- Medical Devices

- Sigmoidoscope Market

Sigmoidoscope Market Size, Share, and Growth Forecast, 2026 – 2033

Sigmoidoscope Market by Product Type (Flexible Sigmoidoscope, Rigid Sigmoidoscope, Digital Sigmoidoscope), Application (Colorectal Cancer Screening, Others), End-user (Hospitals, Specialty Clinics, Ambulatory Surgical Centers), and Regional Analysis for 2026–2033

Sigmoidoscope Market Size and Trends Analysis

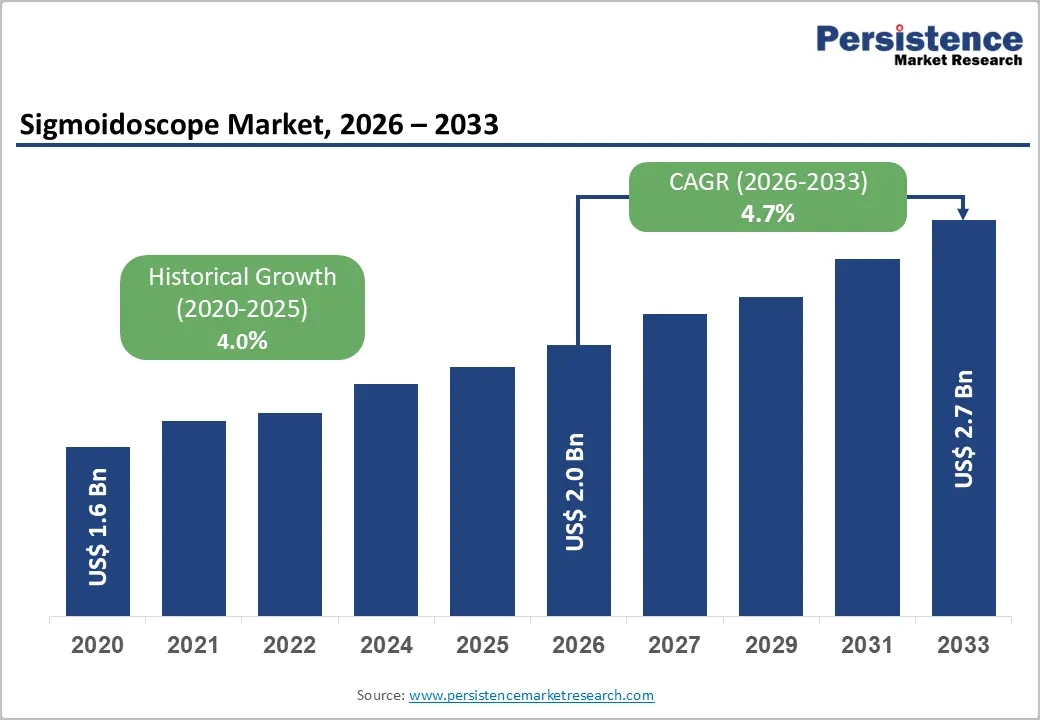

The global sigmoidoscope market size is likely to be valued at US$2.0 billion in 2026, and is expected to reach US$2.7 billion by 2033, growing at a CAGR of 4.7% during the forecast period from 2026 to 2033, driven by the rising global burden of colorectal cancer, expanding national population screening programs, growing inflammatory bowel disease prevalence, and the increasing physician recognition of sigmoidoscopy’s clinical utility as a cost-effective, well-tolerated colorectal screening modality that complements colonoscopy in population health management programs.

Key Industry Highlights:

