- Communication Infrastructure & Services

- Satellite Servicing Market

Satellite Servicing Market Size, Share, and Growth Forecast 2026 - 2033

Satellite Servicing Market by Orbit (Low Earth Orbit, Medium Earth Orbit), Service (Active Debris Removal and Orbit Adjustment), Satellite Type (Small Satellites, Medium Satellites), End-user, and Regional Analysis, 2026 - 2033

Satellite Servicing Market Size and Trends Analysis

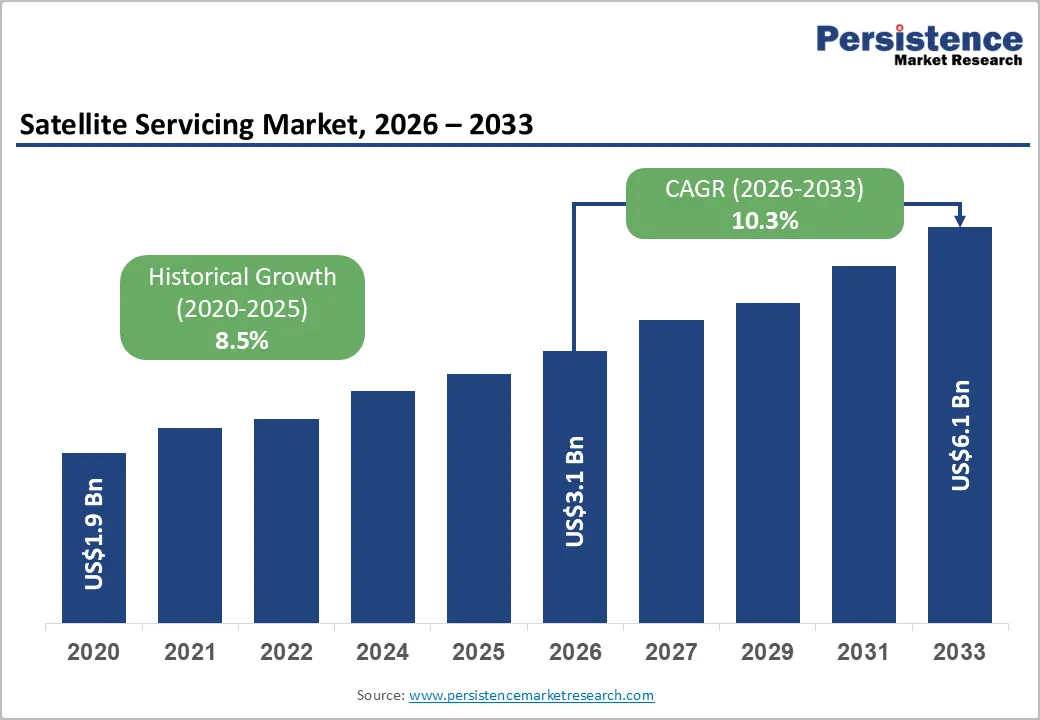

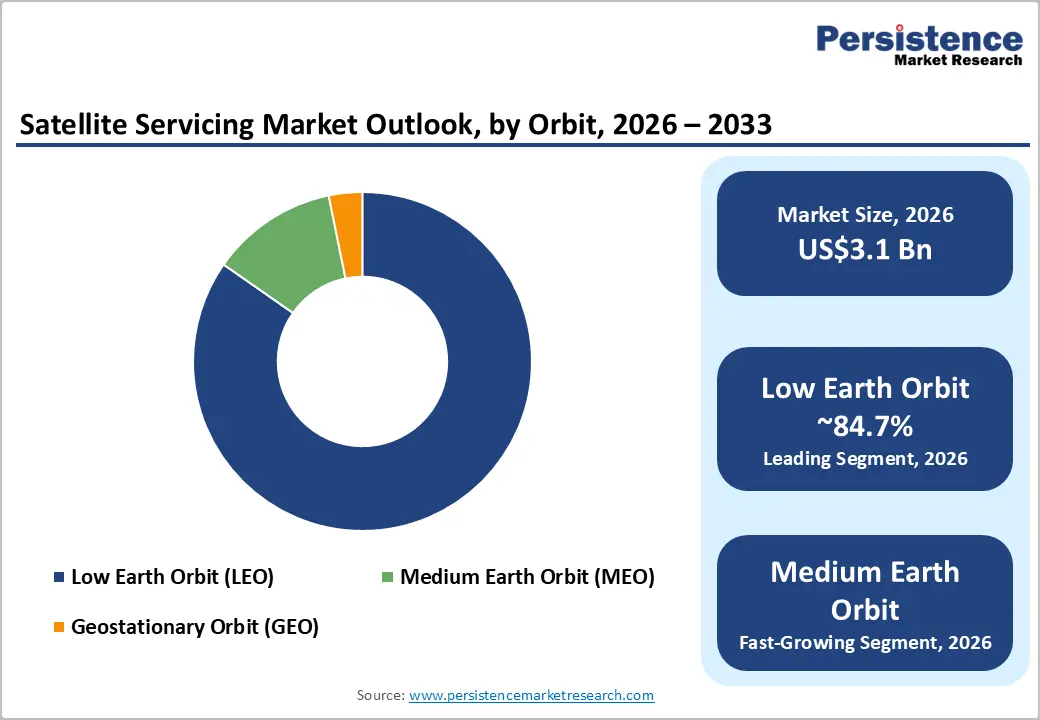

The global satellite servicing market size is likely to be valued at US$3.1 billion in 2026 and is expected to reach US$6.1 billion by 2033, growing at a CAGR of 10.3% during the forecast period from 2026 to 2033, driven by the steady rise in orbital congestion, the need to protect high-value space assets, and the shift toward sustainable space operations.

Successful demonstrations, including the Mission Extension Vehicle (MEV-1), which docked with an aging satellite to extend its usability, are validating the commercial viability of servicing models.

Key Industry Highlights:

- Upcoming Satellite Missions: The U.S. is preparing four satellite servicing missions in 2026 to demonstrate capabilities such as refueling, repair, inspection, and in-orbit maneuvering, mainly for military satellites. These missions are supported by various Department of Defense units but also involve commercial companies, indicating a shift toward public-private collaboration.

- Leading Orbit: Low Earth Orbit (LEO) is expected to account for nearly 84.7% of the market share in 2026, as it hosts dense satellite constellations that require frequent maintenance and orbital adjustments.

- Dominant Service: Robotic servicing, with approximately 45.8% share in 2026, as it enables precise and repeatable operations in space without human involvement, thereby reducing mission risk and cost.

- Leading Region: North America is predicted to surge with around 39.2% share in 2026, due to early in-orbit servicing missions and various government-backed programs that support commercial deployment.

- Fast-growing Region: Europe, owing to strict space sustainability norms and active debris removal initiatives backed by regional agencies.

DRO Analysis

Driver - Rising Demand for Operational Stability of Satellites

Satellite servicing is gaining popularity as operators look to maximize returns on existing assets rather than invest in costly new launches. Life-extension missions can add five or more years to a satellite’s operational timeline. This is important, as a single geostationary satellite launch can exceed US$100 million. In 2020, Northrop Grumman’s Mission Extension Vehicle (MEV-1) successfully docked with Intelsat 901, extending its life by five years.

