- Automotive

- Mining Truck Market

Mining Truck Market Size, Share, and Growth Forecast 2026 - 2033

Mining Truck Market by Truck Type (Haul Trucks, Dump Trucks, Articulated Trucks, Underground Mining Trucks), Power Source (Diesel-Powered, Electric-Powered, Hybrid (Diesel-Electric), Hydrogen-Powered), Load Capacity (Light-Duty (Up to 100 tons), Medium-Duty (100-200 tons), Heavy-Duty (200-400 tons), Ultra-Class (Above 400 tons)), Application and Regional Analysis for 2026 - 2033

Mining Truck Market Size and Trend Analysis

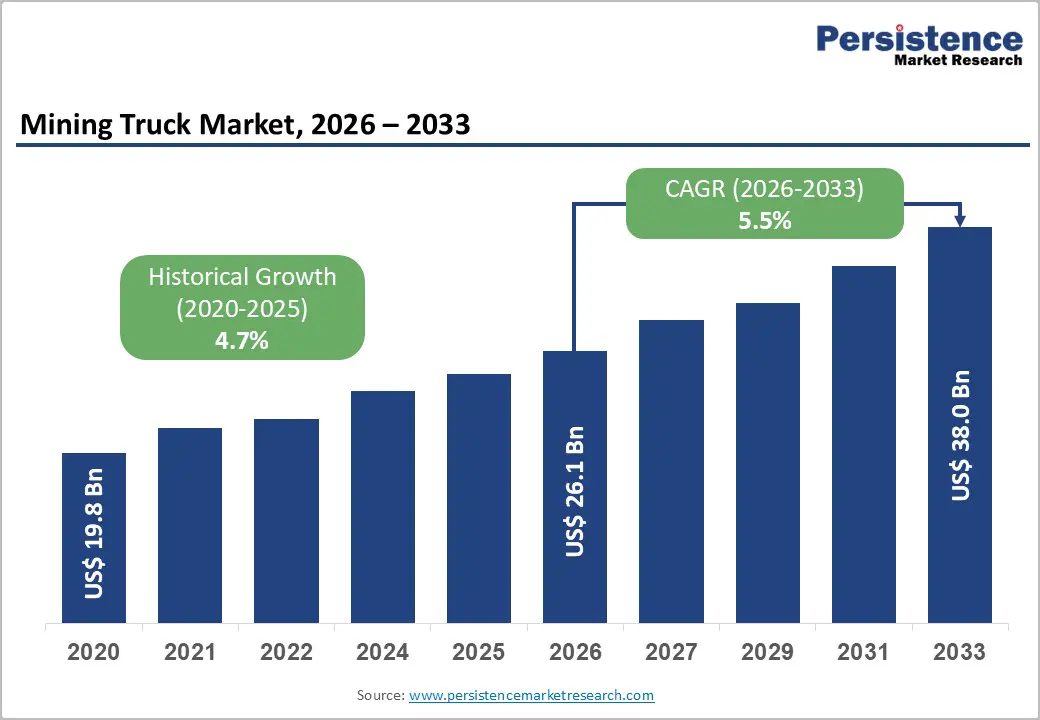

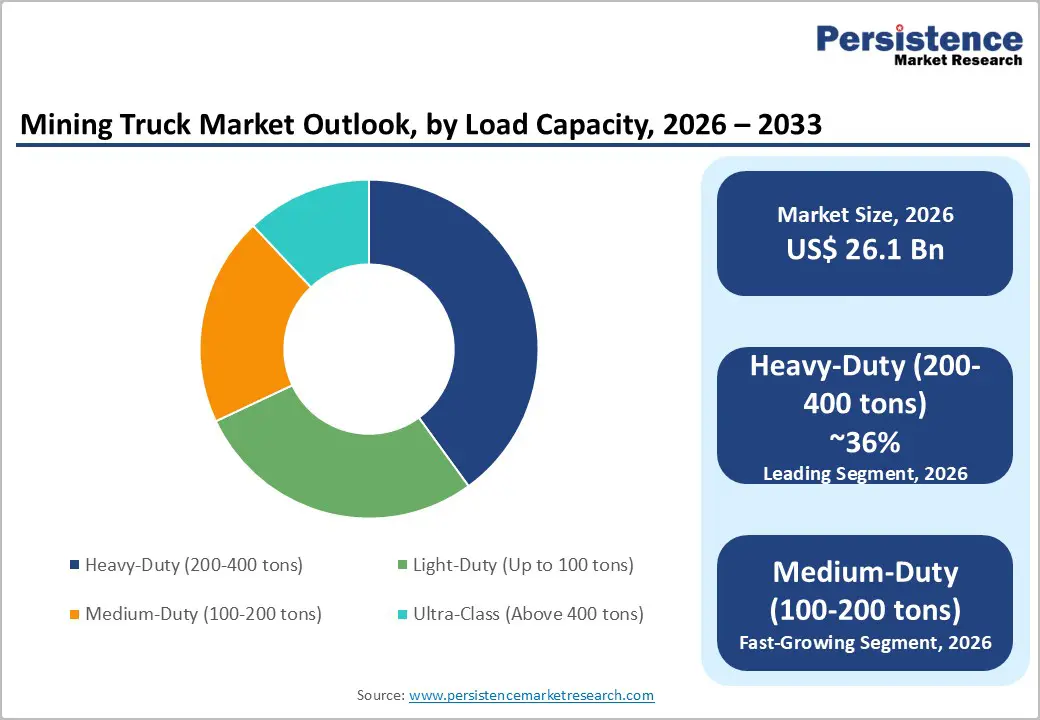

The global mining truck market size is likely to be valued at US$ 26.1 billion in 2026 and is projected to reach US$ 38.0 billion, growing at a CAGR of 5.5% between 2026 and 2033.

The market is primarily driven by accelerating global mining activity, surging demand for critical minerals such as lithium, copper, and cobalt essential for energy transition, and the rapid modernization of mining fleets with autonomous and electric vehicle technologies. Government-backed resource extraction programs in countries like Australia, Chile, and Canada continue to expand the operational base for mining truck deployments.

Key Industry Highlights:

