run on methanol and equipped with three turntables offering a cable-laying capacity of 23,000 tonnes making it one of the world's largest and most sustainable CLVs, supporting NKT's EUR 3.5 Bn multi-project HVDC framework agreement with TenneT.

- 2024-2025: Nexans partnered with Crowley Wind Services to develop and operate a Jones Act-compliant cable lay barge dedicated to supporting U.S. offshore wind cable installation strategic move to capture the growing North American offshore wind market protected by U.S. maritime law.

Companies Covered in Cable Laying Vessel Market

- Prysmian Group

- Nexans S.A.

- NKT A/S

- Jan De Nul Group

- Global Marine Group

- Alcatel Submarine Networks (ASN)

- Orange Marine

- LS Cable & System

- Toyo Construction

- Penta-Ocean Construction

- NCT Offshore

- DEME Group

- Huawei Marine Networks

- SubCom LLC

- Crowley Wind Services

Frequently Asked Questions

The global Cable Laying Vessel market is valued at US$ 3.6 Bn in 2026 and is projected to reach US$ 4.6 Bn by 2033, growing at a CAGR of 3.6%.

The key demand drivers are accelerating offshore wind farm development requiring submarine export and inter-array cables with over 18,000 km of cable projected to be laid in 2028 alone and surging submarine telecommunications cable investment by technology majors including Google, Microsoft, Meta, and Amazon.

The Power Cable segment dominates with approximately 62% of total market revenue, driven by the scale of offshore wind HVDC export cable installations. Over 40% of new vessel orders placed in 2024 were dedicated to high-voltage power cable installations far exceeding the telecommunications cable segment's share of new project procurement.

Europe leads the global Cable Laying Vessel market with approximately 45% revenue share in 2024, driven by its mature offshore wind industry and billions of euros in active HVDC cable contracts. Asia Pacific is the fastest-growing region, underpinned by China's 40 GW offshore wind target by 2030, Japan's domestic CLV fleet build-up, and ASEAN digital infrastructure expansion.

The key market participants are Prysmian Group, Nexans S.A., NKT A/S (Denmark), Jan De Nul Group, Global Marine Group, Alcatel Submarine Networks/ASN, Orange Marine, LS Cable & System, Toyo Construction, DEME Group, SubCom LLC, and Crowley Wind Services, among others.