- Oil & Gas

- Wireline Services Market

Wireline Services Market Size, Share, and Growth Forecast, 2026 - 2033

Wireline Services Market by Service (Electric Line, Slick Line), Well Type (Open Hole, Cased Hole), Application (Well Completion, Well Intervention, Well Logging), and Regional Analysis for 2026 - 2033

Wireline Services Market Size and Trends Analysis

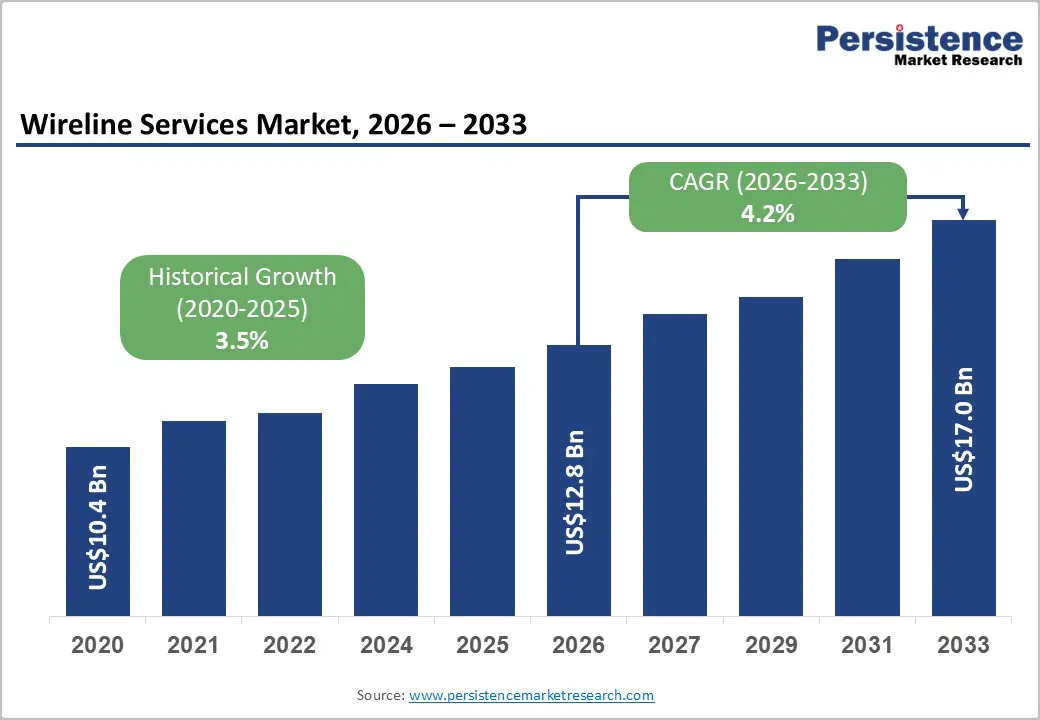

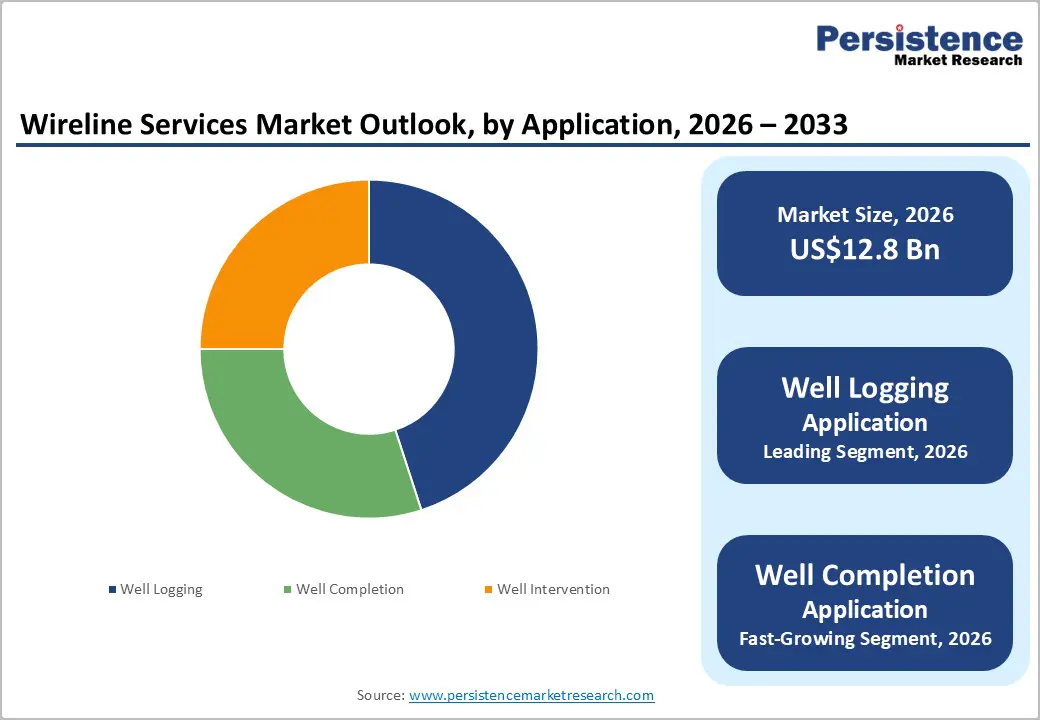

The global wireline services market size is likely to be valued at US$12.8 billion in 2026, and is expected to reach US$17.0 billion by 