- Oil & Gas

- Vacuum Gas Oil Market

Vacuum Gas Oil Market Size, Share, and Growth Forecast, 2026 - 2033

Vacuum Gas Oil Market by Product Type (Light Vacuum Gas Oil, Heavy Vacuum Gas Oil, Medium Vacuum Gas Oil), Grade (High Quality, Medium Quality, Low Quality), End-User (Refineries, Chemical Plants, Power Generation, Transportation), and Regional Analysis for 2026 - 2033

Vacuum Gas Oil Market Share and Trends Analysis

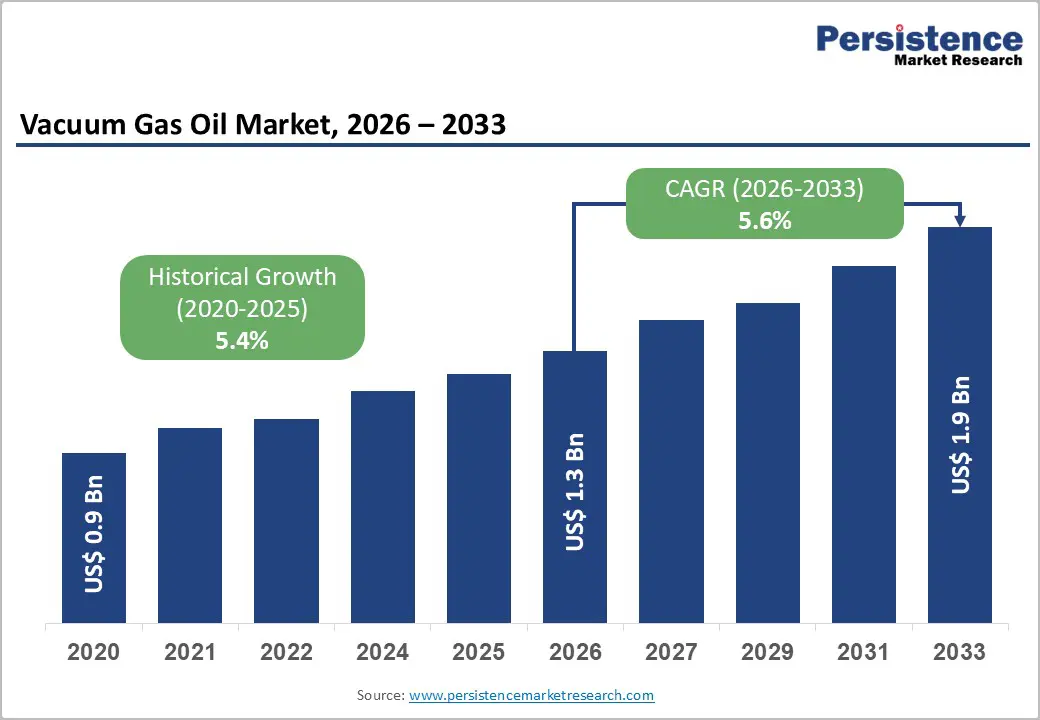

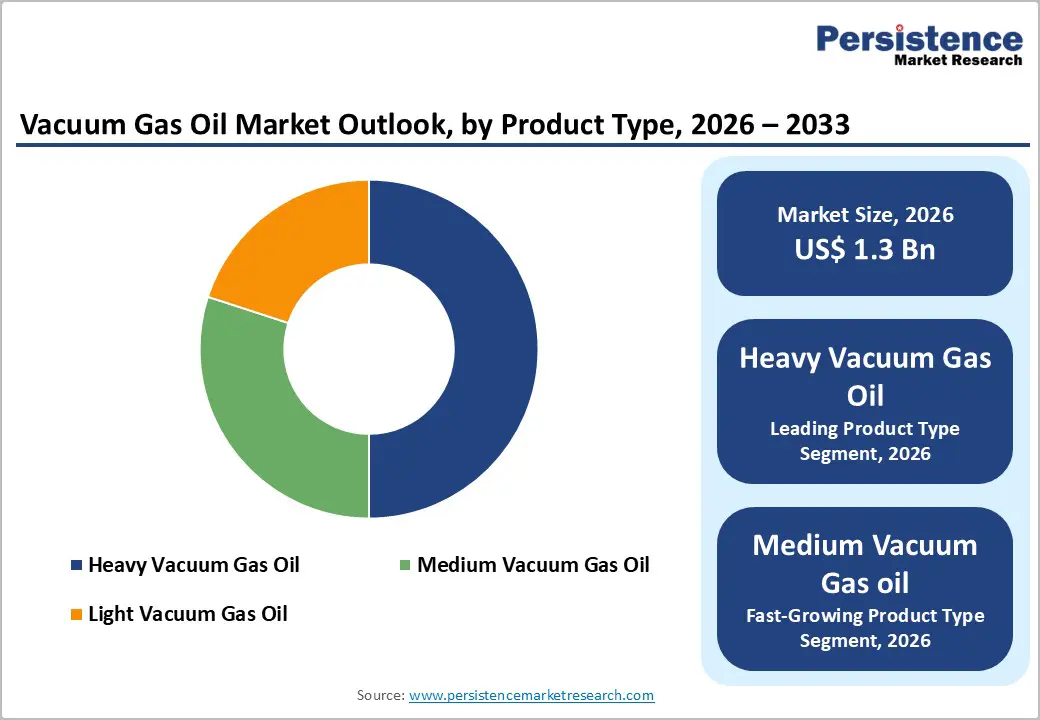

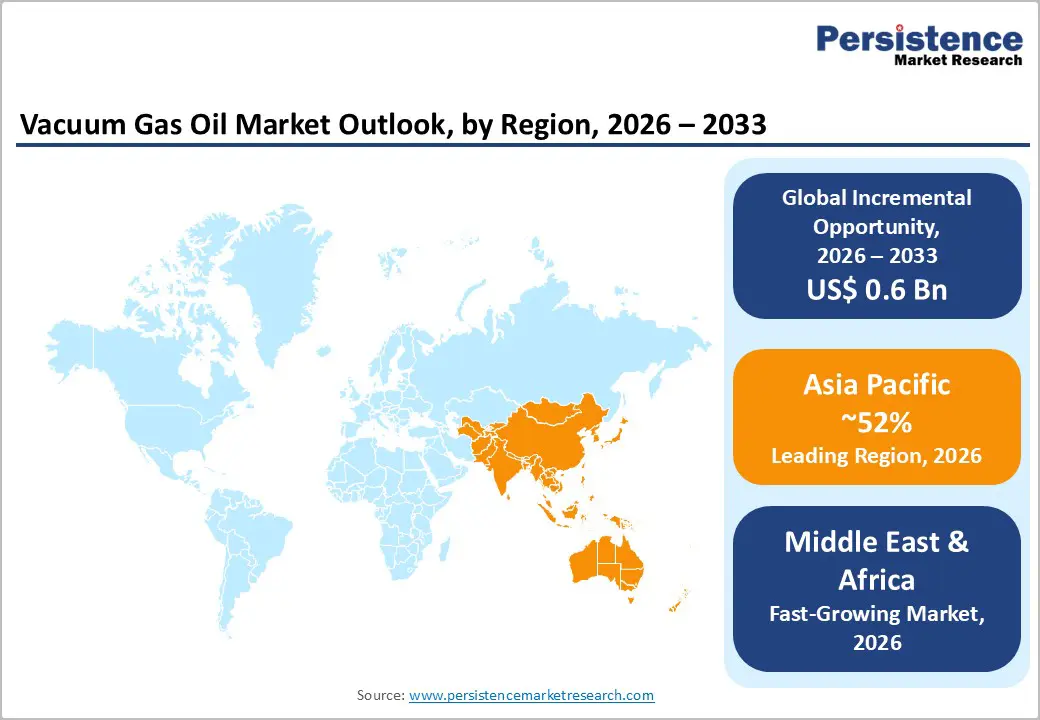

The global vacuum gas oil market size is likely to be valued at US$ 1.3 billion in 2026, and is projected to reach US$ 1.9 billion by 2033, growing at a CAGR of 5.6% during the forecast period 2026−2033. The market demonstrates steady expansion driven by structural demand in refining and downstream petrochemical value chains. Growth is supported by increasing global energy consumption linked to population expansion and industrial activity, which elevates demand for refined petroleum products derived from vacuum gas oil.

Rising awareness of efficient fuel processing and upgrading techniques enhances utilization rates across refineries, leading to consistent consumption patterns. Technological integration in refining operations improves conversion efficiency of heavy fractions into high-value fuels, strengthening demand for vacuum gas oil as a key intermediate feedstock. Expansion of refining capacity in emerging economies contributes to higher throughput requirements, reinforcing supply-demand alignment.

