- Plastics, Polymers & Resins

- Blow Molded Plastics Market

Blow Molded Plastics Market Size, Share, and Growth Forecast 2026 - 2033

Blow Molded Plastics Market by Product Type (Polyethylene (PE), Polyethylene Terephthalate (PET), Polypropylene (PP), Polyvinyl Chloride (PVC), Other), Technology (Extrusion, Stretch, Injection, Compound), Application (Packaging, Automotive, Consumer Goods, Medical, Other), and Regional Analysis for 2026 - 2033

Blow Molded Plastics Market Size and Trend Analysis

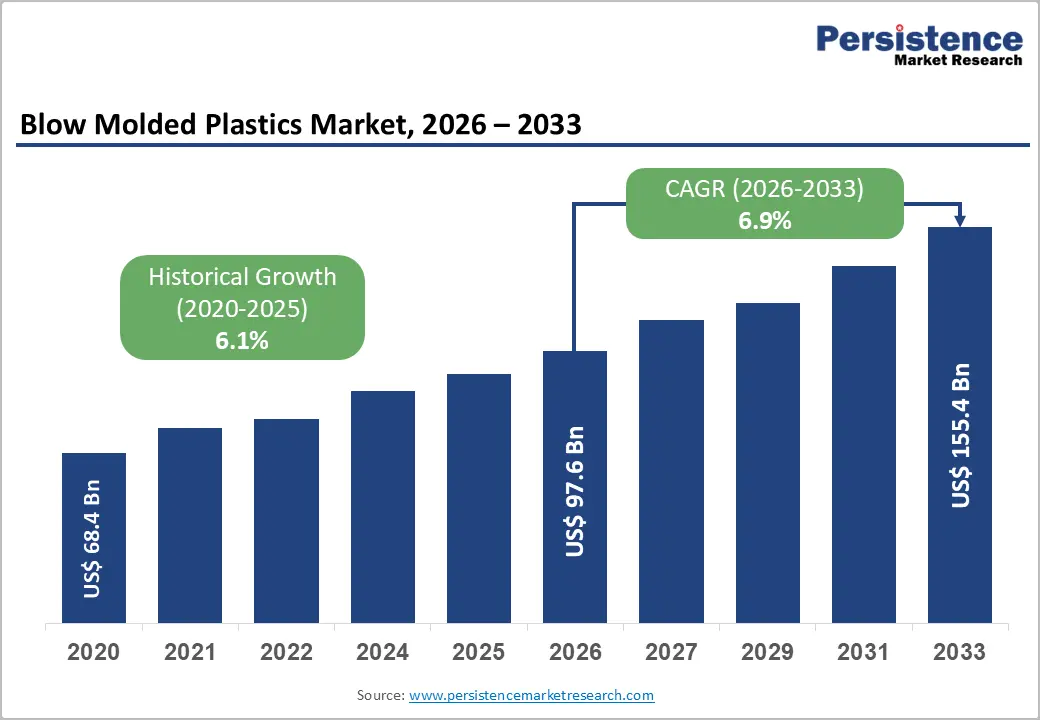

The global blow molded plastics market size is valued at US$ 91.2 billion in 2026 and is projected to reach US$ 155.7 billion by 2033, growing at a CAGR of 6.9% between 2026 and 2033. The market's steady expansion is underpinned by accelerating demand from the packaging, automotive, and healthcare end-use sectors, which collectively consume the largest volume of blow-molded plastic components globally.

The automotive industry's transition toward lightweight plastic components to meet fuel efficiency and emission reduction mandates, particularly as electric vehicle production scales in the Asia Pacific and Europe, is reinforcing demand across extrusion and injection blow molding segments. Additional tailwinds include innovations in resin chemistry, process automation, and the integration of recycled content into blow-molded products, aligning with circular economy targets set by governments across the European Union and North America.