2033, growing at a CAGR of 4.2% during the forecast period from 2026 to 2033, driven by the increasing need for efficient downhole measurement, intervention, and completion services using electric and slick lines. These services are essential across the well lifecycle and play a critical role in optimizing upstream oil and gas operations.

Key Industry Highlights:

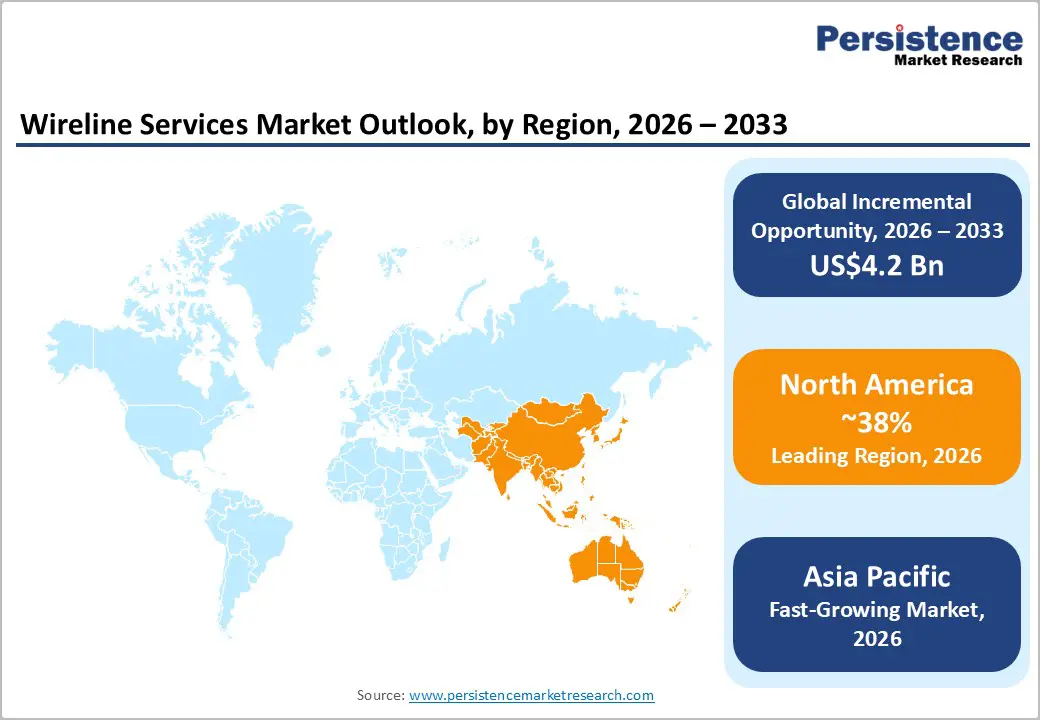

- Leading Region: North America is expected to dominate, approximately 38% in 2026, supported by intensive shale and tight oil activity in the U.S. Permian, Eagle Ford, and Bakken basins.

