- Technology

- Agriculture IoT Market

Agriculture IoT Market Size, Share, and Growth Forecast 2026 - 2033

Agriculture IoT Market by Component (Hardware, Software, Services), Deployment (On premise, Cloud), by Connectivity (Wi Fi, Bluetooth, Cellular, Others), Farm Type (Large, Mid sized, Small), Application (Precision Farming, Livestock Monitoring, Smart Greenhouse, Aquaculture, Others), and Regional Analysis, 2026 - 2033

Agriculture IoT Market Size and Trend Analysis

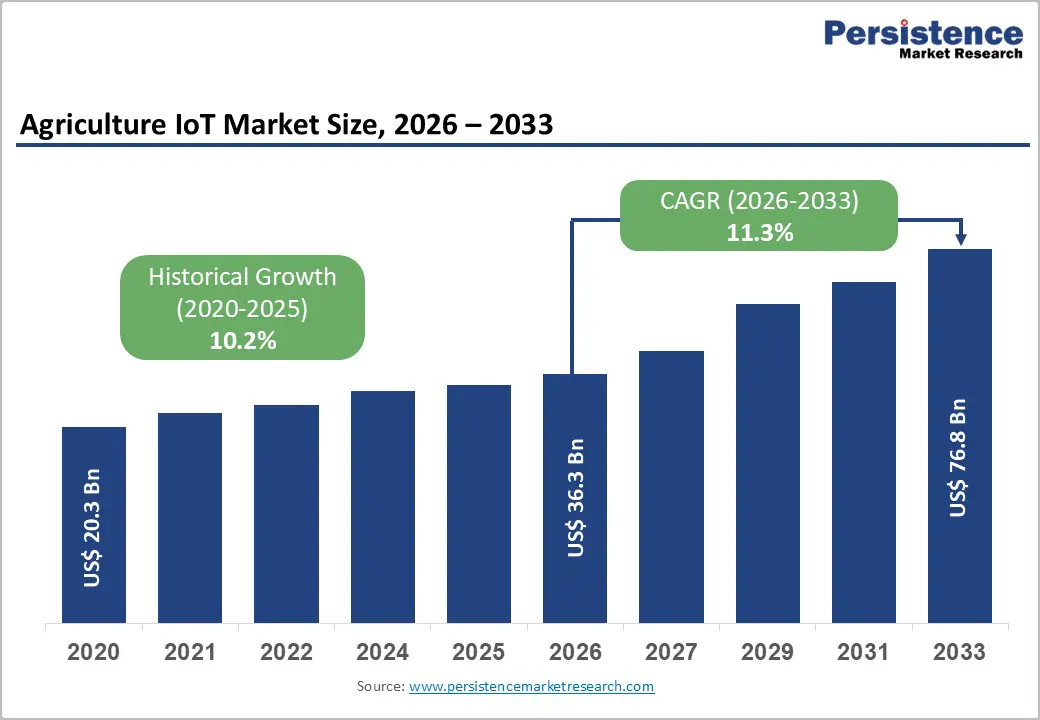

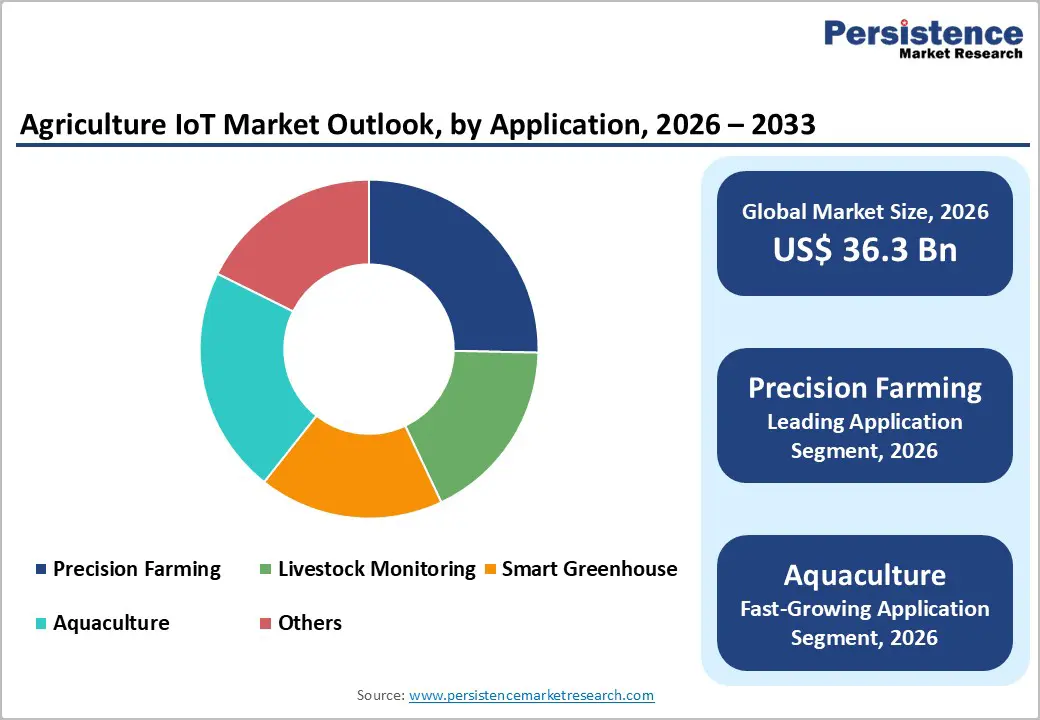

The global Agriculture IoT market is projected to reach US$ 36.3 billion in 2026 and grow to US$ 76.8 billion by 2033, registering a CAGR of 11.3%. Growth is driven by the increasing need to enhance crop productivity, reduce input costs, and strengthen resilience against climate-related challenges.