Key Industry Highlights:

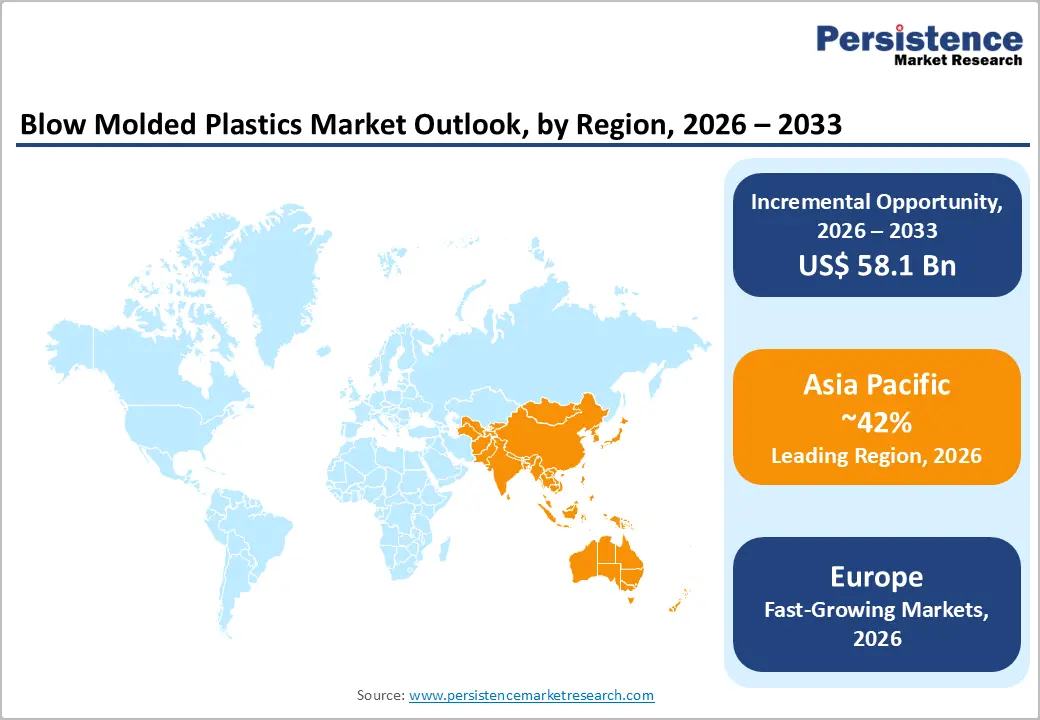

- Regional Leadership: Asia Pacific dominates the global blow molded plastics market with approximately 42% revenue share, driven by China and India's massive packaging, automotive, and consumer goods manufacturing ecosystems.

- Fast-Growing Market: Europe is the fastest-growing region, propelled by EU sustainability mandates including the Single-use Plastics Directive, Green Deal-aligned packaging redesign investments, and accelerating adoption of recycled-content blow-molded solutions.

