- Automotive Components & Materials

- Vehicle Control Unit Market

Vehicle Control Unit Market Size, Share, and Growth Forecast 2026 - 2033

Vehicle Control Unit Market by Propulsion (BEV, HEV, PHEV), Component (Hardware, Software, Aluminum, Titanium), Voltage (12/24 V, 36/48 V), Capacity (16-Bit, 32-Bit, 64-Bit), and Regional Analysis for 2026 - 2033

Vehicle Control Unit Market Size and Trend Analysis

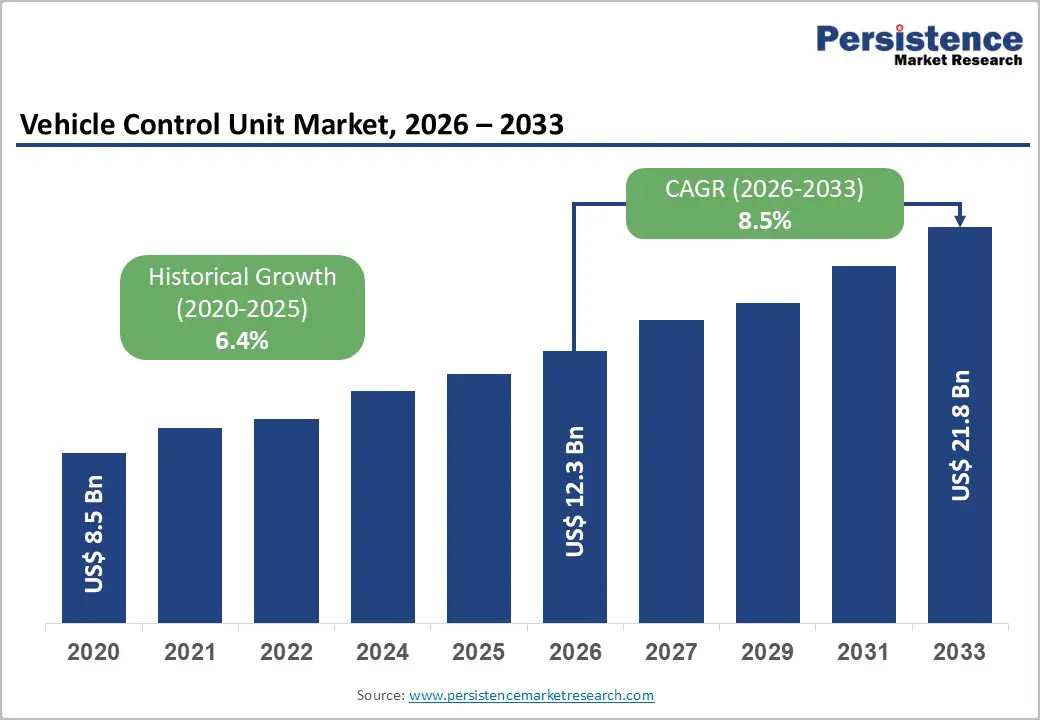

The global vehicle control unit (VCU) market size is valued at US$ 12.3 Bn in 2026 and is projected to reach US$ 21.8 Bn by 2033, growing at a CAGR of 8.5% between 2026 and 2033. This strong growth trajectory is primarily driven by the accelerating global transition to electric and hybrid vehicles, which require sophisticated VCUs to manage battery systems, electric motors, regenerative braking, and real-time multi-domain communication.

According to the International Energy Agency (IEA), global electric car sales topped 17 million units in 2024, surpassing a 20% share of total new car sales worldwide for the first time, a milestone that directly amplifies demand for advanced VCU solutions.

Key Market Highlights

- Leading Region: North America leads the global vehicle control unit market with approximately 39% revenue share in 2026, supported by strong U.S. EV policy incentives, EPA emissions mandates, and established Tier 1 supplier presence, including Bosch and Continental AG.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, led by China's over 11 million EV sales in 2024 and supportive government trade-in incentives, alongside India's FAME and PLI schemes stimulating domestic EV manufacturing and VCU adoption.

