- Automotive

- Fire Fighting Vehicle Market

Fire Fighting Vehicle Market Size, Share, and Growth Forecast 2026–2033

Fire Fighting Vehicle Market by Vehicle Type (Pumper Truck, Aerial Ladder Truck, Rescue Truck, Tanker/Tender Truck, Airport Crash Tender, Wildland Fire Truck), Propulsion (Internal Combustion Engine (ICE), Hybrid Electric, Battery Electric Vehicle (BEV), Fuel Cell Electric Vehicle (FCEV)), End-user (Municipal Fire Departments, Industrial Facilities, Airports, Military & Defense, Forestry & Wildland Agencies), and Regional Analysis, 2026–2033

Global Fire Fighting Vehicle Market Size and Trend Analysis

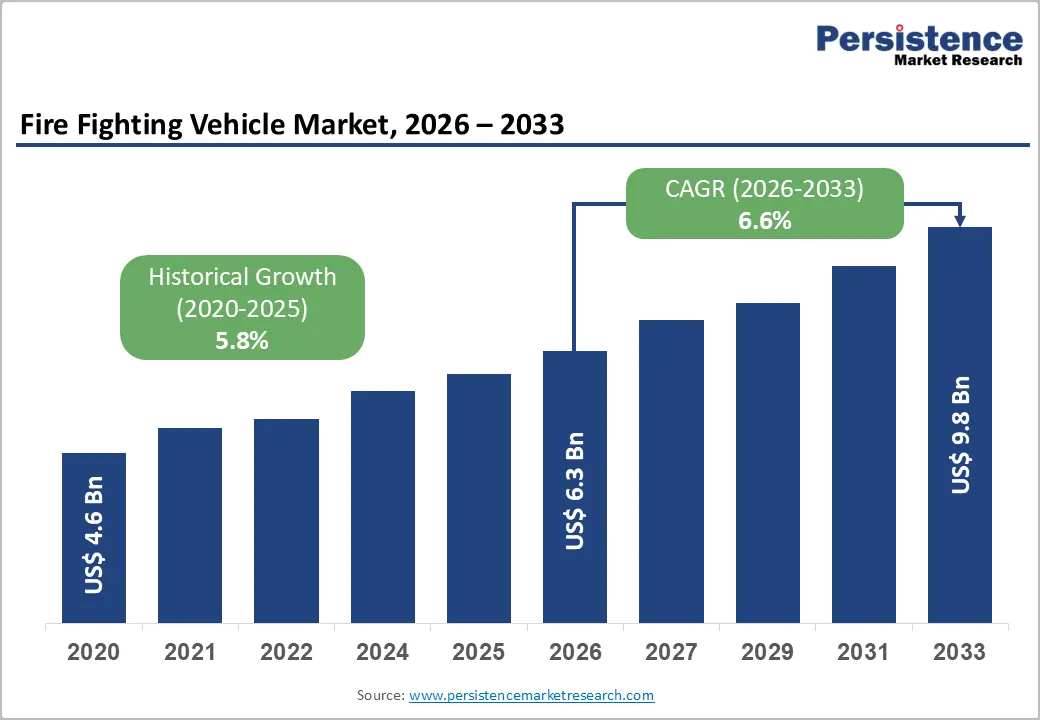

The global fire fighting vehicle market is expected to be valued at US$ 6.30 billion in 2026 and is projected to reach US$ 9.85 billion by 2033, growing at a CAGR of 6.6% between 2026 and 2033.

The U.S. Federal Emergency Management Agency (FEMA)'s Assistance to Firefighters Grant (AFG) programme, which disbursed over US$360 million in fiscal year 2023 alone, is directly funding apparatus replacement cycles that sustain procurement volumes in the world's largest fire equipment market. Cal Fire's commitment to expand its ground fleet by more than 30% through 2027 in response to California's escalating wildfire seasons provides a concrete demand signal validating this trajectory.

