- Energy Storage Solutions

- Battery Swapping Charging Infrastructure Market

Battery Swapping Charging Infrastructure Market Size, Share, and Growth Forecast 2026 - 2033

Battery Swapping Charging Infrastructure Market by Vehicle Type (2-Wheelers, 3-Wheelers, Passenger Vehicles, Commercial Vehicles), Service Type (Subscription, Pay-per-Use, Battery-as-a-Service (BaaS)), Battery Type (Lithium-Ion Batteries, Solid-State Batteries), Application (Passenger Transportation, Commercial Transportation, Shared Mobility), and Regional Analysis, 2026 - 2033

Battery Swapping Charging Infrastructure Market Analysis

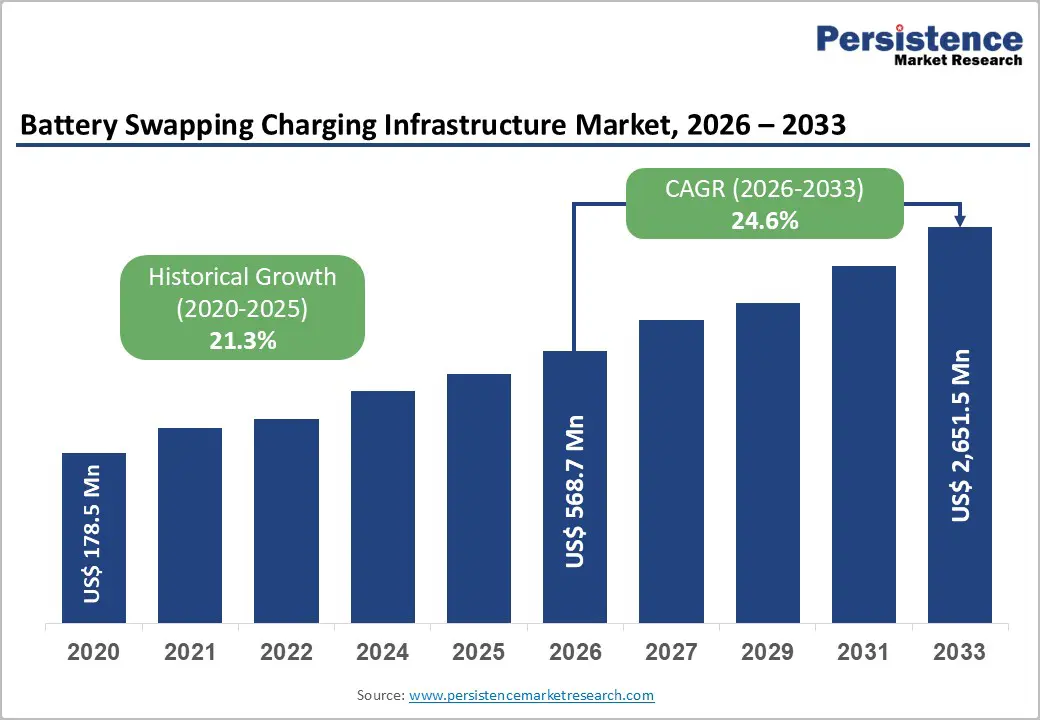

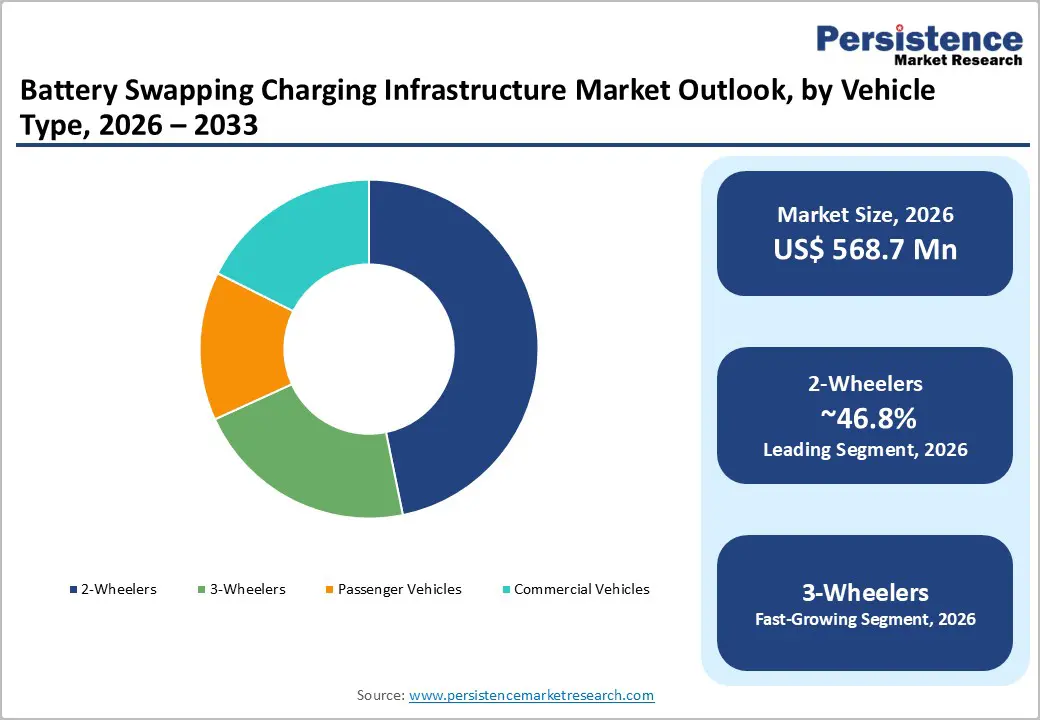

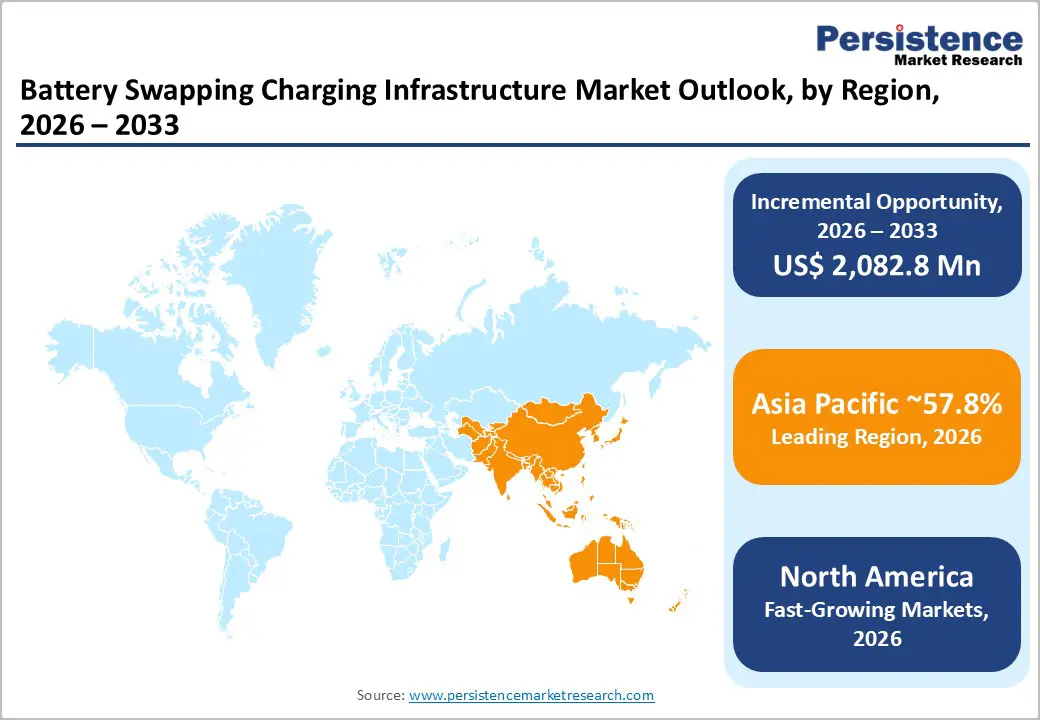

The global battery swapping charging infrastructure market size is expected to be valued at US$ 568.7 million in 2026 and projected to reach US$ 2,651.5 million by 2033, growing at a CAGR of 24.6% between 2026 and 2033.

