- Energy Storage Solutions

- Solid Oxide Fuel Cell Market

Solid Oxide Fuel Cell Market Size, Share, and Growth Forecast 2026 - 2033

Solid Oxide Fuel Cell Market by Structure (Planar, Tubular), Application (Stationary, Transportation, Portable), End-user (Residential, Commercial & Industrial, Data Center, Military & Defense, Others), and Regional Analysis, 2026 - 2033

Solid Oxide Fuel Cell Market Size and Trend Analysis

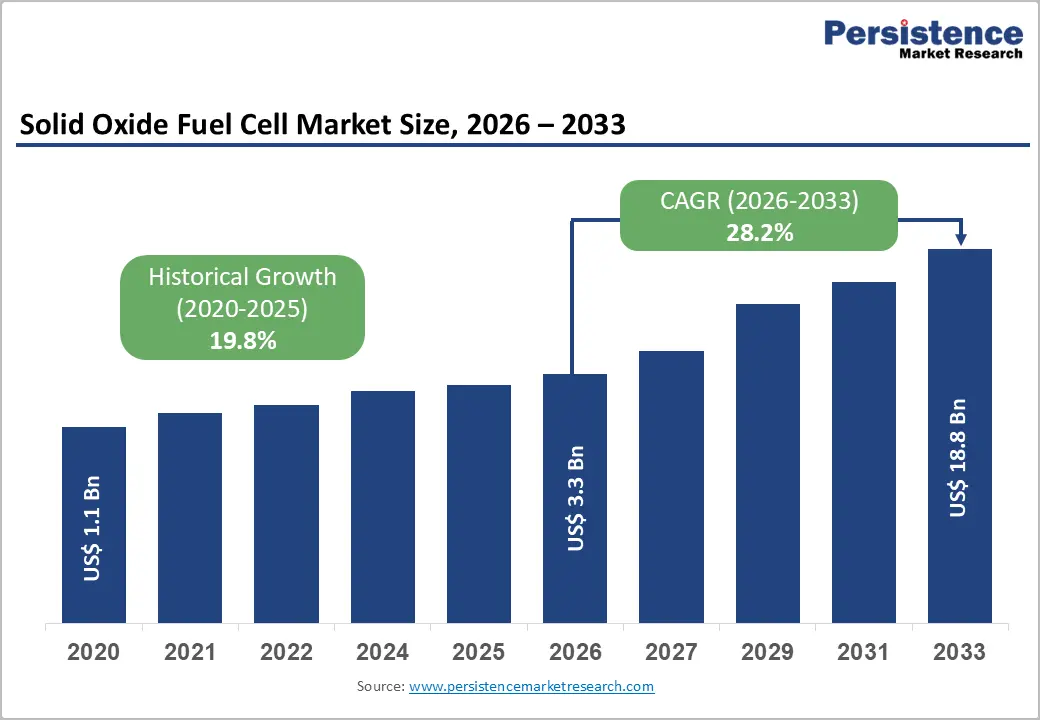

The global solid oxide fuel cell (SOFC) market size is expected to be valued at US$ 3.3 billion in 2026 and is projected to reach US$ 18.8 billion by 2033, growing at an exceptional CAGR of 28.2% between 2026 and 2033. This remarkable growth trajectory is driven by the global energy transition toward low-carbon and hydrogen-based power generation, rapidly growing demand for highly efficient distributed power systems, and intensifying government investment in clean energy infrastructure across North America, Europe, and the Asia Pacific.

SOFCs, which convert fuel directly to electricity at efficiencies exceeding 60% in combined heat and power (CHP) configurations, are increasingly recognized as a cornerstone technology in achieving net-zero energy commitments. Supportive policies, including the U.S. Inflation Reduction Act (IRA), the EU Hydrogen Strategy, and Japan's Green Growth Strategy, are channeling billions in public and private capital toward SOFC commercialization across stationary, data Centre, and military applications.

