- Energy Storage Solutions

- Portable Power Stations Market

Portable Power Stations Market Size, Share, and Growth Forecast 2026 - 2033

Portable Power Station Market by Battery Type (Lead Acid, Lithium Ion), Application (Emergency Power, Off-grid), Capacity Range (2,000 Wh – 2,500 Wh, 2,501 Wh – 3,000 Wh, 3,001 Wh – 5,000 Wh, Above 5,000 Wh), Sales Channel (Electrical Equipment Retailers, Big Box Retailers, Direct Sales, E-commerce), and Regional Analysis, 2026 - 2033

Portable Power Stations Market Size and Trend Analysis

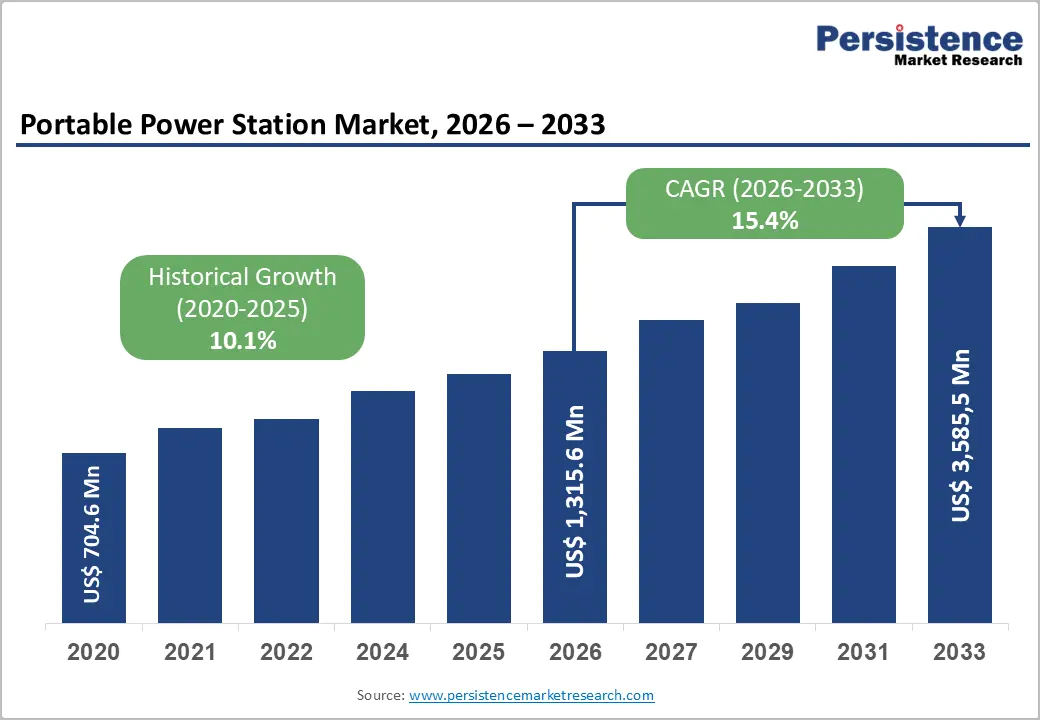

The global portable power stations market size is expected to be valued at US$ 1,140.0 million in 2026 and projected to reach US$ 3,107.0 million by 2033, growing at a CAGR of 15.4% between 2026 and 2033.

The market is being shaped by an unmistakable shift toward decentralized clean energy solutions, with consumers and small businesses moving away from fossil-fuel generators toward quieter lithium-based alternatives. Climate-linked outage frequency is a major catalyst; according to the U.S. Energy Information Administration (EIA), U.S. electricity customers experienced an average of 5.5 hours of power interruption in 2022, more than double the duration recorded a decade earlier. Coupled with a surge in outdoor recreation participation and the rapid normalization of remote work, demand for high-capacity, plug-and-play backup power continues to escalate across both developed and emerging economies.