Government-backed swapping policies in India, China, and parts of Southeast Asia, alongside the strategic decoupling of battery ownership from the vehicle through Battery-as-a-Service models, are converting urban delivery, ride-hailing, and last-mile mobility ecosystems into anchor demand pools. Falling lithium-ion cell prices and standardisation efforts further compress the total cost of ownership.

Key Market Highlights

- Leading Region: Asia Pacific dominates the global Battery Swapping Charging Infrastructure market with a 57.8% share in 2025, propelled by China's extensive swap-network buildout and India's two- and three-wheeler swap economy.

- Fast-Growing Market: South Asia, led by India, is the fastest-growing regional market, expanding at a 28% CAGR through 2033, anchored by NITI Aayog's Battery Swapping Policy and three-wheeler fleet electrification.

- Dominant Vehicle Type: The 2-Wheeler vehicle category leads with 47% market share in 2025, driven by gig-economy delivery riders and the structural fit of lightweight, swap-friendly batteries in dense urban Asian markets.

- Fast-Growing Vehicle Type: The 3-Wheeler category is forecast to expand at a 23% CAGR between 2026 and 2033, fuelled by commercial cargo and passenger-auto fleet electrification across India and Southeast Asia.

- Key Opportunity: Heavy-duty trucking swap networks, validated by CATL's QIJI Energy rollout, represent a high-value frontier as long-haul and mining operators displace diesel through standardised modular battery-swap architectures.

DRO Analysis

Drivers - Fleet Electrification Mandates and Last-Mile Delivery Economics

Public transport agencies and e-commerce fleet operators are anchoring infrastructure rollout because operational uptime is non-negotiable for them. According to the International Energy Agency (IEA) Global EV Outlook 2024, electric two- and three-wheeler stock surpassed 80 million units worldwide, with over 60% concentrated in Asia.

NITI Aayog's Battery Swapping Policy framework in India estimates that swapping cuts vehicle downtime by 80% versus plug-in charging, a decisive factor for gig-economy riders averaging 120 km daily. Logistics majors such as Amazon, Flipkart, and Meituan have integrated swap-enabled fleets into delivery operations, validating unit economics. Similar fleet-led traction in Indonesia and Vietnam is creating self-reinforcing infrastructure demand around urban delivery corridors.

Battery-as-a-Service Decouples Vehicle Affordability from Battery Cost

BaaS lowers the upfront price of an electric vehicle by 30-40% because the battery, which represents the costliest component, is leased rather than purchased. NIO Inc. has demonstrated commercial scalability with more than 2,400 Power Swap Stations operational across China as of 2024, completing over 40 million cumulative swaps.

The model is being replicated by Gogoro Inc. in Taiwan, where its network now serves over 600,000 subscribers through 12,000+ GoStations, executing roughly 400,000 swaps per day. The China Electricity Council notes that swap-enabled commercial vehicles can amortise battery costs across multiple users, generating utilisation rates two to three times higher than privately owned packs and substantially improving project IRR for infrastructure operators.

Restraints - Absence of Universal Battery Standardisation

Battery form factors, voltage profiles, and connector geometries differ widely across original equipment manufacturers, fragmenting the addressable network for any single operator. The Society of Automotive Engineers (SAE) and IEC 62840 have proposed standardisation pathways, yet adoption remains voluntary, and dominant OEMs prefer proprietary architectures to lock in customers.

In China, only about 15% of swap stations support cross-brand compatibility, according to the China EV100 Forum. This forces network operators to either commit to a single OEM ecosystem or bear the capex of multi-format bays, eroding station economics and slowing the geographic expansion that scale-driven business models require.