- Fastest-growing Region: Asia Pacific is expected to be the fastest growing, driven by China/India's offshore fields, Indonesia/Malaysia's deepwater boom, and rapid urbanization spiking energy demand. Shale exploration and capex in new E&P fuel slickline/e-line for logging and interventions.

- Dominant Service Type: The electric line segment is expected to dominate with an estimated ~62% revenue share in 2026, owing to its superior data transmission capabilities and versatility in complex well environments, while Slick Line remains cost-effective for targeted intervention tasks.

- Leading Well Type: Cased hole services are expected to account for approximately 70% of the well-type segment in 2026, supported by high volumes of well intervention, production logging, and perforation work on mature fields globally.

- Key Driver: Digital transformation, AI-assisted log interpretation, and the expansion of intelligent completions present high-value opportunities forecast to accelerate wireline service adoption through 2033.

DRO Analysis

Driver - Digital Oilfield Transformation and Adoption of Advanced Formation Evaluation Technologies

The accelerating integration of digital technologies, including IoT-enabled downhole sensors, real-time data transmission via fiber-optic wireline cables, and AI-assisted log interpretation platforms is significantly elevating the strategic value and frequency of wireline operations. Digital wireline systems now enable operators to transmit high-bandwidth formation data in real time from depths exceeding 20,000 feet, supporting instantaneous reservoir decisions and adaptive completion designs. This capability directly increases the number of wireline logging runs per well and expands the scope of services deployed per campaign.

Baker Hughes' FiberVision and Schlumberger's LIVE platform exemplify how integrated digital wireline ecosystems are transforming formation evaluation. These platforms combine advanced multi-physics logging tools with cloud-based analytics to deliver formation evaluation reports in hours rather than days, creating measurable operational efficiencies that incentivize broader wireline adoption. In the deepwater segment, where well costs routinely exceed US$100 million per well, the economic case for comprehensive formation evaluation via wireline is exceptionally strong.

Restraint - Volatility of Oil & Gas Prices and Upstream Capex Cyclicality

The wireline services market remains acutely exposed to oil price cycles, as upstream operators routinely curtail discretionary wireline programs during periods of oil price weakness. The 2020 collapse in crude oil prices, when Brent fell below US$20 per barrel, resulted in wireline service revenue declines of 35–40% within a single year for major providers, demonstrating the sector's cyclical vulnerability.

Even with partial structural improvements in operator spending discipline, a sustained downturn in oil prices below the US$60 per barrel threshold would likely prompt meaningful reductions in wireline call-out volumes. This inherent cyclicality makes sustained workforce and capital investment in wireline difficult for service companies, potentially constraining capacity expansion ahead of demand inflections.

Opportunity - Deepwater and Ultra-Deepwater Wireline Expansion

Rising demand for offshore hydrocarbons drives expansion in deepwater (500-3,000m) and ultra-deepwater (>3,000m) wireline operations, enabling precise well interventions without full rigs. Wireline using slickline for mechanical tasks or e-line for powered logging deploys tools for perforating, logging, and plug-and-abandon (P&A) in high-pressure, high-temperature (HPHT) environments.

Innovations such as riserless wireline logging enable access to ultra-shallow formations prior to casing installation, significantly reducing operational costs compared to conventional rig-based methods. Real-time depth control supported by live telemetry enhances precision and efficiency in complex well completions, while advanced heavy-duty cables facilitate extended reach in ultra-long deployments. Key growth drivers include recent discoveries in Guyana and Namibia, rapid industrialization across Asia Pacific, and increasing adoption of subsea tieback developments focused on lower-carbon production. Additionally, operators such as Shell are expanding their activities in Malaysia by deploying AI-optimized wireline systems to accelerate data acquisition, minimize downtime, and improve overall exploration economics.