Key Market Highlights

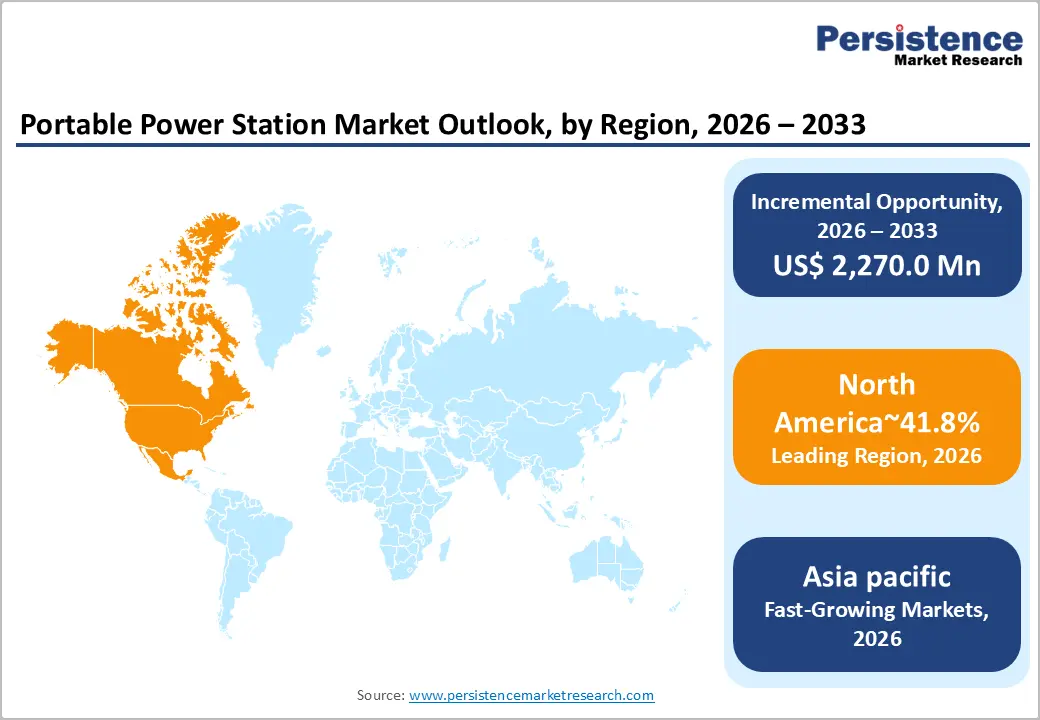

- Leading Region: North America dominates the global portable power station market with a 41.8% share in 2025, propelled by frequent weather-driven outages, deep RV and outdoor recreation culture, and high consumer purchasing power across the U.S. and Canada.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, expanding at a CAGR of approximately 17.2% during 2026–2033, supported by China's manufacturing leadership, Japan's disaster-resilience policy push, and rising adoption across India and Southeast Asia.

- Dominant Segment: Lithium-ion chemistry leads the global market with a commanding 91% share in 2025, owing to its superior energy density, longer cycle life of 3,000–6,000 cycles, lighter weight, and rapidly declining cost per kWh across global supply chains.

- Fastest Growing Segment: Lead acid is the fastest-growing chemistry segment at a CAGR of 9% during 2026–2033, driven by cost-sensitive emerging-market demand and continued use in budget-tier emergency-backup units across price-conscious regional markets.

- Key Market Opportunity: Government-backed disaster resilience procurement programs such as FEMA's BRIC and Japan's National Resilience Plan present multi-year institutional demand, complementing seasonal consumer purchases and offering stable, higher-margin revenue streams for certified manufacturers.

DRO Analysis

Drivers - Heightened Frequency of Climate-Driven Power Outages Anchoring Backup Energy Demand

Severe weather events are reshaping how households and businesses approach energy resilience. Data from the National Oceanic and Atmospheric Administration (NOAA) confirmed that the United States alone experienced 27 separate billion-dollar weather and climate disasters in 2024, the second-highest annual count on record.