Key Industry Highlights

- Dominant Region: Asia Pacific is projected to hold around 52% of the market share in 2026, supported by capacity expansion and industrial demand.

- Fastest-growing Regional Market: Middle East & Africa is expected to grow the fastest between 2026 and 2033, due to heavy infrastructure investments.

- Leading Product Type: Heavy vacuum gas oil is expected to hold an approximate 50% revenue share in 2026, due to its high utilization in refining processes.

- Fastest-growing Product Type: Medium vacuum gas oil is projected to grow the fastest between 2026 and 2033, driven by flexible processing demand.

| Key Insights | Details |

|---|---|

|

Vacuum Gas Oil Market Size (2026E) |

US$ 1.3 Bn |

|

Market Value Forecast (2033F) |

US$ 1.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Refining Complexity and Demand for Secondary Conversion Feedstock

Refining systems are advancing toward higher complexity configurations, where secondary conversion units such as hydrocrackers and delayed cokers play a central role in upgrading heavier fractions into lighter, high-value outputs. This structural transition elevates the importance of intermediate streams generated after atmospheric and vacuum distillation, positioning them as essential inputs for downstream processing. Expansion of conversion-oriented infrastructure reflects strategic alignment with product optimization and feedstock flexibility. According to the U.S. Energy Information Administration (EIA), United States operable atmospheric crude oil distillation capacity reached approximately 18.4 million barrels per day in 2025, indicating large-scale throughput that requires efficient integration of secondary conversion units.

Feedstock demand patterns are shaped by refining margin optimization and increasing emphasis on petrochemical integration. Complex refining configurations enable processing of heavier and lower-cost crude slates, supporting higher yields of transportation fuels and chemical intermediates through catalytic and hydro processing pathways. Growth in petrochemical consumption drives refiners to maximize output of naphtha, propylene, and aromatics, intensifying reliance on partially processed streams as adaptable inputs. Integration of renewable feedstocks within conventional refining systems further strengthens the role of such intermediates, supporting operational flexibility and compatibility with evolving product specifications and regulatory frameworks across global energy markets.

Expansion of Petrochemical Industry and Feedstock Diversification

Petrochemical demand growth is reshaping refinery configurations toward integrated production models, where intermediate streams from vacuum distillation support generation of olefins, aromatics, and other chemical precursors. These streams act as essential inputs for catalytic cracking and hydro processing units, enabling efficient conversion into high-value petrochemical outputs required across packaging, automotive, electronics, and construction sectors. Increasing focus on chemical yield optimization is directing operational strategies toward maximizing conversion of heavier fractions into feedstocks suitable for downstream chemical manufacturing, strengthening the role of such intermediates within evolving refinery-petrochemical integration frameworks.

Feedstock diversification strategies are advancing in response to crude variability, cost optimization objectives, and shifting product demand structures. Refiners are processing a wider range of crude grades, including heavier and opportunity crudes, which generate intermediate streams suited for flexible upgrading pathways. These streams provide adaptability across multiple conversion processes, supporting production balancing between fuels and petrochemicals. Integration of bio-based and recycled inputs into refining systems further reinforces the importance of versatile intermediates, enabling alignment with sustainability targets, regulatory requirements, and circular economy principles shaping industrial and chemical production ecosystems.

Volatility in Crude Oil Supply and Pricing Dynamics

Fluctuations in crude supply availability and pricing structures are reshaping refinery feedstock strategies, with emphasis on operational flexibility and margin stability. Variations in crude quality, geopolitical disruptions, and shifting trade flows are encouraging refiners to optimize processing of heavier fractions generated during distillation. Intermediate streams provide a relatively stable and controllable input for secondary conversion units, supporting consistent output across changing upstream conditions. This adaptability allows refiners to respond to supply-side uncertainty through improved utilization of existing assets and enhanced conversion efficiency within complex refining configurations.

Pricing volatility is influencing decision-making across refining operations, where feedstock selection directly impacts profitability and product yield optimization. Wider price spreads between light and heavy crude grades are driving increased use of lower-cost inputs that require advanced upgrading processes. Intermediate streams serve as balancing components within refining systems, enabling adjustments in production slates across fuels and petrochemical outputs. Exposure to dynamic pricing environments is reinforcing investment in conversion technologies and process integration, supporting agile responses to margin fluctuations, regulatory pressures, and evolving global energy trade patterns without disrupting operational continuity.