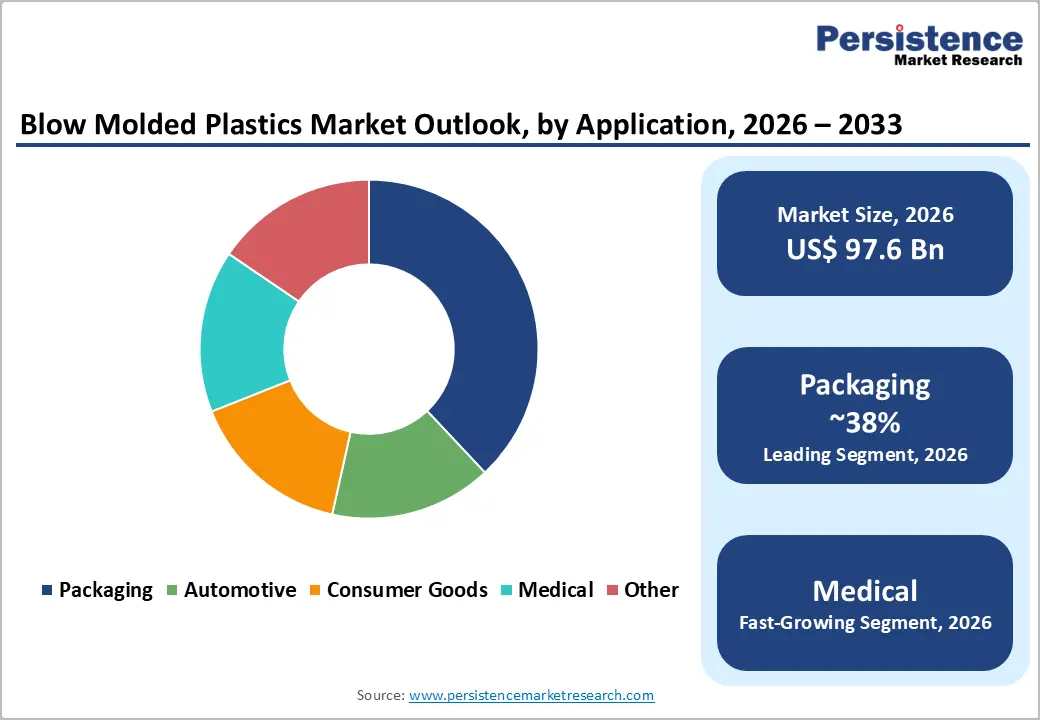

- Dominant Packaging Type: Packaging segment leads with an estimated 38% market share, driven by global consumption of PET and HDPE bottles for food, beverage, personal care, and pharmaceutical end-uses.

- Fast-Growing Applications: Medical applications are the fastest-growing segment, underpinned by rising pharmaceutical output, stringent hygiene standards, and expanding healthcare infrastructure investment globally.

- Key Opportunity: The shift toward bio-based and recycled-content blow-molded plastics offers high-margin growth opportunities as global sustainable packaging demand rises.

DRO Analysis

Drivers - Surge in Global Packaged Goods Consumption

The global packaged food and beverage industry is one of the most powerful demand catalysts for blow-molded plastics. According to the Food and Agriculture Organization (FAO) of the United Nations, global food production is projected to rise by over 60% by 2050 to meet population needs, directly intensifying demand for protective packaging formats. Plastics dominate this space, accounting for approximately 44% of all packaging materials produced globally, as highlighted by the Plastic Soup Foundation.

Blow-molded containers and bottles are critical to this sector, offering lightweight design, chemical barrier protection, and cost-efficient manufacturability. The rapid proliferation of quick-service retail, food delivery apps, and modern trade channels across South Asia, Southeast Asia, and Latin America continues to amplify the consumption of blow-molded bottles, containers, and packaging closures.

Automotive Industry Lightweighting and EV Expansion

The global automotive sector's pursuit of lightweighting to comply with stringent fuel economy and carbon emission regulations is a significant structural driver for blow-molded plastic components. Blow-molded plastics are used extensively in air ducts, fuel tanks, bumper systems, and seat backs. The rise of electric vehicles (EVs) further compounds this demand, as EV architectures require complex hollow plastic structures for battery compartments and thermal management systems.

According to the International Energy Agency (IEA), global electric car sales surpassed 17 million units in 2024, with China alone accounting for more than 60% of that volume. Nations like Germany, Japan, and India are also ramping up domestic EV manufacturing, which is boosting co-located plastics manufacturing investment. Automotive-grade blow molding requirements for polymer precision, dimensional consistency, and safety compliance drive adoption of advanced HDPE and PP grades from leading resin suppliers.

Restraints - Volatile Raw Material Prices and U.S. Tariff Disruptions

Raw material price volatility represents a persistent headwind for blow-molded plastics manufacturers. Primary resins such as polyethylene (PE), polypropylene (PP), and polyvinyl chloride (PVC) are petrochemical derivatives, making their pricing highly sensitive to crude oil and natural gas price swings. Compounding this is the introduction of U.S. Section 301 and IEEPA tariffs in 2025, which imposed a baseline 10% tariff on most imports and up to 25% on certain petrochemical feedstock.

According to the American Chemistry Council, manufacturers sourcing raw materials internationally may see cost increase of 12-20% depending on supply chain configurations. The Plastics Industry Association further noted that U.S. plastics industry resin imports reached US$ 13.3 billion year-to-date in 2025, down by 6.9% compared to the previous years, reflecting trade-policy-driven supply chain adjustments.

Rising Environmental Regulatory Pressure on Single-Use Plastics

Stringent regulatory restrictions on single-use and non-recyclable plastics are constraining market scope in key economies. The European Union's Single-Use Plastics Directive (SUPD) has already banned several plastic product categories and mandated extended producer responsibility for packaging. The European Green Deal and Circular Economy Action Plan are pushing manufacturers toward higher recycled content and recyclable-by-design products.