The U.S. Department of Energy further reports that weather-related outages cost the American economy between US$ 25 billion and US$ 70 billion annually. With grid reliability under strain from hurricanes, wildfires, and ice storms, portable power stations have evolved from a niche outdoor accessory into a household preparedness essential. This consumer behavioral shift, supported by lower battery costs and silent operation, is meaningfully expanding the addressable buyer base for compact battery energy storage systems.

Falling Lithium-Ion Battery Prices Improving Product Affordability

Cost compression in battery cells has been the single most consequential supply-side enabler for this market. According to BloombergNEF, the volume-weighted average price of lithium-ion battery packs fell to US$ 115 per kWh in 2024, marking a 20% year-on-year decline and reaching the lowest level since the index began tracking.

Lithium iron phosphate (LFP) cell prices in particular dropped below US$ 80 per kWh, enabling manufacturers such as EcoFlow, BLUETTI, and Jackery to release units in the 2 kWh–5 kWh segment at consumer-friendly price points. This affordability transition is broadening adoption beyond early adopters into mainstream retail, particularly through e-commerce platforms operated by Amazon and large-format retailers.

Restraints - Stringent Lithium Battery Air-Transport Regulations Limiting Cross-Border Logistics

Air-cargo restrictions remain a notable bottleneck for global brands managing international fulfillment. The International Civil Aviation Organization (ICAO) and International Air Transport Association (IATA) classify lithium-ion units above 100 Wh as Class 9 Dangerous Goods, with cells above 160 Wh prohibited on passenger aircraft entirely.

Since most portable power stations exceed 1,000 Wh, brands rely on slower and costlier ocean freight, lengthening replenishment cycles and inflating landed costs. Post-2024 amendments to IATA's 66th Edition Dangerous Goods Regulations introduced stricter state-of-charge caps for cargo shipment, complicating warehousing and last-mile distribution for manufacturers servicing emergency-response and recreational markets.

Fire Safety Concerns and Product Recalls Eroding Consumer Trust

Battery thermal-runaway incidents continue to weigh on consumer confidence, particularly in the higher-capacity segment. The U.S. Consumer Product Safety Commission (CPSC) documented over 25,000 incidents linked to lithium-ion batteries across consumer products between 2018 and 2023, resulting in multiple fatalities and substantial property damage.

High-profile recalls, including a 2023 recall affecting 22,800 portable power station units in the U.S. due to overheating risks, have prompted greater regulatory scrutiny. Insurance providers in some jurisdictions are also restricting coverage for indoor lithium storage, which directly affects the residential emergency power segment and pressures manufacturers to invest more heavily in UL 2743 and IEC 62619 certifications.

Opportunities - Off-Grid Camping and Overlanding Lifestyle Driving Premium-Tier Demand

The outdoor recreation economy presents a compelling avenue for premium portable power station sales. According to the Outdoor Industry Association (OIA), 76.8 million Americans participated in camping in 2023, the highest figure ever recorded, while the RV Industry Association (RVIA) reported that more than 11.2 million U.S. households own a recreational vehicle.

Within this cohort, off-grid "boondocking" and overlanding subcultures are driving demand for units in the 3,001 Wh–5,000 Wh range, capable of running 12V refrigerators, induction cooktops, and CPAP machines simultaneously. Brands like Jackery, Goal Zero, and EcoFlow are responding with solar-bundled kits, expandable battery architectures, and IP-rated rugged housings. This experiential-spending tailwind is also visible in adjacent verticals such as the solar generator market, where overlapping consumer profiles are accelerating bundled-product adoption.