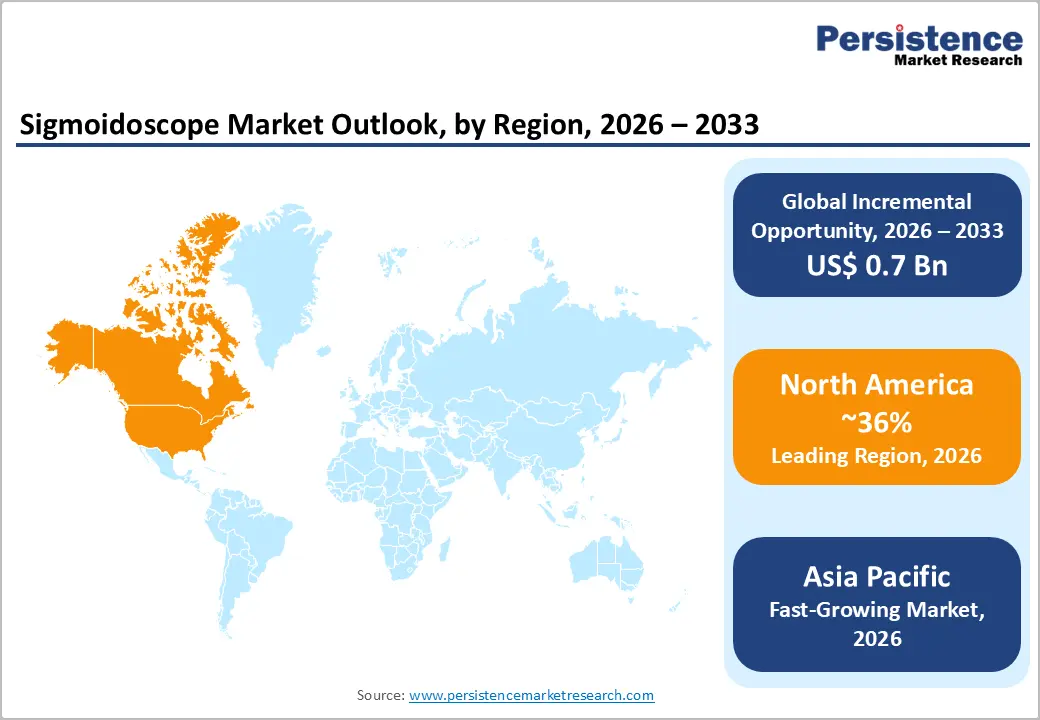

- Dominant Region: North America is expected to hold approximately 36% of market revenue in 2026, driven by established colorectal cancer screening guidelines, a strong gastroenterology care infrastructure, and the presence of major endoscopy manufacturers and commercial operations across the region.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing regional market, with a CAGR of approximately 5.8% from 2026 to 2033, supported by rising colorectal cancer cases, expanding screening programs, and increasing adoption of gastrointestinal endoscopy services across hospitals in China, India, and other regional markets.

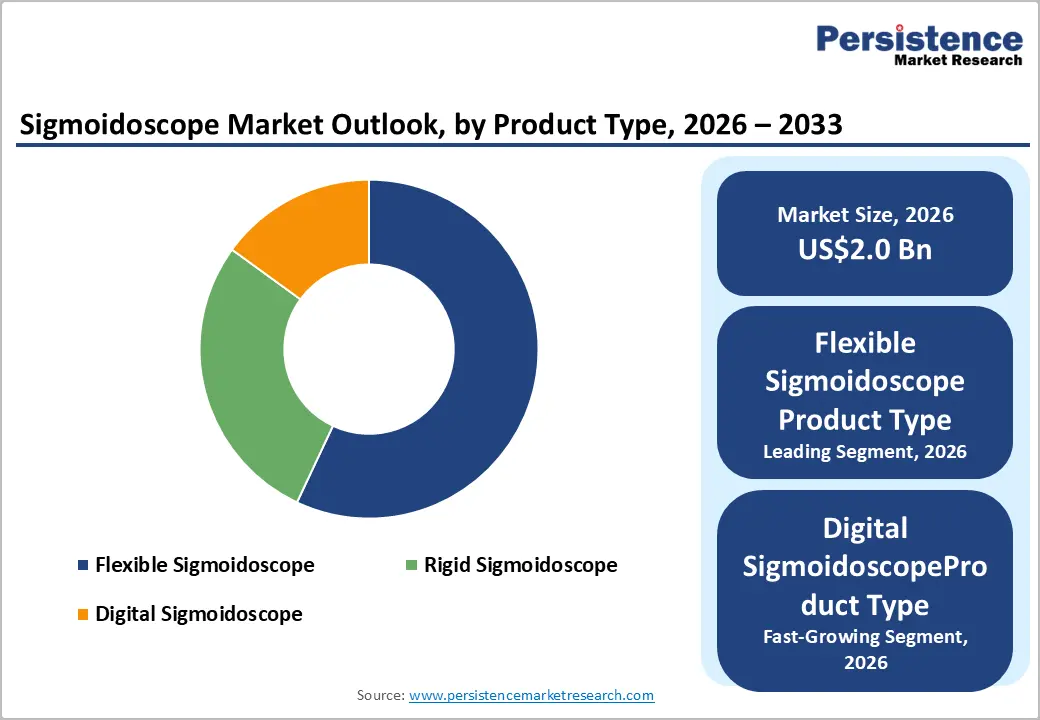

- Leading Product Type: Flexible sigmoidoscopes are expected to account for approximately 57% of the total revenue share in 2026, driven by their widespread use in colorectal cancer screening, IBD surveillance, and the diagnosis of lower gastrointestinal disorders across hospitals and gastroenterology clinics.

