- Automotive Components & Materials

- Green Tires Market

Green Tires Market Size, Share, and Growth Forecast, 2026 - 2033

Green Tires Market by Vehicle Type (Passenger Cars, Light Commercial Vehicles, Others), Sales Channel (OEM, Aftermarket, Others), Application, and Regional Analysis for 2026 - 2033

Green Tires Market Size and Trends Analysis

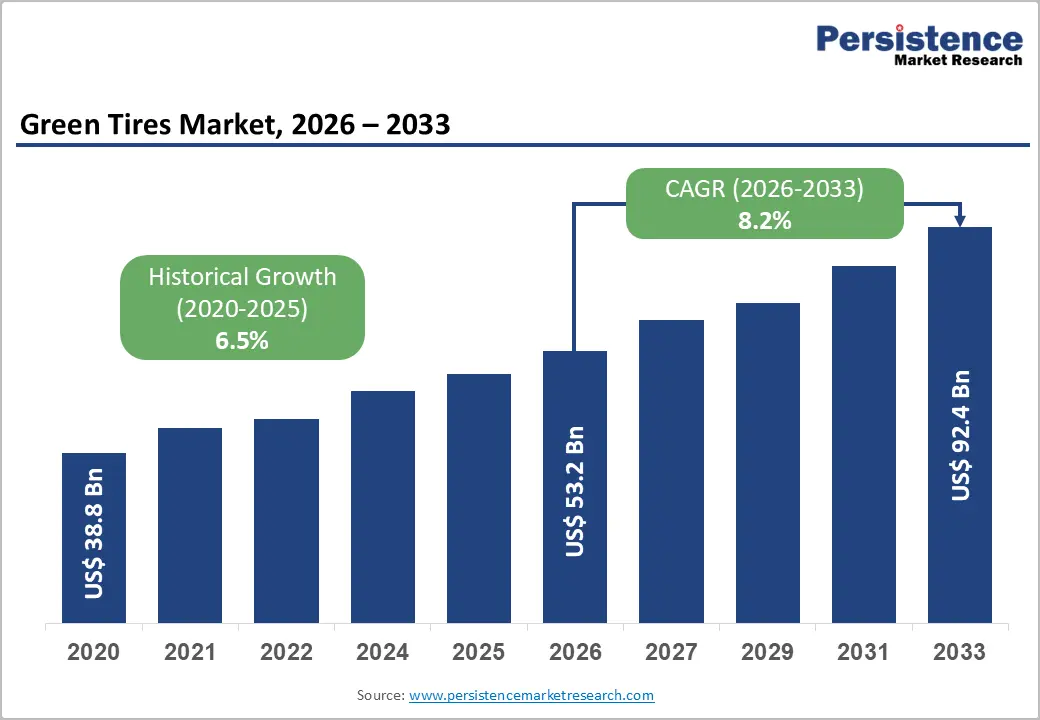

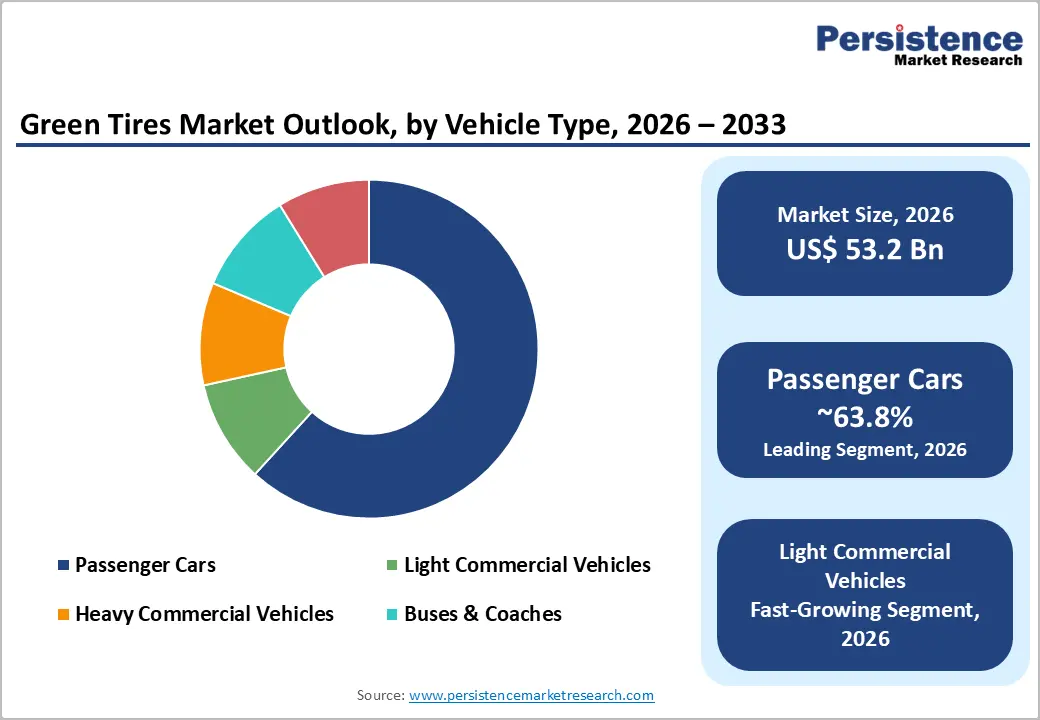

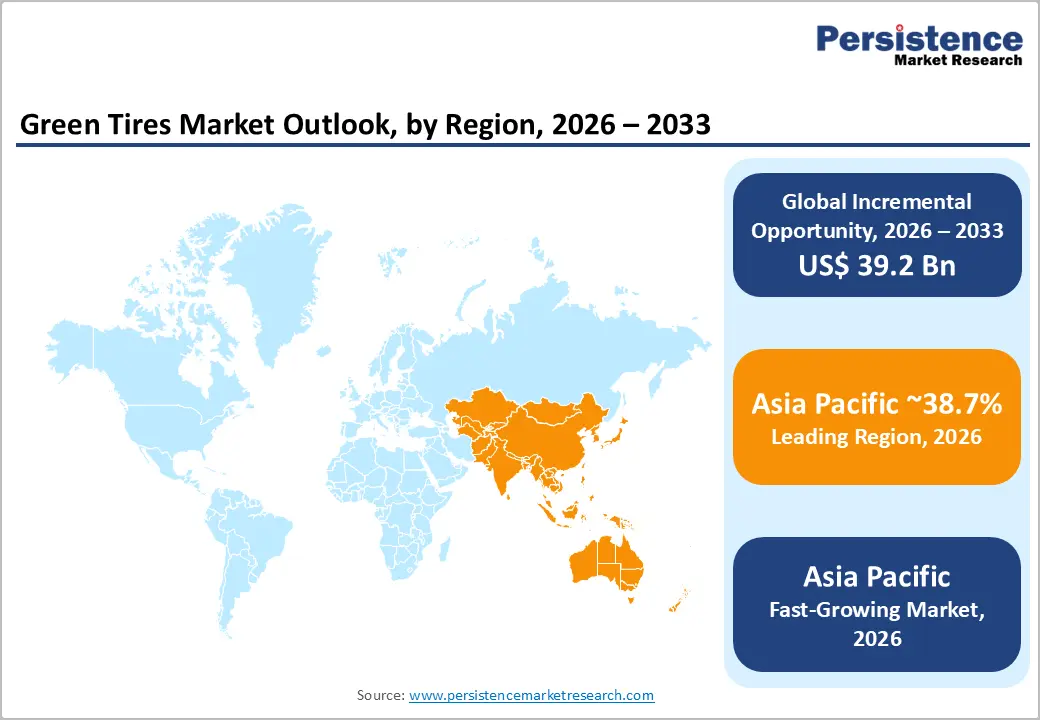

The global green tires market size is likely to be valued at US$53.2 billion in 2026 and is expected to reach US$92.4 billion by 2033, growing at a CAGR of 8.2% between 2026 and 2033, driven by rising EV adoption, stricter fuel-efficiency regulations, and increasing demand for sustainable mobility solutions.

Green tires are evolving from a niche offering to a mainstream requirement, with buyers prioritizing low rolling resistance, durability, wet grip, and eco-friendly materials. Demand is particularly strong in passenger vehicles and light commercial transport, where tire efficiency directly impacts fuel consumption, EV range, and emissions compliance.

Key Industry Highlights:

- Leading Region: Asia Pacific is projected to account for approximately 38.7% of market share in 2026, driven by high vehicle production, strong EV adoption, and cost-efficient manufacturing ecosystems across China, India, and Japan.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, driven by rapid urbanization, expanding automotive demand, and greater alignment with global fuel-efficiency and sustainability standards.

- Investment Plans: Industry investments are primarily focused on EV-specific tire development, sustainable materials (bio-based and recycled content), and low-rolling-resistance technologies, with major players allocating capital toward R&D, advanced manufacturing, and OEM partnerships to strengthen long-term competitiveness.