It marked a commercial milestone in in-orbit servicing. Such missions reduce capital expenditure while ensuring continuity of services such as broadcasting and broadband. At present, there are more than 1,000 active satellites in geostationary orbit alone. Hence, even partial adoption of servicing solutions is estimated to create substantial cost efficiencies and operational stability for fleet operators.

Surging Focus on Orbital Sustainability and Debris Reduction

Surging concerns around space congestion are pushing governments and private players to prioritize sustainable orbital practices, thereby supporting demand for satellite servicing. As of 2024, the European Space Agency estimates over 36,500 debris objects larger than 10 cm orbiting Earth, posing collision risks to operational satellites. Servicing technologies such as refueling, repair, and controlled deorbiting help reduce the need to launch replacements and limit debris generation.

Astroscale’s ELSA-d mission, for instance, demonstrated active debris removal by safely capturing a simulated defunct satellite in orbit. Regulatory bodies are also tightening norms. The U.S. Federal Communications Commission (FCC) now mandates satellite deorbiting within five years post-mission, down from the earlier 25-year guideline. These developments are accelerating the integration of servicing capabilities into satellite lifecycle planning.

Restraint- Technical Complexity and High Risk in Autonomous In-orbit Operations

Satellite servicing faces a key limitation due to the extreme precision required for autonomous rendezvous and docking in space. Unlike controlled terrestrial environments, servicing missions must operate in microgravity with limited real-time human intervention, increasing the risk of failure. Even minor navigation errors can lead to mission loss or the creation of additional debris.

Defense Advanced Research Projects Agency’s (DARPA) Robotic Servicing of Geosynchronous Satellites (RSGS) program has already experienced delays. It is due to the complexity of developing reliable robotic systems for delicate operations, including refueling and repairs. Various prominent satellites were also not designed with servicing interfaces, making docking very challenging. These technical uncertainties increase mission costs and insurance risks, discouraging widespread adoption despite surging interest in satellite life-extension solutions.