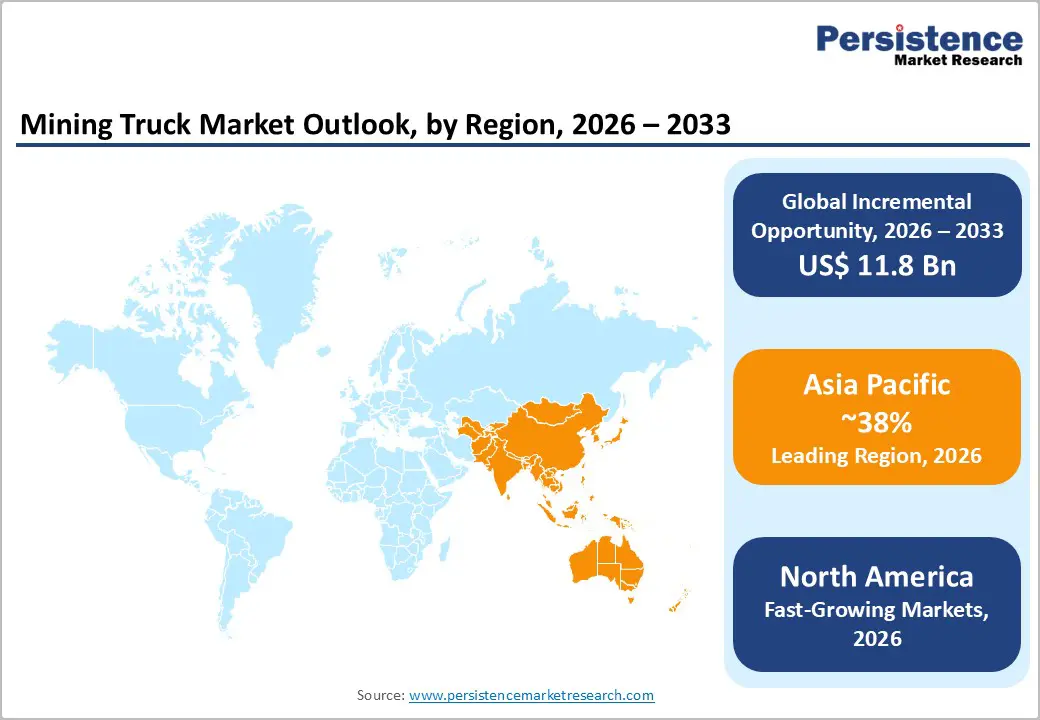

- Leading Region - Asia Pacific dominates the global mining truck market with over 38% revenue share in 2026, driven by China's large-scale coal mining, Australia's iron ore exports, India's expanding coal and mineral extraction, and Southeast Asia's growing nickel and copper mining operations.

- Fast-Growing Region - North America remains one of the most mature and technologically advanced markets for mining trucks, driven by large-scale mining activity in the United States, Canada, and Mexico.

- Dominant Truck Type - Haul trucks represent the largest segment, underpinned by their indispensable role in large-scale open-pit operations. Their ability to haul payloads exceeding 300 metric tons makes them the backbone of copper, coal, and iron ore extraction globally.

- Fast-Growing Source Segment - The electric-powered segment is set to register the fastest CAGR in the forecast period driven by ICMM net-zero pledges, trolley-assist mine infrastructure investments, and pioneering electric haul truck deployments by companies such as Caterpillar and Liebherr.

- Key Opportunity - With mining companies globally committing to net-zero targets by 2050, the transition from diesel to battery-electric and hydrogen fuel cell trucks represents a transformative revenue opportunity, particularly as OEM platforms mature and total cost of ownership parity with diesel is achieved.

DRO Analysis

Drivers - Surge in Critical Mineral Extraction and Energy Transition Demand

The global pivot toward clean energy has substantially elevated demand for mining trucks, as the extraction of battery-critical minerals, namely lithium, nickel, cobalt, and copper, intensifies worldwide. According to the International Energy Agency (IEA), demand for critical minerals is projected to quadruple by 2040 under net-zero scenarios, directly stimulating expanded mining operations across Latin America, Africa, and the Asia Pacific.

The U.S. Geological Survey (USGS) reports that global copper mine output reached approximately 22 million metric tons in 2023, with projected output expansions requiring large-scale fleet upgrades. As open-pit mines deepen and widen, the operational throughput requirements make high-capacity haul trucks indispensable, directly propelling market expansion.

Rapid Adoption of Autonomous and Technologically Advanced Mining Trucks

Autonomous haulage systems (AHS) are reshaping fleet management across major mining regions. Rio Tinto reported that its autonomous truck fleet operating in the Pilbara region of Australia has collectively hauled over 5 billion tonnes of material, demonstrating a 15% improvement in productivity compared to conventional manned vehicles.

The Australian Government's Department of Industry, Science and Resources has acknowledged automation as a critical productivity multiplier in the mining sector. Similarly, Caterpillar Inc. and Komatsu Ltd. have launched next-generation autonomous platforms that integrate real-time GPS, AI-driven path planning, and predictive maintenance, thereby reducing downtime and total cost of ownership.

Restraints - High Capital Expenditure and Total Cost of Ownership

Mining trucks particularly ultra-class haul trucks represent one of the most capital-intensive equipment categories in mining operations. A single ultra-class mining truck can cost between US$ 3.5 million and US$ 5 million, with annual maintenance costs adding another 20% of the purchase price.