- Dominant Vehicle Type: Passenger cars are expected to dominate, with 63.8% market share in 2026, driven by their large global vehicle base, high replacement frequency, and increasing integration of green tire technologies across both ICE and electric vehicles.

- Leading Sales Channel: OEMs are estimated to account for approximately 67.1% of the market, as automakers increasingly adopt green tires to meet regulatory requirements, improve fuel efficiency, and optimize EV performance.

DRO Analysis

Driver Analysis - Stringent Regulatory Frameworks Driving Adoption

Regulatory pressure is transforming sustainability from a differentiator into a mandatory product requirement. Tire labeling systems in major markets evaluate products based on rolling resistance, wet grip, and external noise, ensuring transparency and accountability. Updated regulatory frameworks have reduced performance classifications, effectively pushing manufacturers toward higher efficiency standards.

In parallel, environmental compliance programs in commercial transport emphasize fuel efficiency and emissions reduction, particularly for heavy-duty vehicles. These regulatory systems directly influence procurement decisions, especially among OEMs and fleet operators, who now prioritize certified, high-efficiency tires. As a result, manufacturers are compelled to invest in advanced materials, testing capabilities, and certification processes. The broader market impact includes faster adoption cycles, reduced product commoditization, and stronger alignment between sustainability goals and purchasing behavior.

Rapid Growth of Electric Vehicles (EVs)

The accelerating adoption of electric vehicles is a critical growth driver for green tires. EV sales surpassed 17 million units in 2024, with projections indicating continued expansion beyond 20 million units annually. EVs require specialized tires due to their heavier weight, instant torque, and range sensitivity. Low rolling resistance is essential in EVs because it directly improves battery efficiency and driving range. At the same time, increased vehicle weight leads to faster tire wear, necessitating enhanced durability and structural strength. These requirements are pushing tire manufacturers to innovate in compound chemistry, tread design, and carcass engineering.

The result is a strong demand for EV-optimized green tires, making this segment one of the fastest-growing within the overall market. As EV penetration increases across both passenger and commercial vehicle segments, green tire adoption is expected to scale proportionally.

Restraint Analysis - Performance Trade-offs and Cost Challenges

Despite strong growth potential, the market faces structural challenges, including performance trade-offs and high development costs. Improving rolling resistance often impacts other critical parameters such as wet grip and braking performance. Balancing these attributes requires significant investment in research, testing, and validation. This complexity increases production costs, making green tires more expensive than conventional alternatives. Price sensitivity remains a key barrier, particularly in emerging markets and the replacement segment, where buyers prioritize affordability. Smaller manufacturers face additional challenges due to limited R&D capabilities, restricting their ability to compete with established global players. These factors, taken together, slow market penetration and create a gap between technical capability and commercial adoption, especially in cost-driven regions.

Opportunity Analysis - Expansion of Aftermarket and Fleet Replacement Demand

The global vehicle parc continues to expand, creating a substantial replacement tire opportunity. With over 92.5 million vehicles produced annually and a rapidly growing EV fleet, demand for replacement tires is both recurring and scalable. Fleet operators, in particular, represent a high-value segment. Their purchasing decisions are driven by total cost of ownership, where fuel savings, energy efficiency, and tire longevity directly impact profitability.

Green tires that deliver measurable performance benefits can accelerate adoption in fleet environments. Manufacturers that integrate durability, efficiency certification, and cost savings into their offerings are well-positioned to capitalize on this opportunity. The aftermarket segment is expected to grow faster than OEM demand due to its volume-driven and recurring nature.

Advancements in Sustainable Materials and Circular Economy

The use of bio-based, recycled, and renewable materials is emerging as a key differentiator in the green tires market. Recent product innovations demonstrate the feasibility of incorporating high percentages of sustainable materials without compromising performance. Technologies such as lightweight tire construction, advanced polymers, and the integration of recycled textiles are gaining traction. These innovations not only reduce environmental impact but also support premium pricing strategies and strengthen brand positioning.

As sustainability becomes a core purchasing criterion, manufacturers that scale these technologies across their product portfolios will gain a competitive advantage. This trend also aligns with broader global goals around carbon reduction and circular manufacturing, opening new avenues for growth.