Government-Backed Disaster Resilience Programs Expanding Institutional Procurement

Public-sector procurement is emerging as a meaningful demand pillar beyond consumer retail. Following the Inflation Reduction Act (IRA) in the U.S., the Federal Emergency Management Agency (FEMA) expanded its Building Resilient Infrastructure and Communities (BRIC) program with annual allocations exceeding US$ 1 billion for community-level resilience hardware, which includes portable battery backup systems for shelters, clinics, and first-responder vehicles.

Japan's Ministry of Economy, Trade and Industry (METI) has similarly subsidized lithium-based emergency storage through the National Resilience Plan following recurring typhoon damage. These institutional channels favor higher-margin, certified-grade products and create multi-year procurement contracts, offering manufacturers stable revenue streams that complement seasonal consumer demand patterns.

Category-wise Analysis

Capacity (Battery Chemistry) Insights

The lithium-ion segment commands an estimated 91% market share in 2025, dominating the global portable power station landscape. This leadership stems from lithium-ion's superior energy density, longer cycle life, and dramatically lighter weight compared to lead acid alternatives. Within lithium-ion, lithium iron phosphate (LFP) chemistry has captured significant traction due to its thermal stability and a typical cycle life of 3,000–6,000 cycles, often exceeding 10 years of usable lifespan as validated by U.S. Department of Energy studies.

Major manufacturers, including EcoFlow, BLUETTI, Jackery, and Anker, have transitioned nearly their entire mid-to-high-capacity portfolio to LFP cells, reinforcing the segment's commanding position. Additionally, lithium-ion units enable rapid charging speeds, with leading models achieving 80% state-of-charge in under one hour, further widening the performance gap.

Application Insights

The emergency power segment leads with approximately 62% market share in 2025, reflecting the role of portable power stations as critical residential and commercial backup infrastructure. Within this segment, residential applications dominate as homeowners seek alternatives to noisy, fuel-dependent generators.

The U.S. Energy Information Administration (EIA) reported that the average annual outage duration for U.S. customers exceeded 5.5 hours in 2022, prompting widespread household adoption. Furthermore, data from the North American Electric Reliability Corporation (NERC) indicates that nearly 70% of major outages over the past decade were weather-related, particularly impacting suburban residential zones. Commercial sub-segments such as small clinics, food retailers, and remote field offices are also embracing these units as part of broader business-continuity planning, especially in regions with aging grid infrastructure.