High Upfront Capex and Real Estate Constraints

A single passenger-vehicle swap station typically requires US$ 400,000 to US$ 1.2 million in capital outlay, including robotics, multiple buffer batteries, fire-safety systems, and grid upgrades, per disclosures by NIO Inc. and Aulton New Energy. Urban land scarcity in Tokyo, Mumbai, and Jakarta further compresses available footprints, while utility interconnection waiting times of 6 to 18 months delay revenue ramp-up.

The Federal Energy Regulatory Commission (FERC) has also flagged distribution-network upgrade backlogs in parts of the United States, making site-level electrification timelines unpredictable for operators planning multi-city deployment.

Opportunities - Three-Wheeler Cargo Segment as the Highest-Velocity Growth Pocket

Three-wheelers represent the fastest-growing vehicle class within swap-enabled networks, projected to expand at a 23% CAGR through 2033. The Society of Manufacturers of Electric Vehicles (SMEV) reports that electric three-wheeler sales in India crossed 691,000 units in 2024, and over 55% of these are operated by commercial drivers covering 150-200 km daily, where swap economics meaningfully outperform overnight charging.

Operators such as SUN Mobility, Battery Smart, and Honda Power Pack Energy are aligning network density to last-mile logistics corridors. Similar dynamics are unfolding in the broader EV ecosystem, with the global Electric Vehicle Market absorbing investment commitments exceeding US$ 615 billion through 2030, providing capital tailwinds for adjacent swap-network buildouts.

Heavy-Duty Trucking and Mining Fleet Conversion

Heavy commercial vehicles are emerging as a high-value frontier because long-haul and mining operators cannot tolerate plug-in charging windows of 4-8 hours. CATL unveiled the QIJI Energy swap solution for heavy trucks in 2024, targeting standardised modular battery packs deployable across multiple OEMs.

The China Association of Automobile Manufacturers (CAAM) noted that swap-enabled heavy trucks accounted for nearly 48% of all electric heavy-truck registrations in China in 2024. In parallel, mining majors in Chile and Australia are piloting electric haul-truck swap stations to displace diesel consumption, with BHP and Rio Tinto committing multi-billion-dollar decarbonisation budgets that include battery-swap pilots, signalling a durable opportunity pool for operators with heavy-asset engineering capability.

Category-wise Analysis

Vehicle Type Insights

The 2-wheeler segment leads with approximately 47% market share in 2025, anchored by the structural fit between short-range urban commuting, lightweight removable batteries, and dense delivery-rider populations across India, Indonesia, Vietnam, and Taiwan.

The Federation of Automobile Dealers Associations (FADA) reported that electric two-wheeler retail sales in India crossed 1.14 million units in fiscal year 2024, with swap-enabled models capturing a meaningful share of the gig-economy fleet. Gogoro Inc. alone facilitates more than 400,000 swaps per day in Taiwan, validating the throughput economics of a 2-wheeler-first network. The convergence of low battery weight (typically 8-12 kg), affordable station capex, and rider willingness to pay per swap explains the segment's persistent dominance.

Service Type Insights

Battery-as-a-Service (BaaS) is the leading service model, accounting for an estimated 52% of the market in 2025. The model resonates because it removes battery ownership risk, hedges against cell-degradation uncertainty, and aligns operating costs with vehicle utilisation. NIO Inc.'s BaaS subscription has been adopted by over 70% of new NIO buyers in China, while Gogoro Inc. runs a recurring monthly subscription embedded in its swap network.

The Ministry of Heavy Industries in India has explicitly endorsed BaaS in its battery-swapping policy draft, recognising lifecycle-cost advantages. Pay-per-Use, while popular among occasional users, lacks the predictable cash-flow profile that infrastructure financiers prefer, leaving BaaS as the structurally favoured model for scalable network economics.

Application Insights

Commercial transportation is the leading application with around 49% market share in 2025, driven by fleet operators in last-mile logistics, food delivery, ride-hailing, and intra-city freight. The International Transport Forum (ITF) highlights that commercial vehicles travel 3-5 times more daily kilometres than private cars, making refuelling-time savings of swap stations financially compelling. Meituan and Ele.me in China operate combined fleets exceeding 6 million delivery riders, the majority utilising swap-enabled two-wheelers.

