- Technology

- Structured Data Management Software Market

Structured Data Management Software Market Size, Share, and Growth Forecast 2026 - 2033

Structured Data Management Software Market by Deployment Model (Cloud-Based, On-Premises, Hybrid), by Component (Software, Services), Organization Size (Small Enterprises, Medium Enterprises, Large Enterprises), Application, End-user, and Regional Analysis, 2026 - 2033

Structured Data Management Software Market Size and Trend Analysis

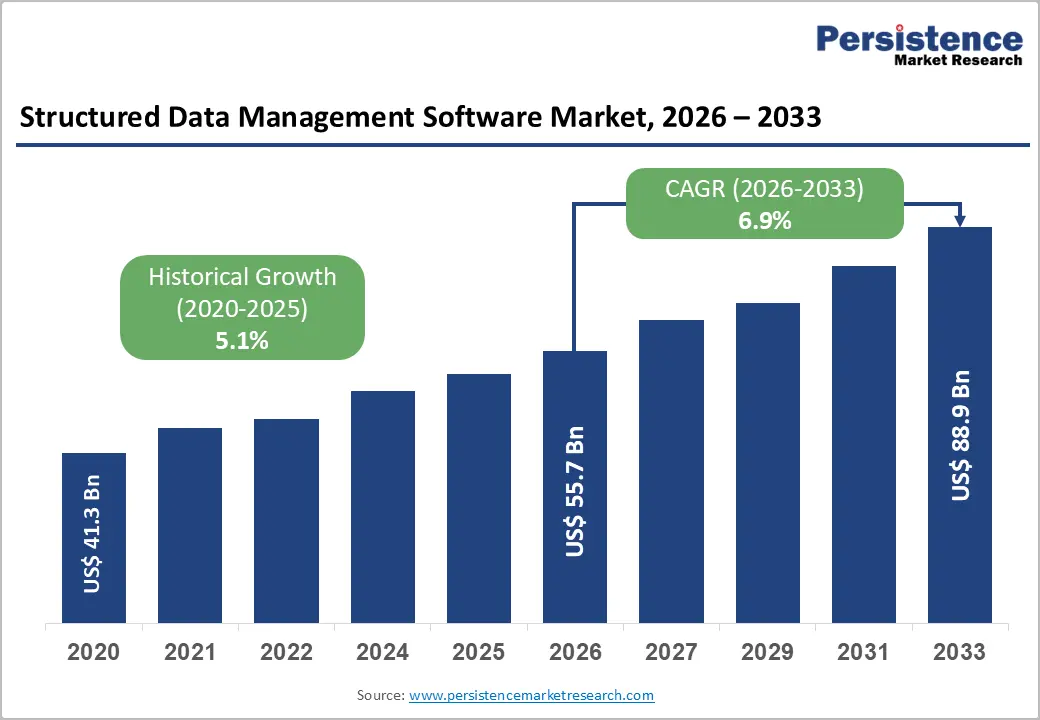

The global structured data management software market size is likely to be valued at US$55.7 billion in 2026 and is expected to reach US$88.9 billion by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 to 2033.

The market is advancing at a robust pace, driven by the exponential growth of enterprise data volumes, accelerating cloud adoption across industries, and the increasing imperative for regulatory compliance in data governance.

Key Industry Highlights:

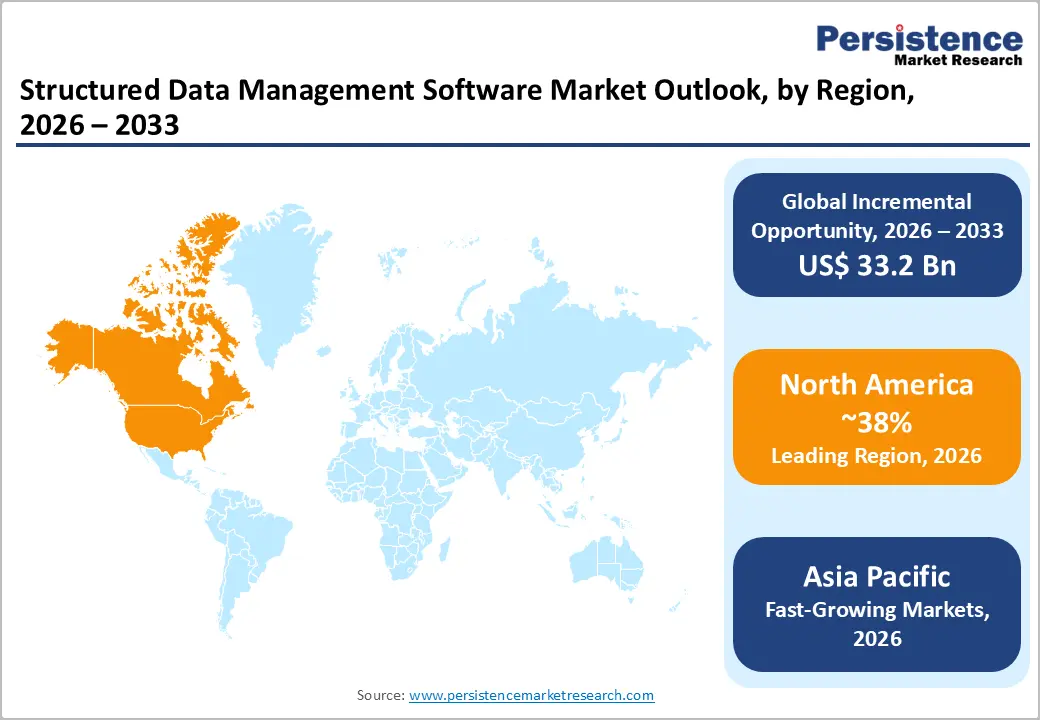

- Leading Region: North America is the leading region in the market holding 38 % share, led by the United States, dominates the global Structured Data Management Software Market, home to industry leaders including IBM, Oracle, Microsoft, and Snowflake, supported by the world's highest enterprise technology investment density and a robust data governance regulatory framework.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market with rising CAGR of 8.7%, driven by China's digital economy mandate under the 14th Five-Year Plan, India's Digital Personal Data Protection Act (DPDPA) 2023 compliance investment, and accelerating cloud adoption across ASEAN digital economy initiatives.