Key Industry Highlights

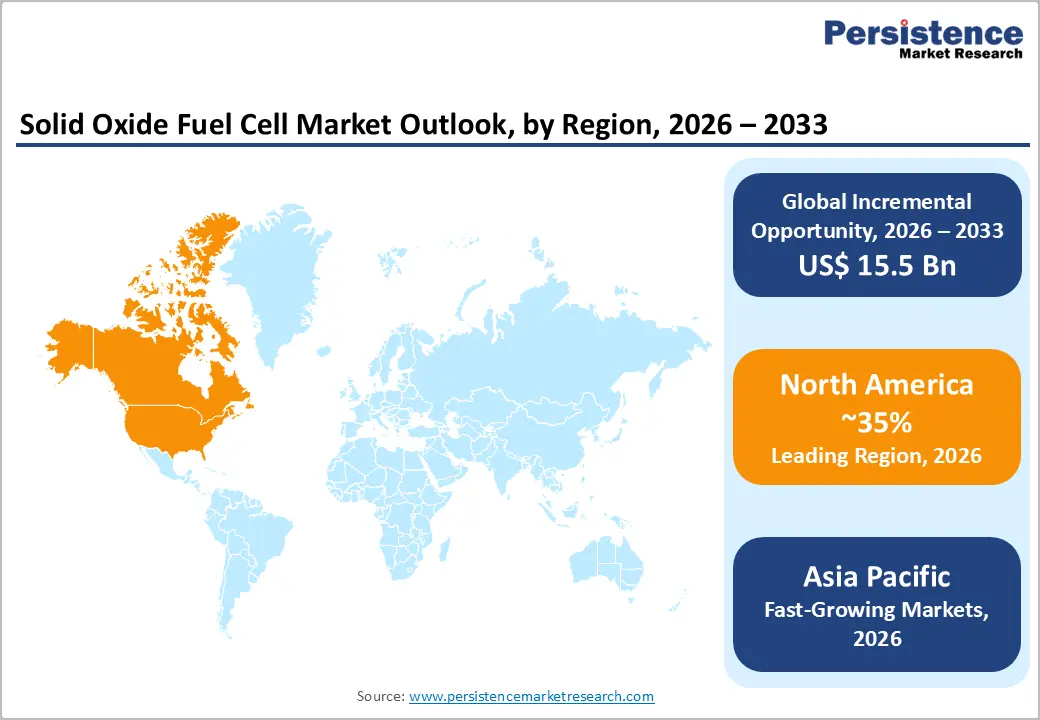

- Leading Region: North America leads the global SOFC market with approximately 35% revenue share in 2026, driven by U.S. IRA investment tax credits, DOE Hydrogen Shot funding, and Bloom Energy's 1+ GW of deployed SOFC capacity serving data centres and C&I customers.

- Fast-Growing Market: Asia Pacific is the fastest-growing SOFC market, propelled by Japan's ENE-FARM programme with over 500,000 residential units, China's hydrogen economy acceleration under the 14th Five-Year Plan, and India's National Green Hydrogen Mission infrastructure investments.

