- Electrical Equipment & Services

- Wire and Cable Materials Market

Wire and Cable Materials Market Size, Share, and Growth Forecast 2026 - 2033

Wire and Cable Materials Market by Product Type (Conductor Material (Copper, Aluminum, Others), Insulation Material (Polyvinyl Chloride (PVC), Cross-linked Polyethylene (XLPE), Polyethylene (PE), Polypropylene (PP), Others)), Application (Electronic Wire, Power Cable, Flexible & Specialty Cable, Control & Instrumentation Cable, Communication Cable), and Regional Analysis, 2026 - 2033

Wire and Cable Materials Market Size and Trend Analysis

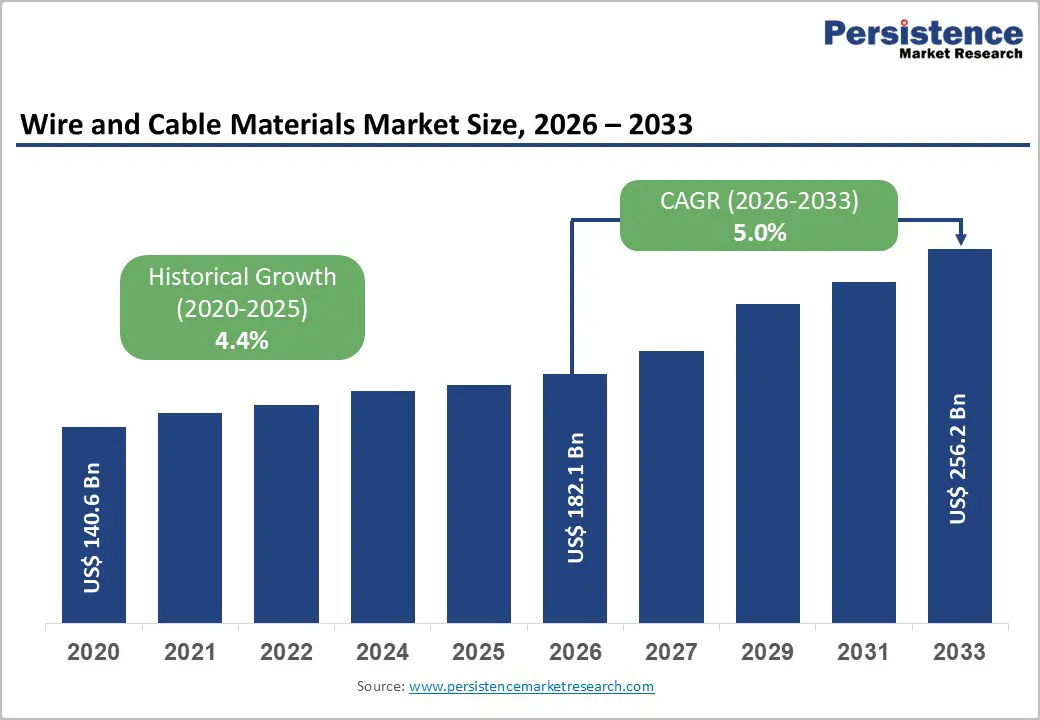

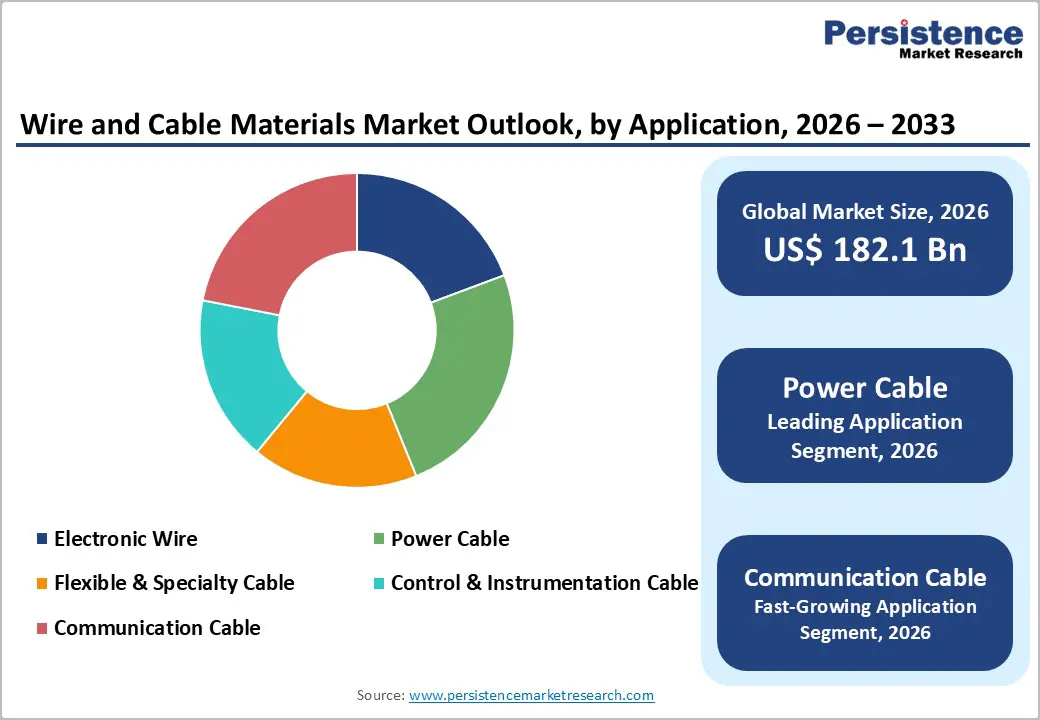

The global wire and cable materials market size is expected to be valued at US$ 182.1 billion in 2026 and projected to reach US$ 256.2 billion by 2033, growing at a CAGR of 5.0% between 2026 and 2033.

Growth is driven by rapid electrification, renewable energy expansion, and smart grid deployments worldwide. Rising electricity demand is accelerating investments in transmission and distribution infrastructure, increasing the need for advanced conductor and insulation materials. Urbanization and expanding construction activities are further boosting demand for wiring solutions. Additionally, the rollout of 5G networks and digital infrastructure is driving demand for high-performance communication cables across developed and emerging economies.

Key Industry Highlights:

