- Automotive

- Semi-autonomous Vehicle Market

Semi-autonomous Vehicle Market Size, Share, and Growth Forecast 2026–2033

Semi-autonomous Vehicle Market by Level of Automation (Level 1 Automation, Level 2 Automation, Level 3 Automation), by Propulsion Type (Internal Combustion Engine (ICE) Vehicles, Hybrid Vehicles, Battery Electric Vehicles (BEVs), Fuel Cell Vehicles), by Application, by End-user, by Regional Analysis, 2026–2033

Global Semi-autonomous Vehicle Market Size and Trend Analysis

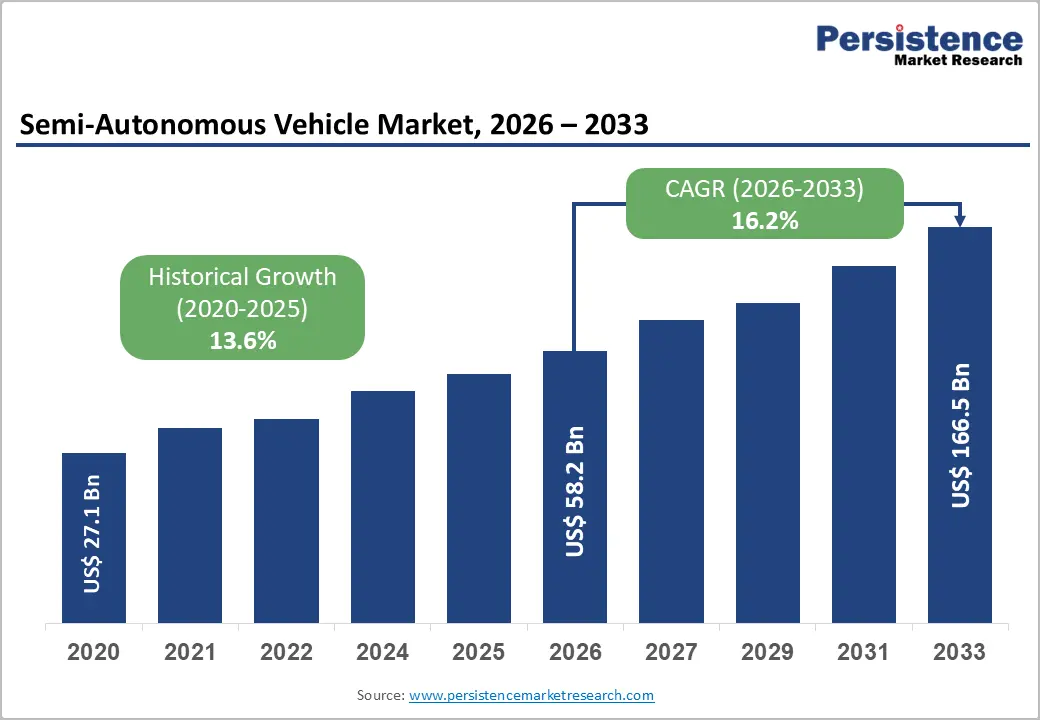

The global semi-autonomous vehicle market is expected to be valued at US$ 58.20 billion in 2026 and is projected to reach US$ 166.48 billion by 2033, growing at a CAGR of 16.2% between 2026 and 2033.

The global semi-autonomous vehicle market encompasses vehicles equipped with advanced driver assistance systems (ADAS) that automate specific driving functions while requiring human supervision. Market growth is driven by stringent vehicle safety regulations, rapid advancements in artificial intelligence and sensor technologies, increasing electric vehicle adoption, and rising consumer demand for safer, more convenient transportation solutions.

Key Industry Highlights:

