- Electrical Equipment & Services

- Shot Blasting Machine Market

Shot Blasting Machine Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Shot Blasting Machine Market by Machine Type (Hanger Type, Roller Conveyor Type, Tumble Type (Tumblast), Table Type / Rotary Table, Cabinet Type, Others (Portable, Spinner Hanger)), Technology (Wheel Blasting, Air Blasting, Wet Blasting), Industry (Automotive, Aerospace, Foundry & Forging, Construction & Infrastructure, Shipbuilding, Rail, Others (Energy, Manufacturing)), and Regional Analysis 2026 - 2033

Shot Blasting Machine Market Trends & Analysis

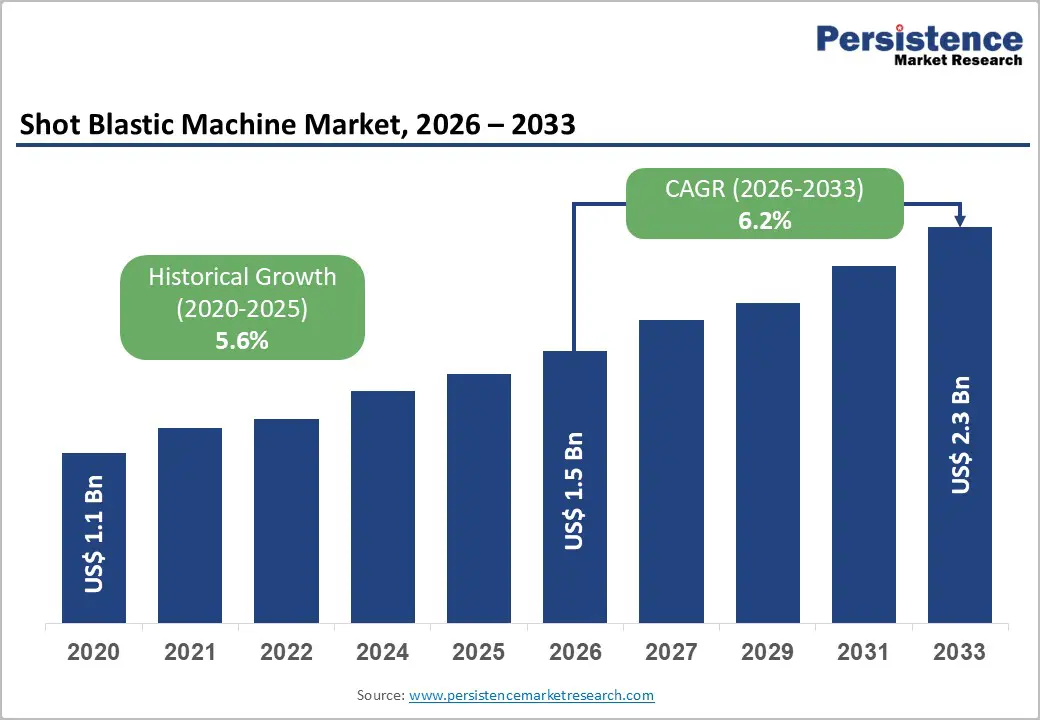

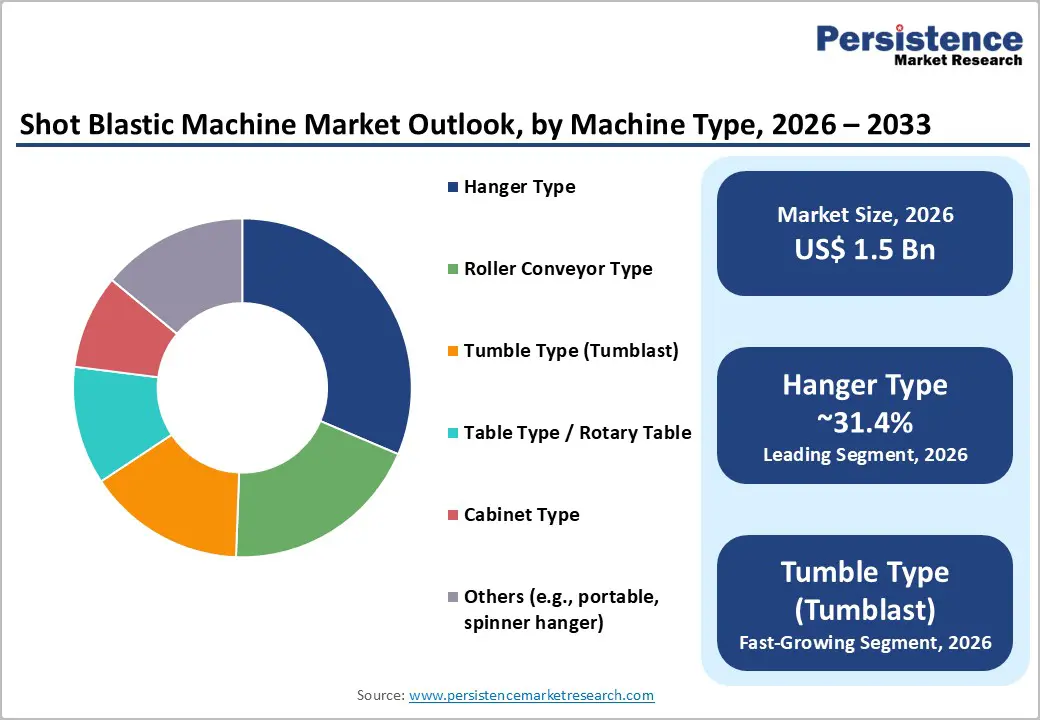

The global shot blasting machine market size is projected at US$ 1.52 billion in 2026 and is projected to reach US$ 2.31 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

The mounting automotive and aerospace production volumes that need a consistent metal surface preparation standard, investments in construction and infrastructure driving structural steel surface treatment demand, and adoption of automated CNC-integrated shot blast systems improving throughput and process repeatability are the primary growth drivers.