The rapid adoption of precision farming, supported by government-led digital agriculture initiatives and subsidies, is accelerating market expansion. The rise in global population and food demand is encouraging both large and small farms to invest in connected sensors, data analytics platforms, and automated systems to optimize resource use and improve overall farm efficiency.

Key Industry Highlights:

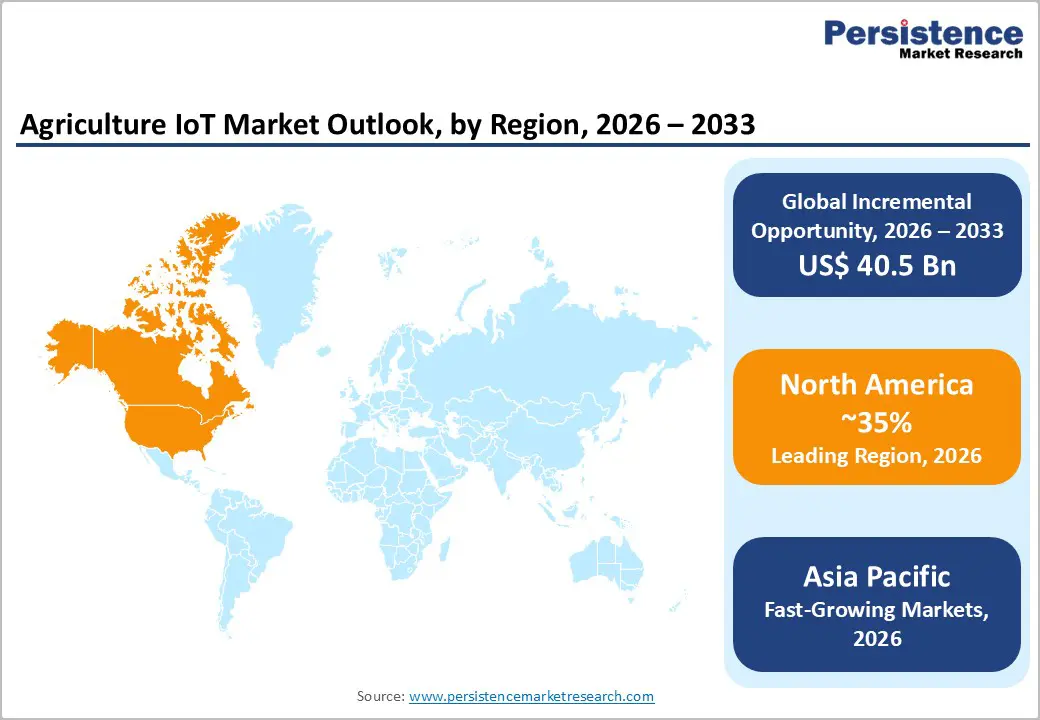

- Leading Region: North America leads with 35% share (2025), driven by advanced precision farming and strong digital infrastructure.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, supported by government initiatives and expanding IoT adoption.