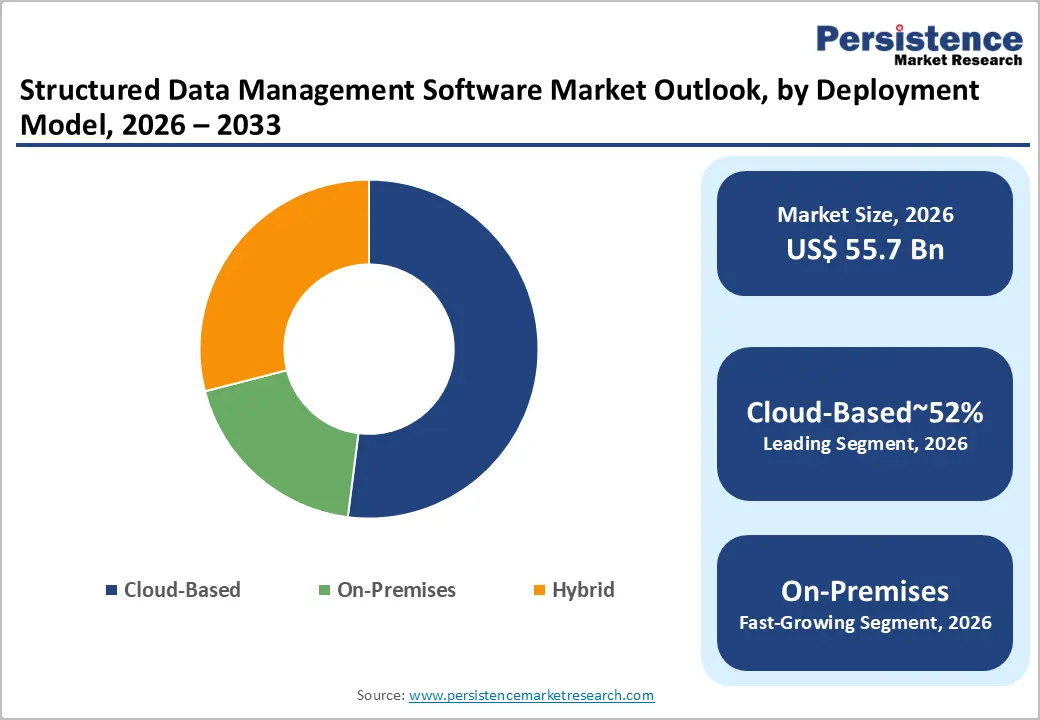

- Dominant Segment: Cloud-Based deployment leads the Deployment Model category with approximately 52% market share, propelled by enterprise multi-cloud strategies, elastic scalability requirements, and the dominance of platforms such as Amazon Redshift, Google BigQuery, and Microsoft Azure Synapse Analytics.

- Fastest Growing Segment: The BFSI end-use vertical is the dominant and fastest-growing sector, driven by real-time financial analytics demand, regulatory mandates including Basel IV, IFRS 9, and DORA, and the explosive growth of digital payments projected to exceed US$ 14 Trillion by 2027 per the BIS.

- Key Opportunity: AI and machine learning integration into structured data management platforms represents the defining growth opportunity, with AI projected to contribute US$ 15.7 Trillion to the global economy by 2030 per the WEF, positioning AI-native data management vendors for outsized revenue growth through 2033.

| Key Insights | Details |

|---|---|

| Structured Data Management Software Market Size (2026E) | US$ 55.7 Billion |

| Market Value Forecast (2033F) | US$ 88.9 Billion |

| Projected Growth CAGR (2026 - 2033) | 6.9% |

| Historical Market Growth (2020 - 2025) | 5.1% |

Market Dynamics

Drivers - Rapid Enterprise Cloud Adoption and Data Modernization Initiatives Driving Structured Data Management Software Market Growth Globally

The rapid shift of enterprise workloads to cloud infrastructure is a major structural driver for the Structured Data Management Software Market. According to the Flexera 2024 State of the Cloud Report, nearly 89% of enterprises now follow a multi-cloud strategy, with data management tools ranking among the top three technology investment priorities. Cloud-native structured data platforms allow organizations to scale storage and computing resources independently, reduce overall ownership costs, and enable real-time analytics that legacy on-premises systems cannot support.

Leading cloud providers such as AWS, Microsoft Azure, and Google Cloud are investing heavily in expanding their data infrastructure capabilities. These continuous investments are accelerating demand for structured data management solutions that seamlessly integrate with cloud ecosystems, helping enterprises modernize their data architecture while improving agility, performance, and decision-making efficiency across distributed business environments.

Rising Global Data Privacy Regulations Accelerating Enterprise Adoption of Structured Data Governance and Compliance Management Solutions

The growing number of global data privacy and governance regulations is pushing organizations to adopt advanced structured data management platforms. These platforms ensure data lineage, auditability, and compliance with evolving legal requirements. Regulations such as GDPR in Europe, which impose heavy penalties for non-compliance, have set global benchmarks for data protection standards.

Laws such as CCPA and the proposed APRA in the United States are strengthening the need for compliance-focused data systems. As per the International Association of Privacy Professionals, more than 160 data protection laws were active worldwide by 2023. This expanding regulatory landscape is driving continuous enterprise investment in structured data management tools equipped with automated compliance features, real-time monitoring, and audit capabilities. As a result, organizations are prioritizing data governance as a core component of their digital transformation strategies.

Market Restraints

High Implementation Complexity and Costs Challenges Structured Data Management Software Adoption Among Small And Medium Enterprises

Implementing enterprise-level structured data management software often requires significant investment in licensing, system integration, customization, and workforce training. Large-scale deployments can take between 18 and 36 months and may involve substantial spending on professional services. This creates a major barrier, especially for small and medium enterprises (SMEs), which often lack the required technical expertise and financial capacity.

Integrating modern data platforms with legacy systems, commonly found in sectors like banking and manufacturing, adds further complexity and risk. These legacy infrastructures, including decades-old databases, require careful migration and compatibility planning. As a result, long implementation timelines and high upfront costs can slow down purchasing decisions and limit market adoption. This challenge continues to restrict broader market penetration despite the increasing demand for advanced data management solutions.