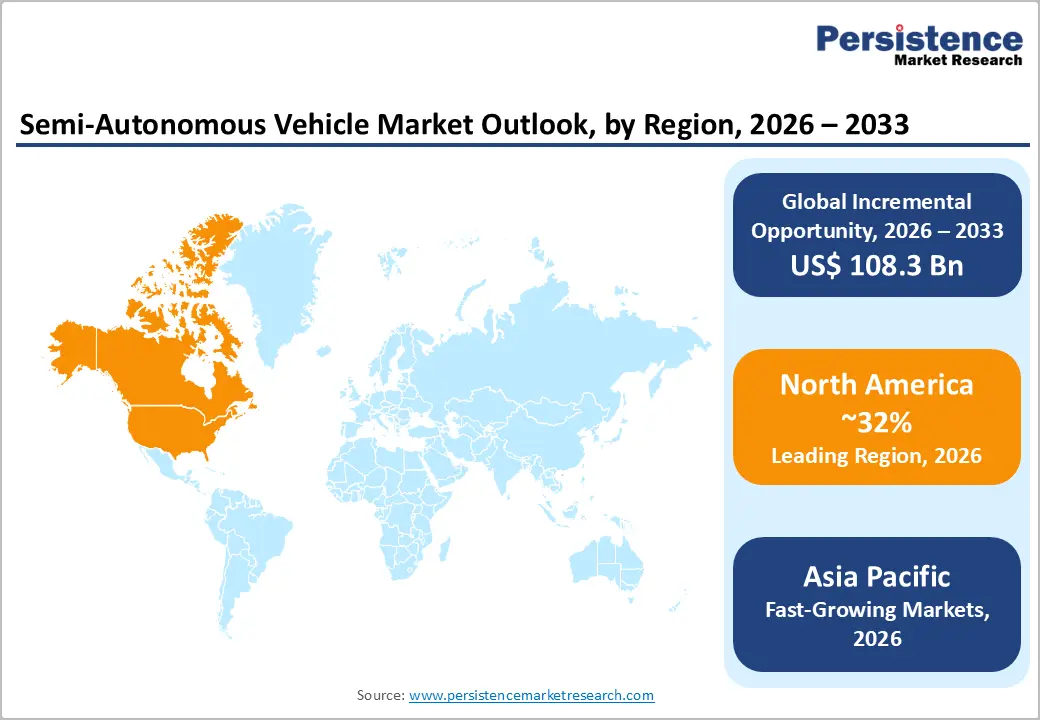

- Leading Region: North America's US$ 18.62 billion regional position in 2026 reflects first-mover regulatory infrastructure, specifically NHTSA's crash-reporting mandate and the Bipartisan Infrastructure Law's V2X corridor funding, that gives U.S.-based ADAS developers a data and deployment velocity advantage that European and Asian rivals cannot replicate within the current forecast window.

- Fastest Growing Region: Asia Pacific's 18.9% CAGR through 2033 makes it the fastest growing regional market, driven by China's MIIT Intelligent Connected Vehicle Roadmap targets and the emergence of domestic OEMs such as BYD and NIO deploying competitive Level 2+ ADAS at mass-market price points, a dynamic that will reshape global ADAS supply chain economics as Chinese hardware costs influence global pricing benchmarks.

