- Beverages

- Yogurt and Probiotic Drink Market

Yogurt and Probiotic Drink Market Size, Share, and Growth Forecast 2026 - 2033

Yogurt and Probiotic Drink Market by Product Type (Yogurt Drink, Juice, Kefir, Others), Source Type (Dairy-based, Plant-based, Water-based), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Retail, Others), and Regional Analysis, 2026 - 2033

Yogurt and Probiotic Drink Market Share and Trends Analysis

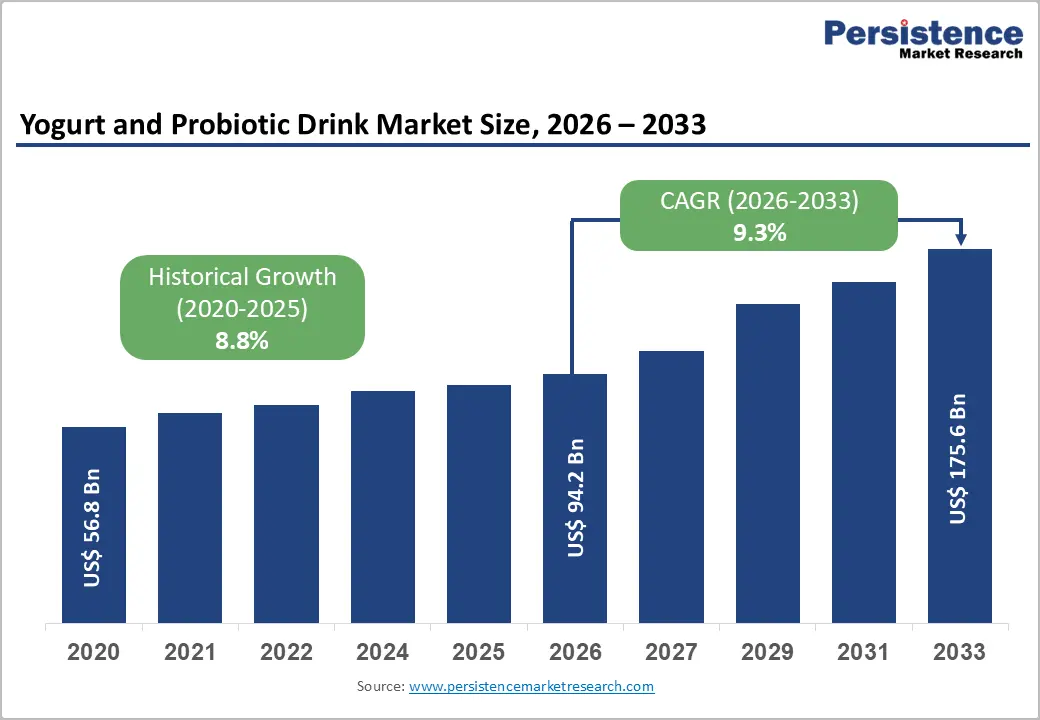

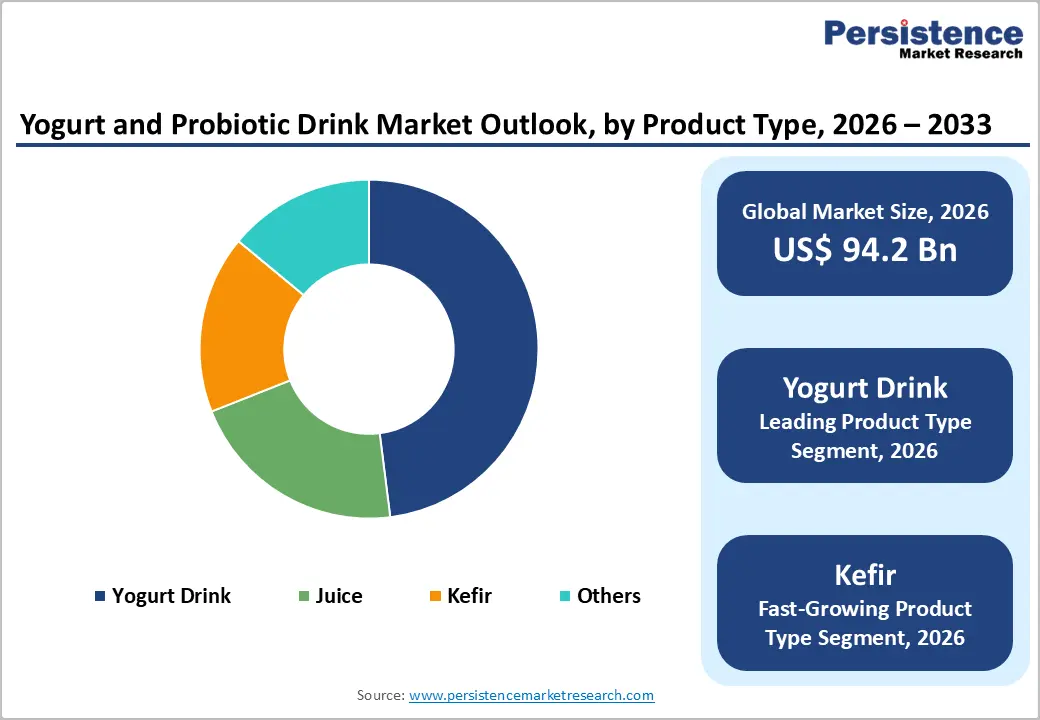

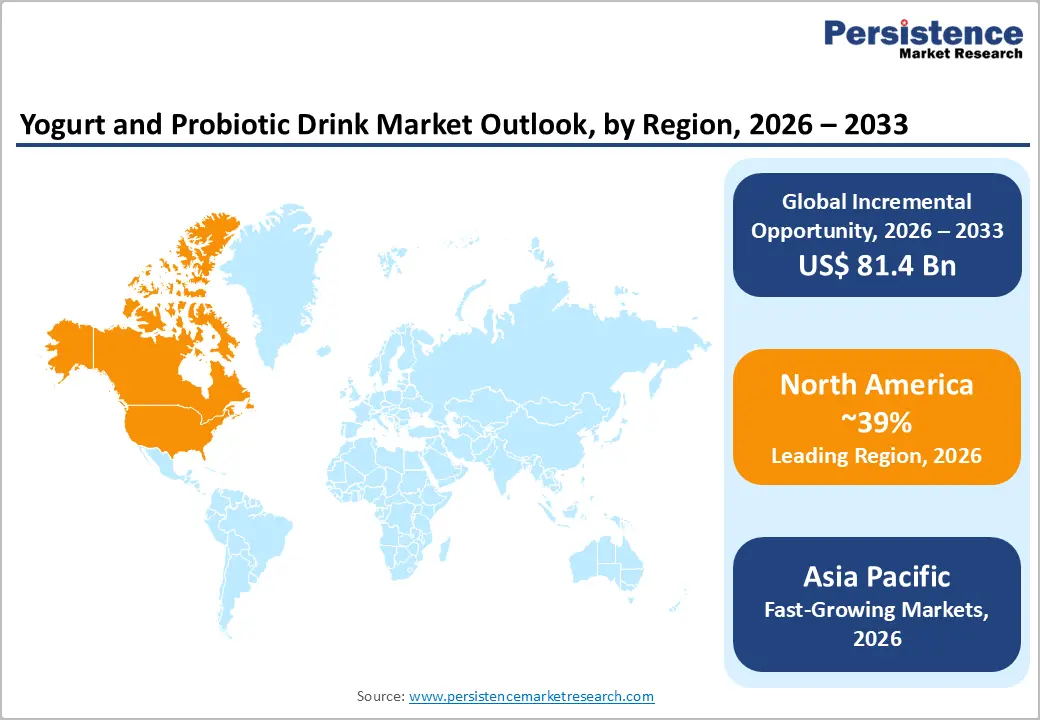

The global Yogurt and Probiotic Drink market size is expected to be valued at US$ 94.2 billion in 2026 and projected to reach US$ 175.6 billion by 2033, growing at a CAGR of 9.3% between 2026 and 2033.