Increasing Data Security Risks and Cloud Vulnerabilities Restraining Adoption Of Cloud-Based Structured Data Management Platforms

Concerns around data security and sovereignty remain key barriers to the adoption of cloud-based structured data management solutions. This is particularly critical in highly regulated industries such as banking, healthcare, and government sectors. According to the IBM Security Cost of a Data Breach Report 2023, the global average cost of a data breach reached USD 4.45 million, highlighting the financial impact of security failures.

Common causes include compromised credentials and cloud misconfigurations, which increase organizational risk. As a result, many enterprises prefer hybrid or on-premises solutions to maintain greater control over sensitive data. These security concerns often delay full cloud adoption and extend decision-making cycles. Consequently, while cloud solutions offer scalability and efficiency, perceived risks around data protection continue to influence enterprise strategies and limit the growth of fully cloud-based deployments.

Opportunities - Integration of Artificial Intelligence and Machine Learning, Transforming Structured Data Management Platforms and Enhancing Operational Efficiency

The integration of artificial intelligence (AI) and machine learning (ML) into structured data management platforms presents a significant growth opportunity for the market. AI-powered tools enable automated data quality checks, intelligent schema mapping, natural language querying, and predictive data governance. These capabilities reduce manual workloads for data teams and improve operational efficiency.

According to the World Economic Forum, AI is expected to contribute approximately USD 15.7 trillion to the global economy by 2030, with data platforms playing a critical role in supporting AI-driven applications. Leading vendors are increasingly embedding generative AI features into their platforms, allowing organizations to extract faster and more meaningful insights from structured data. This convergence of AI and data management is transforming how enterprises handle data, making processes more efficient, scalable, and cost-effective while enhancing overall decision-making capabilities.

Growing Demand in BFSI for Real-Time Financial Analytics Driving Structured Data Management Software Market Expansion Globally

The BFSI sector is emerging as the most valuable and fastest-growing end-use segment for structured data management software. This growth is driven by increasing demand for real-time analytics in fraud detection, algorithmic trading, regulatory reporting, and customer data management. The global rise in digital payment transactions, expected to exceed USD 14 trillion by 2027, is generating massive volumes of structured data.

Financial institutions are under pressure to process this data efficiently while complying with strict regulatory requirements such as Basel IV, IFRS standards, and digital resilience frameworks. These demands are encouraging investment in advanced data management platforms that support real-time processing, accurate reporting, and data lineage tracking. As a result, the BFSI sector continues to create strong and sustained demand for structured data management solutions, making it a key driver of long-term market growth.

Category-wise Analysis

Deployment Model Insights

Cloud-based deployment leads the structured data management software market, accounting for approximately 52% of total revenue. This dominance is driven by the scalability, flexibility, and cost efficiency offered by cloud solutions. Organizations benefit from elastic pricing models and seamless integration with modern analytics and data pipeline tools. As data volumes continue to grow rapidly, cloud platforms enable businesses to manage and process information more effectively across distributed environments.

Reports indicate that enterprise cloud spending frequently exceeds planned budgets, reflecting strong commitment to cloud-first strategies. Platforms such as Amazon Redshift, Google BigQuery, Snowflake, and Azure Synapse Analytics have become essential components of modern data ecosystems. These solutions provide high-performance capabilities for managing structured data at scale. As enterprises continue to prioritize digital transformation, cloud deployment is expected to remain the dominant and fastest-growing segment through the forecast period.

Component Insights

Software dominates the component segment, contributing approximately 68% of the total market revenue. This includes relational database systems, cloud data warehouses, data integration tools, and master data management solutions. These software platforms form the backbone of enterprise data infrastructure by enabling efficient storage, processing, and analysis of structured data. Increasing complexity in data environments, combined with the rise of hybrid and multi-cloud architectures, is driving continuous demand for advanced software solutions.

Organizations are investing heavily in tools that support real-time analytics, automation, and seamless data integration. At the same time, services such as consulting, implementation, and managed support are gaining importance as complementary offerings. These services help organizations optimize deployment and maximize return on investment. Overall, the software segment continues to lead due to its critical role in enabling data-driven business operations.