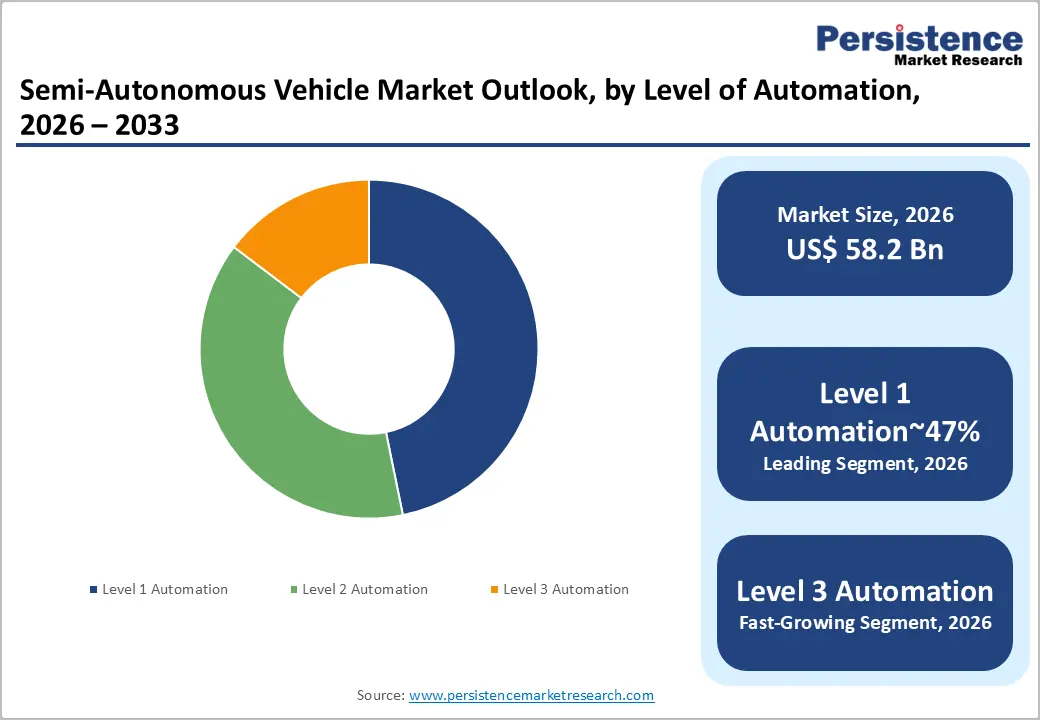

- Leading Segment: Level 1 Automation's 47.0% share of the semi-autonomous vehicle market confirms that mandated safety baseline features, automatic emergency braking, blind-spot detection, and forward collision warning, constitute the commercial foundation of the industry; OEMs and Tier-1 suppliers with locked-in platform contracts for these systems hold a multi-year revenue certainty that higher-automation entrants cannot yet match.

- Fastest Growing Segment: Driver Monitoring Systems are the fastest growing application segment, with the EU General Safety Regulation mandating fitment on all new type-approved EU vehicles from July 2024 and UNECE Regulation 79 amendments tying DMS certification to higher automation level approvals, creating a compliance-driven demand surge that specialists such as Seeing Machines and Smart Eye are positioned to capture through 2028.

- Key Opportunity: Mobility-as-a-Service providers represent the highest-margin strategic opportunity within the semi-autonomous vehicle market for technology stack vendors, as MaaS operators' willingness to pay for per-vehicle ADAS performance guarantees, rather than one-time hardware sales, enables subscription and outcome-based pricing models that fundamentally improve lifetime revenue per vehicle relative to traditional OEM supply arrangements.

Market Dynamics

Market Growth Drivers

Regulatory Mandates Compelling Baseline ADAS Integration Across Global OEM Platforms

Automakers that fail to embed at least Level 2 automation features into new model platforms now face direct commercial consequences, not regulatory penalties alone, but lower safety scores that suppress retail sales. The U.S. National Highway Traffic Safety Administration (NHTSA) finalised its Advanced Impaired Driving Technology rule in 2024, requiring passive monitoring systems in all new passenger vehicles by 2026, while Volvo Cars committed in 2022 to standardising its Pilot Assist highway-driving system across its entire XC and S-series lineup. Over the next two to three years, every Tier-1 supplier that has locked in platform-level ADAS contracts will benefit from multi-year volume compounding as these mandated fitments scale through global production runs.

Proliferation of Sensor Fusion and AI Chipsets Reducing System Cost Below the Mass-Market Threshold

System cost compression, driven by the commoditisation of LiDAR sensors, radar sensors, and computer vision processors, is the mechanism translating regulatory intent into consumer affordability at scale. NVIDIA's DRIVE Thor system-on-chip, announced in 2022 and entering production deployment with BYD and ZEEKR in 2024, consolidates perception, mapping, and driver monitoring onto a single compute platform at a bill-of-materials cost trajectory that makes Level 2+ automation viable in vehicles priced below US$ 35,000. As sensor fusion architectures mature and silicon yields improve through 2026–2027, per-vehicle ADAS hardware costs are estimated to fall a further 25%, directly expanding the addressable consumer base into the mass-market sedan and compact SUV segments.

Market Restraints

Cybersecurity Vulnerability and Data Sovereignty Regulations Creating Compliance Cost Premiums

Connected vehicles equipped with semi-autonomous driving systems generate continuous streams of behavioural, positional, and biometric data, making them priority targets under emerging national cybersecurity frameworks, and this compliance burden compresses the margin for suppliers and OEMs alike.

The EU Cyber Resilience Act, adopted in 2024, imposes mandatory vulnerability disclosure and patching obligations on all connected automotive systems sold in European markets, adding an estimated 12% to software development and validation lifecycle costs per platform. New entrants without established cybersecurity operations face acute disadvantage relative to incumbents such as Aptiv, which has dedicated software security teams already integrated into its autonomous driving architecture.

