- Automotive Components & Materials

- Two-Wheeler Fuel Injection System Market

Two-Wheeler Fuel Injection System Market Size, Share, Trends, Growth, Regional Forecasts, 2026 - 2033

Two-Wheeler Fuel Injection System Market by Product Type (Single-Point Fuel Injection, Multi-Point Fuel Injection), Vehicle Type (Standard, Sports, Touring, Cruiser, Scooter, Moped, Others), Engine Capacity (Up to 150 cc, 151-350 cc, 351-650 cc, 651-1000 cc, Above 1000 cc), and Regional Analysis for 2026 to 2033

Two-wheeler Fuel Injection System Market Share and Trends Analysis

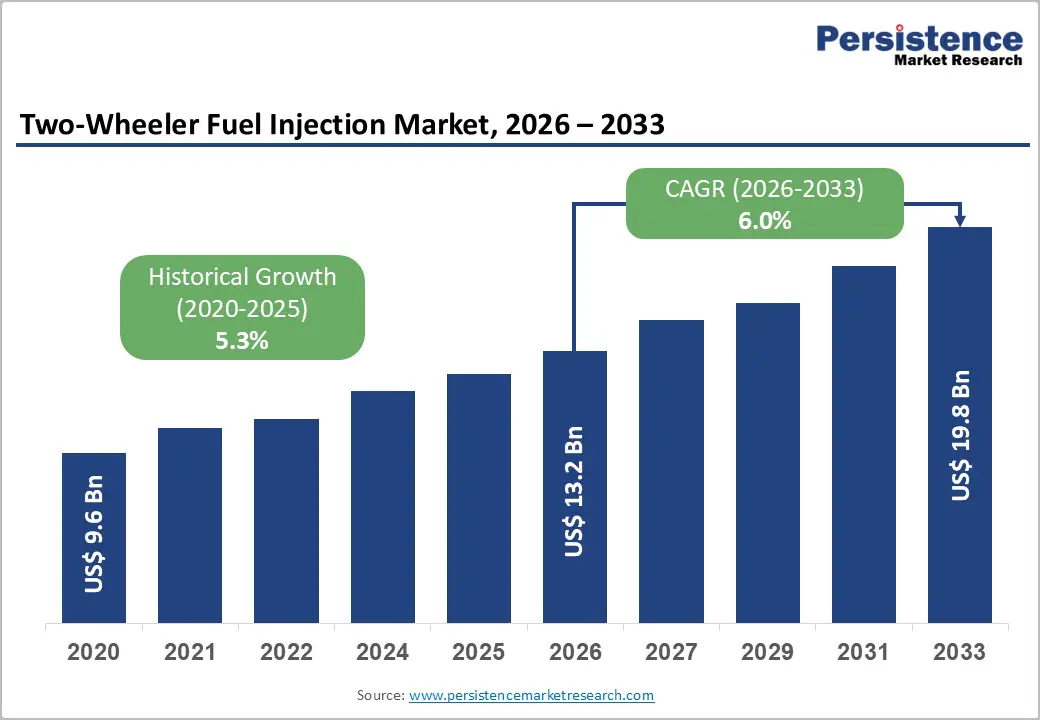

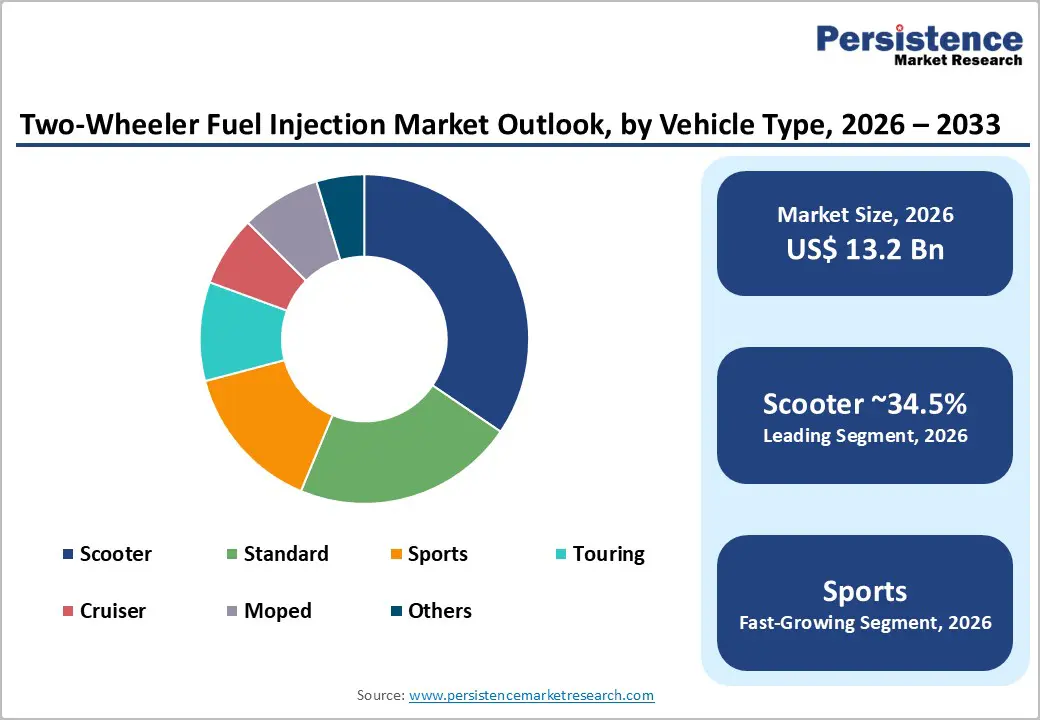

The global two-wheeler fuel injection system market size is anticipated at US$ 13.2 billion in 2026 and is projected to reach US$ 19.8 billion by 2033, growing at a CAGR of 6.0% between 2026 and 2033.

Tightening global emission regulations, including Euro 5 and BS-VI mandates, are compelling OEMs to standardize electronic fuel injection systems across all two-wheeler segments. Accelerating commuter motorcycle penetration in the Asia Pacific, coupled with consumer demand for superior fuel efficiency, reinforces consistent volume growth. OEM integration accounts for approximately 64.5% of market share in 2026, confirming factory-level adoption as the dominant commercial driver.

Key Industry Highlights:

- Leading Product: Multi-Point Fuel Injection leads product type with 71.6% share and is the fastest-growing segment at 6.7% CAGR, driven by OEM premiumization and Euro 5/BS-VI compliance mandates.

- Leading Vehicle Type: Scooters command 34.5% vehicle type share; Sports motorcycles grow fastest at 6.9% CAGR, fueled by rising performance motorcycle demand in mid-displacement categories.

- Dominant Engine Capacity: Up to 150 cc leads engine capacity at 46.2% share; 151-350 cc is fastest-growing at 6.5% CAGR, driven by rapid market expansion in India and ASEAN performance commuter segments.