According to World Mining Congress data, many mid-tier mining companies cite capital constraints as a primary barrier to fleet renewal. Operators in developing economies face additional financing challenges due to limited access to long-term credit instruments, constraining the pace of fleet modernization and, consequently, limiting the addressable market for OEMs in cost-sensitive geographies.

Stringent Emission Regulations and Operational Compliance Costs

Regulatory pressure from bodies such as the U.S. Environmental Protection Agency (EPA), the European Environment Agency (EEA), and national governments is imposing increasingly strict emission norms on off-highway diesel equipment.

The EPA Tier 4 Final and EU Stage V standards require significant engine redesigns and the integration of diesel particulate filters (DPF) and selective catalytic reduction (SCR) systems, increasing unit manufacturing costs by an estimated 8%. For smaller mining operators, retrofitting or replacing non-compliant fleets to meet these standards introduces financial strain, particularly in jurisdictions where compliance timelines are accelerated, potentially slowing market uptake in certain segments.

Opportunities - Electrification of Mining Truck Fleets A Transformative Growth Frontier

The electrification of mining trucks presents one of the most significant near-to-medium-term opportunities in the industry. In 2022, Boliden's Aitik copper mine in Sweden commissioned one of the world's first fully electric underground mining truck deployments, while Anglo American announced the world's largest hydrogen-powered mining truck prototype, the nuGen™ Zero Emission Haulage Solution developed in partnership with Engie and NPROXX.

The International Council on Mining & Metals (ICMM) has committed its 27 member companies to net-zero Scope 1 and Scope 2 emissions by 2050. OEMs that invest in battery-electric and hydrogen fuel cell truck platforms stand to capture disproportionate share as mining companies globally overhaul fleets to meet decarbonization pledges, particularly in jurisdictions where carbon pricing mechanisms are in place.

Infrastructure-Driven Demand in Emerging Economies and Greenfield Mine Development

Rapid urbanization and infrastructure development across Africa, Southeast Asia, and South America are generating unprecedented demand for construction materials, fuelling parallel growth in quarrying and surface mining activities. The African Development Bank (AfDB) estimates that Africa requires over US$ 130 billion annually in infrastructure investment, a portion of which directly stimulates mining and quarrying of aggregates, iron ore, and bauxite.

Greenfield mine development in the Democratic Republic of Congo (DRC), Zambia, and Tanzania, driven by Chinese and Western investment, is expected to commission thousands of new mining trucks over the forecast period. OEMs with localized service networks and flexible financing structures are best positioned to capitalize on this rapidly expanding demand frontier.

Category-wise Analysis

Truck Type Insights

Haul trucks represent the dominant segment within the truck type category, accounting for approximately 42% of total market revenue. Their dominance is rooted in their unmatched payload capacity and operational efficiency in large-scale surface mining operations. The Caterpillar 797F and Komatsu 930E among the world's largest haul trucks can carry payloads exceeding 300 metric tons, making them indispensable in mega open-pit mines for coal, copper, and iron ore extraction.

According to the World Coal Association, over 65% of global coal is extracted via surface mining, a method that inherently relies on high-capacity haul trucks. The growing number of large-scale copper and iron ore projects in Chile, Brazil, and Australia continues to reinforce the segment's market leadership throughout the forecast period.

Power Source Insights

Diesel-Powered trucks continue to dominate the power source category, accounting for an estimated share of approximately 68% of the global mining truck market. This dominance reflects decades of established operational infrastructure, widespread availability of diesel fuel in mining regions, and the superior energy density of diesel compared to current battery technology, particularly critical for ultra-class haul trucks requiring sustained high-torque performance.

The U.S. Energy Information Administration (EIA) notes that diesel remains the primary energy source for off-road heavy equipment globally due to its versatility across diverse climates and terrains.

Load Capacity Insights

Heavy-duty trucks (200-400 tons) constitute the leading segment within the load capacity category, capturing approximately 36% of total market revenue. This segment's supremacy is directly attributable to the expanding scale of open-pit copper, gold, and coal mines, where operational efficiency mandates high-payload vehicles that minimize the number of trips per cycle.