- Leading Deployment: Cloud leads with 52% share (2025), driven by scalability and cost efficiency.

- Leading Connectivity: Cellular holds 38% share (2025), supported by wide-area coverage in remote farms.

- Key Opportunity: Edge AI integration enables real-time decision-making and improved resource efficiency across farming operations.

| Key Insights | Details |

|---|---|

|

Agriculture IoT Size (2026E) |

US$ 36.3 Billion |

|

Market Value Forecast (2033F) |

US$ 76.8 Billion |

|

Projected Growth CAGR (2026–2033) |

11.3% |

|

Historical Market Growth (2020–2025) |

10.2% |

Market Dynamics

Drivers - Rising Adoption of Precision Farming Technologies Driving Growth

The rapid uptake of precision farming is a key driver of the Agriculture IoT market across developed and emerging regions. IoT-enabled sensors, GPS-guided equipment, and analytics platforms allow farmers to monitor soil conditions, crop health, and inputs in real time, enabling targeted application of water, fertilizers, and pesticides. This improves productivity, reduces resource wastage, and enhances overall farm profitability.

Governments and institutions are actively promoting precision agriculture as a pathway to sustainable intensification. Programs in Europe and India are supporting IoT-based monitoring and variable rate technologies, demonstrating measurable improvements in yield and cost efficiency. These successful field-level outcomes are strengthening farmer confidence and accelerating the global adoption of connected farming solutions.

Expanding Government Support and Subsidies Accelerating Adoption

Public sector support through subsidies, grants, and favorable policies is significantly boosting Agriculture IoT adoption. Large-scale funding initiatives in regions such as Europe and North America are encouraging farmers to invest in smart sensors, automated machinery, and data-driven farm management systems. These measures reduce financial barriers and promote the modernization of agricultural practices across both commercial and mid-sized farms.

Additionally, global development organizations are emphasizing digital agriculture to improve food security and rural productivity. Policy-backed investments in IoT infrastructure, along with farmer training programs, have increased adoption rates of connected technologies in multiple regions. By reducing investment risks and enhancing awareness, these initiatives are creating a strong foundation for sustained market growth.

Restraints - High Initial Investment and Rural Infrastructure Limitations

High upfront costs remain a major barrier to widespread adoption of Agriculture IoT, particularly for small and mid-sized farms. Deploying IoT systems, including sensors, connectivity, and data platforms, requires significant capital investment per hectare. This becomes challenging for smallholders, who make up the majority of global farms, limiting their ability to adopt comprehensive digital farming solutions despite their potential long-term benefits.

The issue is further intensified by inadequate digital infrastructure in rural areas. Limited broadband access and unreliable connectivity make it difficult to operate IoT devices effectively. Farmers in such regions often face operational disruptions and higher maintenance costs, leading them to delay or partially implement IoT solutions, ultimately slowing overall market penetration.

Rising Cybersecurity Risks and Data Privacy Concerns

Cybersecurity threats and data privacy concerns are increasingly hindering the adoption of Agriculture IoT. Connected farming systems generate sensitive operational data, making them vulnerable to cyberattacks and unauthorized access. As digital integration deepens, farms and agribusinesses are increasingly exposed to data breaches, creating hesitation among users about the reliability and safety of IoT platforms.

Stringent data protection regulations require secure data storage, encryption, and compliance mechanisms. These requirements increase implementation complexity and operational costs for technology providers. For many farmers, especially smallholders, uncertainty around data ownership and security reduces trust and willingness to fully adopt IoT-driven agricultural systems.

Opportunities - Integration of Edge Computing and AI Enhancing Farm Efficiency

The convergence of edge computing and artificial intelligence is creating significant opportunities in the Agriculture IoT market. By processing data locally on farms, edge-enabled systems enable real-time decision-making for irrigation, pest control, and environmental adjustments. This reduces latency, improves responsiveness, and enhances operational efficiency, making IoT solutions more practical for time-sensitive agricultural activities.

Leading agribusinesses are leveraging AI-integrated platforms that combine sensor data, satellite imagery, and drone inputs to deliver predictive insights on crop health and yield performance. These technologies have demonstrated measurable improvements in productivity and input optimization, encouraging further investment in advanced, data-driven farming systems, particularly in precision agriculture and high-value crop segments.