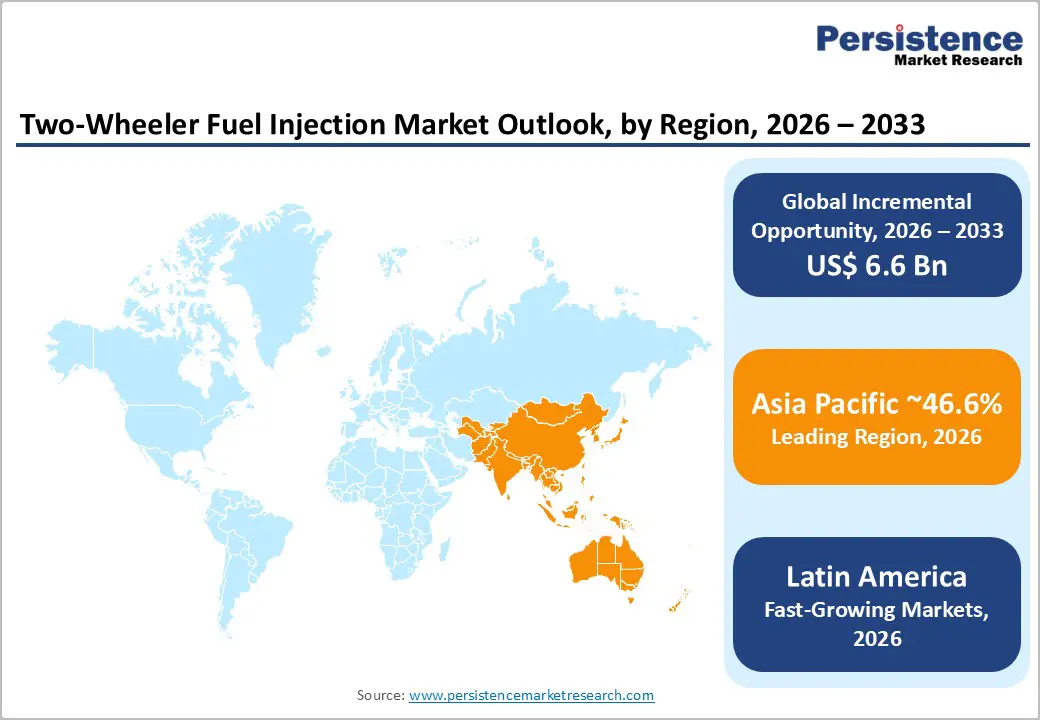

- Regional Leadership: Asia Pacific holds a 46.6% global share, with India projected to grow at 7.3% CAGR. Latin America follows as the second-fastest growing region at 6.1%, driven by increased two-wheeler adoption and stricter emission regulations replacing carburetors with fuel injection.

- Market Competitiveness: Robert Bosch's 2025 cost-optimized EFI platform launch and Denso's Thailand capacity expansion mark key strategic moves reinforcing Asia Pacific supply chain competitiveness.

| Key Insights | Details |

|---|---|

| Global Two-Wheeler Fuel Injection System Market Size (2026E) | US$ 13.2 Bn |

| Market Value Forecast (2033F) | US$ 19.8 Bn |

| Projected Growth CAGR (2026 - 2033) | 6.0% |

| Historical Market Growth (2020 - 2025) | 5.3% |

DRO Analysis

Drivers - Stringent Global Emission Regulations Mandating EFI Adoption

Governments worldwide are enforcing progressively stricter emission norms that are rendering carburetor-based systems non-compliant, effectively mandating fuel injection systems as the functional baseline across all two-wheeler categories. The European Union's Euro 5 standard, effective from January 2021, and India's Bharat Stage VI (BS-VI) norms, implemented in April 2020, have fundamentally restructured powertrain specifications for both OEMs and aftermarket suppliers.

India's BS-VI transition alone impacted over 21 million annual two-wheeler unit sales, the world's largest market, compelling every major domestic manufacturer, including Hero MotoCorp, Honda, Bajaj, and TVS, to transition entirely to EFI platforms. As emission frameworks continue to tighten toward Euro 6 and equivalent regional standards, adoption penetration will deepen across all engine displacement categories, reinforcing multi-year demand for the Two-Wheeler Fuel Injection System Market through 2033.

Consumer Shift Toward Fuel Efficiency and Connected Powertrain Technology

Beyond regulatory compliance, consumer preference is increasingly favoring fuel injection systems for their demonstrated superiority in fuel economy, cold-start reliability, and throttle responsiveness over conventional carburetor setups. EFI systems deliver measurably better fuel efficiency, reducing consumption by approximately 15% to 20% relative to carburetor configurations, which translates to tangible cost savings for high-mileage commuter users in cost-sensitive markets. The convergence of EFI platforms with electronic control units (ECUs), ride-by-wire systems, and traction control technologies is elevating two-wheeler performance intelligence and creating a technology upgrade cycle that benefits the two-wheeler fuel injection system market. Premium segment consumers in North America and Europe are additionally driving demand for high-performance multi-point injection systems in sports and touring motorcycle categories.