Consumer Trust Deficit and Liability Ambiguity Suppressing Willingness to Pay for Higher Automation Levels

Documented incidents involving semi-autonomous systems, particularly Tesla's Autopilot, which faced NHTSA investigations resulting in a 2.0 million-vehicle recall in December 2023, erode consumer confidence precisely when OEMs need buyers to accept premium pricing for Level 2+ features.

The absence of a harmonised international liability framework for ADAS-related incidents means insurers apply elevated risk premiums to semi-autonomous vehicles, raising total cost of ownership and dampening demand elasticity among price-sensitive buyers. Smaller OEMs and software-only vendors without the brand resilience of established players bear disproportionate reputational risk from any high-profile system failure.

Market Opportunities

Fleet Electrification and Automation Convergence Opening a High-Value B2B Commercial Vehicle Channel

Fleet operators managing last-mile delivery, long-haul trucking, and public transit networks represent the most capital-efficient entry point for suppliers seeking volume commitments that justify ADAS platform investment at scale. Amazon's deployment of Rivian's electric delivery vans, equipped with Mobileye's EyeQ driver assistance chips, reached 10,000 vehicles in 2023, demonstrating that fleet buyers will commit to semi-autonomous electric platforms when the total operating cost case is clear. Suppliers and OEMs that build modular ADAS architectures compatible with commercial vehicle powertrains will capture disproportionate share as corporate sustainability mandates and fuel cost pressures accelerate commercial fleet replacement cycles through 2028.

Vehicle-to-Everything (V2X) Infrastructure Buildout Creating a New Connectivity-Dependent Feature Layer

Governments investing in smart mobility infrastructure are creating conditions where semi-autonomous vehicles equipped with Vehicle-to-Everything (V2X) communication modules can access real-time traffic signal, hazard, and routing data, unlocking a new tier of assisted-driving features impossible in isolated vehicle architectures.

The Japanese Ministry of Land, Infrastructure, Transport and Tourism launched a national V2X corridor programme in 2023, deploying C-V2X roadside units on 1,200 km of expressways, directly enabling highway pilot and traffic jam assist features for connected vehicles. Technology providers and mobility platforms best positioned to capture this opportunity are those with existing telemetry infrastructure, such as HERE Technologies and cellular network operators already contracted for automotive-grade connectivity, provided that standardisation of the ETSI ITS-G5 and C-V2X protocols converges within the forecast window.

Category-wise Insights

Level of Automation Insights

Level 1 Automation is expected to account for 47% of the global semi-autonomous vehicle market in 2026, supported by its widespread adoption across passenger vehicles. Features such as automatic emergency braking and blind-spot monitoring have become standard in many entry-level and mid-range models. Additionally, insurance providers including Progressive and Allstate offer premium discounts for vehicles equipped with these safety systems, encouraging consumer adoption and reinforcing Level 1 automation as the largest market segment globally.

Level 3 Automation is projected to be the fastest-growing segment, driven by advancements in conditional autonomous driving technologies. These systems enable vehicles to manage driving tasks independently within specific operating conditions. Mercedes-Benz pioneered the segment through regulatory approval of its DRIVE PILOT system in Germany, establishing a framework for broader adoption. Similar approval initiatives in regions such as California and Japan are expected to accelerate commercialization and support growth across premium vehicle categories.

Propulsion Type Insights

Internal Combustion Engine (ICE) Vehicles are anticipated to hold 52% of the global semi-autonomous vehicle market in 2026, reaching approximately US$ 30.26 billion. The segment's leadership reflects the continued dominance of petrol and diesel vehicles in the global fleet. Commercial transportation operators, particularly in North America, increasingly specify advanced driver assistance features such as adaptive cruise control and lane departure warning in procurement requirements, supporting sustained demand for semi-autonomous technologies within ICE-powered vehicles.

Battery Electric Vehicles (BEVs) represent the fastest-growing propulsion segment, benefiting from the compatibility between electric vehicle architectures and advanced autonomous technologies. High-voltage electrical systems efficiently support compute-intensive ADAS functions, while over-the-air software updates enable continuous performance improvements. Tesla’s Full Self-Driving Version 12 demonstrated the scalability of this model by enhancing automation capabilities through software upgrades alone, strengthening BEVs’ position as a key platform for future semi-autonomous vehicle development.

