- Sporting Goods & Equipment

- Sports Protective Equipment Size, Share, and Growth Forecast 2026 - 2033

Sports Protective Equipment Size, Share, and Growth Forecast 2026 - 2033

Sports Protective Equipment Market by Product Type (Protective eyewear (Goggles, Eye shield), Face Protection & Mouthguards, Helmets & Headgear, Pads, Guards & Chest Protectors (Knee Pads, Elbow Guards, Shin Guards, Shoulder Pads), Foot & Ankle Protection, Others), Distribution Channel (Offline Retail (Specialty Sports Stores, Supermarkets / Hypermarkets), Online), by Price Range (Economy, Mid-range, Premium), and Regional Analysis, 2026 - 2033

Sports Protective Equipment Market Size and Trend Analysis

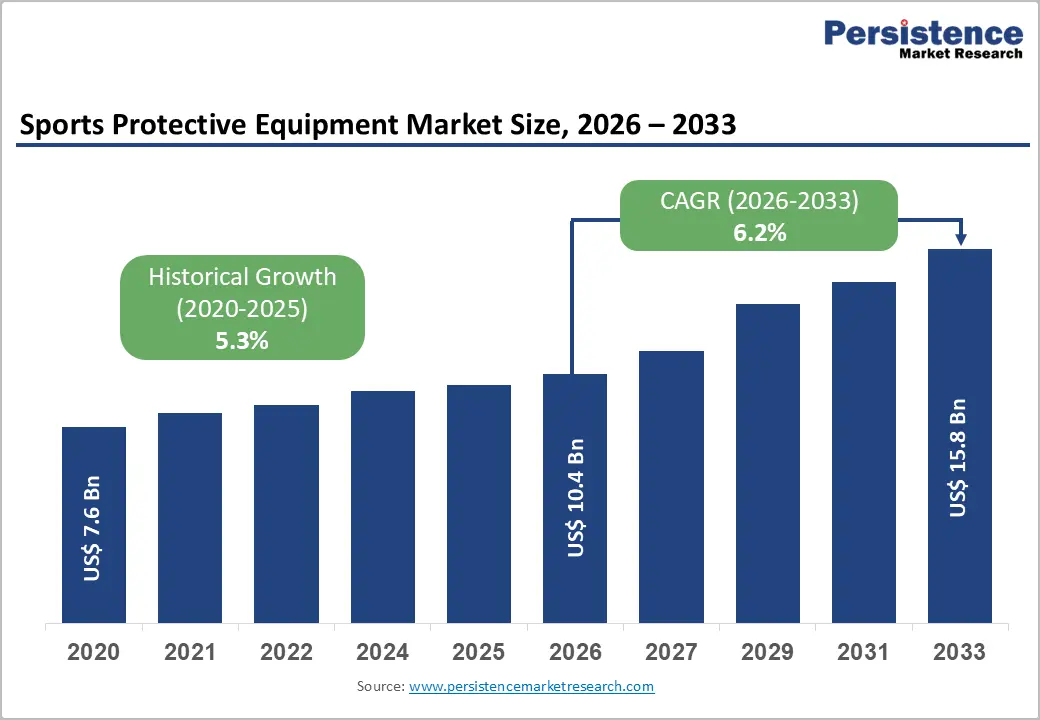