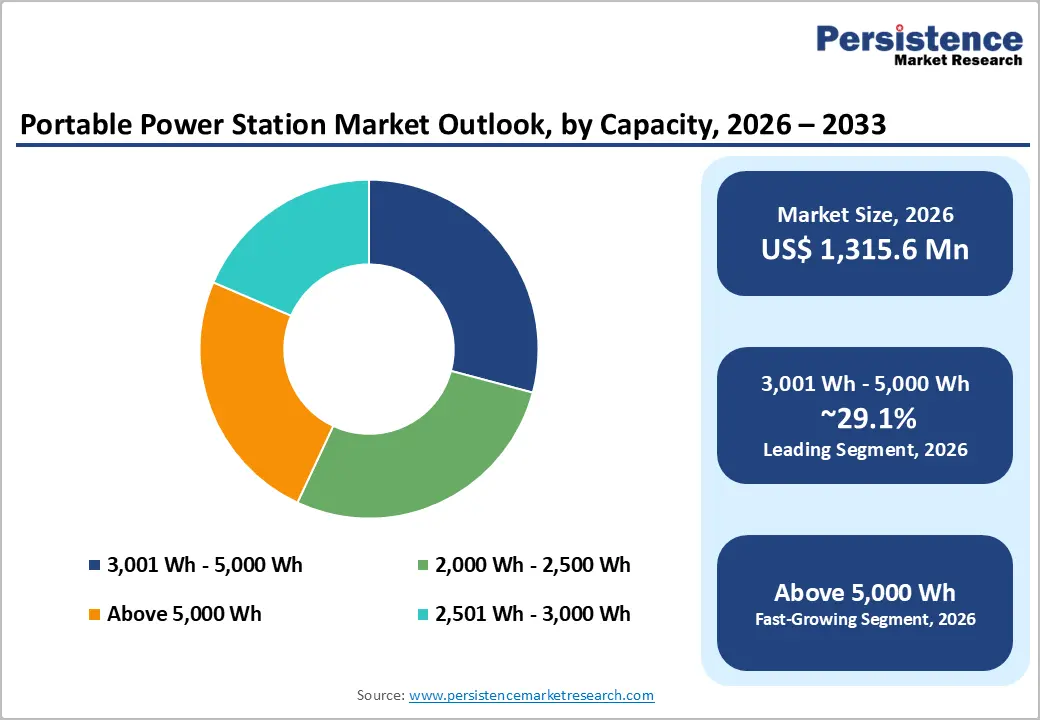

Capacity Range Insights

The 2,001 Wh–2,500 Wh range holds the leading position with approximately 38% market share in 2025, reflecting the sweet spot between portability and meaningful runtime. This capacity tier is large enough to power essential household loads such as refrigerators, routers, lighting, and medical devices for 8 to 12 hours, while remaining transportable by a single user without mechanical assistance.

Best-selling products, including the EcoFlow DELTA 2 Max, Jackery Explorer 2000 Plus, and BLUETTI AC200L all sit within this band. According to product-launch data from Consumer Electronics Show (CES) 2024 and 2025, more than 40% of new portable power station SKUs introduced by leading brands fell into this capacity bracket, validating its centrality to mainstream consumer demand and confirming its standing as the most commercially viable segment.

Sales Channels Insights

The e-commerce channel commands an estimated 54% market share in 2025, decisively outpacing physical retail formats. This dominance reflects the digital-native purchasing patterns of the early-adopter demographic and the inherent suitability of portable power stations to online merchandising, which depends heavily on detailed specifications, video demonstrations, and peer reviews.

Amazon alone hosts thousands of SKUs from leading brands, and direct-to-consumer brand websites operated by EcoFlow, BLUETTI, and Jackery routinely report e-commerce contributions of 60–70% of their global revenue. Crowdfunding platforms such as Indiegogo and Kickstarter also serve as launch channels for innovation-led releases, exemplified by the BLUETTI Apex 300 debut in May 2025. The shift is reinforced by Amazon Prime Day and Black Friday seasonality, which collectively account for a substantial share of annual sell-through volume.

Regional Insights

North America Portable Power Station Market Trends and Insights

North America stands as the largest regional market, holding a commanding 41.8% share in 2025, supported by frequent climate-related grid disturbances, a deep RV and outdoor recreation culture, and high consumer purchasing power. Adoption is accelerating across both home-backup and recreational use cases, with strong direct-to-consumer e-commerce penetration. Wildfire seasons in the West and hurricane exposure along the Gulf and East Coasts continue to reinforce structural demand.

U.S. Portable Power Station Market Size

The U.S. portable power station market reached approximately US$ 454.0 million in 2025, anchored by California's Public Safety Power Shutoff (PSPS) events and Texas's recurring grid stress following the 2021 Winter Storm Uri episode. The California Public Utilities Commission has documented PSPS events affecting over 2 million customers across multiple wildfire seasons, directly driving household adoption.

Federal incentives under IRA Section 25D for residential clean-energy property and aggressive seasonal e-commerce promotions through Amazon further reinforce U.S. leadership. Strategic donations such as BLUETTI's January 2025 partnership with the Los Angeles Fire Department also strengthen brand equity within the disaster-response category.

Europe Portable Power Station Market Trends and Insights

Europe holds a 23.5% share in 2025, with adoption driven by energy security concerns following the 2022 European energy crisis and rising consumer interest in solar-paired storage. Germany, the U.K., and France lead consumption, while Spain emerges as the fastest-growing country in the region. Stringent CE and IEC 62619 certification requirements favour established global brands, and balcony-solar adoption is creating cross-sell pathways into portable battery systems.