Restraints - High System Cost Relative to Carburetor Alternatives in Price-Sensitive Markets

Electronic fuel injection systems carry a materially higher unit cost compared to carburetor-based fuel delivery systems, creating adoption friction in highly price-sensitive emerging markets where entry-level commuter motorcycles dominate volume. In markets such as rural India, Indonesia, and Sub-Saharan Africa, incremental system costs of US$ 30 to US$ 80 per unit can meaningfully impact total vehicle affordability for end consumers. While regulatory mandates are overcoming this barrier at the OEM level, after-replacement demand remains constrained by cost sensitivity, limiting after-sale revenue streams for system suppliers.

Supply Chain Complexity and Semiconductor Component Availability

Fuel injection systems integrate precision-engineered components, including injectors, sensors, ECUs, and fuel pressure regulators that depend on specialty semiconductor inputs and precision manufacturing supply chains concentrated in Asia. Global semiconductor supply disruptions, which caused the auto and two-wheeler sector production shortfalls of over 7 million units globally between 2021 and 2022, have highlighted structural vulnerability in EFI system supply continuity. Ongoing geopolitical tensions affecting semiconductor trade flows between the U.S., China, and Taiwan retain the potential to impose lead-time extensions and cost increases on fuel injection system manufacturers, constraining market responsiveness.

Opportunities - Upgrade Demand in the 151-350 cc Sports and Performance Segment

The 151-350 cc engine displacement segment, identified as the fastest-growing capacity category at 6.5% CAGR, presents a structurally compelling upgrade opportunity for multi-point fuel injection system suppliers. Consumer demand for performance-oriented mid-displacement motorcycles including the KTM Duke series, Royal Enfield 350 platform, and Yamaha MT series, is expanding rapidly across India, Southeast Asia, and Europe. These models require sophisticated EFI calibration for optimal power delivery and emissions compliance. Manufacturers investing in scalable, cost-optimized MPFI solutions for the mid-displacement performance segment can capture a high-value margin pool while benefiting from volume ramp-up in one of the fastest-growing vehicle categories globally within the Two-Wheeler Fuel Injection System Market.

Aftermarket EFI Retrofit and Modernization in Emerging Economies

Millions of carburetor-equipped two-wheelers currently operating across emerging markets in South Asia, Latin America, and Africa represent a substantial latent, aftermarket EFI retrofit opportunity. As regulatory compliance requirements extend to in-use vehicle fleets in some jurisdictions and as fuel savings awareness grows among high-mileage commercial riders, demand for aftermarket EFI kits is beginning to form commercially viable market segments. Companies such as SEDEMAC and UCAL Systems are developing cost-optimized, plug-and-play EFI retrofit solutions targeting this underserved need. Government programs supporting cleaner transportation in developing economies may further stimulate aftermarket demand with incentive mechanisms, creating an actionable growth opportunity for specialized retrofit suppliers within the two-wheeler fuel injection system market.

Category-wise Analysis

Product Type Insights

Multi-Point Fuel Injection (MPFI) leads the product type segmentation with a dominant 71.6% global market share in 2026, reflecting its superior performance credentials across sports, touring, and premium commuter motorcycle categories. MPFI systems deliver individualized fuel injections at each cylinder intake port, enabling precise air-fuel ratio control, enhanced combustion efficiency, and lower emissions output relative to single-point alternatives. OEM adoption of MPFI across mid-to-high displacement platforms, including flagship models from Honda, Yamaha, Suzuki, and Kawasaki, reinforces this segment's sustained commercial leadership across all major geographies.

Multi-Point fuel injection is simultaneously the fastest-growing segment at 6.7% CAGR, driven by continuous OEM premiumization, tightening Euro 5 and BS-VI compliance requirements across higher displacement models, and consumer preference for high-performance powertrain systems in sports and touring categories.