- Leading Application: Colorectal cancer screening is expected to account for approximately 48% of the total revenue share in 2026, supported by national screening programs, increasing awareness of early cancer detection, and the USPSTF’s Grade B recommendation recognizing flexible sigmoidoscopy as an effective colorectal cancer screening method.

DRO Analysis

Driver – Inflammatory Bowel Disease Prevalence Growth and Endoscopic Surveillance Requirements

The increasing global burden of inflammatory bowel disease (IBD), including Crohn’s disease and ulcerative colitis, is generating sustained demand for sigmoidoscopy as a key tool for disease monitoring and surveillance. Since the distal colon and rectum are commonly involved in ulcerative colitis, regular endoscopic evaluation is essential for assessing mucosal healing, monitoring disease activity, detecting dysplasia, and guiding treatment decisions.

Flexible sigmoidoscopy continues to play a significant role in IBD management. In the U.S., where the Crohn’s & Colitis Foundation estimates that approximately 6 million adults are living with IBD, guidelines from the American College of Gastroenterology recommend its use to evaluate distal ulcerative colitis, assess proctitis, and obtain targeted surveillance biopsies. Likewise, the European Crohn’s and Colitis Organisation endorses flexible sigmoidoscopy for disease activity assessment, dysplasia surveillance, and treatment-response monitoring in patients with proctosigmoiditis. The growing prevalence of IBD across North America and Europe is therefore contributing to increased utilization of sigmoidoscopy procedures and related devices.

Restraint – Reprocessing Complexity and Healthcare-Associated Infection Risk in Reusable Flexible Sigmoidoscopes

Reusable flexible sigmoidoscopes require rigorous high-level disinfection (HLD) procedures between patient uses, typically involving agents such as glutaraldehyde, ortho-phthalaldehyde (OPA), or hydrogen peroxide plasma sterilization through automated endoscope reprocessors (AERs). Reported healthcare-associated infection outbreaks, including cases involving carbapenem-resistant Enterobacteriaceae (CRE) linked to insufficient reprocessing of duodenoscopes and colonoscopes, have heightened industry-wide attention toward reprocessing compliance, operational complexity, and liability risks across all categories of flexible endoscopes, including sigmoidoscopes.

In response to documented CRE transmission incidents associated with duodenoscopes between 2012 and 2015, the U.S. Food and Drug Administration intensified oversight of flexible endoscope reprocessing practices. This increased regulatory focus has prompted hospitals to strengthen biomedical engineering and infection-control protocols for endoscope reprocessing, leading to greater compliance obligations, higher operational expenditures, and increased liability considerations related to the management of reusable flexible sigmoidoscope fleets.

Opportunity – Digital Sigmoidoscope Adoption in Outpatient and Community Screening.

The launch of compact, high-definition digital sigmoidoscope platforms with wireless connectivity, LED illumination, and tablet-compatible imaging is expanding the use of sigmoidoscopy beyond hospitals. These systems reduce equipment and infrastructure requirements, enabling procedures in primary care clinics, community health centers, and mobile screening units. In contrast, conventional sigmoidoscopes require costly processor systems, reprocessing equipment, and dedicated procedure rooms, limiting their adoption to hospital endoscopy departments and specialist clinics.

Digital sigmoidoscopes, including solutions from FUJIFILM, are reducing equipment costs and space requirements by integrating imaging capabilities into compact, self-contained systems. This enables primary care physicians and colorectal nurse specialists to perform office-based flexible sigmoidoscopy without separate processors or light sources. Growing interest from the NHS Bowel Cancer Screening Programme and European screening initiatives in community-based sigmoidoscopy is creating new adoption opportunities, particularly as healthcare systems seek to reduce pressure on hospital colonoscopy services.

Category-wise Analysis

Product Type Insights

Flexible sigmoidoscopes are expected to dominate the product type, commanding approximately 57% of the total revenue share in 2026. Flexible sigmoidoscopes are the standard instruments for colorectal cancer screening, IBD surveillance, and evaluation of lower gastrointestinal symptoms, enabling examination of the rectum, sigmoid colon, and descending colon. Hospitals and endoscopy centers widely use Olympus’ EVIS X1 platform for lower gastrointestinal examinations, including flexible sigmoidoscopy, colorectal cancer screening, and IBD surveillance.