- Dominant Segment: The BEV propulsion segment dominates with approximately 48% share in 2026, driven by the highest VCU complexity requirements and rapidly scaling global production volumes from OEMs, including Tesla and Volkswagen Group.

- Fastest-Growing Segment: The 64-Bit capacity segment is the fastest growing, propelled by the computational demands of Level 3+ autonomous driving, centralized vehicle domain architectures, and the deployment of AI-enabled predictive analytics within next-generation VCU platforms.

- Key Market Opportunity: The proliferation of 36/48V architectures in hybrid and full EV platforms, combined with the global commercial vehicle electrification wave, presents a high-value opportunity for VCU suppliers offering scalable, high-voltage-compatible, safety-certified control solutions across passenger and fleet segments.

| Key Insights | Details |

|---|---|

| Vehicle Control Unit Market Size (2026E) | US$ 12.3 Bn |

| Market Value Forecast (2033F) | US$ 21.8 Bn |

| Projected Growth CAGR (2026 - 2033) | 8.5% |

| Historical Market Growth (2020 - 2025) | 6.4% CAGR |

DRO Analysis

Market Growth Drivers

Rapid Electrification of Global Vehicle Fleets

The single most powerful growth driver for the vehicle control unit market is the global acceleration of electric vehicle adoption. The IEA's Global EV Outlook 2025 confirms that global electric car sales surpassed 17 million units in 2024, a year-on-year increase of over 25%, with China alone accounting for over 11 million units. In the first quarter of 2025, EV sales rose by a further 35% year-on-year across all major markets.

Unlike conventional ICE vehicles, BEVs, PHEVs, and HEVs rely on VCUs to coordinate battery management systems (BMS), electric motor control, regenerative braking, and powertrain torque distribution in real time. As OEMs such as Volkswagen Group (which delivered 744,800 all-electric vehicles in 2024) and Tesla (which delivered over 1.78 million vehicles globally in 2024) scale production, the systemic demand for sophisticated, multi-domain VCUs grows correspondingly, making electrification the market's primary long-term catalyst.

Integration of ADAS, Autonomous Driving, and Software-Defined Vehicle Platforms

The rapid integration of Advanced Driver Assistance Systems (ADAS) and the broader transition to software-defined vehicle (SDV) architectures are significantly expanding the functional scope and, in turn, the market value of Vehicle Control Units. ADAS technologies such as lane-keeping assist, automatic emergency braking, and adaptive cruise control require VCUs to process real-time data from multiple sensor arrays with millisecond latency.

The global ADAS market was valued at approximately US$ 42.9 Bn in 2024, growing at a CAGR of 17.8%. SDV architectures further demand VCUs with OTA update capabilities and cloud connectivity, enabling continuous software improvement post-sale. In January 2026, NXP Semiconductors unveiled the S32N7 super-integration processor series at CES 2026, with Robert Bosch GmbH being the first to deploy it in its next-generation vehicle integration platform, a direct testament to the deepening synergy between semiconductor innovation and VCU advancement.

Market Restraints

High Development and Implementation Costs

The development of advanced VCU, particularly those supporting 64-bit processing, functional safety compliance (ISO 26262), cybersecurity standards (UNECE WP.29 / ISO 21434), and multi-domain integration, entails substantial R&D expenditure and prolonged validation cycles. These costs are amplified by the need for bespoke hardware designs for different vehicle platforms across OEM programs.

For smaller Tier-2 suppliers and emerging EV start-ups, particularly in price-sensitive markets, the high capital requirements for VCU development and qualification create significant barriers to entry, limit competitive participation, and slow the pace of broad market adoption across lower-margin vehicle segments.

Growing Cybersecurity Vulnerabilities in Connected Vehicles

As VCU increasingly serves as a central computing hub, managing critical vehicle functions via V2X communication, cloud connectivity, and OTA update channels, it becomes a high-value target for cyberattacks. The UNECE WP.29 regulation, now mandatory across the EU, Japan, and South Korea, requires OEMs to implement comprehensive cybersecurity management systems for all connected vehicle systems.