Key Industry Highlights:

- Leading Machine Type: Hanger type leads at 31.4% share; Tumble type (Tumblast) grows fastest at 8.4% CAGR, driven by high-volume automotive casting and foundry batch processing expansion across Asia Pacific and India.

- Leading Technology: Wheel blasting leads and grows fastest at 56.2% share and 8.3% CAGR, sustained by throughput efficiency advantages and automation-integrated EV component and wind tower fabrication adoption.

- Leading End-user: Automotive leads at 34.6% share; Aerospace is expected to grow fast, driven by record Boeing and Airbus delivery backlogs and expanding defense aviation MRO shot peening demand globally.

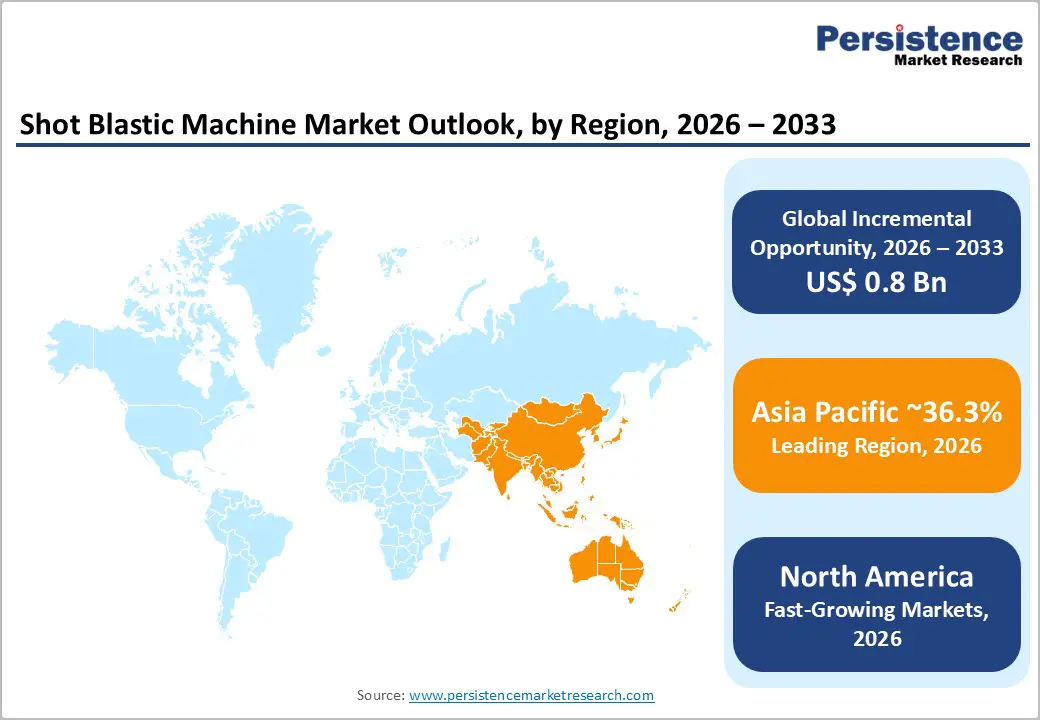

- Regional Performance: Asia Pacific leads and grows fastest at 6.7% CAGR with China at US$ 270 Mn and India at US$ 60 Mn; North America holds 25.6% share with the U.S. at US$ 279.6 Mn in 2026.