Furthermore, the United Nations Environment Programme (UNEP) is advancing a global plastics treaty framework, which is expected to impose further production and waste-reduction obligations. In the food industry, only approximately 25% of plastic packaging is currently recyclable, and less than 1% is reusable, according to Statista. These systemic limitations add capital expenditure burdens on manufacturers to invest in sustainable alternatives and compliance infrastructure.

Opportunities - Bio-Based and Recycled Content Blow-Molded Plastics

The transition toward sustainable packaging is creating a lucrative opportunity for blow-molded plastics manufacturers willing to innovate with bio-based and recycled content resins. In June 2024, Dow Inc. announced the launch of two new REVOLOOP recycled plastics resins, enabling circular solutions for packaging applications.

In March 2024, Dow scientists also published a breakthrough in novel polyethylene architecture in the journal Science, with potential for lower carbon emissions in industrial-scale production. Meanwhile, in November 2024, a consortium including Indorama Ventures, Suntory, and Neste launched what was described as the world's first bio-PET container made from used cooking oil.

Expansion of Medical and Healthcare Packaging

The healthcare and pharmaceutical packaging segment presents a high-growth avenue for blow-molded plastics, particularly in the wake of heightened hygiene awareness and increased medical device manufacturing. Blow-molded HDPE bottles and containers are widely used for liquid medications, disinfectants, IV delivery systems, and pharmaceutical storage. In June 2023, Airnov Healthcare Packaging launched new HDPE bottles compliant with U.S. FDA, Chinese DMF registration, and EU regulations for dry pharmaceutical applications.

The global medical devices market is on a robust growth trajectory, with increasing public health investment across the Asia Pacific, the Middle East, and Africa. As governments mandate sterile, single-use plastic containers for hospital and home-care settings, demand for injection-grade blow-molded containers with precise dimensional tolerances is expected to grow substantially, making medical packaging an especially high-margin growth pocket for market participants.

Category-wise Analysis

Product Type Insights

Polyethylene (PE) is the dominant product segment in the blow-molded plastics market, with an estimated revenue share of approximately 37% globally. PE's unrivaled combination of chemical resistance, impact strength, and process versatility makes it the material of choice for packaging bottles, industrial drums, fuel tanks, and agricultural containers. Both High-Density Polyethylene (HDPE) and Low-Density Polyethylene (LDPE) are extensively processed through extrusion blow molding.

According to data from the American Chemistry Council, HDPE is the most widely used blow-molding resin for household chemicals, milk jugs, and industrial packaging due to its superior stiffness and chemical barrier properties. Mold-Tek Packaging Ltd., a leading rigid plastics manufacturer in India, expanded its annual production capacity by 5,500 tons through three new factories in 2024, evidencing the robust demand for PE-based blow-molded products in emerging markets.

Technology Insights

Extrusion blow molding is the leading technology segment, holding an estimated share of approximately 50% of the global market by revenue. This dominance is attributed to its cost efficiency, operational flexibility, and suitability for a broad range of container configurations, from small bottles to large industrial drums. The process requires lower capital investment relative to injection or stretch blow molding, and enables production of complex geometries incorporating handles, threads, and varying wall thickness in a single step.

High automation levels and shorter cycle times further reinforce extrusion blow molding's competitive advantage for high-volume manufacturing. The technology is widely adopted by FMCG, agricultural chemicals, and industrial packaging producers globally. Manufacturers such as Berry Global and INEOS Group operate highly automated extrusion blow molding lines at scale to serve food, beverage, and personal care markets across North America and Europe.

Application Insights

The packaging segment is the dominant application category in the blow molded plastics market, accounting for an estimated 38% or more of total revenue. This leadership is driven by the ubiquitous use of blow-molded bottles and containers across food and beverage, personal care, household chemicals, and pharmaceutical end-uses.

Within blow-molded packaging, beverage bottles, particularly PET water and carbonated drink bottles, form the largest volume subcategory globally. Asia Pacific dominates packaging consumption, driven by the rapid growth of online food delivery platforms, FMCG brands, and modern retail formats in China, India, and Southeast Asia.

Regional Insights

North America Blow Molded Plastics Market Trends & Analysis

North America represents a mature but continuously evolving market for blow-molded plastics, holding an estimated revenue share of approximately 27% of the global market. However, the 2025 tariff regime, imposing 25% duties on Canadian and Mexican imports, and 10-20% on Chinese goods, has created significant cost and supply chain headwinds for plastic resin procurement.