In parallel, three-wheeler aggregators in India, such as Mahindra Logistics and Zypp Electric, are deploying swap-tied fleets across more than 30 cities. Commercial demand is structurally stickier than retail demand because route economics dictate uptime, locking operators into recurring swap-network usage.

Regional Insights

North America Battery Swapping Charging Infrastructure Market Trends and Insights

North America holds a share of 13.7% in 2025, with market traction concentrated in commercial fleet pilots, mining-sector haul-truck conversion, and select urban micromobility programmes. The region's growth is constrained by entrenched plug-in charging infrastructure, but momentum is building around heavy-duty trucking corridors aligned with the U.S. Inflation Reduction Act clean-vehicle credits. Cross-border standardisation discussions with Canada under the U.S.-Canada EV Alliance are gradually de-risking multi-state network economics.

U.S. Battery Swapping Charging Infrastructure Market Size

The U.S. Battery Swapping Charging Infrastructure market is valued at US$ 454.0 Million in 2025, driven by mining-sector electrification commitments from Caterpillar Inc. and Komatsu, and federal funding under the Bipartisan Infrastructure Law allocating US$ 7.5 billion for EV infrastructure.

Pilot deployments by Ample Inc. in San Francisco and New York, alongside Stellantis fleet-vehicle swap programmes, anchor commercial demand. The U.S. Department of Transportation has cleared swap stations as eligible recipients under the NEVI Formula Program in select states.

Europe Battery Swapping Charging Infrastructure Market Trends and Insights

Europe is likely to register a share of 16.4% in 2026, propelled by the European Union Alternative Fuels Infrastructure Regulation (AFIR) and the Fit for 55 decarbonisation package. Demand is concentrated in commercial fleet corridors and last-mile delivery clusters across Germany, the United Kingdom, the Netherlands, and France. Standardisation under CEN-CENELEC and pilot deployments by Stellantis with Ample Inc. in Madrid are catalysing cross-border network design and unlocking institutional capital flows.

Germany Battery Swapping Charging Infrastructure Market Size

Germany’s market size is valued at US$18 million in 2026, supported by Volkswagen Group's strategic battery-swap evaluation for commercial vans and the Kraftfahrt-Bundesamt (KBA) registering more than 1.65 million electric vehicles in circulation. Federal incentives under Klimaschutzprogramm 2030 and pilots in Munich and Berlin for last-mile delivery operators provide a structural demand base, while the country's industrial logistics density makes commercial swap economics particularly attractive.

U.K. Battery Swapping Charging Infrastructure Market Size

The U.K. market is valued at US$ 10.9 Million in 2025, anchored by London-centric ride-hailing electrification under the Transport for London (TfL) Ultra-Low Emission Zone framework. The Office for Zero Emission Vehicles (OZEV) allocated more than GBP 950 million for charging infrastructure, of which a portion is being directed toward swap-pilot trials. Tevva Motors is advancing swap-enabled medium-duty trucks, and Uber's London electrification commitment provides a captive demand corridor for two- and three-wheel swap operators.

Asia Pacific Battery Swapping Charging Infrastructure Market Trends and Insights

Asia Pacific is poised to account for a dominant share of 57.8% in 2026, anchored by China's state-backed swap-network rollouts and India's policy-driven two- and three-wheeler swap economy. Regional growth is amplified by urbanisation, gig-economy fleets, and the manufacturing concentration of CATL, BYD, and Gogoro Inc. The MIIT in China has greenlit national swap-station standards, while ASEAN governments are piloting cross-border interoperability for two-wheelers.

China Battery Swapping Charging Infrastructure Market Size

China's market size is likely to be valued at US$167.5 million in 2026, driven by NIO Inc.'s 2,400+ Power Swap Stations, Aulton New Energy's 1,000+ taxi-focused stations, and CATL's QIJI Energy heavy-truck rollout. The Ministry of Industry and Information Technology (MIIT) has formalised swap-station construction codes, while subsidies under the New Energy Vehicle (NEV) policy continue funding both passenger-car and commercial-truck swap deployments across 30+ provincial cities.