Growing Adoption in Emerging Markets Through Affordable Solutions

Emerging markets present a strong opportunity for Agriculture IoT expansion through the development of low-cost and scalable solutions. With a large base of smallholder farmers, there is increasing demand for affordable technologies such as solar-powered sensors, low-bandwidth connectivity, and flexible pay-as-you-use models that reduce financial barriers to adoption.

Governments and development organizations are supporting digital agriculture initiatives to improve productivity and resilience in these regions. Simplified IoT tools that provide actionable insights into soil and weather conditions have already shown strong adoption potential. This trend is opening a vast untapped market, encouraging providers to design modular and cost-efficient solutions tailored to resource-constrained farming environments.

Category wise Analysis

Component Insights

Hardware dominates the agriculture IoT market with an estimated 45% share in 2025, driven by its essential role in data collection and transmission. Devices such as sensors, controllers, gateways, and connected machinery form the backbone of IoT-enabled farming systems. A significant proportion of precision agriculture adopters rely on these tools for real-time monitoring of soil, weather, and crop conditions, reinforcing hardware’s central position in the ecosystem.

Software is emerging as the fastest-growing segment, supported by rising demand for advanced analytics and farm management platforms. AI-driven insights, predictive modeling, and seamless integration with cloud systems are enhancing decision-making capabilities. As farms increasingly shift toward data-driven operations, software solutions are becoming critical for optimizing productivity and enabling intelligent automation across agricultural processes.

Deployment Insights

Cloud-based deployment leads the agriculture IoT market with an estimated 52% share in 2025, owing to its scalability, centralized data management, and remote accessibility. Large-scale farms particularly benefit from cloud platforms, which support complex data processing, analytics, and multi-location farm monitoring. Cost efficiencies and reduced infrastructure requirements further strengthen cloud adoption across commercial agricultural operations.

On-premise deployment is witnessing steady growth as some farmers prioritize data control, customization, and reduced dependency on external networks. It is particularly relevant in regions with connectivity challenges or strict data governance requirements. As hybrid models evolve, on-premise solutions are increasingly being integrated with cloud capabilities to balance flexibility and security needs.

Connectivity Insights

Cellular connectivity holds the leading position with an estimated 38% share in 2025, driven by its ability to provide reliable, wide-area coverage across large and remote farmlands. Technologies such as LTE-M and NB-IoT enable efficient communication for low-power devices like soil sensors and livestock trackers. The ease of integration with existing mobile networks makes cellular a practical and scalable solution for continuous farm monitoring.

LPWAN and satellite-based connectivity solutions are emerging as the fastest-growing segments, especially in regions with limited traditional network infrastructure. These technologies offer extended range and energy efficiency, making them suitable for remote agricultural environments. As connectivity demands expand, these alternatives are gaining traction for enabling seamless IoT operations across diverse geographies.

Farm Type Insights

Large farms dominate the Agriculture IoT market with an estimated 55% share in 2025, supported by their ability to invest in advanced technologies and deploy IoT systems at scale. Their access to capital, skilled labor, and extensive landholdings enables efficient implementation of precision farming tools, resulting in higher productivity and optimized resource utilization. These factors make large farms key contributors to overall market growth.

Small and mid-sized farms are emerging as the fastest-growing segment, driven by increasing awareness and availability of affordable IoT solutions. Government support, digital training programs, and flexible pricing models are encouraging adoption among these farmers. As technology becomes more accessible, smaller farms are gradually integrating IoT tools to enhance efficiency and competitiveness.

Application Insights

Precision farming leads the agriculture IoT market with an estimated 42% share in 2025, owing to its direct impact on yield optimization and resource efficiency. By leveraging IoT-enabled sensors, satellite data, and analytics platforms, farmers can implement targeted interventions, such as variable-rate fertilization and smart irrigation, significantly improving productivity while minimizing environmental impact.

Aquaculture and smart greenhouse applications are among the fastest-growing segments, driven by the need for controlled environment agriculture and efficient resource management. These applications leverage IoT technologies for monitoring water quality, climate conditions, and automated systems, enabling consistent output and higher operational efficiency in specialized farming practices.

Regional Insights

North America Agriculture IoT Market Analysis

North America leads the agriculture IoT market with an estimated 35% share in 2025, supported by a highly mechanized farming ecosystem and strong digital infrastructure. The United States drives regional dominance through widespread adoption of precision agriculture technologies, backed by government support, funding programs, and partnerships with technology providers. Advanced equipment and integrated IoT systems are widely deployed across large-scale commercial farms.