Rising consumer focus on gut health, the shift toward preventive nutrition, and rapid product innovation in both dairy and plant-based probiotic beverages underpin this robust outlook. Scientific reviews increasingly link fermented dairy products with benefits for bone, metabolic, and gastrointestinal health, reinforcing consumer trust and repeat purchases. At the same time, yogurt and probiotic drinks fit the demand for convenient, on-the-go functional beverages that can be easily integrated into daily routines.

Key Industry Highlights:

- Regional Leadership: North America remains the largest revenue contributor to the Yogurt and Probiotic Drink market, supported by high dairy consumption, advanced retail infrastructure, and strong presence of leading brands focused on gut-health and immune-supporting beverages.

- Fast-growing Market: Asia Pacific is projected to be the fastest-growing region, driven by urbanization, rising disposable incomes, and cultural acceptance of fermented foods, with China, Japan, India, and ASEAN markets rapidly expanding their portfolios of yogurt drinks, kefir, and plant-based probiotic beverages.

- Leading Source Type: The Dairy-based segment dominates by source type, contributing well over half of global revenues due to strong clinical evidence, nutritional density, and established consumer trust in fermented milk products, while plant-based alternatives scale from a smaller base.

- Leading Product Type: The Kefir segment is emerging as the fastest-growing product type, as consumers seek more diverse probiotic profiles and experiment with both dairy and water-based kefir, often positioned as a more potent or artisanal alternative to conventional yogurt drinks.

- Opportunity: A key opportunity lies in premiumized, personalized functional formulations that combine specific probiotic strains with vitamins, minerals, and bioactives to target immune health, metabolic wellness, or beauty benefits, enabling higher margins and stronger brand loyalty.

| Key Insights | Details |

|---|---|

|

Yogurt and Probiotic Drink Market Size (2026E) |

US$ 94.2 billion |

|

Market Value Forecast (2033F) |

US$ 175.6 billion |

|

Projected Growth CAGR (2026-2033) |

9.3% |

|

Historical Market Growth (2020-2025) |

8.8% |

Market Dynamics

Drivers - Rising Focus on Gut Health and Preventive Nutrition

Growing awareness of the gut–microbiome–immunity axis is a primary demand driver for yogurt and probiotic drinks. Clinical and systematic reviews show that fermented milk and yogurt consumption can improve lactose digestion, support weight management, and lower risks of type 2 diabetes and cardiovascular disease, strengthening their positioning as everyday health foods rather than occasional indulgences. Evidence also indicates that probiotic-rich beverages help modulate the gut microbiota, improve intestinal barrier function, and may reduce the incidence of obesity and metabolic disorders. In consumer surveys, a majority of yogurt users cite general health and digestive wellness as key purchase motivations, with about 70% consuming yogurt for overall health and 60% specifically for gut health, highlighting the strong alignment of these drinks with preventive nutrition behaviors.

Convenience, Urban Lifestyles, and On-the-Go Consumption

Urbanization and busier lifestyles are accelerating demand for portable, ready-to-drink probiotic products that deliver both nutrition and convenience. In the United States, loss-adjusted yogurt availability has increased roughly fivefold over the last four decades, reflecting its shift from a niche breakfast item to an all-day snack and beverage occasion. Industry and dietary statistics show that consumers increasingly use drinkable yogurts, yogurt shots, and single-serve probiotic beverages as snacks or meal replacements, attracted by their protein content, live cultures, and perceived weight-management benefits. Fermented foods such as yogurt, kefir, and other cultured drinks are now among the most popular choices for consumers seeking gut-friendly options, with nearly 3 in 5 U.S. consumers actively looking for foods that support their microbiome. This on-the-go format advantage strongly supports sustained growth for yogurt drinks, kefir, and other probiotic beverages.