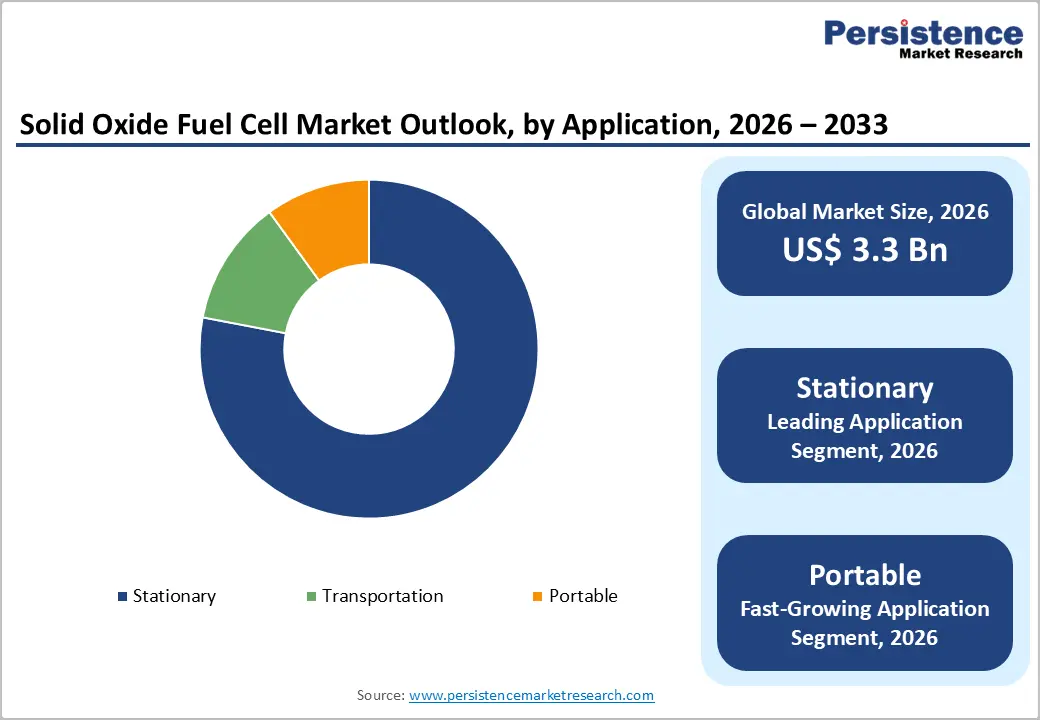

- Dominant Applications: Stationary SOFC systems dominate with approximately 79% of global market share in 2026, underpinned by large-scale C&I and data centre deployments, Japan's residential CHP programme, and SOFC's unmatched efficiency advantage exceeding 65% in distributed generation applications.

- Fast-Growing Application: Portable SOFC applications are growing at a projected CAGR of 34%, driven by U.S. military procurement via DARPA programmes, emergency backup power demand, and SOFC's superior energy density and silent operation versus diesel generators and lithium-ion batteries.

- Key Opportunity: The most transformative near-term opportunity is in data center SOFC deployments serving 24/7 carbon-free energy mandates from Google, Microsoft, and Amazon), and in green hydrogen-fueled SOFC systems enabled by the IRA and EU Hydrogen Strategy investment frameworks.

DRO Analysis

Drivers - Global Decarbonization Mandates and Clean Hydrogen Energy Policy Support

Binding net-zero commitments and clean energy policy frameworks are the most powerful structural forces accelerating SOFC adoption globally. The International Energy Agency (IEA) projects that hydrogen, the primary fuel for SOFC systems, must supply approximately 10% of final energy demand by 2050 under net-zero scenarios, requiring a massive scale-up of fuel cell power generation. The U.S. Department of Energy (DOE) has allocated over US$ 9.5 billion through the Bipartisan Infrastructure Law for clean hydrogen hubs, while the European Commission has committed €470 billion in investments under the REPowerEU Plan to accelerate hydrogen economy development.

The IRA's investment tax credit (ITC) extension to fuel cell systems, covering up to 30% of installed costs, is directly stimulating SOFC project development and deployment across the U.S. commercial and industrial power sector.

Surging Power Demand from Data Centers and Digital Infrastructure

The explosive growth of data centers driven by artificial intelligence, cloud computing, and 5G infrastructure is creating a structurally new and high-value demand segment for SOFC technology. The International Energy Agency (IEA) estimates that global data Centre electricity consumption could reach 1,000 TWh by 2026, nearly doubling from 2022 levels. Data center operators face intensifying pressure to decarbonize while ensuring highly reliable, low-latency power, a dual requirement that SOFC systems satisfy through their combination of high efficiency, ultra-low emissions, and resilient distributed generation capability.

Bloom Energy, which supplies SOFC-based power solutions to major technology companies including Google, Microsoft, and Samsung, has demonstrated SOFC systems achieving electrical efficiencies of over 65%, significantly outperforming conventional gas turbines and grid-supplied power in both cost and carbon performance at scale.

Restraints - High Capital Cost and Complex Manufacturing Requirements

Despite compelling operational economics, the high upfront capital cost of SOFC systems remains a significant barrier to mass-market adoption. Current installed costs for SOFC-based distributed generation systems range between US$ 4,000-7,000 per kilowatt, substantially higher than conventional combined cycle gas turbines at US$ 1,000-1,500 per kilowatt.

The manufacture of SOFC cells requires high-purity ceramic materials processed at temperatures exceeding 1,400°C, demanding sophisticated production infrastructure and quality controls that limit manufacturing scale-up speed. These cost and complexity dynamics restrict near-term SOFC adoption primarily to high-value, mission-critical applications where premium reliability and efficiency justify elevated capital expenditure.

Fuel Purity Requirements and Hydrogen Infrastructure Immaturity

SOFC systems are sensitive to fuel contaminants, particularly Sulphur compounds and certain hydrocarbons, which can degrade ceramic electrode materials and reduce cell lifetime. While SOFCs can operate on natural gas, biogas, and hydrogen, fuel pre-processing and Sulphur removal systems add system complexity and cost.