According to the International Copper Study Group (ICSG), global copper mine production exceeded 22 million metric tons in 2023, with the majority sourced from large-scale open-pit operations in Chile and Peru.

Application Insights

Surface mining is the leading application segment, accounting for approximately 58% of the global mining truck market. Surface mining operations including open-pit, strip, and quarry mining demand the highest concentration of heavy haulage equipment due to the sheer volume of material moved per extraction cycle. The U.S. Geological Survey (USGS) reports that open-pit mining accounts for most global production of copper, iron ore, coal, and gold.

Large-scale surface mines in Australia, Chile, India, and South Africa operate fleets of 50-200 trucks per site, contributing substantially to demand. The ongoing development of new surface mines to meet battery mineral demand particularly lithium and copper alongside expansions at existing operations, is expected to sustain surface mining's dominant share throughout the forecast horizon.

Regional Analysis

North America Mining Truck Market Trends & Analysis

North America remains one of the most mature and technologically advanced markets for mining trucks, driven by large-scale mining activity in the United States, Canada, and Mexico. The region benefits from well-established mining infrastructure, robust OEM service networks, and progressive adoption of autonomous haulage systems.

Canada's oil sands operations in Alberta, among the world's largest by volume, represent a major ongoing demand centre for ultra-class trucks. North America is estimated to account for approximately 26% of global mining truck revenues in 2026, with steady growth underpinned by fleet modernization and electrification initiatives.

U.S. Mining Truck Market Insights

The United States holds the largest share within North America, supported by active copper, coal, and gold mining operations in states such as Nevada, Arizona, and Wyoming. The U.S. Bureau of Land Management (BLM)'s expanded permitting for critical mineral projects, combined with the Defense Production Act designations for rare earth and battery minerals, is accelerating new mine development, positioning the U.S. as a key growth driver within the regional market.

Europe Mining Truck Market Trends, Drivers, & Insights

Europe's mining truck market is undergoing a structural transformation, shaped by the European Green Deal and the EU Critical Raw Materials Act (2023), which targets domestic extraction of strategic minerals. While Europe's mining output remains modest compared to other regions, Scandinavian countries particularly Sweden and Finland are at the vanguard of electric and autonomous mining truck adoption, leveraging hydroelectric power grids to enable zero-emission underground mining.

Germany Mining Truck Market Size

Germany's market is primarily linked to quarrying and construction aggregates, supported by the country's extensive road and infrastructure development programs. While large-scale mining is limited, demand for medium-duty dump trucks and articulated trucks in quarrying remains consistent, anchored by the construction industry's robust activity.

U.K. Mining Truck Market Size

The United Kingdom's mining truck market is supported primarily by quarrying operations the country is one of Europe's largest producers of aggregates. The Mineral Products Association (MPA) reports that the U.K. quarrying industry produces over 200 million tonnes of aggregate annually, sustaining steady demand for medium-duty trucks.

France Mining Truck Market Size

France's market is driven by quarrying and construction materials extraction, particularly limestone and granite. The country's significant infrastructure investment pipeline, including projects under the France 2030 Plan, supports continued demand for articulated and dump trucks across quarry operations in central and southern regions.

Asia Pacific Mining Truck Market Drivers & Analysis

Asia Pacific is the largest and fastest-growing regional market for mining trucks, underpinned by the colossal mining industries of China, Australia, and India. The region is estimated to account for over 38% of global market revenues in 2026. Australia's iron ore and coal export-driven mining sector, India's rapidly expanding coal and iron ore extraction, and China's extensive domestic mining of coal, copper, and rare earth elements collectively generate enormous ongoing demand for mining trucks across all capacity classes.