Compliance imposes high ongoing costs, and any security breach could expose manufacturers to recalls, regulatory penalties, and reputational damage. This cybersecurity imperative adds complexity to VCU architecture design and extends development timelines, constraining near-term growth particularly for suppliers lacking dedicated automotive cybersecurity expertise.

Market Opportunities

BEV Adoption and 48V Architecture Proliferation Across Vehicle Segments

The accelerating transition to Battery Electric Vehicles (BEVs) and the growing adoption of 36/48V mild-hybrid architectures represent a substantial opportunity for VCU suppliers. Higher voltage systems supported by modern power electronics improve energy efficiency, enable more powerful ancillary systems, and are essential for managing regenerative braking and advanced thermal management in EVs.

According to the IEA, global EV sales are projected to surpass 20 million units in 2025. This volume surge directly drives demand for higher-capability VCUs with 48V compatibility. In April 2024, NXP Semiconductors and ZF Friedrichshafen AG announced a collaboration on next-generation SiC-based traction inverter solutions for 800V EV architectures, highlighting the commercial momentum behind high-voltage vehicular electronics and the expanding opportunity for VCU manufacturers to deliver compatible, scalable control solutions.

Expansion of Autonomous and Commercial Vehicle Electrification

The electrification of commercial vehicle fleets, including buses, trucks, and logistics vans, is creating a high-growth parallel opportunity for industrial-grade VCU manufacturers. The global electric commercial vehicle market was valued at approximately US$ 59.23 Bn in 2024 and is expected to reach US$ 80.69 Bn by 2025.

Commercial applications require VCU capabilities to manage heavy load cycles, fleet telematics, and real-time route optimization under demanding duty conditions. Rivian delivered its initial fleet of 10,000 electric delivery vans to Amazon by early 2024, while Ford sold 12,610 E-Transit vans in the same year. Simultaneously, the emergence of Level 3+ autonomous vehicles requiring domain-centralized VCUs with AI-driven perception and decision-making capabilities is poised to unlock premium-value, high-margin VCU platforms for leading semiconductor and automotive electronics suppliers through the forecast period.

Category-wise Analysis

Propulsion Insights

Within the propulsion category, the Battery Electric Vehicle (BEV) segment holds the dominant market share, accounting for approximately 48% of the Vehicle Control Unit market in 2026. BEVs require the most complex and high-performance VCU configurations to manage fully electric powertrains including battery state estimation, regenerative braking coordination, thermal management, and multi-motor torque vectoring without any ICE fallback. This makes BEV-grade VCUs the highest-value and most feature-rich units in the market.

Tesla's delivery of over 1.78 million vehicles in 2024 and China's monthly BEV sales exceeding conventional car sales since July 2024 underscore the accelerating production volumes driving BEV VCU demand. The BEV segment is further supported by growing government mandates phasing out ICE vehicles across the EU, U.K., and multiple U.S. states, ensuring sustained segment leadership through 2033.

Component Insights

The Hardware segment leads the component category in the Vehicle Control Unit market, commanding approximately 62% of total market share in 2026. Hardware encompassing microcontrollers, microprocessors, memory units, I/O interfaces, and power management components forms the physical foundation on which all VCU functionality is built.

Automotive-grade microcontrollers from companies such as Infineon Technologies, NXP Semiconductors, and STMicroelectronics remain indispensable for meeting the functional safety requirements of ISO 26262 ASIL-D classification. While the software segment is growing rapidly, driven by OTA updates and SDV architectures, hardware continues to dominate due to high per-unit ASPs, the critical role of specialized silicon in high-voltage applications, and the ongoing semiconductor investment cycle, including Bosch's planned expansion of its Reutlingen clean room to 44,000 square meters by 2025.

Voltage Insights

The 12/24V segment leads the voltage category, holding an estimated share of approximately 58% of the Vehicle Control Unit market in 2026. This dominance reflects the massive installed base of conventional passenger and light commercial vehicles globally, where 12/24V electrical architectures remain the standard for powering basic control functions, body electronics, lighting, and infotainment systems.