Vehicle Type Insights

Scooters represent the leading vehicle type segment with 34.5% of global market share, reflecting their dominance in urban commuter mobility across Asia Pacific, Southern Europe, and Latin America. Scooters account for the highest annual two-wheeler production volumes in markets including India, Vietnam, Indonesia, and China, where compact, automatic urban mobility solutions command mass consumer preference. Regulatory mandates under BS-VI in India and Euro 5 in Europe have accelerated factory-level EFI standardization across the scooter category, converting previously carburetor-equipped volume models to electronically managed fuel delivery systems at scale.

Sports motorcycles are the fastest-growing vehicle type segment at 6.9% CAGR, fueled by rising consumer aspiration for performance-oriented two-wheelers in the 151 cc to 650 cc displacement range, OEM model proliferation in emerging markets, and demand for advanced MPFI systems with ride-by-wire integration.

Engine Capacity Insights

Up to 150 cc is the dominant engine capacity segment, commanding 46.2% of global market share in 2026, reflecting the extraordinary volume concentration of sub-150 cc two-wheelers in the world's largest markets. India, Indonesia, Vietnam, and China collectively produce tens of millions of sub-150 cc motorcycles and scooters annually for commuter use, and the wholesale transition of these platforms to EFI under national emission norms represents the single largest volume driver within the Two-Wheeler Fuel Injection System Market. Hero MotoCorp alone produces over 7 million units annually, the majority of which now incorporate compliant EFI systems post BS-VI implementation.

The 151-350 cc segment is the fastest-growing engine capacity category at 6.5% CAGR, driven by rapid market development in the performance commuter and entry-level sports segment. Rising consumer aspiration, competitive OEM pricing in this displacement range, and regulatory compliance demands are collectively accelerating EFI adoption.

Regional Market Analysis

North America Two-Wheeler Fuel Injection System Market

North America holds approximately 19.6% of the global two-wheeler fuel injection system market share, supported by a mature premium motorcycle ecosystem dominated by large-displacement touring, cruiser, and sports platforms. The U.S. represents the primary regional market, where consumers exhibit a high willingness-to-pay for advanced EFI technologies integrated with ECUs, traction control, and riding mode systems.

The U.S. Environmental Protection Agency's (EPA) Tier 3 standards and California Air Resources Board (CARB) regulations mandate EFI-compatible emission control systems across all compliant motorcycles. Harley-Davidson, Indian Motorcycle, and Polaris all rely on sophisticated EFI platforms for their domestic product lines, reinforcing premium system demand. Innovation in fuel injection integration with connected vehicle platforms and telematics is progressing strongly across North American OEMs and Tier 1 suppliers.

Investment activity in North America is increasingly directed toward EFI system software calibration, OTA update capability, and hybrid powertrain integration, reflecting the regional market's shift toward technology premiumization as the primary demand growth driver.

Europe Two-wheeler Fuel Injection System Market Insights

Europe is expected to achieve a prominent 5.8% CAGR, driven by the regulatory transition to Euro 5 standards and approaching Euro 6 frameworks that are progressively eliminating carburetor systems from all compliant two-wheeler categories.

Germany, the U.K., France, and Spain constitute the dominant European markets, collectively accounting for a significant portion of regional EFI system demand. Germany's strong sports and touring motorcycle culture, anchored by BMW Motorrad and KTM, sustains premium MPFI system demand at high average selling prices. The U.K. and France demonstrate sustained scooter and urban commuter growth, particularly in major metropolitan areas adopting low-emission zone policies that favor EFI-compliant vehicles over older carburetor-equipped models.

Spain represents a growing market for mid-displacement sports motorcycles, while EU harmonized type approval regulations enable pan-European EFI certification, reducing compliance complexity for Tier 1 system suppliers operating across multiple member state markets.