Category-wise Analysis

Vehicle Type Insights

Passenger cars are expected to dominate, accounting for 63.8% of market share in 2026, driven by their large global vehicle base and high replacement frequency. This segment benefits from strong OEM demand, rising EV adoption, and increasing consumer awareness of fuel efficiency and sustainability. Automakers are increasingly fitting low-rolling-resistance tires as standard equipment to meet emissions and efficiency targets, particularly in hybrid and electric passenger vehicles.

Consumers are showing a clear preference for tires that offer better mileage, reduced noise, and extended lifespan, which directly impacts total ownership cost. For instance, Michelin introduced the Primacy 5 tire range with improved energy efficiency and longer tread life, while Pirelli has integrated sustainable materials into its premium passenger tire lineup. These developments illustrate how manufacturers are embedding green technologies into mainstream offerings rather than positioning them as niche products. As a result, the passenger car segment remains the largest revenue contributor and the primary innovation platform.

Light commercial vehicles (LCVs) are expected to be the fastest-growing segment, driven by the rapid expansion of e-commerce, logistics networks, and last-mile delivery services. Fleet operators prioritize tires that reduce operating costs while maintaining durability under high utilization rates and varying load conditions.

Green tires deliver measurable fuel savings and lower maintenance costs, making them particularly attractive for fleet-based operations. For example, Bridgestone has developed ENLITEN-based tire technologies focused on reducing rolling resistance and improving efficiency in commercial applications, while Continental supplies EV-compatible tires to leading electric van manufacturers. The increasing adoption of electric delivery vehicles by companies such as Amazon further accelerates demand for specialized LCV green tires. This segment is expected to outpace overall market growth due to its strong economic and operational value proposition.

Sales Channel Insights

OEMs are expected to dominate, accounting for 67.1% share in 2026, as vehicle manufacturers increasingly integrate green tires into their design and production processes. Tire performance has become a critical factor in achieving fuel efficiency targets, optimizing EV range, and complying with stringent regulatory standards. OEM partnerships provide tire manufacturers with stable, long-term demand and early involvement in vehicle development cycles.

For instance, Continental supplies tires to a majority of high-volume EV manufacturers worldwide, underscoring the importance of efficiency-focused tire solutions for new vehicle platforms. Similarly, Goodyear collaborates with automakers to develop EV-specific tires that address weight distribution and torque demands. This segment is characterized by high entry barriers, strict technical requirements, and strong brand competition, reinforcing its leadership position.

The aftermarket is expanding rapidly due to the growing global vehicle parc and increasing awareness of tire performance benefits. Consumers and fleet operators are shifting from price-driven decisions to value-based evaluations, focusing on durability, fuel efficiency, and lifecycle cost. Replacement cycles ensure continuous demand, while advancements in tire labeling and digital retail platforms improve transparency and product comparison.

For example, Apollo Tires and CEAT are expanding their green tire portfolios in emerging markets to cater to cost-conscious yet performance-oriented buyers. At the same time, premium brands are leveraging OE-derived technologies to differentiate their aftermarket offerings. This segment presents significant growth potential, particularly in regions with high vehicle ownership, rising mobility demand, and increasing EV adoption.

Regional Insights

North America Green Tires Market Trends - Fleet Efficiency and EV-Driven Premium Tire Innovation

North America represents a mature yet strategically important market, led by the U.S., supported by high vehicle ownership, strong fleet operations, and a well-developed replacement ecosystem. The region’s demand profile is shaped by long-distance freight movement and a high concentration of SUVs and pickup trucks, making tire efficiency and durability commercially critical.

Growth in the region is strongly influenced by EV adoption, regulatory frameworks, and a rising focus on fuel efficiency. Commercial fleets play a central role, as tire performance directly affects fuel consumption and operating margins. For example, Goodyear has expanded its portfolio of EV-ready and low-rolling-resistance tires tailored for North American road conditions, enabling fleets to reduce fuel costs and improve sustainability metrics. Similarly, Michelin has strengthened its presence in the region through SmartWay-verified truck tires, helping logistics operators meet emissions and efficiency targets.

Investment trends are centered on premium products, EV-specific tires, and advanced materials. Bridgestone has been scaling its ENLITEN technology in North America, focusing on lightweight construction and reduced rolling resistance for both passenger and commercial vehicles. These developments reinforce the region’s position as an innovation hub, where technology-driven differentiation and fleet economics shape market growth.

Europe Green Tires Market Trends - Regulation-Led Green Tire Evolution with Circular Material Focus

Europe remains the regulatory benchmark for the green tires market, driven by stringent labeling requirements and environmental policies that emphasize performance transparency. Tire labeling frameworks evaluating rolling resistance, wet grip, and noise have pushed manufacturers to meet higher efficiency standards, making compliance a baseline requirement rather than a competitive advantage.