- Strategic Developments: Rösler's Smart Blast® 4.0 IoT platform launch (March 2025) and Norican Group's India manufacturing expansion (November 2024) are strengthening automation-integrated machine capabilities and Asia Pacific market penetration.

Market Dynamics Analysis

Drivers - Surging Automotive and Aerospace Production Volumes Demanding Precision Surface Preparation

Global automotive production exceeded 93 million vehicles in 2023 (OICA data), with each vehicle incorporating 200-400 individual metal components requiring shot blast surface preparation for paint adhesion, corrosion resistance coating, and fatigue life enhancement, generating structurally recurring shot blasting machine utilization and replacement procurement across OEM stamping, casting, and forging supply chains.

Electric vehicle platform expansion is intensifying surface preparation requirements further, with EV battery enclosure aluminum die castings, motor housing forgings, and structural battery tray components requiring precision surface treatment specifications exceeding those of conventional ICE vehicle parts.

The global aerospace MRO market, valued at US$ 96 Bn in 2023 (IATA Maintenance Cost Task Force), drives sustained air blasting machine demand for turbine blade, landing gear, and airframe component surface preparation and shot peening applications that improve metal fatigue life by 20-30% in safety-critical aviation components. Boeing's 2024 Commercial Market Outlook, projecting 43,975 new aircraft deliveries over the next 20 years, and Airbus's 42,000-unit 20-year forecast, collectively indicate a multi-decade aerospace surface treatment equipment demand pipeline that directly sustains shot blasting machine procurement across aerospace Tier 1 and MRO facility investment cycles globally.

Global Infrastructure Investment Programs Driving Structural Steel Shot Blast Demand

The World Bank estimates global infrastructure investment requirements at US$ 3.7 trillion annually through 2035 to meet sustainable development goals, with bridges, tunnels, offshore platforms, and industrial facility structural steel fabrication generating mandatory shot blast surface preparation requirements before protective coating application. The U.S. Infrastructure Investment and Jobs Act, allocating US$ 110 Bn to roads and bridges, is driving structural steel fabrication activity, directly expanding the use of roller conveyors and hanger-type shot blast machines across North American steel fabrication facilities.

China's 14th Five-Year Plan infrastructure investment program, allocating approximately CNY 14 trillion across transportation, energy, and urban development through 2025, has sustained domestic steel fabrication shot blast machine procurement, as the world's largest steel producer and consumer drives continuous investment in structural steel surface treatment capacity.

India's National Infrastructure Pipeline, committing INR 111 trillion across 9,142 projects through 2025, and the EU's European Green Deal infrastructure modernization program, are further reinforcing global structural steel surface preparation demand that sustains shot blasting machine procurement across construction, shipbuilding, and rail end-use sectors through 2033.

Restraints - Stringent Environmental and Occupational Health Regulations Constraining Abrasive Blasting Operations

Shot blasting machine operations, particularly open-air and cabinet air blasting processes, generate respirable silica dust, metallic particulate, and spent abrasive waste streams subject to increasingly stringent OSHA (U.S.), EU REACH, and China GB environmental health and safety regulations. OSHA's revised Permissible Exposure Limit for crystalline silica, reduced to 50 μg/m³ in 2016 and now enforced with graduated penalty structures reaching US$ 156,259 per willful violation, compels facility-level engineering controls, dust collection system upgrades, and operator respiratory protection programs that extend machine integration project timelines by 4-12 months per installation across regulated markets globally.

Skilled Operator Shortage and Complex Machine Maintenance Constraining Facility Throughput

Shot blasting machines, particularly automated hanger, roller conveyor, and tumblast configurations that incorporate PLC-controlled blast wheel speed, media flow rate, and conveyor velocity parameters, require trained maintenance engineers for wheel liner replacement, separator calibration, and blast pattern optimization, which are in critically short supply across industrial markets.