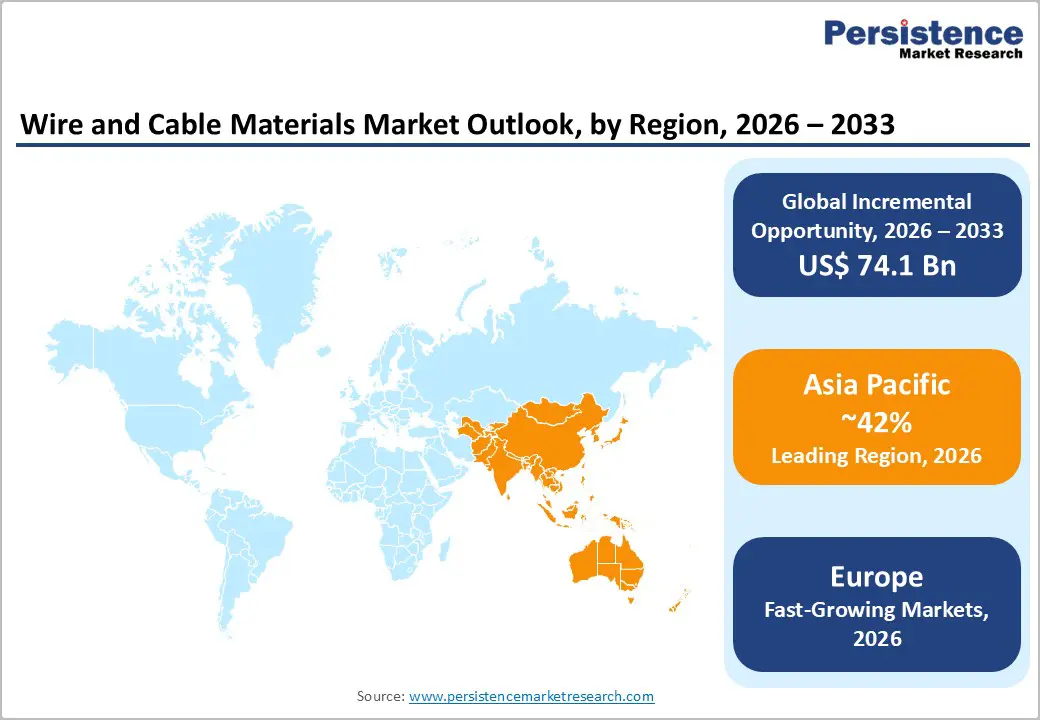

- Leading Region: Asia Pacific leads the wire and cable materials market with a 42% share in 2025, driven by strong manufacturing bases and large-scale infrastructure development.

- Fastest Growing Region: Europe is the fastest-growing region, expanding at a CAGR of 6.5%, supported by renewable energy targets and grid modernization initiatives.

- Leading Application: Power cables dominate the application segment with a 40% share, supported by rising global electrification and transmission infrastructure demand.

- Leading Material: Copper leads the material segment with a 55% share, owing to its superior conductivity and widespread use in power and communication networks.

- Key Opportunity: Growing subsea cable projects present a key opportunity, driven by expanding offshore wind capacity and increasing global investments in cross-border energy connectivity.

| Key Insights | Details |

|---|---|

| Wire and Cable Materials Size (2026E) | US$ 182.1 billion |

| Market Value Forecast (2033F) | US$ 256.2 billion |

| Projected Growth CAGR (2026 - 2033) | 5.0% |

| Historical Market Growth (2020 - 2025) | 4.4% |

Market Dynamics

Drivers - Accelerating Renewable Energy Integration Driving High-Performance Cable Material Demand

The surge in renewable energy projects significantly propels the wire and cable materials market. Solar and wind installations require efficient conductors and advanced insulation to manage fluctuating loads and long-distance transmission. Increasing renewable capacity additions are creating strong demand for reliable cabling systems to ensure stable grid connectivity and minimize transmission losses across expanding energy networks.

Copper remains a preferred material due to its high conductivity, enabling efficient energy transfer. Government initiatives and funding for clean energy infrastructure are further accelerating deployment of advanced cabling systems. As countries continue focusing on decarbonization and grid modernization, the demand for durable and high-performance wire and cable materials is expected to rise steadily.

Rapid Electric Vehicle Expansion Boosting Advanced Wiring Material Needs

The global transition toward electric vehicles is significantly driving demand for specialized wire and cable materials. EVs and charging infrastructure require high-performance insulation materials capable of withstanding elevated temperatures and electrical loads. The increasing adoption of EVs is intensifying the need for efficient, lightweight, and durable cabling solutions across automotive and charging ecosystems.

Materials such as XLPE and aluminum are gaining traction due to their thermal resistance and weight advantages. Expanding EV infrastructure, including fast-charging networks, is further boosting demand for high-voltage cables. Supportive government policies and electrification targets are encouraging investments, positioning wire and cable material suppliers to benefit from the accelerating shift toward electric mobility.

Restraints - Fluctuating Raw Material Prices Impacting Production Costs Stability

Volatility in key raw material prices such as copper and aluminum acts as a significant restraint for the wire and cable materials market. Frequent price fluctuations driven by supply disruptions, geopolitical tensions, and mining constraints increase uncertainty for manufacturers. This instability directly affects procurement strategies and raises overall production costs across the value chain.

Rising costs of insulation materials like PVC and other polymers further compound the challenge due to fluctuations in petrochemical supply. These cost pressures reduce profit margins for manufacturers and limit their ability to offer competitive pricing. As a result, investment decisions may be delayed, ultimately slowing market growth and expansion in both developed and emerging economies.

Stringent Environmental Regulations Limiting Material Usage Flexibility

Increasingly strict environmental regulations on hazardous materials are restricting the use of conventional wire and cable materials. Regulations targeting substances such as lead, phthalates, and halogen-based compounds are forcing manufacturers to shift toward safer alternatives. This transition often requires significant investment in research, compliance, and material substitution processes.