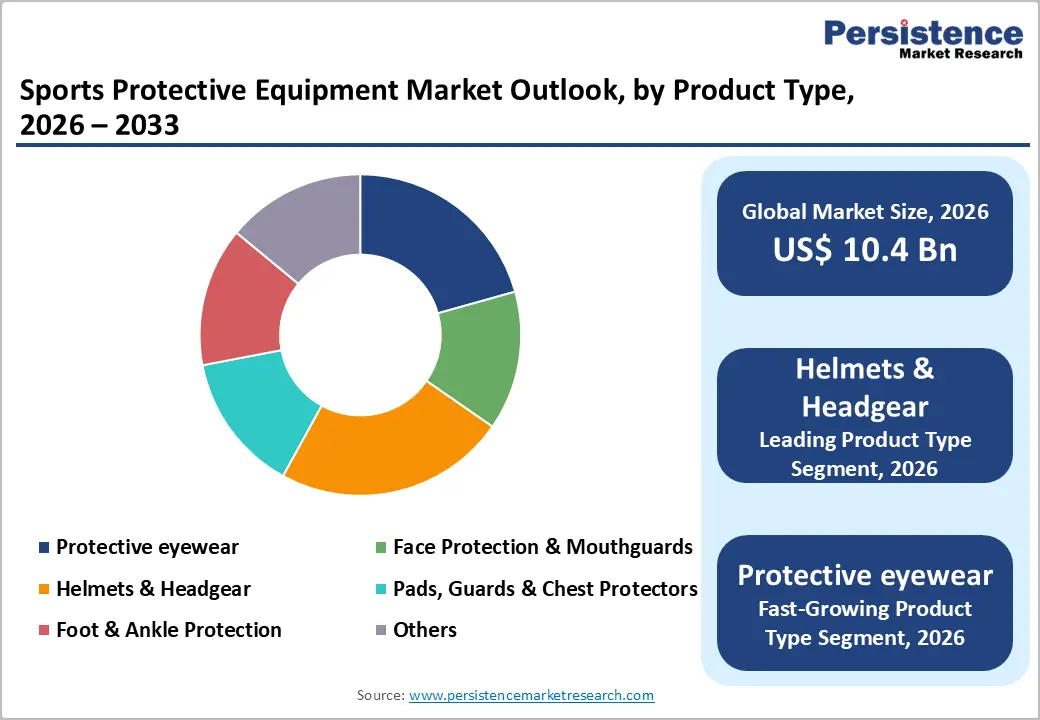

The global Sports Protective Equipment market size is expected to reach US$10.4 billion in 2026 and US$15.8 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

Growth is driven by rising participation in contact sports and increasing enforcement of safety standards across professional and amateur leagues. The high incidence of sports-related injuries is accelerating demand for certified protective gear. Additionally, growing parental awareness, school-level safety mandates, and continuous innovation in lightweight, impact-absorbing materials are supporting widespread adoption, enhancing performance, comfort, and injury prevention across diverse sporting activities globally.