The American Welding Society's 2024 Workforce Report identifies a projected shortfall of 360,000 skilled metalworking and surface treatment equipment technicians in the U.S. by 2027. This talent constraint limits machine utilization rates, with industry benchmarks indicating that inadequately maintained shot blast machines operate at 60-70% of rated throughput capacity, directly restricting market volume productivity and new system justification.

Opportunities - Automated and Robotics-Integrated Shot Blasting Systems for Industry 4.0 Manufacturing Environments

Progressive adoption of Industry 4.0 manufacturing architectures, incorporating automated material handling, real-time process monitoring, and MES-integrated production data management, is generating structural demand for next-generation shot blasting machines featuring robotic loading/unloading integration, IoT-enabled blast parameter monitoring, and AI-driven abrasive media consumption optimization.

Rösler Oberflächentechnik's Smart Blast® IoT platform and Wheelabrator's digital process monitoring systems represent commercially deployed automation-integrated shot blast solutions already generating OEM procurement traction across German automotive and aerospace Tier 1 suppliers.

The global industrial automation market is projected to exceed US$ 400 Bn by 2030 (IFR World Robotics Report), with automated surface preparation equipment representing a US$ 2.5-3.5 Bn addressable sub-segment.

For shot blasting machine manufacturers investing in robotic integration interfaces, IoT connectivity, and predictive maintenance software platforms, automation-ready machine configurations command 25-40% price premiums over standard configurations while generating recurring software service revenue, creating a structurally enhanced revenue model per installed unit that broadens addressable buyer segments across lean manufacturing-oriented OEM and Tier 1 automotive and aerospace facility investment programs globally.

Opportunity 2: Expansion into Renewable Energy Sector Component Surface Treatment Applications

Wind turbine tower fabrication, offshore foundation steel structure preparation, and solar mounting structure galvanizing pre-treatment are emerging as high-growth segments for shot blasting machine applications, driven by the accelerating global deployment of renewable energy infrastructure. The International Energy Agency's Renewables 2024 report projects 7,300 GW of new renewable energy capacity additions through 2030, with wind energy steel tower fabrication alone requiring shot-blast surface preparation for structural corrosion-protection coatings across an estimated 1.2 million metric tonnes of fabricated steel annually at full deployment scale.

Each 5 MW onshore wind tower requires approximately 200 tonnes of structural steel, with ISO 8501-1 Sa 2.5 shot-blast surface preparation specification before epoxy coating application, generating shot-blast machine capacity investment at tower fabrication facilities across China, Germany, Denmark, India, and the U.S. The renewable energy sector's shot blasting equipment addressable market is estimated at US$ 0.4-0.6 Bn by 2030, growing at approximately 8-9% CAGR, presenting a structurally underserved greenfield opportunity for roller conveyor and hanger-type shot blast machine suppliers targeting wind tower and offshore steel fabrication facility procurement programs through 2033.

Category-wise Analysis

Machine Type Insights

Hanger Type shot blasting machines lead the machine type segment with a 31.4% market share in 2026. Hanger type machines command segment leadership through their versatile handling capability for large, geometrically complex workpieces, including automotive chassis components, aerospace structural parts, heavy machinery castings, and fabricated steel structures, that cannot be processed efficiently in tumble or roller conveyor configurations. Their overhead suspension system enables 360-degree blast coverage of irregular geometry components without manual repositioning, making them the default specification for automotive OEM stamping and forging shops, aerospace Tier 1 suppliers, and general metal fabrication facilities requiring broad component range compatibility.

Roller Conveyor Type systems serve high-volume flat profile structural steel applications competitively, but Hanger Type's geometry versatility sustains its leading market share.

Tumble Type (Tumblast) is the fastest-growing machine type at 8.4% CAGR through 2033. High-volume small-to-medium casting, forging, and stamping component batch processing requirements in automotive and foundry sectors, combined with Tumblast systems' lower footprint, automated loading compatibility, and media recovery efficiency, are driving adoption across Asia Pacific and Indian subcontinent foundry and forging facility capacity expansion programs.

Technology Insights

Wheel blasting leads the technology segment with a 56.2% market share in 2026. Wheel blasting technology dominates through its decisive operational efficiency advantages over air blasting alternatives, delivering 10-15 times higher abrasive media throughput per unit energy input, enabling continuous high-volume production-line integration in automotive, foundry, and structural steel fabrication environments.