Compliance with environmental standards raises production costs and creates operational complexities, especially for small and mid-sized manufacturers. Additionally, restrictions on widely used materials like PVC can impact scalability in cost-sensitive markets. These regulatory pressures may slow adoption rates and limit material choices, posing challenges to overall market growth.

Opportunities - Advancements in High-Performance Polymers Enabling Efficient Power Transmission

Significant opportunities are emerging in the development of advanced insulation materials such as next-generation XLPE and polyethylene variants. These materials are essential for high-voltage direct current (HVDC) systems, which require superior dielectric strength and thermal performance. As long-distance power transmission expands, the demand for reliable, low-loss insulation solutions is steadily increasing.

Manufacturers investing in advanced polymer technologies can benefit from premium product offerings and improved efficiency outcomes. Ongoing grid modernization and renewable energy integration are accelerating the adoption of such materials. Government initiatives supporting transmission infrastructure upgrades are further strengthening opportunities, positioning high-performance polymers as a key growth area in the wire and cable materials market.

Rising Subsea Cable Projects Driving Demand for Specialized Materials

The expansion of subsea cable projects for offshore wind farms and interconnection networks presents strong growth opportunities. These projects require highly durable materials, including corrosion-resistant conductors and water-resistant insulation, to ensure long-term performance in harsh marine environments. Increasing offshore energy capacity is driving consistent demand for such specialized cable materials.

Growing investments in submarine cable infrastructure are creating long-term opportunities for manufacturers. Large-scale offshore wind projects and cross-border interconnections are boosting demand for advanced cabling solutions. Companies specializing in subsea-grade materials can secure long-term contracts, benefiting from the global transition toward renewable energy and enhanced grid connectivity.

Category-wise Analysis

Product Type Insights

Copper dominates the conductor material segment, accounting for approximately 55% market share in 2025 due to its superior electrical conductivity and efficiency in minimizing transmission losses. Its extensive use in high-reliability applications such as power grids and data centers strengthens its leadership despite higher costs. Additionally, copper’s high recyclability supports sustainability goals, further reinforcing its widespread adoption across infrastructure and telecom sectors.

Insulation materials such as XLPE and advanced polyethylene variants are witnessing rapid growth due to increasing demand for high-performance and heat-resistant solutions. These materials are gaining traction in renewable energy systems, electric vehicles, and high-voltage applications. Continuous innovation and the need for durable, efficient insulation are driving their adoption across modern power and communication infrastructure.

Insulation Material Insights

Polyvinyl Chloride (PVC) leads the insulation material segment with around 45% market share in 2025, driven by its cost-effectiveness, flame-retardant properties, and ease of processing. Its widespread use in residential and low-voltage wiring applications makes it a preferred choice in construction and infrastructure projects. PVC’s versatility and compliance with safety standards further support its dominant position in the market.

Advanced insulation materials such as XLPE and halogen-free compounds are emerging as the fastest-growing segments due to increasing environmental concerns and performance requirements. These materials offer enhanced thermal stability and safety, making them suitable for high-voltage and critical applications. Growing demand for sustainable and high-efficiency solutions is accelerating their adoption globally.

Application Insights

Power cables dominate the application segment, holding approximately 40% market share in 2025, supported by increasing investments in grid modernization and expanding electricity demand. Their critical role in power transmission and distribution infrastructure ensures consistent demand across urban and industrial developments. Rising electrification and infrastructure expansion continue to strengthen the segment’s leading position.

Communication cables and flexible specialty cables are witnessing the fastest growth due to the rapid expansion of digital infrastructure and advanced technologies. Increasing deployment of 5G networks, data centers, and smart systems is driving demand for high-performance materials. The shift toward connected and energy-efficient systems is further accelerating growth across these application areas.

Regional Insights

North America Wire and Cable Materials Market Trends and Insights

North America holds a significant position in the wire and cable materials market, accounting for approximately 25% share in 2025. Growth is driven by strong investments in grid modernization, renewable energy integration, and infrastructure resilience. The U.S. leads the region with substantial funding directed toward upgrading aging transmission networks and enhancing grid reliability, supporting demand for advanced conductor and insulation materials.