Category-wise Analysis

Service Insights

Electric line services are expected to dominate the segment, accounting for an estimated 62% of total service revenue in 2026. Electric line's superiority stems from its capacity to transmit high-resolution formation data in real time through its conductive cable, enabling multi-physics logging, perforation, and intervention operations with instantaneous data readback. In a Schlumberger electric-line intervention case study, operators used a fully controllable e-line powered shifting tool to diagnose and fix a failed sliding sleeve in a well.

Slick line is likely to represent the fastest-growing segment, serving a complementary role focused primarily on mechanical intervention tasks, valve actuation, plug retrieval, gauge deployment, and simple perforating operations. Baker Hughes, which provides dedicated slickline services for routine well interventions. Slickline is used to shift sliding sleeves, set/retrieve plugs, and perform fishing operations.

Well Type Insights

Cased hole is anticipated to dominate the market with approximately 70% revenue share in 2026, reflecting the larger universe of producing and mature wells requiring ongoing surveillance, perforation, and mechanical intervention relative to newly drilled open-hole environments. SLB provides wireline cased-hole logging and perforating services that are specifically designed for producing and mature wells. Production logging and reservoir monitoring during the entire life of the well.

Open hole is likely to be the fastest growing, driven by performing during the drilling phase to evaluate formation properties before casing is run. Rising exploration activity in frontier basins, particularly in East Africa, Guyana, and offshore Southeast Asia, is driving demand for comprehensive open-hole formation evaluation suites. SLB (Schlumberger), where open-hole wireline logging was deployed in horizontal wells in the Bahrain Oilfield. SLB used wireline open-hole logging tools conveyed via the UltraTRAC tractor in uncased horizontal sections.

Application Insights

Well logging is expected to dominate applications with ~45% revenue share in 2026, supported by its essential role in subsurface formation characterization across exploration and development. Formation evaluation is non-discretionary, as operators rely on log-derived data such as porosity, permeability, and saturation to make development decisions. Halliburton’s well logging services are used to quantify porosity, saturation, and lithology, which directly determine hydrocarbon volumes and guide field development, reinforcing the segment’s resilience across commodity cycles.

Well completion is forecast to be the fastest-growing application segment. The surge in multi-stage hydraulic fracturing completions, particularly in the U.S., China, and Argentina, is generating strong demand for perforation services, plug setting, and post-frac diagnostic logging delivered via wireline. Halliburton utilizes wireline-conveyed perforating and pump-down systems to execute multi-stage completions, enabling efficient reservoir stimulation and driving strong demand for perforation, plug setting, and post-frac diagnostic services.

Regional Insights

North America Wireline Services Market Trends

North America is estimated to dominate, accounting for 38% revenues in 2026, with the U.S. representing the majority of regional demand. Wireline companies service multiple wells per pad simultaneously, with average perforation job counts per horizontal well in the Permian routinely exceeding 30 stages, creating structural volume that sustains service provider revenues even during moderate oil price environments.

U.S. Wireline Services Market Insights

The U.S. market is structurally anchored by the high-velocity unconventional plays of the Permian Basin, Eagle Ford, Haynesville, and Bakken formations, where plug-and-perforation completion methods generate extraordinarily high wireline activity per pad.

Canada Wireline Services Market Insights

Canada's wireline market is driven by Alberta's oil sands, SAGD (Steam-Assisted Gravity Drainage) thermal projects, and the Montney tight gas play in British Columbia, which is attracting significant LNG-linked investment. Montney completion activity is forecast to remain elevated through 2033 as LNG Canada Phase 2 and related export projects accelerate upstream development.

Europe Wireline Services Market Trends

Europe's market is defined predominantly by North Sea activity spanning the U.K. Continental Shelf (UKCS), the Norwegian Continental Shelf (NCS), and the Danish and Dutch sectors, as well as onshore and offshore operations in the Netherlands, Germany, and Eastern Europe.

U.K. Wireline Services Market Trends

The U.K. remains Europe's largest wireline market, supported by an extensive inventory of producing fields requiring ongoing intervention and production optimization. The North Sea Transition Deal, signed by the U.K. government and the oil and gas industry, commits to maintaining production while simultaneously meeting net-zero targets, providing policy certainty that sustains wireline investment through the mid-2030s.