Application Insights

Adaptive cruise control (ACC) is likely to register 24% of the global semi-autonomous vehicle market in 2026, equivalent to US$ 13.97 billion, establishing it as the single most commercially deployed autonomous driving application across both passenger and commercial vehicle segments. Long-haul trucking operators across Europe, including fleets procured under Deutsche Post DHL's green logistics programme, specify radar-based ACC as a mandatory specification because the system demonstrably reduces driver fatigue and rear-end collision frequency on motorway routes exceeding 500 km, creating a direct operational cost justification beyond safety compliance.

Driver Monitoring Systems (DMS) are the fastest growing application segment, driven primarily by the European Commission's General Safety Regulation, which made DMS mandatory on all new type-approved passenger and light commercial vehicles in the EU from July 2024. Seeing Machines, an Australian DMS specialist, secured a multi-year supply agreement with a major European OEM in 2023 to integrate its infrared eye-tracking and head-pose estimation technology into cabin-facing camera systems, a deployment that will expand to millions of vehicles annually as the GSR mandate propagates through the full European new-car cycle.

End-user Insights

Individual consumers represent 69% of the global semi-autonomous vehicle market in 2026, equivalent to US$ 40.16 billion, anchored by the mass-market adoption of ADAS features in private passenger vehicles purchased through franchised dealership and direct-to-consumer channels. Middle-class urban commuters in South Korea, the world's highest vehicle ADAS penetration market by new-car fitment rate according to the Korea Automobile Manufacturers Association (KAMA), routinely select lane-keeping assist, automated parking, and traffic jam assist as primary purchase decision criteria ahead of infotainment features, demonstrating that semi-autonomous capabilities have crossed from premium differentiator to expected standard equipment.

Mobility-as-a-Service (MaaS) Providers are the fastest growing end-user segment, propelled by urban mobility platforms deploying semi-autonomous vehicles to reduce driver cost-per-kilometre and extend operational hours beyond human shift limits. Waymo One, which expanded its fully commercial robotaxi service in San Francisco and Phoenix through 2023–2024 using vehicles equipped with Level 4-capable hardware operating in geofenced Level 3 mode, demonstrated average per-ride economics improving by an estimated 35% relative to human-driven ride-hail benchmarks, a proof point attracting significant institutional capital into the MaaS-ADAS convergence.

Regional Insights

North America Semi-autonomous Vehicle Market Trends and Insights

North America accounts for 32.0% of the global semi-autonomous vehicle market in 2026, representing US$ 18.62 Billion, cementing its position as the leading regional market through a combination of regulatory leadership and the world's highest concentration of autonomous driving technology developers. The NHTSA's Standing General Order on crash reporting for ADAS and ADS-equipped vehicles, in effect since 2021, has generated the world's most comprehensive real-world semi-autonomous incident dataset, enabling faster regulatory iteration and accelerating OEM learning cycles. North America's lead is reinforced by its disproportionate share of global ADAS R&D investment, with Silicon Valley and Detroit hosting the majority of the top-tier autonomous driving software companies operating today.

United States Semi-autonomous Vehicle Market Size

The United States is poised for an estimated 82% of North America's semi-autonomous vehicle market, approximately US$ 15.27 Billion in 2026, driven by the largest single-country new-vehicle sales volume in the region combined with the highest consumer willingness to pay for technology-differentiated vehicles. General Motors' Super Cruise, available across 22 Cadillac, Chevrolet, and GMC models as of 2023, represents the broadest hands-free highway driving deployment by any U.S. domestic OEM, directly expanding the addressable consumer base for Level 2 automation. Federal investment in V2X infrastructure under the Bipartisan Infrastructure Law will further widen the U.S. lead as connectivity-dependent ADAS features become commercially viable through 2028.

Europe Semi-autonomous Vehicle Market Trends and Insights

Europe is likely to reach US$ 16.30 Billion in the coming years owing to the regulatory convergence under UNECE frameworks and Euro NCAP standards compelling faster and broader ADAS adoption than market demand alone would generate. The EU General Safety Regulation, which mandated autonomous emergency braking, intelligent speed assistance, and lane-keeping systems on all new type-approved vehicles from July 2022, has functionally made semi-autonomous technology a commodity fitment across the European new-car market.

Europe's dense motorway network and high vehicle replacement rates ensure sustained hardware upgrade cycles that will keep regional ADAS revenue on a strong growth trajectory through the forecast period.