Key Industry Highlights:

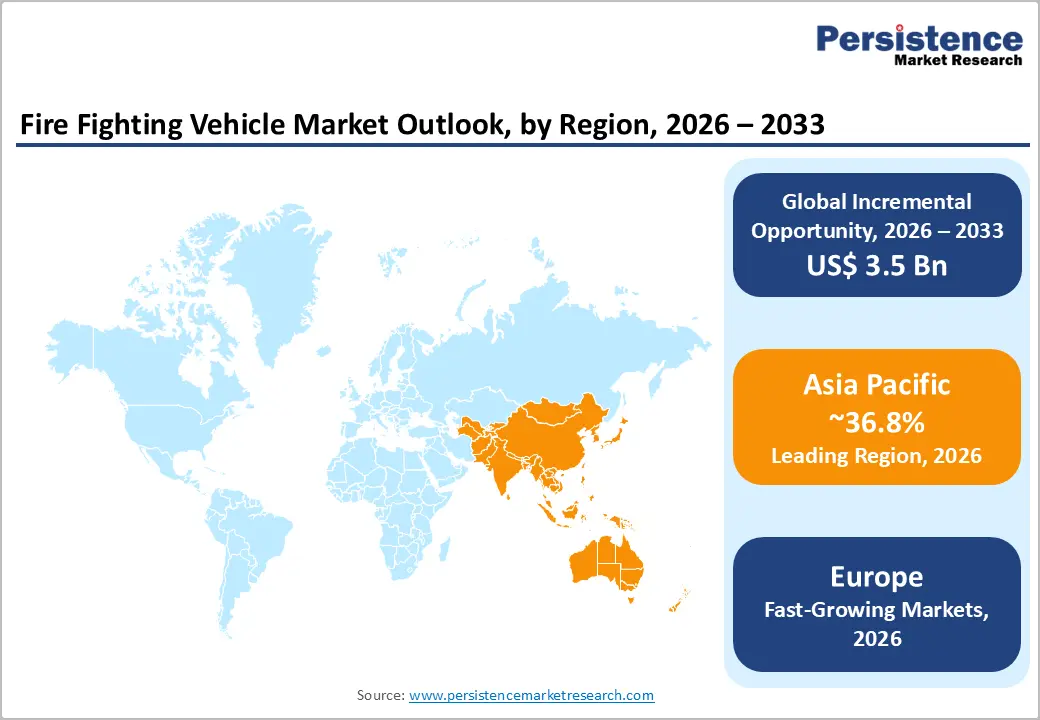

- Leading Region: Asia Pacific's regional leadership in the global fire fighting vehicle market is likely to register 36.8% of global revenue at US$ 2.32 Billion in 2026. rests on simultaneous fleet build-outs across China, Japan, India, and South Korea, driven by independent national mandates that collectively ensure the region's market primacy will deepen through 2033.