France Wireline Services Market Trends

France's direct upstream wireline market is limited, given the country's moratorium on hydraulic fracturing, but French-headquartered oilfield service companies, particularly Schlumberger (now SLB) and TotalEnergies' affiliated services, play important roles as technology developers and global operators with exposure to European wireline revenues.

Asia Pacific Wireline Services Market Trends

Asia Pacific is likely to be the fastest growing, which can be attributed to China/India's offshore fields, Indonesia/Malaysia's deepwater boom, and rapid urbanization spiking energy demand. Shale exploration and capex in new E&P fuel slickline/e-line for logging and interventions.

China Wireline Services Market Trends

China is the dominant country market within the region, driven by NOC-led development of tight gas and coalbed methane (CBM) in the Sichuan, Ordos, and Tarim basins. China National Petroleum Corporation (CNPC) and China Petroleum & Chemical Corporation (Sinopec) are operating thousands of active wireline crews across the country, with COSL serving as the primary integrated wireline service provider.

India Wireline Services Market Trends

India presents one of the fastest-expanding wireline opportunity markets within the region, underpinned by the government's ambitious US$100 billion upstream investment plan through 2025 and ONGC's accelerated development of the KG Basin deepwater fields. India's wireline market is transitioning from predominantly simple slick line operations to more advanced electric line logging and completion services, reflecting the increasing technical complexity of new well designs.

Competitive Landscape

The global wireline services market exhibits a moderately concentrated competitive structure, with the three supermajor oilfield service companies Schlumberger (SLB), Baker Hughes, and Halliburton collectively commanding over 55% of global wireline revenues in 2026. SLB leads the market through its comprehensive OneSubsea and Formation Evaluation product portfolios, its LIVE digital wireline platform, and its unmatched global deployment capability spanning over 120 countries.

Baker Hughes differentiates through its FiberVision distributed acoustic and temperature sensing systems, its advanced perforating systems, and its strong position in deepwater wireline markets in Brazil and the U.S. Gulf of Mexico. Halliburton's EarthStar and WellDynamics platforms anchor its formation evaluation and wireline completion offering, with particular strength in North American unconventional markets.

The broader competitive ecosystem includes Weatherford International, which has rebuilt its wireline capabilities following its 2019 restructuring and is targeting mid-tier operators in the Middle East and Latin America. China Oilfield Services Limited (COSL) serves as the dominant wireline provider across Chinese domestic operations and is expanding internationally across Asia Pacific and Africa.

Key Industry Developments:

- In March 2026, Archer secured a three-year extension with a major Norwegian oil and gas operator for wireline services under a long-term frame agreement. The company continued delivering well services on the Norwegian Continental Shelf after the operator exercised its contract option. Archer stated that the extension sustained its long-running collaboration and ensured uninterrupted field operations.

- In March 2026, Petrobras identified an oil-bearing interval in the Marlim Sul field offshore Brazil after drilling in the Campos Basin. The company confirmed the discovery at well 3-BRSA-1397-RJS, located 113 km offshore in deepwater conditions. Petrobras used wireline logs, gas indicators, and fluid sampling to evaluate the reservoir and validate the presence of hydrocarbons.

Companies Covered in Wireline Services Market

- Schlumberger

- Baker Hughes

- Halliburton

- Weatherford

- China Oilfield Services Limited

- Archer Limited

- Superior Energy Service Inc.

- FMC Technologies

Frequently Asked Questions

The global wireline services market is projected to reach US$12.8 billion in 2026.

Key growth drivers include the surge in global upstream capital expenditure, rising demand for well logging and reservoir evaluation in unconventional plays, the adoption of digital and fiber-optic wireline technologies, and the growing number of aging wells requiring intervention and workover services.

The Wireline services market is poised to witness a CAGR of 4.2% from 2026 to 2033.

High-potential opportunities exist in the deepwater and ultra-deepwater segment, digitalization of wireline operations using AI-driven analytics, expansion of unconventional well logging in Asia Pacific and Latin America, and the growing demand for carbon capture well assessment services tied to energy transition mandates.

Key players include Schlumberger (SLB), Baker Hughes, and Halliburton, while notable challengers include Weatherford, China Oilfield Services Limited (COSL), Archer Limited, and Superior Energy Services.