ID: PMRREP17992| 185 Pages | 9 Dec 2025 | Format: PDF, Excel, PPT* | Packaging

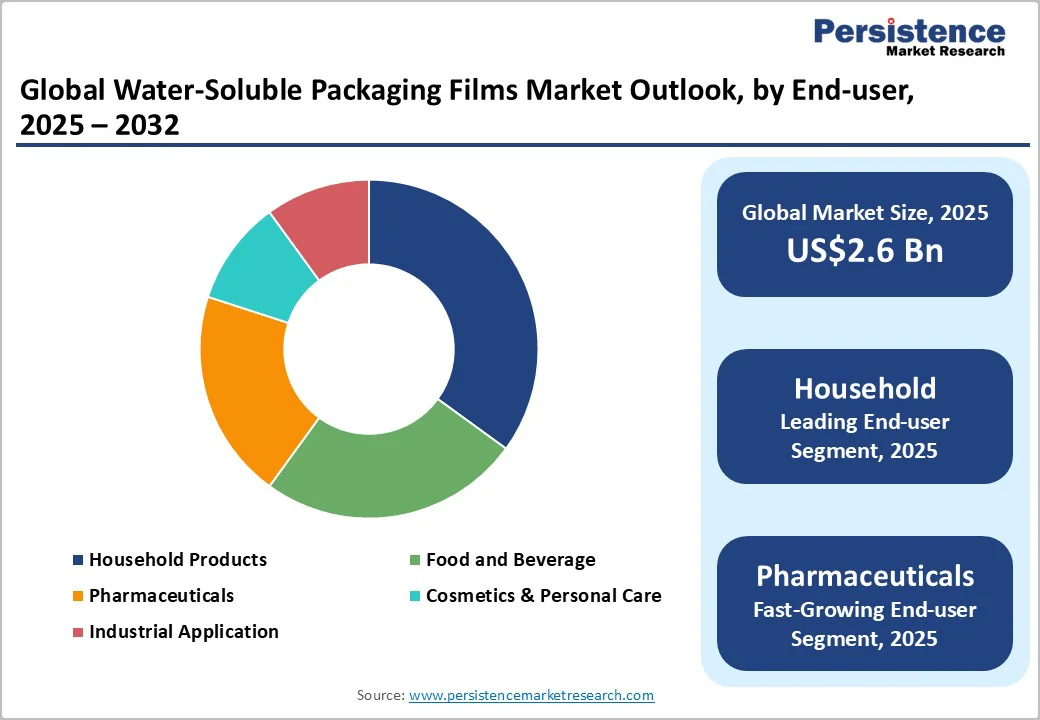

The global water soluble packaging films market size is likely to be valued US$2.6 Billion in 2025 and is expected to reach US$4.3 Billion by 2032, growing at a CAGR of 7.5% during the forecast period from 2025 to 2032, driven by the increasing prevalence of eco-friendly packaging solutions, rising demand for single-use dissolvable films in detergents, and advancements in biodegradable materials.

Rising demand for sustainable and convenient packaging, especially in household products, is driving the adoption of water-soluble films. Innovations in PVA and starch-based polymers cater to dissolvable and compostable preferences, with strong uptake in pharmaceuticals to reduce plastic waste.

| Key Insights | Details |

|---|---|

| Water Soluble Packaging Films Market Size (2025E) | US$2.6 Bn |

| Market Value Forecast (2032F) | US$4.3 Bn |

| Projected Growth (CAGR 2025 to 2032) | 7.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 7.3% |

The increasing prevalence of eco-friendly packaging solutions globally is a primary driver of the water soluble packaging films market. Manufacturers and policymakers place greater emphasis on reducing plastic waste, and dissolvable films have emerged as a practical and environmentally conscious alternative.

These films naturally eliminate the need for traditional plastics by fully dissolving in water, reducing landfill accumulation, and lowering the environmental footprint associated with packaging disposal. Their ability to support waste-free consumption aligns well with modern sustainability goals across households, industries, and institutional sectors.

Single-use dissolvable films are gaining rapid traction as they offer convenience, hygiene, and precise dosing qualities that are essential in applications such as detergents, household cleaners, agrochemicals, and healthcare products. By eliminating direct handling of potentially hazardous substances and ensuring accurate product usage, these films contribute to both safety and operational efficiency. Growing urbanization and busier lifestyles further enhance the appeal of unit-dose, pre-measured formats.

The high costs associated with production and precise solubility control of water-soluble packaging films pose a significant restraint on market growth. Producing high-quality dissolvable films requires specialized raw materials, precise formulation processes, and advanced equipment capable of maintaining uniform thickness, strength, and dissolution consistency.

These requirements increase operational expenses compared to conventional plastic film production. Maintaining strict environmental conditions, such as controlled humidity and temperature during manufacturing and storage, also adds further complexity and cost.

Solubility control is another cost-intensive aspect. Creating films that dissolve reliably at specific temperatures or under certain conditions demands extensive testing, fine-tuning of polymer blends, and the use of modified additives.