Opportunity - Development of Shared Technical Standards to Enable Cross-servicing

Developing common servicing standards is expected to create new opportunities for key players during the forecast period. These standards are predicted to enable multiple satellites to be handled by different servicing vehicles. Currently, most satellites are not designed for interoperability, which hampers large-scale adoption of satellite servicing.

Industry initiatives, including the Consortium for Execution of Rendezvous and Servicing Operations (CONFERS), are addressing this gap. CONFERS has defined technical guidelines for docking interfaces, safety protocols, and mission coordination. Backed by DARPA, it has already released best-practice documents that companies are beginning to integrate into new satellite designs. This shift is predicted to create a standardized ecosystem, enabling service providers to expand operations across fleets.

Collaborations between Satellite Makers, Servicing Firms, and Government Bodies

Surging collaborations among satellite manufacturers, service providers, and government agencies are opening the door to advances in servicing architectures. Key players are now co-developing satellites with built-in servicing features such as refueling ports and modular components. Airbus and Northrop Grumman, for instance, have explored cooperative approaches to integrate life-extension capabilities into future satellite designs.

Space agencies, including NASA, are also partnering with private firms to test in-orbit assembly and repair technologies. These joint efforts reduce development risks, bolster testing cycles, and help establish shared infrastructure. These further help make satellite servicing more practical and scalable in the long term.

Category-wise Analysis

Orbit Insights

Low Earth Orbit (LEO) is estimated to dominate in 2026, with a market share of approximately 84.7%. This is attributed to its ability to host the largest and fastest-growing satellite population, mainly from mega-constellations. Companies such as SpaceX have deployed more than 5,000 Starlink satellites as of 2025, with thousands more planned. It is hence creating a dense operational environment that requires frequent maintenance, repositioning, and end-of-life handling. LEO satellites also face comparatively higher atmospheric drag, which raises the requirement for servicing interventions.

The Medium Earth Orbit (MEO) segment is expected to be the fastest-growing in the forecast period. This is owing to its important role in global navigation systems and secure communications. Constellations such as GPS and Galileo operate in MEO and are constantly being upgraded to support high accuracy. These satellites are expensive and strategically important, which makes life-extension, refueling, and repair services more attractive.

Service Insights

The robotic servicing segment is expected to account for nearly 45.8% of the market in 2026, as it enables highly controlled operations such as refueling, component replacement, and inspection without human presence in space. Missions, including NASA’s On-orbit Servicing, Assembly, and Manufacturing (OSAM-1), are designed to demonstrate robotic refueling of satellites not originally built for servicing. Robotic arms and autonomous navigation systems reduce mission risk while enabling reuse across different satellites.

The Active Debris Removal (ADR) and orbit adjustment segment is anticipated to exhibit steady growth in the foreseeable future. These have become essential services due to the increasing congestion in Earth’s orbit. Companies, including Astroscale, have successfully demonstrated capture technologies through missions such as ELSA-d, which tested the safe retrieval of defunct objects. Orbit adjustment services are equally important for avoiding collisions and maintaining optimal satellite positioning.

Regional Insights

North America Satellite Servicing Market Trends

With a share of nearly 39.2% in 2026, North America is projected to lead the global market. This is due to its mature space industry, where government funding and private innovation operate together. The region benefits from superior institutional backing and early deployment of servicing missions, giving it a first-mover advantage. Agencies and defense bodies actively fund in-orbit servicing programs, while private companies continuously test commercial models. The region is also supported by high investments in robotic servicing and debris removal technologies.

U.S. Satellite Servicing Market Trends

The U.S. dominates as it combines government programs with a powerful private space sector. Organizations such as NASA are actively developing in-orbit servicing technologies through programs, including OSAM. Defense agencies also fund servicing for strategic satellites. At the same time, companies such as SpaceX and Northrop Grumman boost real-world deployment of servicing missions. The U.S. further leads in terms of global launches, accounting for over 80% of launches in 2025. It is gradually creating a large installed base that requires maintenance and servicing.

Europe Satellite Servicing Market Trends

In 2026, Europe will likely account for a share of approximately 28.4%, spurred by its regulatory focus on space sustainability and coordinated regional programs. The region actively promotes debris mitigation and responsible satellite operations, which increases demand for servicing solutions.

Agencies such as the European Space Agency are funding projects related to life extension and debris removal. These agencies strive to comply with strict space traffic management policies. Europe’s collaborative approach across multiple countries also helps build shared infrastructure, making it a strong, policy-backed market.

U.K. Satellite Servicing Market Trends

The U.K. is a key market due to its focused investment in satellite servicing technologies and strong policy backing. The U.K. Space Agency supports research and development activities in in-orbit servicing and debris removal, positioning the country as a specialist hub in Europe. The U.K. is also investing in satellite manufacturing and the small-satellite industry, which will create future demand for servicing. Its strategy is less about expansion and more about building niche expertise in emerging servicing technologies.