Organization Size Insights

Large enterprises account for around 61% of the structured data management software market revenue, making them the dominant customer segment. These organizations handle vast volumes of data across multiple systems, requiring advanced platforms for data governance, integration, and compliance. Large enterprises typically operate complex IT environments with numerous interconnected databases and applications.

This complexity drives the need for centralized data management solutions that ensure consistency, accuracy, and regulatory compliance. Additionally, these organizations have the financial resources to invest in high-end software and long-term implementation projects. Their focus on digital transformation and data-driven decision-making further strengthens demand for structured data management platforms. While small and medium enterprises are increasingly adopting cloud-based solutions, large enterprises remain the primary revenue contributors due to their scale, complexity, and regulatory requirements.

Application Insights

Financial analytics is the leading application segment, contributing approximately 22% of total market revenue. The need for accurate and timely financial data is critical for organizations operating in global markets. Structured data management platforms support various financial applications, including risk assessment, fraud detection, portfolio analysis, and regulatory reporting. These use cases require high-performance systems capable of processing large volumes of transactional data in real time.

Regulatory authorities impose strict reporting standards, further increasing the demand for reliable data management solutions. Additionally, the adoption of cloud-based data warehouses and machine learning technologies is enhancing financial analytics capabilities. Organizations are leveraging these tools to gain deeper insights and improve decision-making. As financial operations become more complex and data-intensive, the demand for structured data management in financial analytics is expected to grow steadily.

End-user Insights

The BFSI sector leads the end-use segment, accounting for approximately 24% of total market revenue. Financial institutions generate and process massive amounts of structured data, including customer information, transaction records, and risk data. Managing this data efficiently is essential for ensuring operational accuracy and regulatory compliance. The global banking sector manages assets worth trillions of dollars, highlighting the scale of data infrastructure required.

Regulations such as Basel standards and financial reporting frameworks require institutions to maintain detailed data records and audit trails. Structured data management platforms play a critical role in meeting these requirements. They enable accurate reporting, real-time monitoring, and improved data governance. As financial institutions continue to expand digital services and adopt advanced technologies, the demand for structured data management solutions remains strong and essential.

Regional Insights

North America Structured Data Management Software Market Trends

North America remains the leading region in the Structured Data Management Software Market, driven by strong technological infrastructure and high enterprise adoption. The United States, in particular, hosts a large number of leading technology companies and cloud service providers. The region benefits from continuous innovation, skilled workforce availability, and significant investment in enterprise software.

Government initiatives focused on data modernization are also contributing to market growth. These programs encourage organizations to adopt advanced data management solutions for improved efficiency and transparency. Canada is also experiencing steady growth, supported by increasing cloud adoption and regulatory requirements. Overall, North America continues to dominate due to its mature technology ecosystem and strong demand for data-driven business solutions.

Europe Structured Data Management Software Market Trends

Europe is the second-largest market, characterized by a strong focus on data governance and regulatory compliance. Strict regulations such as GDPR and emerging data policies are driving consistent demand for structured data management solutions. Organizations are required to maintain high standards of data security, transparency, and accountability.

Germany leads the region due to its strong industrial base and investment in digital transformation initiatives. The United Kingdom and other European countries are also adopting advanced data management technologies to support innovation and compliance. Increasing cloud adoption and cross-border data initiatives are further boosting market growth. Overall, Europe presents a stable and regulation-driven market environment.

Asia Pacific Structured Data Management Software Market Trends

Asia Pacific is the fastest-growing regional market, fueled by rapid digital transformation across emerging economies. Countries such as China, India, and Japan are investing heavily in data infrastructure and cloud technologies. Government initiatives supporting digital economies are accelerating adoption across industries. In India, strong growth in IT services and cloud adoption is driving demand for structured data management solutions. Southeast Asian countries are also expanding digital ecosystems, creating new opportunities for vendors. The region’s growing data volumes and increasing regulatory focus are further supporting market expansion. As a result, the Asia Pacific is expected to remain a key growth engine in the coming years.