Centrifugal wheel blast systems operating at 1,500-3,000 RPM propel steel shot and grit media at controlled velocities producing consistent Sa 2.5 surface profiles across high-throughput batch and continuous conveyor production lines. Air blasting retains specialty positioning for precision aerospace component shot peening and complex geometry cabinet applications where wheel blast media control is insufficient. Wet blasting serves niche fine-finish applications. Wheel blasting's throughput and energy efficiency sustain its dominant position through 2033.

Wheel blasting is also the fastest-growing technology at 8.3% CAGR through 2033. Automation-integrated wheel blast machine adoption across EV component manufacturing, wind tower fabrication, and expanded foundry production lines, combined with advanced turbine blade design improvements increasing media velocity efficiency, are collectively sustaining wheel blasting's simultaneous share and growth leadership through 2033.

Industry Insights

Automotive leads the Industry segment with a 34.6% share in 2026. Automotive's segment dominance reflects the industry's unmatched metal component volume, with each of the 93+ million vehicles produced annually incorporating cast, forged, and stamped components requiring shot blast surface preparation for paint adhesion, galvanizing pre-treatment, and fatigue life enhancement. EV platform transition is further elevating surface preparation specification requirements for battery housing castings, motor components, and structural elements, increasing per-vehicle shot blast processing intensity versus ICE platform benchmarks. Aerospace, Foundry & Forging, and Construction sectors serve significant complementary roles but remain volume-subordinate to automotive's production scale through 2033.

Aerospace is the fastest-growing Industry at a notable growth trajectory. Record commercial aircraft delivery backlogs at Boeing and Airbus, expanding defense aviation procurement programs, and MRO activity growth sustaining precision air blasting and shot peening demand for turbine blade, landing gear, and airframe component fatigue life enhancement applications are collectively driving aerospace segment shot blasting machine procurement acceleration.

Regional Market Insights

North America Shot Blasting Machine Market Trends

North America holds a 25.6% share of the global shot blasting machine Market in 2025, underpinned by the U.S.'s large automotive OEM and Tier 1 supplier shot blast machine installed base, aerospace MRO surface preparation demand, and structural steel fabrication activity supported by Infrastructure Investment and Jobs Act project execution.

OSHA silica exposure compliance requirements are driving dust collection system-integrated shot blast machine upgrade investment across existing industrial facilities, adding a regulatory compliance procurement layer to standard capacity expansion demand across automotive and construction sector operators.

U.S. Shot Blasting Machine Market: Automotive & Aerospace OEM Investment Leadership

The U.S. market is estimated at US$ 279.6 Mn in 2026, driven by Ford, GM, and Stellantis automotive casting and forging shot blast facility investment, Boeing and Lockheed Martin aerospace precision air blasting procurement, and structural steel fabricator roller conveyor machine upgrades. Canada contributes automotive parts manufacturing shot blast demand in Ontario and Quebec, and oil sands equipment heavy steel fabrication surface preparation investment through 2033.

Europe Shot Blasting Machine Market Trends

Europe is growing at a prominent 6.0% CAGR through 2033, driven by automotive OEM quality standard mandates across the German, French, and Czech vehicle manufacturing ecosystems, EU EN ISO 8501 surface cleanliness standard enforcement at structural steel fabricators, and Rösler and Wheelabrator's European manufacturing and innovation leadership sustaining premium automated machine adoption across aerospace and industrial end users.

Germany Shot Blasting Machine Market: Precision Engineering Standards & Supply Chain Investment

Germany's market is estimated at US$ 83.2 Mn in 2026, anchored by BMW, Mercedes-Benz, and Volkswagen foundry and forging supplier shot blast equipment investment, Rösler Oberflächentechnik's Untermerzbach-headquartered global product development, and DIN EN ISO 8501-1 compliance enforcement across steel fabrication facilities. The U.K. contributes Rolls-Royce and BAE Systems aerospace precision air blasting procurement. France sustains Safran and Airbus Tier 1 supplier surface treatment investment, while Spain contributes automotive sector foundry shot blast capacity expansion.

Asia Pacific Shot Blasting Machine Market Trends

Asia Pacific is the fastest-growing market at 6.7% CAGR through 2033, driven by China's dominant steel production and automotive manufacturing base generating continuous shot blast machine procurement, India's rapidly expanding automotive and foundry sector investment, and Japan's precision manufacturing standards sustaining high-specification automated machine adoption at Tier 1 automotive and aerospace suppliers.