Germany Semi-autonomous Vehicle Market Size

Germany commands an estimated 27% share of the Europe semi-autonomous vehicle market, approximately US$ 4.40 billion in 2026, anchored by its role as the home market for BMW AG, Audi AG, and Mercedes-Benz Group AG, all of which deploy premium ADAS packages as core brand differentiators. BMW's Personal CoPilot hands-free driving feature, launched on the 7 Series and iX in 2023, illustrates how German luxury OEMs are using Level 2+ automation as the primary technology battleground for premium segment competition. Germany's legislative first-mover advantage in Level 3 approval under its amended road traffic law positions the country to attract international OEM certification investment through 2030.

United Kingdom Semi-autonomous Vehicle Market Size

The United Kingdom holds an estimated 16% of the European semi-autonomous vehicle market, approximately US$ 2.61 Billion in 2026, supported by the Automated Vehicles Act 2024, which established the world's first legislative framework explicitly permitting self-driving vehicles on public roads and assigning liability to the authorised self-driving entity rather than the driver. This liability clarity removes a key commercial barrier that has delayed Level 3 system deployment in other markets, making the UK an attractive early-launch jurisdiction for OEMs seeking regulatory proof-of-concept outside Germany. Continued domestic investment through Innovate UK's £100 million Connected and Automated Mobility programme signals sustained government commitment to maintaining a leading innovation environment.

France Semi-autonomous Vehicle Market Size

France is expected to represent 14% of the European semi-autonomous vehicle market, approximately US$ 2.28 Billion in 2026, with Stellantis and Renault Group driving domestic ADAS adoption through their combined volume across the Peugeot, Citroën, Opel, Dacia, and Renault brands. Renault's launch of the Scenic E-Tech Electric in 2023, featuring a full suite of Level 2 ADAS including highway lane-centering and hands-free parking, demonstrated that French OEMs are successfully embedding advanced automation into mass-market price points below €45,000. France's Loi d'Orientation des Mobilités (LOM 2019) and its subsequent implementation decrees continue to shape the regulatory architecture for connected and automated vehicles, providing policy predictability that supports long-cycle supplier investment.

Asia Pacific Semi-autonomous Vehicle Market Trends and Insights

Asia Pacific is likely to account for 30% of the global semi-autonomous vehicle market in 2026, representing US$ 17.46 Billion, and is advancing at the fastest regional CAGR of 18.9% through 2033, propelled by China's New Energy Vehicle industrial policy, Japan's V2X infrastructure buildout, and India's rapidly expanding premium vehicle segment. China's Ministry of Industry and Information Technology (MIIT) published its "Intelligent Connected Vehicle Technology Roadmap 2.0" in 2020, targeting 50% of new vehicle sales equipped with Level 2+ automation by 2025, enabling growth corridors for China and posing as the world's largest volume market for semi-autonomous features. This trajectory is likely to intensify as domestic Chinese EV brands, equipped with competitive ADAS stacks at sub-US$ 25,000 price points, begin exporting to Southeast Asian and Middle Eastern markets, amplifying Asia Pacific's share of global semi-autonomous vehicle market revenue.

China Semi-autonomous Vehicle Market Size

China represents an estimated 55% of the Asia Pacific semi-autonomous vehicle market, approximately US$ 9.60 Billion in 2026, driven by the world's largest annual new vehicle production volume and a domestic tech ecosystem supplying competitive ADAS components at scale. Huawei's ADS 2.0 system, integrated into the AITO M9 and Avatr 11 in 2023–2024, delivers city-level Navigation Guided Pilot without high-definition maps, a capability that reduces deployment cost and accelerates geographic coverage across China's 300+ tier-1 and tier-2 cities.

As Baidu Apollo continues expanding its open-source autonomous driving platform to additional Chinese OEM partners, China's ADAS software ecosystem will deepen its competitive moat against Western rivals through the forecast horizon.

India Semi-autonomous Vehicle Market Size

India accounts for an estimated 12% of the Asia Pacific semi-autonomous vehicle market, approximately US$ 2.10 Billion in 2026, with demand concentrated in the rapidly expanding premium SUV segment, where Hyundai Motor India and Tata Motors are deploying ADAS suites including automatic emergency braking and lane departure warning as competitive differentiators. The Bharat New Car Assessment Programme (Bharat NCAP), launched in August 2023, introduced a formal safety rating regime that rewards ADAS fitment with higher star ratings, creating an immediate market incentive for OEMs selling in India to accelerate feature adoption.