Key Market Highlights

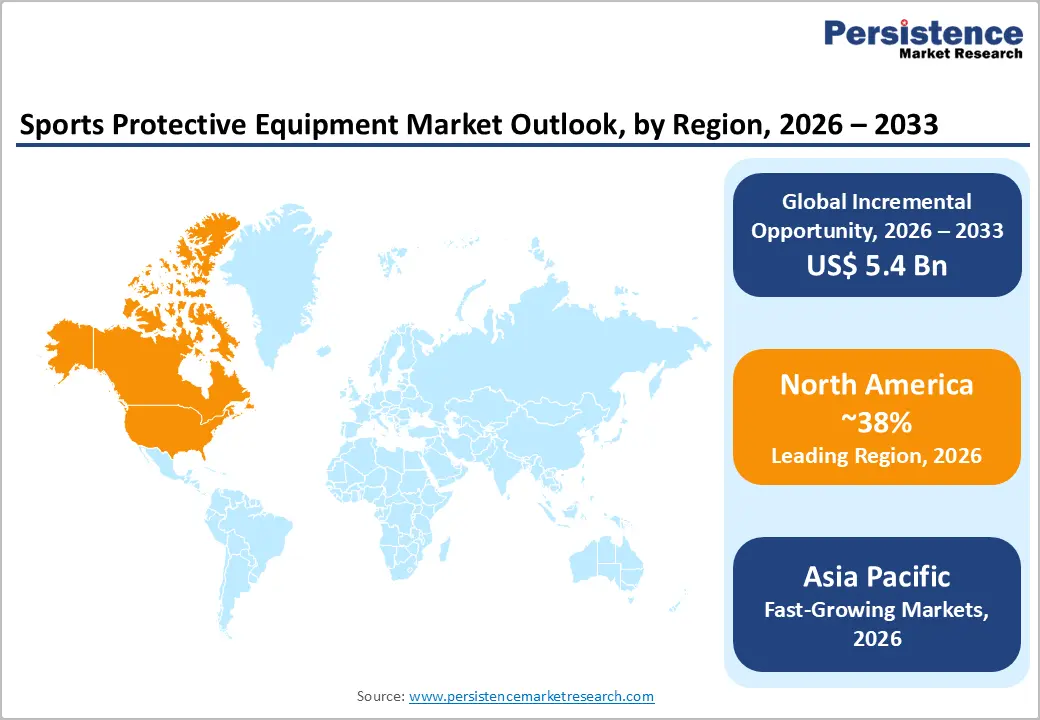

- Leading Region: North America leads the Sports Protective Equipment market with 38% share in 2025, driven by a strong sports culture and stringent safety regulations.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with a positive CAGR supported by rising sports participation and manufacturing expansion.

- Leading Product Type: Helmets & Headgear dominate with 35% share in 2025, owing to their critical role in preventing head injuries in contact sports.

- Fastest-Growing Category: Online distribution is growing at a leading CAGR, fueled by rapid e-commerce adoption and convenience.

- Key Opportunity: Increasing integration of smart and sensor-based protective gear presents strong opportunities for enhanced injury prevention and performance tracking.

| Key Insights | Details |

|---|---|

|

Sports Protective Equipment Size (2026E) |

US$ 10.4 Billion |

|

Market Value Forecast (2033F) |

US$ 15.8 Billion |

|

Projected Growth CAGR(2026-2033) |

6.2% |

|

Historical Market Growth (2020-2025) |

5.3% |

Market Dynamics

Drivers - Rising Global Participation in Contact Sports Driving Demand

Global participation in contact sports such as football, hockey, and cycling continues to grow significantly, increasing injury risk and boosting demand for protective equipment. Sports bodies report billions of active participants worldwide, while school-level engagement is also rising steadily, particularly in organized athletic programs. This growing base of athletes is creating sustained demand for reliable and certified safety gear across multiple age groups.

Additionally, strict safety mandates from governing organizations and leagues are reinforcing the use of equipment. Regulations requiring helmets and protective gear have demonstrated measurable reductions in injury rates, encouraging wider adoption. Manufacturers are responding with ergonomically designed products that comply with established safety standards, ensuring comfort, performance, and regulatory adherence while supporting long-term market growth.

Continuous Innovations in Advanced Protective Material Technologies

Advancements in material science are significantly enhancing the performance and adoption of sports protective equipment. The use of lightweight composites, carbon fiber, and smart polymers improves impact resistance while maintaining flexibility and comfort. These materials offer superior shock absorption compared to traditional foam-based products, making them increasingly preferred across high-impact and endurance sports applications.

Furthermore, innovations in breathable, moisture-wicking fabrics are improving user comfort and encouraging prolonged use among athletes. Endorsements from sports federations and ongoing research highlight the effectiveness of modern protective gear in reducing injury risks. Enhanced durability and performance characteristics are also driving demand for premium products, contributing to the overall expansion of the global market.

Restraints - High Manufacturing Costs Limiting Market Accessibility Globally

The production of sports protective equipment involves expensive raw materials such as advanced foams, composites, and high-performance fibers, which are subject to significant price fluctuations. Supply chain disruptions and material scarcity further increase procurement costs, directly impacting manufacturing margins. These elevated input costs make it challenging for manufacturers to maintain competitive pricing, especially in cost-sensitive markets.

Additionally, stringent certification and testing requirements add a substantial financial burden to production processes. Compliance with international safety standards requires rigorous validation, increasing overall product costs. Smaller manufacturers often struggle to meet these requirements, limiting their market presence and reducing product affordability, particularly in developing regions.