The region continues to evolve with rapid innovation in AI-driven farming solutions and connected machinery. Adoption of drone-based monitoring and automated input application systems is expanding, improving efficiency and sustainability. Strong broadband penetration and ongoing technological advancements are expected to further strengthen North America’s leadership in smart and data-driven agriculture practices.

Europe Agriculture IoT Market Insights

Europe represents a mature and policy-driven market for agriculture IoT, characterized by strong regulatory alignment and sustainability-focused initiatives. Countries such as Germany, France, and the United Kingdom are actively adopting IoT-enabled precision farming tools supported by regional frameworks. Government-backed programs encourage digital monitoring, emissions tracking, and efficient resource utilization across agricultural operations.

Europe is projected to reach a CAGR of around 11–12% during the forecast period, driven by increasing emphasis on climate-smart agriculture and digital transformation. The integration of IoT with simulation tools and data platforms is gaining traction, enabling farmers to optimize decisions. Continued policy support and cross-border standardization are expected to sustain steady growth across the region.

Asia Pacific Agriculture IoT Market Insights

Asia Pacific accounts for approximately 28% share of the agriculture IoT market in 2025, making it one of the most significant and rapidly expanding regions. Growth is driven by large agricultural populations, rising food demand, and increasing government initiatives promoting digital farming. Countries such as China and India are investing heavily in IoT-enabled systems to improve productivity and resource efficiency.

The region is witnessing the rapid adoption of cost-effective IoT solutions tailored for smallholder farmers. Government programs and technological advancements are enabling widespread deployment of sensors, mobile-based platforms, and analytics tools. With strong manufacturing capabilities and supportive policies, the Asia Pacific is expected to remain a key growth engine for the Agriculture IoT market.

Competitive Landscape

The global agriculture IoT market is moderately consolidated, with a mix of established global technology providers and numerous regional and niche players addressing specific farming needs. While leading players dominate core offerings such as connected equipment and integrated platforms, smaller firms focus on localized solutions, language support, and specialized applications, fostering continuous innovation and competitive diversity across the ecosystem.

Companies are actively expanding through partnerships, acquisitions, and product innovation to strengthen their capabilities in sensors, software, and cloud-based platforms. There is a growing focus on AI-driven analytics, edge computing, and system interoperability. Additionally, flexible business models such as subscription-based services and usage-based pricing are gaining traction, making IoT solutions more accessible to a wider range of farmers.

Key Developments:

- In June 2025, Deere & Company introduced its AI-powered See & Spray Ultimate system, leveraging computer vision and machine learning to identify weeds in real time and apply herbicides selectively, significantly improving efficiency and reducing chemical usage across large-scale U.S. farming operations.

- In March 2024, Trimble Inc. partnered with Bayer to develop advanced cloud-based crop monitoring solutions across Europe, integrating IoT data, satellite imagery, and analytics platforms to enhance decision-making, improve crop health insights, and support precision agriculture adoption among regional farmers.

- In October 2024, Raven Industries launched autonomous sprayer systems equipped with IoT capabilities in Brazil, enabling precise and automated application of inputs, reducing operational costs, improving field efficiency, and supporting large-scale farms in adopting advanced precision agriculture technologies.

Companies Covered in Agriculture IoT Market

- Deere & Company

- Trimble Inc.

- AGCO Corporation

- Raven Industries

- Topcon Corporation

- DeLaval

- Merck & Co., Inc.

- Kubota Corporation

- The Climate Corporation

- Farmers Edge Inc.

- Ag Leader Technology

- Libelium Comunicaciones Distribuidas S.L.

- AKVA Group

- Innovasea Systems Inc.

- GEA Group Aktiengesellschaft

Frequently Asked Questions

The agriculture IoT market is projected to reach US$ 36.3 billion in 2026, driven by rapid adoption of precision farming and IoT-enabled technologies.

Key drivers include rising demand for precision farming (42% share), cost optimization, climate resilience, and supportive government initiatives.

North America leads with 35% share (2025) due to advanced mechanization and strong digital infrastructure.

Edge AI integration presents a major opportunity by enabling real-time analytics and scalable IoT adoption across farms.

Leading players include Deere & Company, Trimble Inc., Raven Industries, AGCO Corporation, CNH Industrial, Topcon Positioning Systems, and Hexagon Agriculture.