Stringent Environmental Regulations and Energy Transition Pressures

Tightening environmental standards and decarbonization mandates are reshaping refinery operations toward cleaner and more efficient output streams. Regulations governing sulfur content, emissions intensity, and fuel quality are driving expansion of secondary conversion units such as hydrocrackers and desulfurization systems. Intermediate streams from vacuum distillation serve as critical inputs within these processes, enabling removal of impurities and production of low-sulfur fuels aligned with compliance requirements. This shift is reinforcing the importance of controlled and upgradeable feedstocks that support consistent product quality while meeting increasingly stringent regulatory frameworks across global refining systems.

Energy transition pressures are accelerating adoption of alternative feedstocks and low-carbon processing pathways within conventional refining infrastructure. Integration of bio-based inputs, waste-derived oils, and synthetic feedstocks requires adaptable intermediate streams capable of supporting multiple upgrading routes. These streams provide operational flexibility for blending, conversion, and co-processing within evolving refinery configurations. Investments in hydrogen utilization, carbon capture, and process electrification are further increasing reliance on such intermediates, enabling alignment with sustainability targets, emissions reduction strategies, and transformation of fuel and petrochemical production systems under shifting global energy priorities.

Integration of Refinery and Petrochemical Complexes

Convergence of refining and petrochemical operations is reshaping asset utilization strategies, where integrated complexes prioritize conversion of heavier fractions into chemical feedstocks. Intermediate streams from vacuum distillation are routed directly into catalytic cracking and hydro processing units, enabling efficient production of olefins, aromatics, and other high-value intermediates. This structural alignment supports higher yield optimization and reduces dependence on standalone processing units. According to the U.S. EIA, United States refinery utilization rates averaged above 90% during 2024, reflecting sustained operational intensity that reinforces the role of integrated processing systems.

Operational synergies within integrated complexes are enhancing flexibility in feedstock allocation and product slate management. Shared infrastructure, including hydrogen networks and conversion units, enables efficient upgrading of intermediate streams across multiple pathways. This configuration supports rapid adjustment between fuel and chemical outputs in response to demand shifts. Increased focus on petrochemical yield maximization is strengthening reliance on such streams as adaptable inputs within complex processing environments. Capital investment trends are aligning toward integrated platforms that improve margin stability, optimize energy use, and support evolving requirements for cleaner fuels and diversified chemical production.

Technological Advancements in Hydrocracking and Catalytic Processes

Advances in hydrocracking and catalytic technologies are transforming refining performance through higher conversion efficiency and improved product selectivity. Modern catalyst formulations, including enhanced acidity and metal dispersion, enable deeper upgrading of heavier fractions into lighter fuels and petrochemical intermediates. Intermediate streams generated from vacuum distillation serve as essential feed inputs for these advanced units, supporting optimized yield structures and operational stability. Continuous improvements in catalyst life cycles and resistance to contaminants are strengthening processing reliability, allowing refiners to sustain consistent output quality while handling heavier and more complex feedstock compositions within evolving refining configurations.

Catalytic process innovation is expanding operational flexibility across refining systems, enabling efficient processing of diverse crude slates and alternative feedstocks. Developments in reactor design, pressure optimization, and hydrogen management are improving conversion rates and energy efficiency within hydro processing units. Intermediate streams provide adaptable inputs that can be routed across multiple catalytic pathways, supporting production balancing between transportation fuels and petrochemical outputs. Integration of digital control systems and real-time monitoring is enhancing process optimization, enabling precise adjustments in feedstock utilization and product distribution in response to shifting demand patterns and regulatory requirements across global energy markets.

Category-wise Analysis

Product Type Insights

Heavy vacuum gas oil is likely to be the leading segment with approximately 50% revenue share in 2026, due to its critical role in secondary conversion processes within refineries. This segment serves as a primary feedstock for fluid catalytic cracking and hydrocracking units, enabling production of gasoline, diesel, and other high-value fuels. Refinery operators prioritize heavy fractions to maximize output efficiency, leading to consistent demand for this segment. Operational compatibility with advanced refining technologies enhances utilization across diverse processing configurations. Accessibility remains high due to widespread production during crude oil distillation. Provider preference aligns with heavy vacuum gas oil due to its economic contribution in improving refining margins.

Medium vacuum gas oil is expected to witness the fastest growth between 2026 and 2033, with an estimated CAGR exceeding 6%, as refineries seek balanced feedstock compositions for flexible processing. This segment offers an optimal blend of lighter and heavier fractions, enabling efficient conversion into both fuel and petrochemical outputs. Increasing adoption of integrated refining-petrochemical models supports its growth trajectory. Technological advancements improve processing adaptability, enhancing utilization rates across multiple units. Accessibility across diverse crude types ensures consistent supply. Innovation in refining processes supports improved yield efficiency, driving adoption among modern refineries.