More critically, the global clean hydrogen supply infrastructure remains nascent: the IEA estimates that clean hydrogen production in 2023 was less than 1 million tons annually against a projected demand of 180 million tons by 2050, representing a significant supply chain maturity gap that constrains the acceleration of pure hydrogen-fueled SOFC deployments.

Opportunities - Portable SOFC Systems - Fastest Growing Application Segment

Portable SOFC applications represent the fastest-growing segment within the market, projected to expand at a CAGR of 34% between 2026 and 2033. Military and defense forces are primary early adopters, driven by the need for silent, high-energy-density portable power for forward operating bases, unmanned vehicles, and soldier-worn electronics. The U.S. Army and U.S. Marine Corps have funded SOFC portable power development programmes through the Defense Advanced Research Projects Agency (DARPA) and the Army Research Laboratory.

Beyond defense, portable SOFC units are gaining traction for emergency backup power, off-grid telecommunications, and expedition use, addressable market segments that benefit from SOFC's superior energy density over lithium-ion batteries and near-silent operation compared to diesel generators. Companies, including Atrex Energy and Redox Power Systems, are specifically targeting these high-growth portable market niches.

Commercial & Industrial and Data Centre End-User Expansion

The Commercial & Industrial (C&I) and Data Centre end-user segments represent the most commercially significant near-term SOFC opportunity. C&I facilities, particularly those with combined heat and power (CHP) requirements such as hospitals, universities, and large manufacturing plants, can achieve total system efficiencies above 85% when utilizing SOFC waste heat for thermal applications, delivering compelling payback periods in energy-intensive operations.

The U.S. DOE's Combined Heat and Power (CHP) Partnership identifies fuel cells as the preferred CHP technology for new commercial installations above 250 kW. For data centers, Bloom Energy has installed over 1 GW of SOFC capacity globally, with projects operational at Samsung, Apple, and AT&T facilities. As hyperscale data center operators commit to 24/7 carbon-free energy targets, a standard increasingly set by Google and Microsoft, SOFC systems with hydrogen fuel capability will become strategically essential to meeting these commitments.

Category-wise Analysis

Structure Insights

The planar SOFC structure is the dominant architecture, representing approximately 72% of total market revenue in 2026. Planar SOFCs offer superior power density compared to tubular designs, with state-of-the-art planar cells achieving power densities above 1.5 W/cm² and are more amenable to compact stack assembly and cost-effective high-volume manufacturing through tape-casting and screen-printing fabrication techniques.

Market leaders including Bloom Energy, Ceres Power, SOLIDpower, and Elcogen all utilize planar cell architectures in their commercial product lines. Ceres Power's SteelCell technology, a proprietary planar SOFC design operable at intermediate temperatures of 500-620°C, has attracted licensing partnerships with Bosch, Weichai Power, and MHPS), reflecting industry confidence in the planar architecture's scalability and manufacturing cost reduction potential.

Application Insights

The Stationary application segment dominates the global SOFC market, accounting for approximately 79% of total market share in 2026. Stationary SOFC systems, deployed for distributed power generation, combined heat and power, and backup power in commercial, industrial, and utility settings, represent the most commercially mature application vertical. Bloom Energy's SureSource platform and Mitsubishi Heavy Industries' MEGAMIE SOFC system have established strong reference installations across the U.S., Japan, and South Korea.

Japan's ENE-FARM programme, the world's largest residential fuel cell deployment initiative supported by the Ministry of Economy, Trade and Industry (METI), has installed over 500,000 residential SOFC units as of 2024, demonstrating the technology's commercial scalability in stationary settings. Portable applications are the fastest-growing segment at a projected CAGR of 34%, driven by military procurement and emergency power demand.

End-user Insights

The commercial & industrial (C&I) is the leading end-use category for SOFC systems, accounting for approximately 48% of total global market revenues in 2026. Large C&I facilities with significant baseload electricity and thermal energy demand, including data centers, hospitals, hotels, universities, and chemical plants, represent the highest-value deployment targets for multi-hundred-kilowatt to megawatt-scale SOFC installations.

The economics are compelling: SOFC-based CHP systems can achieve total fuel utilization efficiencies above 85%, compared to grid electricity generation efficiencies of approximately 33-40% for conventional fossil-fuel power plants as reported by the U.S. EIA. The Data Centre sub-segment is the fastest-growing end-user category, with hyperscale operator procurement accelerating on the back of AI workload growth and corporate 24/7 carbon-free energy commitments.