Restraints - Regulatory Complexity and Claims Management

Regulatory frameworks governing probiotic labeling and health claims remain complex and fragmented across regions, creating compliance challenges and lengthening product-development timelines for market players. In the United States, the U.S. Food and Drug Administration (FDA) distinguishes between foods, dietary supplements, and drugs, with probiotic-containing products subject to different requirements depending on the claims made.

The guidelines from the Consumer Healthcare Products Association (CHPA) stress accurate strain identification and colony-forming unit (CFU) declaration to align labels with available scientific evidence. Inconsistent enforcement and varying interpretations of what constitutes a permissible structure/function or health claim can discourage aggressive messaging around benefits, limiting consumer understanding and slowing adoption in more regulated markets.

Safety Perceptions and Quality Variability

Although probiotics are generally regarded as safe for healthy populations, isolated safety concerns and inconsistent product quality can restrain growth among risk-averse consumers and healthcare professionals. Scientific reviews note that certain probiotic strains, such as Saccharomyces boulardii, require caution in hospitalized or immunocompromised patients due to rare cases of fungemia, highlighting the importance of strain-specific risk assessment. At the same time, guidelines from industry and scientific bodies emphasize that not all products marketed as “probiotic” meet standards for strain documentation, viability at the end of shelf life, or evidence-backed dosages. Variability in live culture counts, improper storage, and unclear labeling can erode trust, prompting regulators and professional associations to call for tighter quality control and clearer consumer information, thereby increasing compliance costs and slowing launches.

Opportunities - Premiumization and Personalized Functional Nutrition

The shift from generic dairy drinks to targeted functional formulations creates significant headroom for premium, science-backed yogurt and probiotic beverages. Personalized nutrition trends are encouraging manufacturers to develop products tailored to specific health outcomes such as immune support, metabolic health, satiety, or skin benefits, often using differentiated probiotic strains and complementary bioactives.

Recent launches of fortified drinkable yogurts combining live cultures with vitamins, minerals, and bioactive ingredients like collagen or zinc illustrate how brands are moving up the value ladder. As consumers gain access to more health data through apps and diagnostics, demand is rising for “problem solution” beverages, for example, formulations focusing on lactose digestion, antibiotic-associated diarrhea, or stress and sleep support, allowing companies to segment the market and command higher price points while deepening brand loyalty.

Expansion of Plant-Based and Non-Dairy Probiotic Beverages

The rapid growth in the diagnosis of lactose intolerance, vegan lifestyles, and flexitarian diets is creating significant opportunities for plant-based and water-based probiotic drinks. Scientific and industry reports highlight the emergence of probiotic beverages based on almond, soy, oat, coconut, and other plant matrices, which can deliver live cultures while meeting dairy-free or halal/vegetarian preferences.

Dairy-based products currently dominate probiotic drink revenue shares, but the plant-based segment is the fastest growing, driven by innovation in taste, texture, and stability of non-dairy formulations. Fermented plant drinks and water kefir tap into the same gut-health and immunity narratives as traditional dairy kefir, while also intersecting with broader trends toward sustainability and reduced animal-product consumption. This segment offers attractive whitespace for brands willing to invest in strain adaptation, clean-label ingredients, and temperature-stable supply chains.

Category-wise Analysis

Product Type Insights

The yogurt drink segment is the leading product type, accounting for around 48% share in 2025 and expected to maintain dominance throughout the forecast period. Industry analyses show that yogurt drinks remain the most widely consumed probiotic beverage format, owing to their familiar taste, creamy mouthfeel, and strong brand recognition in both developed and emerging markets.