Ensuring consistent performance across various applications, such as detergents, agrochemicals, or pharmaceuticals, requires ongoing R&D investments and rigorous quality standards. Any variability in solubility can lead to functional failures, resulting in product waste and financial loss.

Advancements in bio-based polymers and smart dissolvable films are transforming the future of water-soluble packaging by combining environmental responsibility with enhanced functionality. New generations of bio-based polymers derived from plant starches, cellulose, and naturally sourced polyesters are increasingly replacing petroleum-based materials, offering improved biodegradability and reduced carbon impact.

These polymers are being engineered for higher tensile strength, better barrier properties, and more reliable solubility across varying temperatures, making them suitable for both consumer and industrial applications.

Smart dissolvable films are emerging as a major innovation area. These films are designed to dissolve only under specific conditions, such as controlled temperature, pH levels, or moisture exposure, allowing precise release of active ingredients.

This is particularly beneficial for detergents, agrochemicals, pharmaceuticals, and specialty chemicals, where accuracy and safety are critical. Smart films can incorporate indicators, embedded micro-encapsulation, or time-release mechanisms that improve product performance and user convenience.

Polyvinyl Alcohol (PVA) dominates the market, accounting for 60% of the share in 2025. Its dominance is driven by excellent solubility, film strength, and versatility, making it preferred for pods. PVA films, such as those from Cortec Corporation, provide rapid dissolution, ensuring convenience. Its performance and approvals make it preferred for manufacturers.

Starch-based Polymers represent the fastest-growing segment, driven by natural sourcing and increasing adoption in food. Starch offers biodegradability, appealing to the green packaging segment. Focus on modified starch innovation accelerates adoption in Europe and Asia Pacific.

Single-use packaging leads the market, holding a 70% share in 2025, driven by strong demand for unit-dose convenience in detergents and household cleaning. Its easy handling, precise dosing, and hygiene benefits make it highly preferred across consumer and industrial applications. As users prioritize safety and waste reduction, single-use soluble packaging continues to dominate adoption.

Multi-use packaging is the fastest-growing segment, propelled by rising interest in reusable and long-lasting packaging solutions across industrial applications. Its combination of durability and controlled solubility offers both functionality and reduced waste. As industries seek cost-efficient, sustainable formats that support repeated handling and safe dissolution, multi-use packaging continues to gain rapid traction.

Biodegradable films dominate the market, contributing 50% of the revenue in 2025, due to rising eco-compliance requirements and strong regulatory support. Their ability to naturally decompose makes them a preferred alternative to traditional plastics. As industries prioritize sustainability and waste reduction, biodegradable films continue to lead with widespread adoption across packaging applications.

Heat sealing films are the fastest-growing segment, driven by rising demand for secure, tamper-proof packaging across pharmaceuticals and high-value products. Their strong sealing performance ensures product integrity, prevents leakage, and maintains safety during transport. As industries prioritize durability and contamination-free packaging, heat sealing films continue to see rapid adoption and expanding applications.

Household products dominate the market, with a 40% share in 2025, driven largely by the widespread use of detergent pods and other unit-dose cleaning formats. Their convenience, safety, and ease of handling make water-soluble packaging highly preferred in daily home-care routines. Growing consumer demand for efficient, low-waste solutions continues to strengthen this segment’s leadership.

Pharmaceuticals are the fastest-growing, driven by rising demand for unit-dose medications and the expanding use of dissolvable films in agrochemical applications. Water-soluble packaging enables precise dosing, improves handling safety, and reduces contamination risks. Its efficiency, combined with compliance benefits, is accelerating adoption across medical, agricultural, and industrial use cases.