As India's annual vehicle sales volumes are projected by the Society of Indian Automobile Manufacturers (SIAM) to approach 5.5 million units by 2027, the volume base supporting ADAS revenue will expand materially, making India a fast-growing market within Asia Pacific.

Japan Semi-autonomous Vehicle Market Size

Japan holds an estimated 20% of the Asia Pacific semi-autonomous vehicle market, approximately US$ 3.49 Billion in 2026, supported by Toyota Motor Corporation's and Honda Motor Co.'s extensive deployment of Level 2 automation across their domestic and export lineups. Honda's Legend became the world's first Level 3 certified production vehicle under Japan's revised Road Transport Vehicle Act when it launched in 2021, and Honda extended this capability with its Sensing Elite system across additional model lines in 2023, reinforcing Japan's position as a global Level 3 commercialisation leader.

Japan's acute demographic challenge, with persons aged 65 and above representing approximately 29% of the population per the Statistics Bureau of Japan, creates a distinct demand driver: elderly licence holders who retain mobility independence through vehicles with advanced driver assistance, sustaining domestic ADAS demand independent of macroeconomic cycles.

Competitive Landscape

The global semi-autonomous vehicle market operates as a technology-stratified oligopoly at the silicon and software layer, where NVIDIA and Mobileye collectively supply compute and perception stacks to a majority of global OEM programmes, while remaining intensely fragmented at the vehicle integration and deployment layer.

Tesla leads on over-the-air software differentiation; Waymo dominates robotaxi-grade perception architecture; and Aptiv anchors the Tier-1 supplier segment through its Motional joint venture with Hyundai. The defining competitive separator is not hardware specification but the proprietary dataset size that trains and validates AI driving models, making data accumulation strategy the primary moat. Aurora Innovation's commercial trucking launch in 2024 represents the most credible near-term challenge to incumbents by concentrating on a single, high-value operational design domain.

Key Developments:

- January 2024: Waymo expanded its commercial robotaxi operations into Los Angeles, becoming the first autonomous vehicle operator to serve three major U.S. cities simultaneously, demonstrating scalable geofenced deployment economics.

- March 2025: Mobileye launched its SuperVision hands-free driving system with ZEEKR in China, marking the first deployment of Mobileye's highest-tier ADAS stack in the world's largest new-vehicle market.

- November 2024: Aurora Innovation initiated the first commercial driverless trucking service in Texas without a safety driver on board, operating Class 8 trucks on the Dallas-to-Houston corridor under a commercial carrier agreement with Hirschbach Motor Lines.

Companies Covered in Semi-autonomous Vehicle Market

- Tesla

- Waymo

- General Motors

- Ford Motor Company

- BMW AG

- Audi AG

- Mercedes-Benz Group AG

- NVIDIA

- Mobileye

- Aptiv

- Baidu Apollo

- Pony.ai

- WeRide

- Aurora Innovation

- Zoox

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Hyundai Motor Company

- Toyota Motor Corporation

- Honda Motor Co.

- Stellantis

- Renault Group

- HERE Technologies

- Seeing Machines

Frequently Asked Questions

The market is valued at US$ 58.20 billion in 2026 and is projected to reach US$ 166.48 billion by 2033, growing at a 16.2% CAGR, driven by ADAS regulations and BEV adoption.

Growth is driven by mandatory safety regulations requiring ADAS features, increasing vehicle automation, advancements in AI-based perception systems, and rising consumer demand for enhanced vehicle safety and convenience.

Level 1 Automation holds the largest share at 47% in 2026 due to its affordability, broad compatibility across vehicle platforms, regulatory support, and widespread adoption in mass-market vehicles.

North America leads with 32% market share in 2026, supported by strong autonomous technology development, favorable regulations, advanced automotive infrastructure, and continued investment in vehicle safety initiatives.

Key opportunities lie in V2X connectivity integration, enabling advanced driving capabilities, improved traffic management, enhanced safety performance, and new revenue streams for automakers and technology providers.

Leading companies include NVIDIA, Mobileye, Aptiv, Tesla, Mercedes-Benz Group AG, and General Motors. Competition increasingly focuses on AI capabilities, software platforms, and over-the-air update technologies.