Regional Analysis

North America Solid Oxide Fuel Cell Market Trends and Insights

North America leads the global SOFC market with approximately 35% of total revenue share in 2026. The region's leadership is anchored by strong policy support from the U.S. Inflation Reduction Act, the DOE's Hydrogen Shot initiative targeting clean hydrogen costs below US$ 1/kg by 2031), and robust private sector investment led by Bloom Energy and FuelCell Energy. Data center and C&I SOFC deployments are accelerating rapidly.

U.S. Solid Oxide Fuel Cell Market Size

The U.S. accounts for approximately 90-92% of North American SOFC revenues, supported by federal clean energy incentives, including the IRA's 30% investment tax credit for fuel cell systems, and the world's most active data centre SOFC deployment market. Bloom Energy alone has deployed over 1 GW of SOFC capacity in the U.S., with major customers including AT&T, Apple, and multiple utility operators.

Europe Solid Oxide Fuel Cell Market Trends and Insights

Europe is the second-largest SOFC market, driven by the EU Hydrogen Strategy's target of 10 million tons of domestic renewable hydrogen production by 2030), Horizon Europe fuel cell R&D funding, and national programmes in Germany), U.K.), and Italy). The region has a strong SOFC technology development ecosystem, with companies including Ceres Power, SOLIDpower, Elcogen, and Convion headquarters operating in Europe.

Germany Solid Oxide Fuel Cell Market Size

Germany is the largest SOFC market in Europe, accounting for approximately 22-25% of European regional revenues. Germany's National Hydrogen Strategy, backed by €9 billion in public funding, and its large industrial base with high combined heat and power demand create a structurally supportive environment for SOFC deployment. SOLIDpower, with its BlueGEN SOFC micro-CHP units, has achieved notable commercial traction in German residential and small commercial installations.

U.K. Solid Oxide Fuel Cell Market Size

The U.K. accounts for approximately 16-18% of European SOFC revenues and hosts one of the world's most prominent SOFC technology developers, Ceres Power), whose SteelCell platform has attracted over £500 million in licensing and investment partnerships. The UK Hydrogen Strategy and the British Energy Security Strategy both identify fuel cells as a priority low-carbon technology, with Innovate UK funding supporting multiple SOFC commercialization programmes.

France Solid Oxide Fuel Cell Market Size

France contributes approximately 10-12% of European SOFC market revenues. The French National Hydrogen Plan, supported by €7 billion in public investment through 2030, prioritizes clean hydrogen production and fuel cell deployment across industrial and transport applications. France's large nuclear power base creates unique opportunities for clean hydrogen production via electrolysis, which can directly feed next-generation pure hydrogen SOFC deployments in C&I and data center applications.

Asia Pacific Solid Oxide Fuel Cell Market Trends and Insights

Asia Pacific is the fastest-growing SOFC regional market, propelled by Japan's world-leading residential SOFC deployment through the ENE-FARM programme, South Korea's fuel cell power plant expansion, and China's accelerating SOFC investment, with China's 14th Five-Year Plan explicitly targeting fuel cell technology development and Ningbo SOFCMAN Energy Technology emerging as a key domestic SOFC manufacturer. India and Southeast Asia represent emerging demand frontiers.

India Solid Oxide Fuel Cell Market Size

India is an emerging SOFC market, contributing approximately 5-7% of Asia Pacific regional revenues in 2026. India's National Green Hydrogen Mission, targeting 5 million tonnes of green hydrogen production annually by 2030 with INR 19,744 crore (approximately US$ 2.4 billion) in incentives, is creating foundational hydrogen infrastructure that will progressively enable commercial SOFC deployments in industrial and defence applications over the forecast period.

Japan Solid Oxide Fuel Cell Market Size

Japan is the world's most mature residential SOFC market, accounting for approximately 28-30% of Asia Pacific regional revenues. The ENE-FARM programme, jointly developed by KYOCERA, Panasonic, and AISIN Corporation with METI support, has deployed over 500,000 residential SOFC units to date. Japan's Green Growth Strategy targets net-zero by 2050), with fuel cells serving as a central pillar of its hydrogen society vision and substantial CHP deployment in industrial and commercial sectors.