While the 36/48V segment is the faster-growing category, driven by the proliferation of mild-hybrid systems and full EV platforms requiring higher power management capability, the sheer volume of existing 12/24V vehicle production across ICE and entry-level hybrid segments maintains the lower-voltage tier's market leadership. The transition to higher-voltage architectures, however, is expected to progressively erode this share gap over the forecast horizon as electrification deepens.

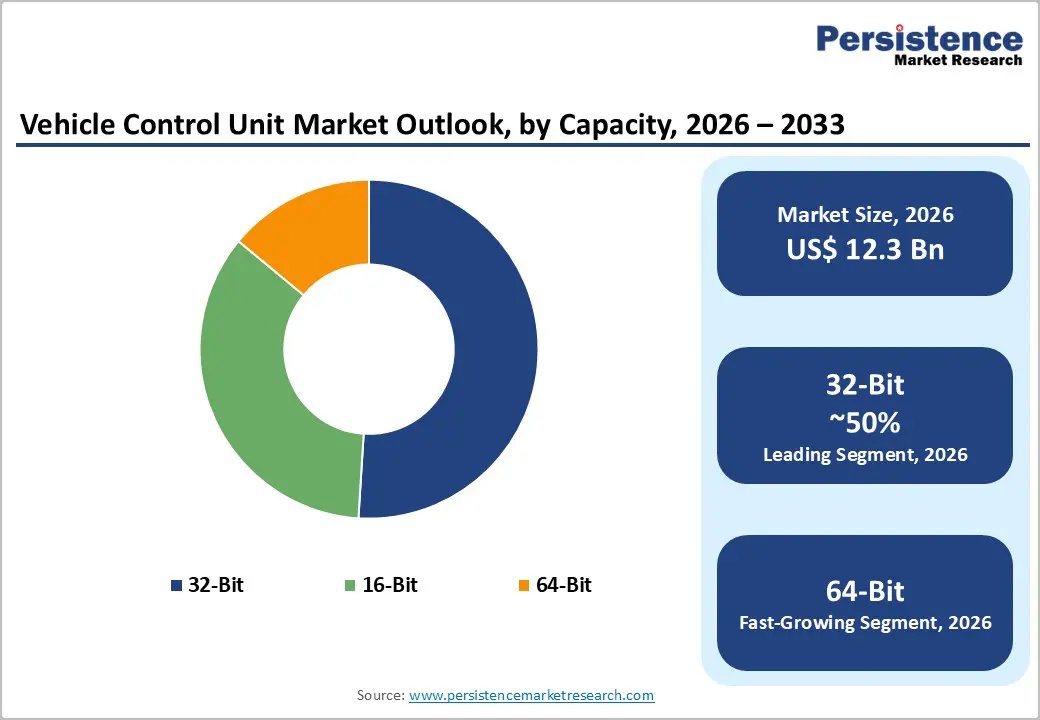

Capacity Insights

The 32-Bit segment holds the leading share in the capacity category, accounting for approximately 51% of the Vehicle Control Unit market in 2026. 32-bit microcontrollers offer the optimal balance between processing power, memory bandwidth, power efficiency, and cost for the majority of automotive VCU applications, including powertrain management, ADAS domain control, and body electronics.

Industry-standard automotive microcontroller families, such as NXP's S32 platform and Infineon's AURIX TC3xx series, are purpose-built 32-bit solutions widely adopted by Tier 1 suppliers and OEMs worldwide. The emerging 64-bit segment is the fastest-growing, propelled by the computational demands of Level 3+ autonomous driving and centralized vehicle compute architectures, but 32-bit will continue to dominate high-volume, cost-optimized applications across the forecast period.