U.S. Blow Molded Plastics Market

The United States is the largest individual national market for blow-molded plastics in North America, with 82% regional market share. Strong consumer goods consumption developed pharmaceutical packaging standards, and a well-established automotive manufacturing base continues to support steady demand. According to the Plastics Industry Association, U.S. plastics industry resin imports fell 6.9% year-to-date through August 2025, due to the tariff regime.

Europe Blow Molded Plastics Market Trends, Drivers, & Insights

Europe is the fastest-growing region in the blow molded plastics market, with demand driven by the region's transition toward sustainable packaging mandated by the European Green Deal and Circular Economy Action Plan. The EU's Single-Use Plastics Directive (SUPD) is reshaping product design across the packaging and consumer goods sectors. European manufacturers are accelerating the adoption of recycled-content blow-molded bottles and containers to meet mandatory recycled content thresholds.

Germany Blow Molded Plastics Market

Germany is a vast market for blow-molded plastics, accounting for 31% regional share, anchored by its world-class automotive and chemical manufacturing industries. The country's polymer and specialty chemicals sector, home to companies such as BASF SE, supplies advanced resins that support high-precision blow molding for automotive components and medical packaging.

U.K. Blow Molded Plastics Market

United Kingdom is likely to account for 17% share in 2026, is underpinned by strong personal care, food, and pharmaceutical packaging demand. Post-Brexit regulatory alignment and domestic sustainability mandates from the UK Plastics Pact, which targets 100% reusable, recyclable, or compostable plastic packaging by 2025, are accelerating product reformulation across blow molding supply chains.

France Blow Molded Plastics Market

France is a key market for blow-molded plastics, with 13% share, with particularly strong demand from the food and beverage sector. TotalEnergies announced the construction of a new polypropylene production line in Carling, France, in late 2022, focused on recycling post-consumer waste for the automotive sector, underscoring the country's industrial commitment to circular plastics.

Asia Pacific Blow Molded Plastics Market Drivers & Analysis

Asia Pacific dominates the global blow molded plastics market with an estimated revenue share of approximately 42%. The region benefits from a combination of massive manufacturing infrastructure, a growing middle-class consumer base, booming e-commerce, and accelerating automotive production, particularly electric vehicles. China and India are the primary growth engines, collectively home to some of the world's largest plastic packaging and automotive industries.

China Blow Molded Plastics Market

China is the largest single-country market for blow-molded plastics, with 44% regional market share, driven by its commanding position as the world's largest manufacturer and consumer of packaged goods, consumer electronics, automobiles, and chemical products. In 2025, China-origin plastics imports to the U.S. faced an additional 10% tariff layer, prompting some Chinese blow molding manufacturers to pivot toward domestic consumption and intra-Asia trade partnerships.

India Blow Molded Plastics Market

India is among the fastest-growing national markets for blow-molded plastics in the Asia Pacific, having 21% market share, driven by its rapidly expanding food processing industry, rise in consumer goods output, and booming pharmaceutical manufacturing. The India Brand Equity Foundation (IBEF) reported that Mold-Tek Packaging Ltd. opened three new factories in 2024 in Tamil Nadu, Telangana, and Haryana, adding 5,500 tons of production capacity.

Japan Blow Molded Plastics Market

Japan represents a mature, innovation-led market for blow-molded plastics, having 24% market share, with demand anchored in high-precision automotive, electronics packaging, and healthcare applications. In October 2025, the United States enacted a new tariff framework on Japanese imports, creating uncertainty for machinery trade flows.

Competitive Landscape

The global blow molded plastics market is moderately fragmented, with a mix of global vertically integrated resin-to-product conglomerates and specialized regional blow molders. Market leaders such as Berry Global (now part of Amcor), INEOS Group, Dow Inc., and Magna International leverage scale, advanced automation, and proprietary resin technologies as key differentiators. Mid-tier players differentiate through application specialization, such as agricultural containers, medical packaging, or automotive components, and geographic proximity to key demand clusters.