China Mining Truck Market Size

China dominates regional and global demand, underpinned by the world's largest coal mining industry, with annual production exceeding 4 billion tonnes as per National Bureau of Statistics (NBS) China data. Domestic manufacturers such as XCMG, SANY Heavy Industry, and LGMG are gaining market share against international OEMs through competitive pricing and expanding product portfolios, including emerging electric mining truck models.

India Mining Truck Market Trends

India's market is driven by the government's ambitious coal production targets under the National Coal India Limited expansion plans and growing iron ore and limestone extraction. Coal India Limited (CIL), the world's largest coal producer, has outlined plans to increase output significantly, creating sustained demand for haul and dump trucks across its extensive open-cast mine network.

Japan Mining Truck Market Trends

Japan's mining truck market is relatively niche in terms of domestic demand due to the country's limited large-scale mining activities. It is significant within the global mining truck industry as a center for technological innovation, engineering excellence, and equipment manufacturing. Komatsu Ltd., headquartered in Tokyo is one of the world's leading mining truck producers and a pioneer in autonomous haulage systems (AHS), advanced fleet management solutions, and electrification technologies. The company's innovations are widely deployed across major mining regions worldwide, improving productivity, safety, and operational efficiency.

Competitive Landscape

The global mining truck market is moderately consolidated, with a small number of international OEMs, namely Caterpillar Inc., Komatsu Ltd., and Liebherr Group, collectively commanding a significant majority of the high-capacity haul truck segment. These incumbents leverage deep customer relationships, extensive global service networks, and proprietary autonomous systems as key differentiators. However, the market is experiencing progressive fragmentation in the mid-tier and electric vehicle segments, with Chinese manufacturers (XCMG, LGMG) and new entrants in the electric mining vehicle space challenging established players

Key Developments:

- In August 2025, Komatsu signed an agreement with Pronto to launch an autonomous solution for quarry operations. The partnership focuses on the launch of Komatsu‘s smart quarry autonomous system, powered by Pronto, that integrates Pronto’s autonomy technologies into quarry-sized haul trucks.

- In March 2025, Caterpillar Inc. introduced the first commercially available Autonomous Water Truck. The new Cat 789D Autonomous Water Truck (AWT) enhances productivity by enabling mine operations to track water consumption and reduce waste digitally. It offers the same potential for greater use than staffed equipment.

Companies Covered in Mining Truck Market

- Caterpillar Inc.

- Komatsu Ltd.

- Liebherr Group

- Hitachi Construction Machinery

- BelAZ

- XCMG Group

- SANY Heavy Industry

- LGMG

- Epiroc AB

- Sandvik AB

- Volvo CE

- Doosan Bobcat

- John Deere

- Weir Group

- Terex Corporation

Frequently Asked Questions

The global mining truck market size is projected to reach US$ 38 billion by 2033, growing from US$ 26.1 billion in 2026 at a CAGR of 5.5% during the forecast period.

The primary drivers of the Mining Truck market include the surge in demand for critical minerals, especially lithium, copper, cobalt, and nickel, essential for the global clean energy transition, and the rapid adoption of autonomous haulage systems (AHS).

Haul Trucks constitute the leading segment in the Truck Type category, holding approximately 42% of market revenues. Their dominance is driven by their indispensability in large-scale open-pit surface mining operations, where payloads exceeding 300 metric tons per vehicle are required to maintain operational efficiency in coal, copper, and iron ore extraction.

Asia Pacific is the leading region, accounting for an estimated 38%-40% of global revenues in 2026. The region's dominance is attributable to China's expansive coal mining sector, Australia's world-class iron ore operations, India's growing coal and mineral extraction industry, and emerging mining investments across Indonesia and the Philippines.

The key players operating in the global mining truck market include Caterpillar Inc., Komatsu Ltd., Liebherr Group, Hitachi Construction Machinery Co., Ltd., BelAZ, XCMG Group, SANY Heavy Industry Co., Ltd., LGMG, Epiroc AB, Sandvik AB, and Volvo Construction Equipment, among others.