Key markets such as Germany, France, Spain, and the U.K. contribute through manufacturing strength, R&D capabilities, and high consumer awareness. For instance, Continental has been advancing sustainable tire technologies, including the integration of recycled materials and energy-efficient designs, aligning with European sustainability targets. At the same time, Pirelli introduced a tire made with over 70% bio-based and recycled materials, reflecting the region’s push toward circular-economy practices.

European manufacturers are also focusing on EV-specific innovations. Michelin launched next-generation passenger tires with improved energy efficiency and extended lifespan, directly addressing regulatory and consumer demands. These developments are reshaping the market toward premium, high-compliance products, where sustainability credentials are validated through measurable performance metrics rather than marketing claims.

Asia Pacific Green Tires Market Trends - High-Growth, EV-Driven Mass Production and Export Expansion Hub

Asia Pacific is expected to be the largest and fastest-growing region, with a projected CAGR of 9.8%. Its dominance is driven by large-scale vehicle production, rapid urbanization, and strong EV adoption, particularly in China, Japan, and India.

China leads the region in both vehicle production and EV sales, creating significant demand for green tires. Domestic manufacturers such as ZC Rubber are aligning their products with international standards, including low-rolling-resistance requirements and export compliance requirements, thereby strengthening their global competitiveness. Meanwhile, Hankook Tire has been expanding EV-focused tire solutions, supplying major electric vehicle manufacturers and reinforcing the region’s role in advanced tire innovation.

India is a high-growth market, with companies such as Apollo Tires and CEAT investing in green tire technologies to address rising fuel-efficiency awareness and evolving regulations. In Japan, Bridgestone continues to lead in sustainable material innovation and premium tire development.

ASEAN countries such as Thailand and Indonesia contribute through cost-efficient manufacturing and export-oriented production. These regional dynamics collectively position Asia Pacific as the primary growth engine, where scale, cost advantages, and increasing regulatory alignment are accelerating the adoption of green tires across both domestic and global markets.

Competitive Landscape

The global green tires market is fragmented, with several global and regional players competing across different segments. Leading companies dominate OEM partnerships and technological innovation, while regional players focus on cost competitiveness and local market penetration. Market competition is driven by product performance, sustainability credentials, and pricing strategies.

Key strategies include technological innovation, OEM collaboration, sustainable material adoption, and portfolio optimization. Companies are focusing on EV compatibility, efficiency improvements, and lifecycle performance to strengthen their market position.

Key Industry Developments:

- In March 2025, Bridgestone unveiled its R273 Ecopia regional tire and Duravis M705 for last-mile delivery and mixed fleet operations, both integrated with ENLITEN technology, aiming to enhance fuel efficiency, durability, and sustainability in commercial fleet applications.

- In August 2025, Bridgestone launched the W920 all-weather commercial truck tire featuring ENLITEN technology, designed to deliver longer wear life, improved traction, and optimized rolling resistance, strengthening its position in sustainable fleet mobility solutions.

Companies Covered in Green Tires Market

- Michelin

- Bridgestone

- Continental

- Goodyear Tire & Rubber Company

- Pirelli & C. S.p.A.

- Hankook Tire & Technology

- Yokohama Rubber Company

- Sumitomo Rubber Industries

- Toyo Tire Corporation

- Apollo Tyres Ltd

- MRF Limited

- CEAT Limited

- JK Tyre & Industries Ltd

- Zhongce Rubber Group Co., Ltd.

- Sailun Group Co., Ltd.

- Triangle Tyre Co., Ltd

Frequently Asked Questions

The global green tires market is estimated to be valued at US$53.2 billion in 2026.

The green tires market is projected to reach approximately US$92.4 billion by 2033.

Key trends include rising adoption of electric vehicles (EVs), increasing use of bio-based and recycled materials, advancements in low-rolling-resistance technologies, and stronger regulatory frameworks promoting fuel efficiency and emissions reduction.

The passenger cars segment is the leading category, accounting for an estimated 63.8% market share, driven by high vehicle ownership and strong OEM integration.

The green tires market is expected to grow at a CAGR of 8.2% from 2026 to 2033.

Major companies with strong product portfolios include Michelin, Bridgestone, Continental, Goodyear Tire & Rubber Company, and Pirelli & C. S.p.A.