Technological innovation and regulatory standards continue to shape the market landscape. Increasing focus on sustainable and recyclable materials is encouraging manufacturers to develop eco-friendly cable solutions. Additionally, expanding data center infrastructure and electrification initiatives are further boosting demand for high-performance wire and cable materials across the region.

Europe Wire and Cable Materials Market Trends and Insights

Europe represents a mature yet steadily growing market, supported by strong regulatory frameworks and energy transition goals. The region is projected to grow at a CAGR of around 6.5% during the forecast period, driven by increasing renewable energy adoption and cross-border grid interconnections. Countries such as Germany, the UK, and France are key contributors to regional demand.

Stringent environmental policies and decarbonization targets are accelerating the shift toward advanced and sustainable cable materials. Investments in offshore wind projects and high-voltage transmission networks are creating consistent demand. Additionally, coordinated efforts to enhance grid efficiency and connectivity are further supporting the growth of wire and cable materials across Europe.

Asia Pacific Wire and Cable Materials Market Trends and Insights

Asia Pacific dominates the global market, accounting for approximately 42% share in 2025, driven by rapid industrialization, urbanization, and large-scale infrastructure development. Major economies such as China, India, and Japan contribute significantly through expanding power generation capacity and strong manufacturing ecosystems, making the region a key hub for wire and cable material demand. The region is also experiencing fast growth supported by government initiatives promoting domestic manufacturing and electrification. Investments in smart grids, renewable energy projects, and electric vehicle infrastructure are accelerating demand for advanced materials. Additionally, rising construction activities and digital infrastructure expansion across emerging economies continue to strengthen market growth in the Asia Pacific.

Competitive Landscape

The wire and cable materials market is moderately consolidated, characterized by the presence of established players leveraging strong manufacturing capabilities and technological expertise. Companies focus on vertical integration strategies, including securing raw material sources and optimizing supply chains to maintain cost efficiency and ensure consistent quality. Continuous investment in research and development is enabling the introduction of advanced and high-performance material solutions.

Key competitive factors include compliance with environmental and safety certifications, along with the ability to offer customized solutions for emerging applications such as electric vehicles and renewable energy systems. Increasing emphasis on sustainability is driving adoption of circular economy practices, including recycling initiatives and eco-friendly material development.

Key Developments:

- In June 2024, Prysmian Group introduced eco-friendly XLPE cable solutions designed for offshore wind applications, focusing on reducing environmental impact. The new development enhances performance while lowering lifecycle emissions, supporting sustainability goals in renewable energy transmission infrastructure.

- In October 2024, Nexans secured a major contract for the France-Spain interconnector project, utilizing advanced copper alloy materials. The project aims to strengthen cross-border electricity transmission capacity while improving efficiency and reliability of high-voltage power networks.

- In March 2025, LS Cable & System expanded its manufacturing facility in the United States to meet rising demand for EV charging cables. The expansion supports growing electrification initiatives and enhances production capacity for high-performance cable solutions.

Companies Covered in Wire and Cable Materials Market

- Prysmian Group

- Nexans

- Sumitomo Electric Industries

- LS Cable & System

- Furukawa Electric

- Fujikura Ltd.

- Belden Inc.

- Southwire Company

- Leoni AG

- NKT A/S

- General Cable Corporation

- Hengtong Group

- Polycab India Limited

- KEI Industries Ltd.

- Finolex Cables Ltd.

Frequently Asked Questions

The global Wire and Cable Materials market is expected to reach US$ 182.1 billion in 2026, driven by electrification and renewables.

Renewable energy integration, with 510 GW added in 2023 per IEA, boosts demand for high-performance conductors and insulators.

Asia Pacific leads with 42% share in 2025, fueled by China's manufacturing and India's infrastructure growth.

Subsea cables for offshore wind, with 100+ projects by 2030 per 4C Offshore, demand specialized materials.

Leading firms include Prysmian Group, Nexans, and LS Cable & System, dominating via innovation and contracts.