Germany Portable Power Station Market Size

Germany's portable power station market reached approximately US$ 70.5 million in 2025, supported by the country's record-breaking balcony solar (Balkonkraftwerk) adoption, which surpassed 780,000 installed units by mid-2024 according to the German Federal Network Agency (Bundesnetzagentur). Households increasingly pair these systems with portable batteries to maximize self-consumption.

Camping culture remains another structural pillar, with the German Camping Industry Association (CIVD) reporting more than 42 million overnight camping stays in 2023, sustaining demand for mid-to-large capacity units across both emergency and recreational use cases.

U.K. Portable Power Station Market Size

The U.K. market reached approximately US$ 56.4 million in 2025, accounting for around 21% of European demand. Drivers include rising electricity prices, with Ofgem's energy price cap remaining elevated through 2024–2025, alongside expanding caravan and motorhome ownership tracked by the National Caravan Council (NCC). Households are increasingly investing in compact battery backup as a hedge against winter peak-demand events and as a complement to rooftop solar installations under the Smart Export Guarantee scheme.

France Portable Power Station Market Size

France contributed approximately US$ 49.8 million in 2025, representing close to 18.5% of the European market. Growth is propelled by the country's vibrant outdoor and camping economy France remains the most-visited camping destination in Europe according to Eurostat, recording over 125 million overnight stays in 2023. Wildfire incidence in southern regions and rural electrification gaps in mountainous areas additionally support emergency-backup demand, with brands such as EcoFlow and Jackery expanding French-language e-commerce operations.

Spain represents the fastest-growing European market with an 8.7% country-level share in 2025, propelled by aggressive solar self-consumption regulation under Royal Decree 244/2019 and surging recreational vehicle registrations.

Asia Pacific Portable Power Station Market Trends and Insights

Asia Pacific holds 21.2% share in 2025, anchored by China's manufacturing dominance and rising domestic adoption. The region serves as the global production hub for lithium cells and finished portable power stations, with Japan, South Korea, and Australia representing the largest demand-side markets. Frequent typhoons, earthquakes, and grid expansion gaps in Southeast Asia continue to strengthen the regional growth profile.

China Portable Power Station Market Size

China's portable power station market reached approximately US$ 93.0 million in 2025, supported by the country's unmatched lithium battery supply chain. According to the China Association of Automobile Manufacturers (CAAM) and China Industrial Association of Power Sources (CIAPS), China accounts for over 75% of global lithium-ion cell production.

Domestic brands, including EcoFlow (Shenzhen-headquartered), BLUETTI, and Jackery, leverage this ecosystem for cost-competitive output. Domestic demand is also rising as outdoor camping participation surged following the post-pandemic reopening, with the China Tourism Academy reporting more than 400 million camping-related trips in 2023.

India Portable Power Station Market Size

India's market reached approximately US$ 23.0 million in 2025, accounting for nearly 10% of Asia Pacific demand. According to the Central Electricity Authority of India (CEA), average annual outage duration in tier-2 and tier-3 cities still exceeds 40 hours, sustaining structural demand for backup systems. Programs under the Pradhan Mantri Surya Ghar: Muft Bijli Yojana rooftop solar scheme are creating supplementary demand for portable battery solutions, while domestic e-commerce penetration through Flipkart and Amazon India is widening accessibility.

Japan Portable Power Station Market Size

Japan contributed approximately US$ 57.3 million in 2025, representing nearly 23% of regional demand. The Japan Meteorological Agency (JMA) records typhoons annually, with the 2024 Typhoon Shanshan causing widespread outages, reinforcing public investment in disaster preparedness. Subsidies from the Ministry of Economy, Trade and Industry (METI) under the National Resilience Plan have institutionalized portable battery adoption among municipalities, schools, and elderly-care facilities, while domestic players such as JVCKENWOOD and EcoFlow Japan dominate the consumer retail space.