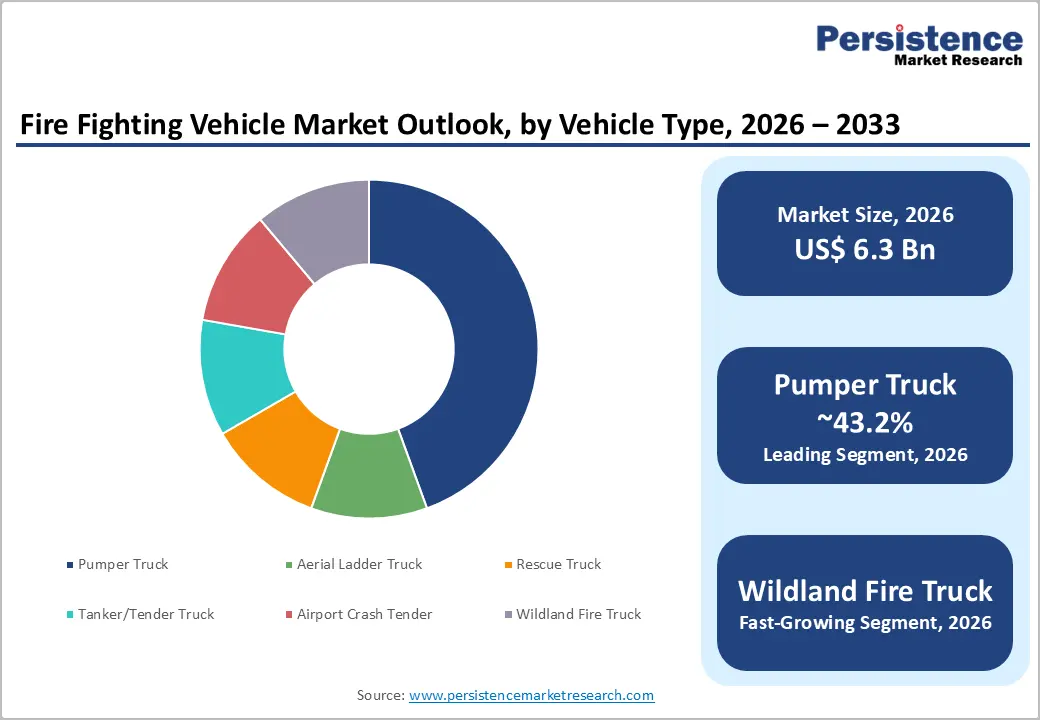

- Leading Vehicle Type: Pumper Trucks' 43.2% share dominance is structurally anchored by NFPA 1901 apparatus deployment standards and the universal role of pumper vehicles as the primary first-response unit across all fire department scales globally; replacement cycle regularity, not growth in new station counts, will sustain this segment's revenue leadership through the forecast period.

- Fast-growing Vehicle Type: Wildland Fire Trucks represent the fastest-growing vehicle type segment, with procurement volumes accelerating as U.S. federal agencies, Australian state rural fire services, and Southern European forestry ministries execute multi-year fleet expansion programmes. The U.S. Forest Service alone operates over 1,700 engines across its national forest system with documented plans to expand capacity.

- Leading Propulsion Type: Battery electric vehicle propulsion is the pivotal strategic opportunity within the firefighting vehicle market, with California's Advanced Clean Fleets regulation and the EU's Euro 7 framework collectively mandating zero-emission procurement milestones that will force fleet electrification decisions at major metropolitan fire departments before the end of the decade, rewarding OEMs with certified commercial BEV platforms today.

Market Dynamics

Drivers – Growing Wildfire Emergencies and Government Fleet Expansion Mandates

The growing frequency and severity of wildfires have become a major driver for the global firefighting vehicle market, prompting governments to accelerate fleet replacement and modernization initiatives. According to the U.S. National Interagency Fire Center (NIFC), more than 64,000 wildfires burned approximately 8.9 million acres across the United States in 2024, highlighting the increasing pressure on firefighting agencies to deploy reliable and specialized apparatus. In response, federal and state authorities have increased investments in wildfire preparedness and emergency response infrastructure.

The U.S. Bipartisan Infrastructure Law (2021) allocated approximately US$ 3.3 billion toward wildfire risk reduction, forest resilience, hazardous fuel management, and firefighting capacity enhancement programs, creating opportunities for fleet upgrades and procurement of advanced wildland fire engines. These programs are encouraging agencies to replace aging apparatus fleets and adopt specialized vehicles such as Type 3, Type 4, Type 5, and Type 6 wildland engines, which offer improved mobility, water delivery efficiency, and off-road performance. Leading manufacturers, including Pierce Manufacturing, Oshkosh Corporation, Rosenbauer, and REV Group, have expanded production capabilities and product offerings to address rising demand from government agencies.