Key Developments:

- February 2025: Berry Global completed the acquisition of CMG Plastics, which operates injection and extrusion blow molding facilities in New Jersey and Ontario, strengthening its North American rigid packaging portfolio ahead of its own acquisition by Amcor.

- February 2026: FirmaPak announced the acquisition of Easy Plastic Containers Corporation, a Canada-based manufacturer of blow-molded plastic packaging, marking a strategic expansion into the Canadian market. The acquired company operates two facilities near Toronto and serves industries including health & beauty, food & beverage, pharmaceuticals, and automotive.

- May 2025: Aaron Packaging Inc. announced the acquisition of Affordable Plastics and Packaging Inc., a California-based PET blow molding manufacturer, strengthening its position in the rigid plastic packaging and blow molding market.

Top Companies in Blow Molded Plastics

- Amcor plc (Evansville, U.S.), through Berry Global, is one of the world's largest producers of blow-molded plastic packaging, generating annual revenues of approximately US$ 12.3 billion in FY2024. The company serves food, beverage, healthcare, and personal care markets through highly automated extrusion and injection blow molding facilities across North America, Europe, and Asia. Its acquisition by Amcor in 2025 will create a packaging mega-player with unmatched global reach.

- Magna International, Inc. (Aurora, Canada) is a global automotive supplier whose blow-molded plastic components, including fuel systems, air management components, and exterior structures, are supplied to leading OEMs such as BMW, Ford, and General Motors. With revenues exceeding US$ 40 billion annually, Magna's scale and automotive engineering expertise make it a dominant force in technical blow-molded plastic applications.

- INEOS Group (Rolle, Switzerland) is one of the world's largest producers of petrochemicals, specialty chemicals, and oil products, with blow molding-grade HDPE and PP resins among its key product lines. The group serves blow molding converters across packaging, automotive, and industrial end-markets globally.

Blow Molded Plastics Report - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 68.4 Bn |

| Current Market Value (2026) | US$ 91.2 Bn |

| Projected Market Value (2033) | US$ 155.7 Bn |

| CAGR (2026 - 2033) | 6.9% |

| Leading Region | Asia Pacific, 42% |

| Dominant Segment | Packaging (Application), 38% |

| Top-ranking Segment | Polyethylene / PE (Product Type), 37% |

| Incremental Opportunity | US$ 64.5 Bn |

Companies Covered in Blow Molded Plastics Market

- Magna International

- Berry Global

- IAC Group

- Apex Plastics

- Pet All Manufacturing

- Dow, Inc.

- Rutland Plastics

- INEOS Group

- Garrtech

- The Plastic Forming Company

- Agri-Industrial Plastics

- North American Plastics

- Comar LLC

- ALPLA

- Plastipak

- Graham Packaging

- LyondellBasell

- SABIC

Frequently Asked Questions

The global blow molded plastics market is valued at approximately US$ 91.2 Bn in 2026 and is projected to reach US$ 155.7 Bn by 2033, reflecting a CAGR of 6.9% over the forecast period.

The primary demand drivers include the global surge in packaged food and beverage consumption, supported by urbanization trends and e-commerce growth, and the automotive industry's adoption of lightweight blow-molded components to meet fuel efficiency targets and electric vehicle production demands. Innovation in resin technology, particularly recycled and bio-based PE and PET grades, is also driving market expansion alongside growing healthcare packaging requirements.

The packaging segment is the dominant application category, accounting for an estimated 38% of total market revenue. This leadership is supported by the pervasive use of blow-molded PET and HDPE bottles across food and beverage, personal care, household chemicals, and pharmaceutical packaging segments globally.

Asia Pacific is the leading region, accounting for approximately 42% of global market revenue. China is the dominant national market within the region, followed by India, both benefiting from large-scale packaging, automotive, and consumer goods manufacturing ecosystems. Europe is the fastest-growing region, driven by sustainability regulations and circular economy mandates.

The most significant market opportunity lies in the development and commercialization of sustainable blow-molded plastics, including products made with recycled post-consumer resins and bio-based alternatives.

The key players operating in the global blow molded plastics market include Amcor plc, Magna International, INEOS Group, Dow, Inc., IAC Group, Apex Plastics, Pet All Manufacturing, Rutland Plastics, Garrtech, Agri-Industrial Plastics, North American Plastics, and The Plastic Forming Company, among others.