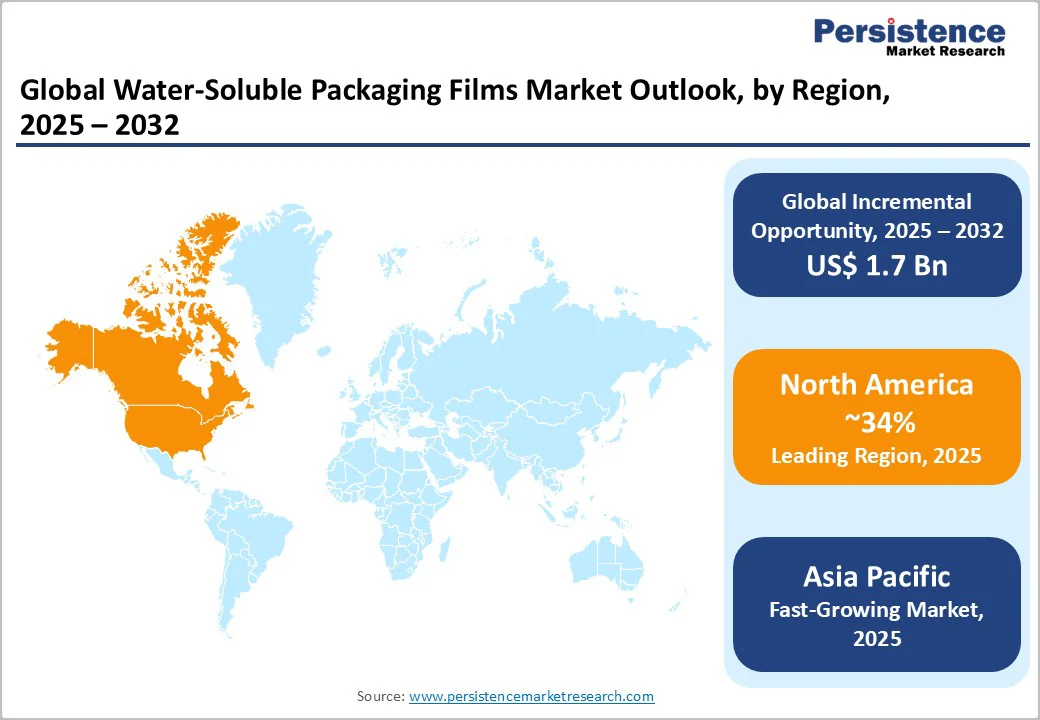

North America accounts for a 34% share in 2025, driven by rising sustainability commitments, increasing regulatory pressure, and a growing preference for environmentally responsible packaging. The region has seen a significant shift toward reducing traditional plastic waste, prompting manufacturers across detergents, household cleaning, agrochemicals, and pharmaceuticals to adopt dissolvable, unit-dose packaging formats.

Water-soluble films, especially those made from PVA, are gaining traction due to their ability to dissolve safely, minimize residue, and support precise dosing qualities that align with both consumer convenience and industrial safety needs.

Technological advancements are also shaping the market, with producers developing films that dissolve effectively in cold water while maintaining higher tensile strength and durability for storage and handling. Growth in e-commerce and packaged household essentials further increases demand for compact, waste-reducing soluble pouches and pods.

Regulatory initiatives encouraging biodegradable materials and extended producer responsibility are motivating brands to transition toward water-soluble solutions.

Europe holds a 22% share in 2025, driven by strict environmental regulations and rising consumer demand for eco-friendly alternatives. The EU’s Single-Use Plastics Directive and broader circular-economy goals are compelling industries to shift from conventional plastics to biodegradable, water-soluble solutions.

This trend is particularly strong in the detergent and household cleaning sectors, where unit-dose pods and dissolvable pouches are widely adopted for convenience and waste reduction.

Pharmaceutical applications are also increasing, with water-soluble films now used in unit-dose packaging, dissolvable drug delivery formats, and precision dosing. Significant R&D investments across the region are focused on enhancing film strength, improving cold-water solubility, and boosting barrier performance, especially for PVA-based materials.

Industrial and agrochemical sectors are adopting dissolvable sachets to improve safety and reduce handling risks. Consumer interest in sustainable packaging continues to rise, encouraging brands to replace traditional plastics with greener solutions.

Asia Pacific is the fastest-growing region, driven by rising environmental awareness, expanding manufacturing activity, and strong government initiatives aimed at reducing conventional plastic waste. Countries such as China, India, Japan, and South Korea are increasingly adopting biodegradable and water-soluble alternatives as part of large-scale sustainability commitments.

The region’s booming FMCG, detergent, agrochemical, and pharmaceutical industries are accelerating the shift toward unit-dose, eco-friendly packaging formats, creating substantial demand for high-performance water-soluble films.

Local manufacturers are expanding production capabilities and introducing cost-effective solutions tailored to regional needs, strengthening competitiveness against global players. Technological advancements such as improved cold-water solubility, enhanced film strength, and bio-based polymer development are further supporting market penetration.

E-commerce growth also contributes significantly, as unit-dose detergent pods, soluble pouches, and dissolvable sachets become more popular for convenience and waste reduction.

The global water soluble packaging films market is highly competitive, with major players such as Kuraray Co., Ltd. and Sekisui Chemical Co., Ltd. leading in North America and Europe through strong R&D, broad distribution, and consistent innovation. Strict sustainability regulations in these regions further strengthen their position.

In Asia Pacific, companies such as Arrow GreenTech Ltd. are gaining traction with cost-effective, locally tailored solutions. Rapid industrial growth, plastic-reduction initiatives, and rising consumer eco-awareness are accelerating adoption. Increasing focus on bio-based polymers, improved solubility technologies, and strategic partnerships is intensifying competition as manufacturers expand capacity and adapt to evolving regulatory demands.

The global water soluble packaging films market is projected to reach US$2.6 Billion in 2025.

The rising prevalence of eco-friendly packaging solutions and demand for single-use dissolvable films are the key drivers.

The water soluble packaging films market is poised to witness a CAGR of 7.5% from 2025 to 2032.

The key opportunities include advancements in bio-based polymers and smart dissolvable films.

The key players include Kuraray Co., Ltd., Sekisui Chemicals Co., Ltd., Aicello Corporation, Cortec Corporation, and Arrow GreenTech Ltd.

| Report Attribute | Details |

|---|---|

| Historical Data/Actuals | 2019 - 2024 |

| Forecast Period | 2025 - 2032 |

| Market Analysis | Value: US$ Bn |

| Geographical Coverage |

|

| Segmental Coverage |

|

| Competitive Analysis |

|

| Report Highlights |

|

By Material Type

By Type of Usage

By Functionality

By End-user

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author