Major brands such as Danone S.A., Yakult Honsha Co., Ltd., Chobani, LLC, and General Mills, Inc. continue to expand portfolios of drinkable yogurts and probiotic shots, supported by scientific communication about digestive and immune benefits.

The Kefir segment, while smaller in absolute terms, is emerging as the fastest-growing product type due to its dense probiotic profile and versatility across dairy and water-based formats. As awareness of kefir’s diverse microbial strains and functional potential grows, it is poised to capture incremental share from both traditional yogurt drinks and carbonated soft drinks.

Source Type Insights

Within the source type, dairy-based products currently lead the yogurt and probiotic drink market, contributing well over half of global revenues in 2024–2025. Dairy-based probiotic drinks represent more than 55% of category sales, reflecting long-standing consumer familiarity with fermented milk beverages and extensive clinical evidence supporting their health benefits.

Reviews in nutrition science reinforce that yogurt and cultured milk are nutrient-dense, providing high-quality protein, calcium, and essential vitamins, as well as live cultures, which strengthen their value proposition among families and older adults. However, Plant-based probiotic beverages made with bases such as soy, almond, oat, and coconut are the fastest-growing segment, as consumers seek lactose-free, vegan, and perceived “cleaner” options.

Manufacturers are rapidly expanding portfolios of non-dairy probiotic drinks to capture this growth, often highlighting sustainability and allergen-friendly positioning, while Water-based formats like kombucha or water kefir serve niche but expanding consumer groups focused on low-calorie refreshment.

Distribution Channel Insights

Supermarkets and hypermarkets constitute the leading distribution channel for yogurt and probiotic drinks, accounting for the largest share of global category sales. Industry and association data indicate that mainstream grocery retailers provide the primary shelf space for fermented dairy and probiotic beverages, benefiting from high footfall, cold-chain infrastructure, and strong promotional capabilities.

Large-format stores frequently dedicate entire refrigerated aisles to yogurt, drinkable yogurts, and probiotic shots, which drives impulse purchases and encourages trial of new flavors, formats, and brands. Is online retail the fastest-growing distribution channel, propelled by broader e-commerce penetration, subscription models for functional beverages, and direct-to-consumer offerings from both multinational and challenger brands?

Digital platforms enable targeted marketing based on health interests and allow consumers to explore premium or niche probiotic beverages that may not be available in physical outlets, including refrigerated home delivery and ambient-stable probiotic shots.

Regional Insights

North America Yogurt and Probiotic Drink Market Trends and Insights

North America is a leading regional market, representing about 39% of global yogurt and probiotic drink revenues in 2025, anchored by high per-capita dairy consumption and a sophisticated functional food ecosystem. Data from the USDA Economic Research Service (ERS) show that yogurt consumption in the United States has grown roughly fivefold over the past four decades, even as fluid milk intake declined, underscoring the structural shift from traditional milk to value-added cultured products.

Consumers increasingly integrate drinkable yogurts and probiotic beverages into daily routines for breakfast, snacking, and post-exercise recovery, often prioritizing high-protein, low-sugar formulations. The region also benefits from a mature regulatory and innovation environment. The U.S. Food and Drug Administration (FDA) provides frameworks for food and dietary supplement labeling, while voluntary guidelines from bodies such as CHPA and the International Probiotics Association (IPA) encourage accurate strain labeling and CFU disclosure.

These structures, combined with strong retail penetration and marketing investments by companies like Danone S.A., General Mills, Inc., Chobani, LLC, and Lifeway Foods, Inc., support continuous product innovation in Greek-style drinkable yogurts, kefir, and plant-based probiotic drinks. The rising popularity of gut-health beverages and immunity-supporting drinks positions North America to remain a high-value, trend-setting region.