Competitive Landscape

The global portable power station market exhibits a moderately fragmented structure, with the top five players collectively accounting for an estimated 55–60% of global revenue. EcoFlow, BLUETTI, Jackery, Anker (Goal Zero), and DJI lead through aggressive R&D, modular battery architectures, and direct-to-consumer e-commerce models. Key differentiation centers on capacity scalability, ultra-fast charging, 0ms UPS functionality, and proprietary ecosystem integrations such as EcoFlow's X-Core 3.0 and BLUETTI's TurboBoost platforms. Emerging trends include crowdfunding-led product launches via Indiegogo and Kickstarter, partnerships with disaster-response agencies, and bundling of solar panels for full off-grid kits to capture wallet share.

Key Market Developments

- In July 2024, Jackery Inc company announced the launch of its Explorer 1000 Plus and Explorer 600 Plus portable power stations in Australia, featuring enhanced capacity (up to 1.26 kWh expandable to 5 kWh), lithium iron phosphate (LFP) battery technology, solar charging compatibility, and multi-output versatility, strengthening its position in the portable power station market by targeting outdoor, residential backup, and off-grid applications.

- In September 2025, Bluetti, EcoFlo, and At the RE+ 2025 energy storage conference, the companies unveiled next-generation battery innovations, including Bluetti’s Pioneer Na, the world’s first sodium-ion portable power station designed for enhanced safety and extreme-temperature performance, along with new application-specific systems targeting RV, residential, and backup use cases, highlighting ongoing technological advancements and product diversification in the portable power station market.

Global Portable Power Station Market - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 640.0 million |

|

Current Market Value (2026) |

US$ 1,140.0 million |

|

Projected Market Value (2033) |

US$ 3,107.0 million |

|

CAGR (2026-2033) |

15.4% |

|

Leading Region |

North America, 41.8% |

|

Dominant Battery Type |

Lithium Ion, 91% market share |

|

Top-ranking Application |

Emergency Power, 62% market share |

|

Incremental Opportunity |

US$ 1,967.0 million |

Companies Covered in Portable Power Stations Market

- Jackery Inc.

- Anker Innovations Co., Ltd.

- PowerOak Technology Co., Ltd. (Bluetti Brand)

- SZ DJI Technology Co., Ltd.

- EcoFlow Technology Inc.

- Goal Zero LLC

- Shenzhen CTECHI Technology Co., Ltd.

- Pisen Electronic Co., Ltd.

- OUPES Technology Co., Ltd.

- GRECELL Technology

Frequently Asked Questions

The global portable power station market is expected to be valued at US$ 1,140.0 million in 2026 and projected to reach US$ 3,107.0 million by 2033, expanding at a CAGR of 15.4% during the forecast period.

Demand is driven by climate-related power outages, with the U.S. EIA reporting an average annual outage duration of 5.5 hours, alongside a 20% drop in lithium-ion battery pack prices to US$ 115/kWh in 2024 per BloombergNEF.

North America leads the global market with a 41.8% share in 2025, driven by frequent extreme-weather outages, strong RV and outdoor recreation culture, deep e-commerce penetration, and federal incentives under the Inflation Reduction Act.

Government-backed disaster resilience procurement, including FEMA's BRIC program with over US$ 1 billion annually and Japan's METI National Resilience Plan, is creating stable institutional demand beyond seasonal consumer purchases for certified manufacturers.

Key players include BLUETTI Power Inc., EcoFlow Inc., Jackery Inc., DJI, Anker Innovations (Goal Zero), OUPES, VTOMAN Technology, Generark Energy, Lion Energy LLC, Westinghouse Electric Corporation, and JVCKENWOOD Corporation, competing through R&D, modular architectures, and e-commerce-led distribution.