India Battery Swapping Charging Infrastructure Market Size

India's market is valued at US$47 million in 2025, propelled by NITI Aayog's Battery Swapping Policy and the FAME-II scheme. Network operators SUN Mobility, Battery Smart, and Bounce Infinity collectively run more than 2,500 swap stations across 40+ cities, serving electric two- and three-wheeler fleets. The Society of Manufacturers of Electric Vehicles (SMEV) projects India's electric three-wheeler park exceeding 3 million units by 2027, providing a structural demand pipeline.

Competitive Landscape

The market is moderately fragmented with regional concentration: NIO Inc., Aulton New Energy, and CATL dominate China; Gogoro Inc. controls Taiwan and is exporting its model to ASEAN; SUN Mobility, Battery Smart, and Bounce Infinity lead India.

Competitive differentiation centres on battery standardisation depth, network density, robotics speed (sub-90-second swaps), and OEM partnerships. Vertical integration into cell manufacturing, exemplified by CATL and BYD, is emerging as a defensible moat. Subscription-based BaaS, fleet-tied long-term contracts, and joint ventures with energy utilities such as Sinopec and State Grid define the dominant business-model trends shaping market consolidation.

Key Developments:

- In March 2025, NIO Inc. and Contemporary Amperex Technology Co., Limited (CATL) signed a strategic partnership agreement to jointly develop one of the largest battery swapping networks for passenger electric vehicles in China. The collaboration includes unified battery swapping technical standards, shared swapping infrastructure, lifecycle battery management, and material recycling systems.

- In December 2024, Contemporary Amperex Technology Co., Limited (CATL) launched two standardised battery swapping models, #20 and #25, during its Choco-Swap ecosystem conference in Xiamen, China. Developed in collaboration with nearly 100 ecosystem partners, the initiative represents a major advancement in the standardisation of electric vehicle battery swapping infrastructure.

Battery Swapping Charging Infrastructure Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 178.5 Million |

| Current Market Value (2026) | US$ 568.7 Million |

| Projected Market Value (2033) | US$ 2,651.5 Million |

| CAGR (2026 - 2033) | 24.6% |

| Leading Region | Asia Pacific, 57.8% Market Share in 2025 |

| Dominant Vehicle Type | 2-Wheelers, 46.8% Market Share in 2025 |

| Top-ranking Service Type | Battery-as-a-Service (BaaS), 44.7% Market Share in 2025 |

| Incremental Opportunity (2026 - 2033) | US$ 2,082.8 Million |

Companies Covered in Battery Swapping Charging Infrastructure Market

- NIO Inc.

- Gogoro Inc.

- Leo Motors Inc.

- Yadea Technology Group Co., Ltd.

- SUN Mobility Private Ltd.

- BYD Co. Ltd.

- BattSwap Inc.

- Kwang Yang Motor Co. Ltd. (KYMCO)

- Panasonic Corp.

- Lithion Power Pvt. Ltd.

Frequently Asked Questions

The global Battery Swapping Charging Infrastructure market is projected to reach US$ 568.7 Million in 2026, advancing toward US$ 2,651.5 Million by 2033 at a 24.6% CAGR, supported by fleet electrification and BaaS adoption.

Fleet electrification mandates and gig-economy delivery economics are the primary drivers. Swapping reduces vehicle downtime by approximately 80% versus plug-in charging, a decisive factor for two- and three-wheeler commercial operators in Asia Pacific.

Asia Pacific leads with a 57.8% share in 2025, anchored by China's 2,400+ NIO Power Swap Stations, CATL's heavy-truck swap rollout, and India's policy-driven two- and three-wheeler swap network expansion.

The 3-Wheeler segment, expanding at a 23% CAGR, and heavy-duty trucking swap networks led by CATL's QIJI Energy platform represent the highest-growth opportunity pockets, alongside Battery-as-a-Service subscription monetisation models.

Leading players include NIO Inc., Gogoro Inc., Aulton New Energy, CATL, BYD Company Limited, SUN Mobility, Battery Smart, Bounce Infinity, Ample Inc., Honda Motor Co., Ltd., Stellantis N.V., and Tevva Motors Limited.