Rising Counterfeit Products Undermining Consumer Trust and Safety

The growing presence of counterfeit sports protective equipment poses a serious challenge to market growth. These low-quality imitations often fail to meet established safety standards, compromising user protection and increasing the risk of injuries. The widespread availability of such products, especially through unregulated distribution channels, negatively impacts consumer confidence in protective gear.

Moreover, counterfeit products weaken the brand value of established manufacturers and create unfair market competition. Frequent product recalls and safety concerns about counterfeit equipment further discourage adoption. This not only affects revenue generation for legitimate players but also slows overall market penetration, particularly in regions with limited regulatory enforcement.

Opportunities - Expanding Youth and Women Participation Creating Growth Opportunities

The increasing participation of youth in organized sports is creating strong demand for properly fitted and reliable protective equipment. A large global base of young athletes requires gear that minimizes injury risk while ensuring comfort and performance. This trend is further supported by school programs and community-level sports initiatives, which continue to expand participation rates across regions.

Simultaneously, the rapid rise in women’s sports is generating new opportunities for specialized protective gear. Demand for ergonomically designed equipment tailored to female athletes is growing, supported by inclusion programs and policy initiatives. Manufacturers focusing on customized and sport-specific designs are well-positioned to capitalize on this expanding segment globally.

Integration of Smart Technologies Enhancing Equipment Performance

The integration of smart technologies into sports protective equipment is emerging as a key growth opportunity. Advanced sensors embedded in helmets and protective gear enable real-time monitoring of impacts and injuries, improving athlete safety and performance tracking. These innovations are gaining traction across professional and amateur sports environments, supporting data-driven decision-making.

Furthermore, increasing adoption of connected and IoT-enabled equipment by coaches and sports organizations is accelerating market expansion. As global participation in athletics continues to rise, demand for technologically advanced protective gear is expected to grow significantly. This trend is particularly driving the premium segment, where enhanced functionality and safety features offer strong value propositions.

Category-wise Analysis

Product Type Insights

Helmets and headgear dominate the product type segment, accounting for around 35% of the market share in 2025 due to the high incidence of head-related injuries in sports. The critical need for cranial protection across activities such as football, hockey, and cycling continues to drive demand. Strict safety standards and regulations further reinforce adoption, while advancements in ventilation and lightweight design enhance comfort and performance, strengthening segment leadership.

Protective eyewear and advanced facial protection are emerging as the fastest-growing categories within this segment. Increasing awareness of eye and facial injuries, along with innovations in impact-resistant materials and anti-fog technologies, is driving adoption. Growth is further supported by expanding participation in high-speed and outdoor sports where visibility and protection are equally critical.

Distribution Channel Insights

Offline retail leads the distribution channel segment with approximately 55% share in 2025, as consumers prefer physical stores for product trials and proper fitting. Specialty sports outlets provide expert guidance and ensure compliance with safety standards, which enhances consumer confidence. The ability to physically assess comfort, durability, and fit continues to make offline channels the preferred channel for purchasing protective equipment.

Online distribution is the fastest-growing channel, driven by increasing e-commerce penetration and convenience. Digital platforms offer a wide range of products, competitive pricing, and easy accessibility, attracting a growing number of consumers. Advancements in virtual fitting tools and detailed product information are further supporting the global shift toward online purchasing.

Price Range Insights

The mid-range segment holds the largest share at around 45% in 2025, driven by its balance between affordability and quality. Consumers, particularly families and recreational athletes, prefer products that offer certified protection at a reasonable price. This segment benefits from strong demand for durable, value-driven equipment that meets safety standards while remaining accessible to a broad consumer base.

The premium segment is witnessing the fastest growth, fueled by increasing demand for technologically advanced and high-performance gear. Innovations in materials, smart features, and enhanced durability are attracting professional athletes and serious enthusiasts. As awareness of safety and performance improves, consumers are increasingly willing to invest in premium protective equipment.

Regional Insights

North America Sports Protective Equipment Market Trends and Insights

North America dominates the sports protective equipment market, accounting for approximately 38% share in 2025, led by the United States. The region benefits from well-established sports infrastructure, high participation rates, and strict safety regulations across professional and amateur leagues. Regulatory frameworks and continuous monitoring of sports-related injuries have significantly improved equipment standards and adoption rates.