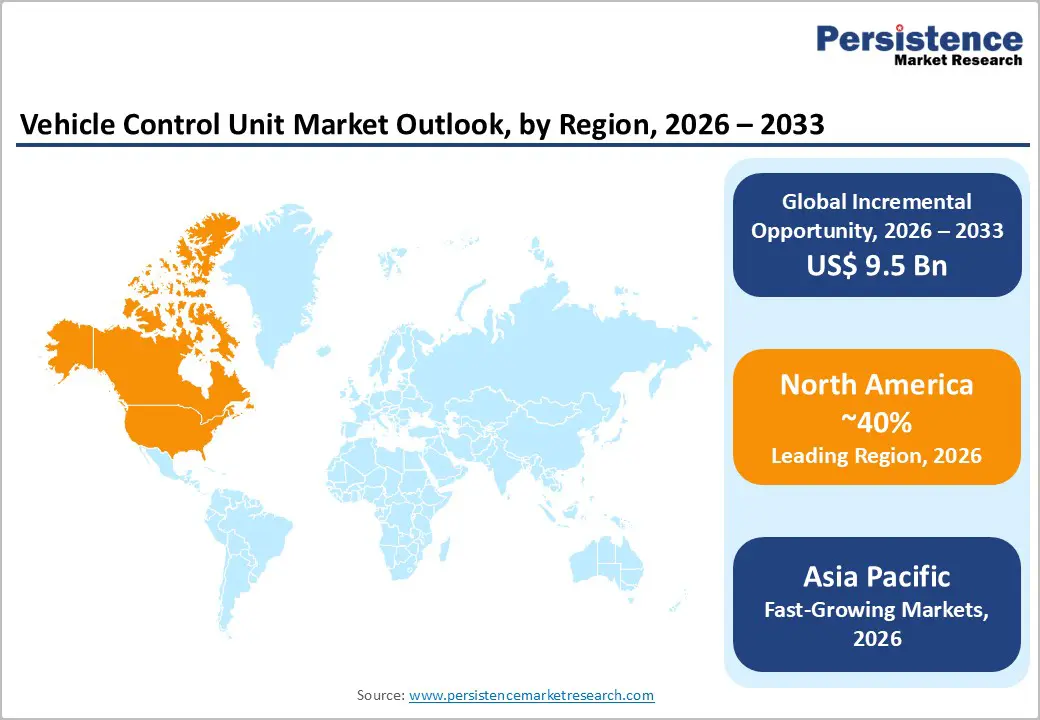

Regional Analysis

North America

North America is the leading region in the global Vehicle Control Unit market, accounting for an estimated revenue share of approximately 40% in 2026. The United States is the primary growth engine, driven by robust federal incentives under the Inflation Reduction Act (IRA), which offers up to US$ 7,500 in clean vehicle tax credits per purchase. The U.S. EPA's Multi-Pollutant Emissions Standards for model years 2027 and beyond are projected to push electric vehicle sales to approximately 70% of total light-duty sales by 2032, creating sustained long-term demand for advanced VCUs.

The U.S. Department of Energy allocated US$ 2 Bn for the Auto Conversion Grant program, with US$ 50 million awarded in August 2024 to help suppliers retool for EV production. Robert Bosch GmbH reported Mobility sector sales of US$ 10.7 Bn in North America in 2024 and is investing US$ 1.9 Bn in its Roseville, California semiconductor facility, with clean room expansion in Reutlingen planned to 44,000 sq. meters by 2025 investments that directly underpin regional VCU supply security.

Asia Pacific

Asia Pacific is the fastest growing region in the global Vehicle Control Unit market, driven by its unparalleled EV production volumes, government policy support, and rapidly expanding automotive electronics manufacturing ecosystem. China is the decisive force: over 11 million electric cars were sold in the country in 2024, with monthly BEV sales surpassing conventional cars since July 2024.

Japan houses major Tier 1 VCU developers including Denso Corporation, while India's EV market is scaling rapidly, supported by the FAME II and Production Linked Incentive (PLI) schemes. In June 2024, NXP Semiconductors and Vanguard International Semiconductor Corp. announced a joint-venture semiconductor wafer fab in Singapore, targeting automotive-grade mixed-signal and power management products reinforcing the region's expanding role as a global VCU semiconductor supply hub.