Asia Pacific Two-wheeler Fuel Injection System Market Trends

Asia Pacific is the dominant regional market with 46.6% of global market share, constituting the commercial center of gravity for the two-wheeler fuel injection system market. India represents the world's largest two-wheeler market by annual unit volume, with sales exceeding 19 million units in FY2024 per SIAM data, and BS-VI compliance having mandated EFI standardization across the entire new vehicle fleet since April 2020.

India's annual two-wheeler production has surpassed 20 million units recently, while China's motorcycle sector still produces significantly, even as it shifts toward electric two-wheelers under 125 cc, with fuel injection demand focused on mid-to-high displacement combustion engines. Japan sustains premium system technology development, with Yamaha, Honda, Suzuki, and Kawasaki headquartered there and continuously investing in next-generation EFI and hybrid powertrain systems. India is projected to grow at approximately 7.3% CAGR through the medium term, reinforcing Asia Pacific's dominant and accelerating position.

Vietnam, Indonesia, Thailand, and the Philippines collectively represent a high-growth ASEAN subsegment, with governments progressively implementing Euro-equivalent emission standards that are driving systematic EFI adoption across high-volume domestic production.

Competitive Landscape

Market leaders in the Two-Wheeler Fuel Injection System Market are prioritizing platform-level EFI integration, system miniaturization, and cost-optimized scalability as the dominant strategic themes. Bosch and Denso leverage global OEM partnerships and localized manufacturing to maintain cost and scale advantages. Emerging players are differentiating through hybrid-compatible EFI architectures, indigenous system development for price-sensitive markets, and integrated ECU-injector module solutions that reduce OEM assembly complexity across high-volume platforms.

Strategic Developments:

- In March 2025, Robert Bosch GmbH Expanded its two-wheeler EFI portfolio with a new cost-optimized fuel injection platform for sub-150 cc commuter motorcycles, targeting high-volume emerging markets in India and Southeast Asia with integrated ECU and sensor modules.

- In 2024, Marelli Holdings Co., Ltd. enhanced its competitive edge by investing in R&D for advanced multi-point and high-pressure fuel injection systems, focusing on hybrid-compatible powertrains. The company aims to support evolving two-wheeler architectures with hybrid and alternative fuel solutions, aligning with OEM developments from Honda and Piaggio.

- In 2024, Denso Corporation Expanded manufacturing capacity for two-wheeler fuel injection components at its Thailand production facility, strategically positioning ASEAN-based supply chain infrastructure to serve the region's tightening emission compliance transition and rising EFI adoption across major local OEM partners.

Companies Covered in Two-Wheeler Fuel Injection System Market

- Robert Bosch GmbH

- Marelli Holdings Co. Ltd.

- Denso Corporation

- Mikuni Corporation

- Hitachi Astemo Ltd

- Continental AG

- UCAL Systems Inc.

- SEDEMAC Mechatronics Pvt. Ltd

- Ducati Energia S.p.A

- Walbro LLC

- Edelbrock LLC

- Keihin Corporation

- Delphi Technologies

- Nikki Co. Ltd

- Magneti Marelli

Frequently Asked Questions

The two-wheeler fuel injection system market is valued at US$ 13.1754 Bn in 2026, projected to reach US$ 19.81 Bn by 2033.

Stringent emission regulations (Euro 5, BS-VI), Asia Pacific production volumes, and consumer demand for fuel efficiency and connected powertrain technology are the primary drivers.

The market is projected to grow at a CAGR of 6.0% from 2026 to 2033, accelerating from a 5.34% historical growth rate.

MPFI adoption in the 151-350 cc performance segment, hybrid two-wheeler EFI integration, and aftermarket EFI retrofit demand in emerging economies represent the highest-potential growth opportunities.

Leading players include Robert Bosch GmbH, Marelli Holdings, Denso Corporation, Mikuni Corporation, Hitachi Astemo, Continental AG, UCAL Systems, SEDEMAC Mechatronics, Ducati Energia, and Keihin Corporation, among others.