Asia Pacific Yogurt and Probiotic Drink Market Trends and Insights

Asia Pacific is the fastest-growing regional market for yogurt and probiotic drinks, driven by rising disposable incomes, rapid urbanization, and strong cultural familiarity with fermented foods. Persistence Market Research and other industry analyses indicate that the region is gaining share quickly, supported by widespread consumption in China, Japan, India, and ASEAN markets. Traditional products such as probiotic yogurt shots in Japan and drinkable yogurts in China serve as entry points for newer formats such as kefir, plant-based probiotic beverages, and functional yogurt drinks targeting beauty, immunity, or stress relief. Growing awareness of lactose intolerance and a shift toward Western-style snacking further drive demand for both dairy and non-dairy probiotic beverages.

Asia Pacific also benefits from a strong manufacturing base and cost-effective supply chains for cultured dairy and beverage processing. Literature on probiotics and fermented milk emphasizes the active role of regional researchers and companies in developing strains suitable for local diets and climatic conditions, including high-temperature-stable cultures and formulations tailored to rice or soy-based matrices.

The region’s young population and digital adoption are fueling the rapid expansion of online retail and quick-commerce channels for yogurt drinks and probiotic shots, positioning Asia Pacific as the key engine of volume growth and innovation in the coming decade.

Competitive Landscape

The yogurt and probiotic drink market is characterized by a moderately fragmented competitive landscape, with large multinational players alongside regional and niche brands. Established companies leverage strong brand recognition, extensive distribution networks, and advanced research capabilities to maintain their market position.

Smaller and emerging players compete by offering innovative products such as plant-based, low-sugar, and clean-label probiotic drinks, targeting health-conscious consumers. Continuous product innovation, strategic collaborations, and expansion into new markets are key competitive strategies.

Key Developments:

- In April 2026, CP-Meiji launched a new probiotic fermented milk drink available in lemon and original flavors, aimed at offering a refreshing and functional beverage option. The product was formulated with approximately 3 billion probiotics per bottle and positioned as a healthier choice, free of added sugar, low in cholesterol, fat-free, and containing about 60 kcal per serving.

- In May 2025, Probi partnered with Nomura Dairy Products and launched a probiotic-enhanced, plant-based carrot juice drink in Japan under the “My Flora” brand, marking a strategic entry into the country’s nascent plant-based probiotic segment.

Companies Covered in Yogurt and Probiotic Drink Market

- Danone S.A.

- Nestlé S.A.

- Yakult Honsha Co., Ltd.

- Chobani, LLC

- General Mills, Inc.

- Lactalis Group

- Fonterra Co-operative Group

- Arla Foods

- FrieslandCampina

- Lifeway Foods, Inc.

- Meiji Holdings Co., Ltd.

- Gujarat Cooperative Milk Marketing Federation Ltd. (Amul)

Frequently Asked Questions

The Yogurt and Probiotic Drink market is expected to reach around US$ 94.2 billion in 2026, driven by rising gut‑health awareness, growing preference for functional beverages, and ongoing product innovation across dairy‑based and plant‑based probiotic drinks.

The foremost demand driver is the increasing focus on gut health and preventive nutrition, supported by scientific evidence that regular yogurt and fermented milk consumption improves lactose digestion, supports metabolic and cardiovascular health, and contributes to immune function and weight management.

North America currently leads the market in value terms, supported by high per‑capita dairy consumption, strong presence of major probiotic drink brands, and a mature regulatory and retail ecosystem that facilitates widespread availability of yogurt drinks, kefir, and functional probiotic beverages.

A major opportunity lies in premium, personalized functional products that combine clinically studied probiotic strains with targeted nutrients or bioactives such as vitamins, minerals, and collagen to address specific needs including immunity, metabolic health, digestive comfort, and skin wellness.

Key players include multinational dairy and beverage companies such as Danone S.A., Nestlé S.A., Yakult Honsha Co., Ltd., Chobani, LLC, General Mills, Inc., Lactalis Group, Fonterra Co-operative Group, Arla Foods, FrieslandCampina, Lifeway Foods, Inc.