Competitive Landscape

The global structured data management software market is moderately consolidated, with major global technology companies holding significant market share. These companies offer comprehensive platforms and maintain strong relationships with enterprise customers. Key competitive factors include advanced analytics capabilities, cloud integration, and regulatory compliance features.

New market entrants are challenging established players by offering cloud-native solutions and flexible pricing models. Strategic partnerships and acquisitions are common, helping companies expand their capabilities and market reach. The shift toward subscription-based and platform-as-a-service models is also transforming the competitive landscape. Overall, the market remains dynamic, with continuous innovation driving competition and growth.

Key Developments:

- February 2025: Snowflake Inc. announced the general availability of its Snowflake Arctic AI model integrated directly into its structured data management platform, enabling enterprise customers to run generative AI workloads natively on their structured data without data movement.

- October 2024: IBM Corporation launched the next generation of its IBM Db2 platform with enhanced AI-assisted query optimization and automated data governance capabilities, targeting large enterprise and regulated industry customers across the BFSI and healthcare verticals.

- March 2024: Microsoft Corporation expanded its Microsoft Fabric unified data platform with new structured data integration capabilities and native Copilot AI assistance, accelerating enterprise adoption of its end-to-end cloud data management ecosystem across Azure customers globally.

Companies Covered in Structured Data Management Software Market

- IBM Corporation

- Oracle Corporation

- Microsoft Corporation

- SAP SE

- Google LLC

- Amazon Web Services (AWS)

- Teradata Corporation

- Informatica Inc.

- SAS Institute Inc.

- Talend S.A.

- Cloudera Inc.

- Snowflake Inc.

- TIBCO Software Inc.

- OpenText Corporation

- Hewlett Packard Enterprise

- Alibaba Cloud

- Salesforce Inc.

- Databricks Inc.

Frequently Asked Questions

The global structured data management software market is projected to reach US$ 88.9 billion by 2033, growing at a CAGR of 6.9% during the forecast period 2026 - 2033, from an estimated US$ 55.7 Billion in 2026. The market recorded a historical CAGR of 5.1% between 2020 and 2025, reflecting sustained enterprise investment in data governance and analytics infrastructure.

The primary demand drivers are accelerating enterprise cloud migration, with approximately 89% of enterprises adopting multi-cloud strategies per the Flexera 2024 State of the Cloud Report, and expanding data governance regulations, including the EU GDPR, CCPA, and over 160 national data protection laws globally as tracked by the International Association of Privacy Professionals (IAPP), compelling sustained investment in structured data management platforms.

Cloud-Based deployment dominates the market with approximately 52% of total revenue, driven by enterprise multi-cloud adoption, elastic scalability requirements, and the dominance of cloud data platforms including Amazon Redshift, Google BigQuery, Snowflake, and Microsoft Azure Synapse Analytics. Cloud deployment enables real-time analytics capabilities and lower total cost of ownership versus legacy on-premises database architectures.

North America, led by the United States, is the dominant regional market. The U.S. hosts the global headquarters of leading vendors including IBM, Oracle, Microsoft, Snowflake, and AWS, while the Federal Data Strategy, CCPA, and Evidence Act of 2018 drive both private sector and government data management investment. The U.S. information technology sector contributes approximately 10% of GDP per the U.S. Bureau of Economic Analysis (BEA).

The integration of artificial intelligence and machine learning into structured data management platforms represents the defining growth opportunity through 2033. With AI projected to contribute US$ 15.7 Trillion to the global economy by 2030 per the World Economic Forum (WEF), vendors embedding generative AI, such as Snowflake's Arctic model and IBM's AI-enhanced Db2 platform, are positioned to capture significant market share through enhanced data automation and governance capabilities.

Key market participants include IBM Corporation, Oracle Corporation, Microsoft Corporation, SAP SE, Google LLC, Amazon Web Services, Teradata Corporation, Informatica Inc., SAS Institute Inc., Talend S.A., Cloudera Inc., Snowflake Inc., TIBCO Software Inc., OpenText Corporation, and Hewlett Packard Enterprise, along with emerging challengers such as Databricks Inc. and Alibaba Cloud.