Germany Satellite Servicing Market Trends

Germany is seeing steady growth driven by its superior engineering base and its involvement in Europe’s collaborative missions. The country contributes to satellite manufacturing, robotics, and space systems integration, which are important for servicing technologies. Germany-based firms often participate in ESA-led programs, focusing on precision engineering required for docking and repair missions. This consistent involvement in high-value components of the servicing chain is bolstering gradual but stable growth in the country.

Asia Pacific Satellite Servicing Market Trends

Asia Pacific is becoming a flourishing region due to several government-led investments in space capabilities. Countries such as China, India, and Japan are treating satellite servicing as strategic infrastructure rather than just a commercial service. The region has seen steady growth in satellite launches and national programs, contributing to global growth. With nearly 15,000 satellites in orbit and rising launch rates each year, demand for maintenance, refueling, and debris removal is growing rapidly.

The momentum is further supported by mission-level developments and policy direction. Indian Space Research Organization (ISRO) is working on the SPADEX mission to demonstrate autonomous docking, which is a key capability for future servicing operations. Similar developments show that the region is not only increasing the number of satellites but also building the technical foundation required for long-term servicing and space sustainability.

Japan Satellite Servicing Market Trends

Japan is advancing satellite servicing primarily through debris-removal and technology-demonstration missions. The space agency JAXA is actively working to capture and deorbit space debris, including missions targeting defunct satellites and rocket stages. These programs are supported by partnerships with private firms, positioning Japan as a leader in sustainable space operations. The country’s approach focuses on addressing congestion challenges rather than immediately broadening commercial services.

China Satellite Servicing Market Trends

China is experiencing steady growth driven by direct government investment in service technologies. Missions such as the Shijian-25 satellite are being developed to demonstrate in-orbit refueling and life-extension capabilities. Unlike market-driven regions, China’s progress is mainly state-controlled, ensuring continuous funding and fast deployment cycles. This approach allows the country to rapidly build indigenous servicing capabilities and reduce dependence on external technologies, making it a fast-evolving player.

Competitive Landscape

The global satellite servicing market is a mix of large aerospace companies and emerging start-ups competing on different strengths. Established firms such as Northrop Grumman and Maxar Technologies lead with proven missions and multiple government contracts. New entrants, including Starfish Space and Orbit Fab, are introducing flexible and low-cost servicing models. This creates a layered market where incumbents focus on high-value missions and start-ups target flexible services such as refueling and autonomous servicing.

Instead of direct head-to-head competition, companies are positioning themselves in specific service niches. For instance, Astroscale focuses on debris removal and sustainability missions, while Northrop Grumman leads in life-extension vehicles. This segmentation allows multiple players to rise simultaneously, as demand spans inspection, repair, refueling, and disposal.

Key Industry Developments:

- In March 2026, Katalyst Space Technologies, headquartered in Arizona, signed a contract with Arianespace to launch its NEXUS-1 satellite servicing spacecraft aboard an Ariane 6 in 2027. The spacecraft is capable of performing various duties, including installing new hardware, extending a satellite’s operational life, and repositioning satellites.

- In January 2026, Aule Space, a start-up based in India, raised funds of about US$2million from investors to enter the market for satellite servicing. It aims to use the funds to develop low-cost spacecraft for the expansion of satellite service lives.

- In January 2026, Washington-based Starfish Space bagged a contract worth US$52.5 million to deorbit satellites for the U.S. Space Force. The company is aiming to launch the Otter spacecraft in 2027. It is specially designed to capture and service satellites.

Companies Covered in Satellite Servicing Market

- Northrop Grumman

- Maxar Technologies

- Astroscale

- Orbit Fab, Inc.

- Thales Alenia Space

- AIRBUS

- Lockheed Martin Corporation.

- ClearSpace

- Altius Space Machines

- Starfish Space

Frequently Asked Questions

The global satellite servicing market is projected to be valued at US$3.1 billion in 2026.

The market is expected to reach US$6.1 billion by 2033.

Shift toward autonomous robotic servicing, standardization of docking interfaces, and the rise of debris removal missions are a few key market trends.

Low Earth Orbit (LEO) is expected to lead with nearly 84.7% share in 2026, as dense mega-constellations create continuous demand for maintenance, repositioning, and end-of-life servicing.

The market is expected to grow at a CAGR of 10.3% from 2026 to 2033.

Northrop Grumman, Maxar Technologies, Astroscale, and Orbit Fab, Inc. are a few key players in the market.