Digital sigmoidoscopes are likely to be the fastest-growing product type, driven by HD imaging, LED illumination, compact design, and seamless digital image integration with electronic health records. These advantages are accelerating adoption in ambulatory surgical centers, specialist clinics, and community screening programs across North America and Europe. PENTAX Medical advanced digital endoscopy adoption with its INSPIRA™ platform, offering HD imaging, LED illumination, and digital workflow integration for efficient endoscopic procedures.

Application Insights

Colorectal cancer screening is expected to remain the leading application segment, representing approximately 48% of total market revenue in 2026. The widespread adoption of flexible sigmoidoscopy for colorectal cancer screening is supported by recommendations from major healthcare organizations such as the USPSTF, ESGE, and BSG, which recognize its effectiveness in reducing colorectal cancer incidence and mortality through the early identification and removal of precancerous lesions. A notable example is the use of Olympus Corporation’s EVIS X1 endoscopy system, which is extensively utilized in lower gastrointestinal diagnostic procedures, including flexible sigmoidoscopy, to support colorectal cancer screening programs.

Inflammatory bowel disease (IBD) diagnosis is projected to be the fastest-growing application segment, driven by the increasing global prevalence of IBD, growing adherence to clinical guidelines recommending flexible sigmoidoscopy for disease evaluation, and the expanding emphasis on mucosal healing as a key treatment target. The need for regular endoscopic monitoring to assess disease activity and therapeutic response further supports segment growth. For example, FUJIFILM’s ELUXEO endoscopy platform, equipped with Linked Color Imaging (LCI) and Blue Light Imaging (BLI) technologies, is widely utilized to enhance visualization of mucosal inflammation and support mucosal healing assessment during lower gastrointestinal endoscopic examinations, including flexible sigmoidoscopy.

End-user Insights

Hospitals are expected to dominate the end-user, accounting for approximately 53% of total revenue share in 2026. Hospital endoscopy departments remain the primary setting for flexible sigmoidoscopy, supporting cancer screening, IBD surveillance, diagnosis of lower GI disorders, and therapeutic procedures through access to specialized staff, reprocessing facilities, and advanced endoscopy infrastructure. A notable example is the deployment of Olympus Corporation’s EVIS X1 endoscopy platform across hospital endoscopy departments, where it supports a broad range of lower gastrointestinal applications, including colorectal cancer screening, IBD monitoring, and diagnostic evaluations.

Ambulatory surgical centers (ASCs) are projected to be the fastest-growing end-user segment, driven by the increasing migration of flexible sigmoidoscopy procedures to lower-cost outpatient settings, the expansion of standalone endoscopy centers, and the availability of compact digital sigmoidoscope systems that enable efficient procedures without requiring extensive hospital infrastructure. Growth is also supported by the demand for streamlined workflows and cost-effective gastrointestinal diagnostic services. For example, PENTAX Medical facilitates endoscopic procedures in ASCs through its INSPIRA™ Video Processor and i20c endoscope platform, which combine high-definition imaging, a space-efficient design, and seamless workflow integration to support outpatient gastrointestinal examinations.

Regional Insights

North America Sigmoidoscope Market Trends

North America is expected to hold approximately 36% of global revenue share in 2026. The region’s leadership reflects the largest gastroenterology clinical practice infrastructure globally, the USPSTF’s maintained flexible sigmoidoscopy recommendation generating insurance reimbursement coverage for screening procedures, and the presence of leading sigmoidoscope platform developers’ primary commercial operations.

U.S. Sigmoidoscope Market Trends

The U.S. is expected to account for approximately 87% of North America's revenue share in 2026. The American Cancer Society estimated approximately 153,020 new colorectal cancer cases in the U.S. in 2023, representing the third most commonly diagnosed cancer in American adults, sustaining the clinical and policy imperative for population colorectal cancer screening that drives flexible sigmoidoscopy procedure volumes in the U.S. endoscopy market.

Canada Sigmoidoscope Market Trends

Canada is expected to hold approximately 13% of North America's revenue share in 2026, with provincial health program colorectal cancer screening initiatives generating flexible sigmoidoscopy utilization at hospital endoscopy centers, and Canada’s Health Canada-regulated medical device market for endoscopy equipment.

Europe Sigmoidoscope Market Trends

Europe is expected to hold approximately 29% of global revenue share in 2026. Europe’s sigmoidoscope market is supported by national organized colorectal cancer screening programs incorporating flexible sigmoidoscopy, the high IBD prevalence generating endoscopic surveillance demand, and the European Endoscopy Society’s strong guideline infrastructure endorsing flexible sigmoidoscopy in both screening and IBD contexts.