Europe

Europe represents a significant and regulatory-driven market for VCUs, underpinned by the EU's CO2 Standards mandating automakers to achieve a 55% reduction in fleet emissions by 2030 and a full transition to zero-emission vehicles by 2035. Germany remains Europe's largest automotive manufacturing hub, home to Continental AG, Robert Bosch GmbH, and ZF Friedrichshafen AG three of the world's premier VCU developers. The U.K., France, and Spain are also active EV growth markets, with Europe-wide EV sales projected to reach a 25% share in 2025 according to the IEA.

The UNECE WP.29 cybersecurity regulation mandatory across the EU since July 2024 is compelling OEMs and Tier 1 suppliers to redesign VCU architectures with embedded ISO/SAE 21434-compliant cybersecurity layers, creating additional engineering and validation investment. In October 2024, Cavitec selected Vetaphone corona treatment systems for its laminating machines for technical textiles used in automotive applications exemplifying Europe's continued investment across the automotive supply chain that sustains VCU demand.

Competitive Landscape

The global vehicle control unit market exhibits a moderately consolidated competitive structure, with the top seven players, including Robert Bosch GmbH, Continental AG, Denso, ZF Friedrichshafen AG, Infineon Technologies, STMicroelectronics, and NXP Semiconductors, collectively holding approximately 40% of the global market share.

Leading companies differentiate through modular, scalable VCU platforms that support multiple vehicle architectures, semiconductor vertical integration, and deep OEM co-development programs. Key strategies include investment in SDV-ready computing platforms, ADAS domain fusion, SiC power electronics, and OTA-capable software stacks.

Key Market Developments

- In January 2026, NXP Semiconductors unveiled the S32N7 super-integration processor at CES 2026, with Robert Bosch GmbH as the first to deploy ECU samples, targeting next-generation software-defined vehicle compute architectures.

- In February 2025, BMW announced that it would launch its proprietary "Heart of Joy" control unit in the upcoming Neue Klasse electric vehicles, which would be a significant advancement in integrated vehicle dynamics and efficiency.

- The Heart of Joy is a cutting-edge central computer that consolidates control of the drivetrain, braking, charging, energy recuperation, and steering systems.

Companies Covered in Vehicle Control Unit Market

- ASI Robots

- Continental AG

- Delphi Technologies

- Denso Corporation

- Dorleco

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Robert Bosch GmbH

- STMicroelectronics N.V.

- ZF Friedrichshafen AG

- Texas Instruments Incorporated

- Mitsubishi Electric Corporation

- Keihin Corporation

- Rimac Technology

- HiRain Technologies Co., Ltd.

- Embitel (by CARIAD Group)

- Hyundai Mobis

Frequently Asked Questions

The global Vehicle Control Unit market is valued at US$ 12.3 Bn in 2026 and is projected to reach US$ 21.8 Bn by 2033, expanding at a CAGR of 8.5% over the 2026-2033 forecast period.

The primary driver is the accelerating global EV adoption with the IEA reporting over 17 million EV sales in 2024 (more than 20% of global car sales) which requires sophisticated VCUs for battery management, powertrain control, and regenerative braking. Integration of ADAS and software-defined vehicle architectures further amplifies per-unit VCU value.

The BEV (Battery Electric Vehicle) segment leads the propulsion category with approximately 48% market share in 2026. BEVs demand the most complex VCU configurations, managing fully electric powertrains without ICE fallback. Accelerating global BEV production by OEMs such as Tesla and the Volkswagen Group reinforces this segment's dominant position.

North America leads the market with approximately 40% revenue share in 2026. The U.S. drives regional dominance through the Inflation Reduction Act's EV tax credits, EPA emissions mandates projecting 70% EV sales by 2032, US$ 2 Bn in DoE Auto Conversion Grants, and the presence of leading Tier 1 suppliers such as Robert Bosch GmbH and Continental AG.

The leading companies include Robert Bosch GmbH, Continental AG, NXP Semiconductors N.V., Denso Corporation, ZF Friedrichshafen AG, Infineon Technologies AG, STMicroelectronics N.V., Delphi Technologies, and ASI Robots.