End-User Insights

Refineries are foreseen to dominate with nearly 60% of the vacuum gas oil market revenue share in 2026, supported by direct utilization of vacuum gas oil in core processing operations. This segment forms the backbone of demand, as vacuum gas oil serves as an essential intermediate in fuel production. High operational capacity and continuous processing requirements sustain demand levels. Industrial reliability and strict quality standards reinforce demand concentration within refinery operations. Large-scale integration of distillation, hydrocracking, and catalytic cracking units ensures consistent consumption patterns. Strategic investments in upgrading capacity and process optimization further strengthen throughput efficiency. Alignment with fuel quality regulations sustains long-term operational relevance.

Chemical plants are expected to emerge as the fastest-growing segment between 2026 and 2033, with an estimated CAGR of approximately 7%, driven by increasing integration of refining and petrochemical production. Demand for chemical derivatives such as olefins and aromatics supports higher utilization of vacuum gas oil. Material-enabled service delivery through advanced chemical processing technologies enhances conversion efficiency. Cost efficiency and diversification of product portfolios encourage adoption within chemical manufacturing. Expansion of petrochemical infrastructure drives sustained growth. Increasing focus on specialty chemicals and performance materials strengthens demand for flexible feedstock inputs. Technological advancements in catalytic processes support higher yield optimization and improved product consistency across chemical production systems.

Regional Insights

North America Vacuum Gas Oil Market Trends

North America demonstrates a mature yet strategically evolving refining landscape, supported by high-complexity configurations and advanced conversion infrastructure. Extensive deployment of hydrocracking, delayed coking, and fluid catalytic cracking units enables efficient upgrading of heavier fractions into transportation fuels and petrochemical intermediates. Strong integration between refining and chemical production supports consistent utilization of intermediate feedstreams across diverse applications. Presence of large-scale refining hubs in United States and Canada ensures stable throughput, supported by access to both conventional and unconventional crude resources, including shale-derived feedstocks that enhance supply flexibility.

Operational focus is shifting toward efficiency optimization, emissions reduction, and integration of low-carbon technologies within existing refining systems. Investments in catalyst innovation, hydrogen management, and digital process control are improving conversion efficiency and supporting adaptable feedstock utilization. Increasing alignment with petrochemical demand is encouraging refiners to optimize yield structures toward higher-value chemical intermediates. Infrastructure modernization and regulatory compliance requirements are reinforcing adoption of cleaner processing pathways, where intermediate feedstreams play a critical role in enabling desulfurization and upgrading processes. Strong logistics networks and export capabilities further position refining operations as key suppliers within global energy and chemical value chains.

Europe Vacuum Gas Oil Market Trends

Europe demonstrates a mature refining structure characterized by high regulatory intensity and a strong shift toward cleaner fuel production and petrochemical integration. Refining configurations emphasize hydrocracking, desulfurization, and residue upgrading to meet stringent fuel quality and emissions standards. Intermediate feedstreams play a critical role in enabling production of ultra-low sulfur fuels and compliant petrochemical inputs. Countries such as Germany, France, and Italy are focusing on modernization of refining assets, integrating digital process controls and advanced catalysts to improve conversion efficiency and operational precision across complex refining systems.

Energy transition policies are reshaping feedstock utilization patterns, with increasing integration of renewable and circular inputs within existing infrastructure. Co-processing of bio-based feedstocks, waste oils, and synthetic alternatives is driving demand for flexible intermediate streams capable of supporting multiple upgrading pathways. Industrial strategies are prioritizing reduction of carbon intensity through hydrogen utilization, electrification, and carbon capture integration within refining operations. Strong petrochemical demand across automotive, packaging, and specialty chemical sectors is reinforcing the role of adaptable feedstreams. Continuous investment in innovation and sustainability-focused technologies is enabling alignment with regulatory frameworks while maintaining stable output across evolving fuel and chemical production systems.

Asia Pacific Vacuum Gas Oil Market Trends

Asia Pacific is expected to lead with an estimated dominant share of 52% of the vacuum gas oil market share in 2026, supported by concentration of large-scale and highly complex refining systems designed to process diverse crude slates. Extensive deployment of hydrocracking and fluid catalytic cracking units increases dependence on intermediate feedstreams for high conversion efficiency. Strong integration between refining and petrochemical production enables continuous routing into olefin and aromatic value chains. Rapid urbanization and industrial output across China and India are reinforcing throughput requirements and capacity expansion.