U.K. Sigmoidoscope Market Trends

The U.K. is projected to command approximately 24% of Europe's revenue share in 2026, driven by NHS bowel cancer screening programs, expanding endoscopy workforce capacity, and the presence of domestic endoscopy equipment manufacturers and distributors.

Germany Sigmoidoscope Market Trends

Germany is expected to hold approximately 21% of the Europe revenue share, driven by national colorectal cancer screening programs, broad insurance coverage for endoscopic procedures, and the presence of leading endoscope manufacturer Karl Storz SE & Co. KG, supporting strong adoption of sigmoidoscopy services.

Asia Pacific Sigmoidoscope Market Trends

Asia Pacific is expected to be the fastest-growing regional market, registering a CAGR of approximately 5.8% during the forecast period from 2026 to 2033. Growth is being driven by the increasing incidence of colorectal cancer, the expansion of national and regional screening initiatives, and the rising number of gastroenterology specialists across key countries such as China, South Korea, and Japan. Improving healthcare infrastructure, greater awareness of early cancer detection, and expanding access to endoscopic diagnostic services are further supporting market growth throughout the region.

Japan Sigmoidoscope Market Trends

Japan is estimated to hold approximately 28% of Asia Pacific revenue share in 2026, driven by its national colorectal cancer screening program, high gastrointestinal endoscopy procedure volumes, advanced endoscopy adoption, and the strong presence of leading endoscope manufacturers such as Olympus Corporation and FUJIFILM.

China Sigmoidoscope Market Trends

China is expected to command approximately 33% of Asia Pacific revenue share in 2026, driven by its high colorectal cancer burden, expanding government-led screening programs, and increasing investment in hospital endoscopy infrastructure across tier-1 and tier-2 cities, boosting sigmoidoscope demand.

Competitive Landscape

The global sigmoidoscope market is highly competitive, led by major endoscopy companies and specialized gastrointestinal device manufacturers. Olympus Corporation holds a leading position in flexible sigmoidoscopes through its EVIS EXERA III and EVIS X1 platforms, supported by advanced NBI imaging technology and a strong global sales and service network.

PENTAX Medical (division of Ricoh, Tokyo) competes directly in the flexible sigmoidoscope market with its high-definition video sigmoidoscope range incorporating i-SCAN optical enhancement, targeting European and North American hospital endoscopy departments with competitive platform pricing and comprehensive gastroenterology endoscopy portfolio breadth, while FUJIFILM (Tokyo) serves the flexible sigmoidoscope market with its EC-760R-V/L and related video sigmoidoscope platforms incorporating Blue Light Imaging (BLI) optical enhancement technology that improves vascular and mucosal pattern visualization relevant to IBD disease activity scoring and polyp characterization.

Key Industry Developments:

- In April 2021, Medtronic strengthened the gastrointestinal endoscopy market by launching its AI-powered GI Genius intelligent endoscopy module in the U.S. following FDA clearance. The system provided real-time polyp detection support during lower gastrointestinal endoscopic procedures, including colonoscopy and sigmoidoscopy, helping clinicians improve lesion identification and enhance colorectal cancer screening outcomes.

Companies Covered in Sigmoidoscope Market

- Olympus Corporation

- PENTAX Medical

- FUJIFILM

- Welch Allyn

- Karl Storz

- HMB Endoscopy Products

- RB Medical

- Bolton Surgical

- Parburch Medical Ltd.

- Anetic Aid

- EVEXAR Medical

- HIENE USA LTD.

- Jindal Medical & Scientific Instruments Company Pvt. Ltd.

- Pal Surgicals

Frequently Asked Questions

The global sigmoidoscope market is projected to reach US$2.0 billion in 2026.

Key drivers include expanded colorectal cancer screening eligibility, strong clinical evidence supporting flexible sigmoidoscopy, and guideline recommendations for its use in IBD assessment and ulcerative colitis surveillance.

The sigmoidoscope market is projected to grow at a CAGR of 4.7% from 2026 to 2033.

Key opportunities include the adoption of compact digital sigmoidoscopes in community healthcare settings, expansion of colorectal cancer screening programs in emerging markets, and growing use of AI-assisted polyp detection technologies in sigmoidoscopy.

Key players include Olympus Corporation, PENTAX Medical, FUJIFILM, Welch Allyn, Karl Storz, HMB Endoscopy Products, RB Medical, Bolton Surgical, etc.