China & India Shot Blasting Machine Market: Manufacturing and Foundry Expansion Leadership

China's market is estimated at US$ 270 Mn in 2026, driven by SAIC, FAW, and BYD automotive casting supplier shot blast facility investment, structural steel fabrication for infrastructure projects, and Shandong Kaitai Group's domestic machine manufacturing scale. India's market at US$ 60 Mn is growing through Tata Motors, Mahindra, and Bharat Forge foundry shot blast capacity expansion. Japan sustains Toyota, Honda, and Denso precision wheel blast and shot peening equipment investment through 2033.

Competitive Landscape

The global shot blasting machine market is moderately consolidated, with Norican Group (Wheelabrator + DISA), Rösler Oberflächentechnik, and Sintokogio collectively commanding an estimated 40-45% global revenue share, differentiating through automated system integration capabilities, IoT-enabled process monitoring platforms, and broad machine type portfolio coverage across all end-use industries. Aftermarket abrasive media and spare parts service contracts are emerging as recurring revenue business model differentiators for market leaders.

Automation-integrated machine platform development, IoT smart blast monitoring system deployment, geographic expansion into India and Southeast Asian foundry markets, and strategic aftermarket service capability investment define the dominant competitive strategic themes shaping the global shot blasting machine market through 2033.

Strategic Developments

- In March 2025, Rösler Oberflächentechnik launched its next-generation Smart Blast® 4.0 IoT platform, integrating AI-driven abrasive media consumption analytics, real-time blast wheel wear monitoring, and MES connectivity across hanger and tumblast machine series, targeting automotive and aerospace Tier 1 customers pursuing Industry 4.0 surface treatment process digitalization.

- In November 2024, Norican Group expanded its Wheelabrator manufacturing and service center in Bangalore, India, adding assembly capacity for roller conveyor and hanger-type shot blast machines targeting India's rapidly growing automotive casting, forging, and infrastructure steel fabrication procurement market through 2033.

- In July 2024, Blastman Robotics entered a technology partnership with Konecranes to co-develop a robotic shot blasting and lifting system integration platform, enabling automated workpiece handling and blast processing for heavy structural steel and shipbuilding fabrication facilities across Nordic and Baltic European industrial markets.

- In April 2024, Sintokogio Ltd. launched a new automated tumblast machine series for EV battery housing and motor component surface preparation, incorporating variable blast intensity PLC control, closed-loop media classification, and dust collection integration, targeting Japan and China EV component manufacturing facility procurement programs.

- In January 2024, AGTOS GmbH expanded its product portfolio with a low-energy, high-efficiency wheel blast turbine design, reducing per-unit energy consumption by 22% versus previous generation turbines, targeting European automotive and foundry facilities seeking EU Energy Efficiency Directive compliance cost reduction in shot blast operations.

Shot Blasting Machine Market Report - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 1.1 Bn |

| Current Market Value (2026) | US$ 1.5 Bn |

| Projected Market Value (2033) | US$ 2.3 Bn |

| CAGR (2026 - 2033) | 6.2% |

| Leading Region | Asia Pacific |

| Dominant Industry | Automotive - 34.6% |

| Top-ranking Technology | Wheel Blasting - 56.2% |

| Incremental Opportunity | US$ 794.5 Mn |

Companies Covered in Shot Blasting Machine Market

- Norican Group

- Rösler Oberflächentechnik GmbH

- Sintokogio Ltd.

- AGTOS GmbH

- Shandong Kaitai Group Co. Ltd.

- Qingdao Qinggong Machinery Co. Ltd.

- Goff Inc.

- Blastman Robotics Ltd.

- Guyson International Ltd.

- Airblast B.V.

- Kaltenbach Group

- C.M. Surface Treatment S.p.A.

- Blastclean Systems Pvt. Ltd.

- STEM d.o.o.

- Gränges AB

Frequently Asked Questions

The shot blasting machine market is valued at US$ 1.5 Bn in 2026, projected to reach US$ 2.3 Bn by 2033.

Rising automotive and aerospace production volumes demanding precision surface preparation standards and global infrastructure investment driving structural steel shot blast demand are the primary growth drivers.

The shot blasting machine market is projected to grow at a CAGR of 6.2% from 2026 to 2033.

Automation and robotics-integrated Industry 4.0 shot blast system adoption and renewable energy wind tower steel fabrication surface preparation equipment demand represent the most actionable near-term growth opportunities.

Norican Group (Wheelabrator), Rösler Oberflächentechnik, Sintokogio, AGTOS GmbH, Shandong Kaitai Group, Goff Inc., Blastman Robotics, Guyson International, Airblast B.V., and Blastclean Systems are the leading global participants.