Dominance is further supported by cost-efficient refining economics and proximity to high-growth end-use industries. Access to a diversified crude import base enables optimization of feedstock selection, where heavier grades are efficiently upgraded through advanced conversion technologies. Refining operators are prioritizing yield optimization across fuels and petrochemical intermediates, strengthening reliance on adaptable feedstreams. Expansion of export-oriented refining hubs in Singapore and Japan is enhancing trade flows, supported by continuous investments in process digitalization, catalyst innovation, and infrastructure development.

Middle East & Africa Vacuum Gas Oil Market Trends

Middle East & Africa is forecasted to be the fastest-growing market for vacuum gas oil between 2026 and 2033, stimulated by large-scale investments in integrated refining and petrochemical complexes aimed at maximizing value from crude resources. Expansion of conversion-focused infrastructure is increasing utilization of intermediate feedstreams within hydrocracking and catalytic processing units. Countries such as Saudi Arabia and United Arab Emirates (UAE) are accelerating downstream diversification strategies, shifting toward higher-margin chemical production. Access to cost-advantaged crude supply supports competitive refining economics and enables efficient upgrading of heavier fractions into lighter fuels and petrochemical intermediates.

Growth momentum is reinforced by development of export-oriented refining hubs and advanced industrial clusters aligned with long-term economic diversification strategies. Expansion of petrochemical capacity is driving demand for flexible intermediate feedstreams that support production of olefins, aromatics, and specialty chemicals. Infrastructure investments across Nigeria and South Africa are strengthening regional processing capabilities and enhancing domestic value chains. Integration of advanced catalysts, process optimization technologies, and digital monitoring systems is improving conversion efficiency and operational reliability, enabling scalable growth across refining and chemical production environments.

Competitive Landscape

The global vacuum gas oil market exhibits a moderately consolidated structure, with leading players controlling a significant share of global capacity. Major oil and gas companies dominate through vertically integrated operations that combine upstream sourcing, refining, and downstream distribution. ExxonMobil Corporation, Royal Dutch Shell plc, BP plc, Chevron Corporation, and TotalEnergies SE maintain strong positions through extensive refining infrastructure, advanced conversion technologies, and consistent large-scale throughput across global operations.

Competitive positioning is shaped by technological advancement, feedstock flexibility, and geographic diversification across key refining hubs. Leading companies are investing in catalyst innovation, hydrocracking efficiency, and digital process optimization to enhance conversion rates and yield structures. Strategic regional presence supports supply chain resilience and demand responsiveness. Smaller participants focus on niche applications and regional supply, leveraging cost efficiency and operational flexibility within specialized processing segments.

Key Industry Developments

- In March 2026, Croatia advanced refinery modernization plans to eliminate reliance on Russian vacuum gas oil imports, with commissioning of a new residue treatment unit enabling full transition by early 2026.

- In March 2026, a new ATEX-compliant vacuum solution for technical and medical gases was introduced, focusing on enhanced safety, efficiency, and regulatory compliance in hazardous industrial environments.

- In June 2025, Russia increased seaborne fuel oil and vacuum gas oil exports to India and Turkey, driven by lower oil product prices and stronger seasonal demand for energy and shipping fuels.

Companies Covered in Vacuum Gas Oil Market

- ExxonMobil Corporation

- Royal Dutch Shell plc

- BP plc

- Chevron Corporation

- TotalEnergies SE

- Saudi Aramco

- Reliance Industries Limited

- Indian Oil Corporation Limited

- Valero Energy Corporation

- Phillips 66

- PetroChina Company Limited

- Sinopec Limited

Frequently Asked Questions

The global vacuum gas oil market is projected to reach US$ 1.3 billion in 2026.

Rising refining complexity, petrochemical integration, feedstock diversification, and demand for high-value fuel and chemical outputs are driving the market.

The market is poised to witness a CAGR of 5.6% from 2026 to 2033.

Expansion of integrated refinery-petrochemical complexes, adoption of advanced conversion technologies, and growth in emerging industrial markets present key opportunities.

Some of the key market players include ExxonMobil Corporation, Royal Dutch Shell plc, BP plc, Chevron Corporation, TotalEnergies SE, and Saudi Aramco.