Southeast Asia Solid Oxide Fuel Cell Market Size

Southeast Asia represents a nascent but high-potential SOFC market, contributing approximately 4-6% of Asia Pacific revenues in 2026. Rapid data centre expansion, particularly in Singapore, Malaysia, and Indonesia, combined with government commitments to clean energy transition and growing ASEAN hydrogen cooperation frameworks, is creating early commercial demand for SOFC-based power solutions. Singapore's Hydrogen Economy Development programme and Malaysia's Hydrogen Roadmap both identify fuel cells as a priority deployment technology.

Competitive Landscape

The global SOFC market is moderately consolidated at the technology leadership tier, with Bloom Energy, Mitsubishi Heavy Industries, Ceres Power, and KYOCERA Corporation commanding significant revenue share and IP portfolios. Strategic priorities include licensing-based business models, notably Ceres Power's platform-licensing approach with Bosch and Weichai, geographic expansion into the Asia Pacific, and stack cost reduction through advanced manufacturing.

Emerging players, including Elcogen, SOLIDpower, and Ningbo SOFCMAN, are scaling production capacity to compete in European and Asian markets. Long-duration energy storage integration and green hydrogen co-generation are emerging as next-generation business model frontiers.

Key Developments:

- In February 2025, Bloom Energy announced a strategic partnership with a major South Korean utility to deploy 500 MW of SOFC-based clean power capacity by 2030, representing one of the largest committed SOFC deployment contracts in the Asia Pacific region.

- In September 2024, Ceres Power completed a major technology licensing agreement with Bosch for SOFC stack manufacturing, targeting gigawatt-scale SOFC production in Europe by 2030 to serve the stationary power and data centre markets.

- In April 2023, Mitsubishi Heavy Industries commissioned its MEGAMIE 250 kW SOFC-MGT hybrid power generation system at a Japanese industrial facility, achieving electrical efficiency exceeding 65% and demonstrating the technology's readiness for large-scale C&I deployment.

Solid Oxide Fuel Cell Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 1.1 Billion |

| Current Market Value (2026) | US$ 3.3 Billion |

| Projected Market Value (2033) | US$ 18.8 Billion |

| CAGR (2026 - 2033) | 28.2% |

| Leading Region | North America, 35% market share (2026) |

| Dominant Category (Application) | Stationary, 79% market share (2026) |

| Top-ranking Category (Structure) | Planar, 72% market share (2026) |

| Incremental Opportunity | US$ 15.5 Billion (2026 - 2033) |

Companies Covered in Solid Oxide Fuel Cell Market

- Bloom Energy

- Siemens Energy

- Mitsubishi Heavy Industries

- AISIN Corporation

- KYOCERA Corporation

- Ceres Power

- FuelCell Energy

- General Electric

- Convion

- SOLIDpower

- Elcogen

- Atrex Energy

- Redox Power Systems

- NGK Spark Plug (Niterra)

- Ningbo SOFCMAN Energy Technology

Frequently Asked Questions

The global solid oxide fuel cell (SOFC) market is estimated to be valued at US$ 3.3 billion in 2026, growing from US$ 1.1 billion in 2020 to a historical CAGR of 19.8%. The market is forecast to reach US$ 18.8 billion by 2033.

The primary demand drivers are global net-zero energy policy commitments, supported by over US$ 9.5 billion in U.S. clean hydrogen investment under the Bipartisan Infrastructure Law and €470 billion under REPowerEU, the rapid growth of data center power demand projected to reach 1,000 TWh by 2026 per the IEA), and Japan's ENE-FARM programme demonstrating SOFC commercial scalability with over 500,000 residential deployments.

North America leads with approximately 35% of global SOFC market share in 2026). The U.S. accounts for over 90% of regional revenues, anchored by Bloom Energy's 1+ GW of installed SOFC capacity, strong IRA investment tax credit incentives for fuel cell installations, and robust data center and C&I sector demand for decarbonized, highly reliable distributed power generation solutions.

The most significant commercial opportunities are in data center SOFC deployments, where Google, Microsoft, and Amazon's 24/7 carbon-free energy commitments are driving demand, and in portable SOFC systems for military and emergency power applications growing at a CAGR of 34%).

The leading companies include Bloom Energy, Mitsubishi Heavy Industries, Ceres Power, KYOCERA Corporation, AISIN Corporation, Siemens Energy, FuelCell Energy, SOLIDpower, Elcogen, and Ningbo SOFCMAN Energy Technology.