Additionally, strong involvement from major sports leagues and youth programs continues to drive innovation and demand. Investments in research and development, particularly in helmet safety and impact protection technologies, further strengthen the region’s leadership. Growing awareness among parents and institutions regarding athlete safety also contributes to sustained market growth across North America.

Europe Sports Protective Equipment Market Trends and Insights

Europe represents a mature market supported by structured regulatory frameworks and strong sports culture across countries such as Germany, the UK, and France. The region benefits from harmonized safety standards that ensure consistent product quality and performance across member states. Increasing participation in organized sports and recreational activities continues to drive steady demand for protective equipment.

Europe is projected to grow at a CAGR of around 6.0% during the forecast period, supported by continuous advancements in product design and materials. Rising awareness regarding athlete safety, along with the presence of established sporting events and governing bodies, is further encouraging adoption. Manufacturers are also focusing on sustainable and high-performance gear to align with evolving consumer preferences.

Asia Pacific Sports Protective Equipment Market Trends and Insights

Asia Pacific is a rapidly expanding market, accounting for approximately 30% of the market share in 2025, driven by rising sports participation and increased investments in sports infrastructure. Countries such as China, India, and Japan are experiencing significant growth driven by government initiatives promoting physical activity and international sporting events. Expanding middle-class populations are also contributing to higher spending on sports safety equipment.

The region is projected to grow at a CAGR of 7.8%, making it the fastest-growing market globally. Growth is supported by strong manufacturing capabilities, rising awareness of injury prevention, and increasing adoption of protective gear across both professional and recreational sports. Additionally, regional production hubs are enabling cost-effective supply, further accelerating market penetration.

Competitive Landscape

The sports protective equipment market is moderately consolidated, with leading players focusing on strengthening their positions through strategic acquisitions and continuous product innovation. Companies are investing in advanced materials, including impact-absorbing and sustainable alternatives, to enhance performance and meet evolving safety standards. Technological differentiation, particularly through patented protection systems and customized designs, plays a critical role in maintaining competitive advantage.

At the same time, market participants are expanding direct-to-consumer channels, leveraging e-commerce platforms and subscription-based models to improve customer engagement. Despite these advancements, regional fragmentation remains a challenge, requiring companies to adapt their strategies based on local regulations, consumer preferences, and distribution dynamics.

Key Developments:

- In June 2025, Riddell introduced the SpeedFlex Diamond helmet featuring enhanced impact mitigation technology. The product demonstrated a 25% reduction in impact force during testing, reinforcing advancements in helmet safety standards and performance optimization.

- In March 2024, Bauer Hockey launched sensor-enabled mouthguards in collaboration with professional leagues, integrating real-time impact tracking technology. This innovation supports injury monitoring and aligns with the growing adoption of smart protective equipment across competitive sports.

- In October 2024, Rawlings unveiled sustainable shin guards developed using eco-friendly materials while meeting established safety certifications. The launch reflects increasing industry focus on sustainability alongside performance, catering to environmentally conscious consumers and regulatory expectations.

Companies Covered in Sports Protective Equipment Size, Share, and Growth Forecast 2026 - 2033

- Riddell

- Schutt Sports

- Bauer Hockey

- Rawlings

- Nike

- Adidas

- Under Armour

- Xenith

- Vulcan, Mach

Frequently Asked Questions

The market is expected to reach US$ 10.4 Billion in 2026, supported by strong demand across key segments like Helmets & Headgear (35%) and Mid-range products (45%).

Rising injury awareness, safety regulations, and strong adoption via Offline Retail (55% share) drive demand.

North America leads with a 38% share in 2025, driven by strict safety standards and high sports participation.

Smart sensor-based protective gear presents a major opportunity, alongside growth in Asia Pacific with 30% share.

Key players include Riddell, Bauer Hockey, and Nike lead with innovations.