As climate change continues to intensify wildfire risks across North America, Australia, and Southern Europe, sustained public-sector spending on emergency response readiness and fleet modernization is expected to support long-term growth opportunities for fire fighting vehicle manufacturers and suppliers worldwide.

Urbanisation and Industrial Growth Driving Structural Demand in Emerging Economies

Rapid urban expansion in South and Southeast Asia is forcing municipal governments to build fire protection infrastructure from near-zero baselines, creating greenfield procurement opportunities that incumbent OEMs are actively targeting. India's National Disaster Management Authority (NDMA) published updated fire service standards in 2023, mandating minimum apparatus-to-population ratios for cities above 500,000 residents, effectively compelling dozens of state governments to tender new vehicle contracts; Rosenbauer International AG responded by establishing a local assembly partnership in India in 2024 to qualify for government procurement preferences.

This regulatory-driven demand pipeline in India alone is projected to sustain double-digit annual order growth through the late 2020s, reinforcing the Asia Pacific region's importance for global OEM revenue diversification strategies.

Restraints - High Unit Cost and Extended Lead Times Constraining Budget-Limited Municipalities

The average cost of a fully equipped pumper truck now exceeds US$ 650,000, with aerial ladder platforms routinely priced above US$ 1.2 Million, creating significant affordability barriers for smaller and rural municipalities operating under constrained annual capital budgets.

The National Fire Protection Association (NFPA)'s annual survey data consistently shows that roughly 30% of U.S. fire departments serve populations under 2,500, making single-apparatus purchases a multi-year budgetary exercise that dramatically lengthens procurement cycles. New entrants without financing arms or lease-to-own programmes face near-insurmountable barriers in this sub-market segment, while incumbents with established municipal credit arrangements maintain durable competitive moats.

Supply Chain Disruptions and Raw Material Cost Volatility Compressing OEM Margins

Steel, aluminium, and specialised pump components, the primary cost inputs in fire apparatus manufacturing experienced sustained price volatility through 2022–2024 that eroded OEM gross margins by an estimated 200–350 basis points across the industry, per reporting from the Specialty Equipment Market Association (SEMA). Section 232 steel tariffs maintained by the U.S. Department of Commerce add a 25% cost premium on imported steel inputs, disproportionately impacting smaller manufacturers without vertically integrated supply chains.

The mid-tier OEMs operating on thin margins face pressure to either pass costs through to already budget-constrained municipal buyers or absorb margin compression, while Tier-1 manufacturers with long-term supplier agreements weather the cycle more effectively.

Opportunities - Electrification of Fire Apparatus Fleets Targeting Zero-Emission Urban Zones

Fleet electrification represents the single most consequential structural investment opportunity in the fire fighting vehicle market through 2033, and OEMs that establish credible battery-electric platforms before 2027 will lock in fleet specification advantages as municipalities commit to long-duration procurement frameworks. The European Union's Euro 7 emissions regulation, adopted in 2023 and phasing in from 2025, is pushing urban fire departments in Germany, the Netherlands, and Scandinavia to evaluate zero-emission apparatus alternatives, with Rosenbauer International AG's RT (Revolutionary Technology) electric fire truck completing operational trials with the Vienna Fire Brigade in 2024.

Established OEMs with proprietary electric drivetrain platforms are best positioned to capture this opportunity, provided battery energy density improves sufficiently to meet the 8–10 hour operational endurance requirements that remains the primary technical barrier to full adoption.

Airport Expansion and ICAO Safety Standards Driving Specialist ARFF Procurement

Airport Rescue and Fire Fighting (ARFF) vehicle procurement represents a structurally insulated opportunity because International Civil Aviation Organization (ICAO) Annex 14 standards mandate specific apparatus quantities and response-time capabilities as a condition of airport certification, making procurement non-discretionary regardless of broader municipal budget cycles.

The Airport Development Reference Manual published by Airports Council International (ACI) projects that over 220 new airport projects will reach operational status globally between 2024 and 2030, each requiring certified ARFF fleet commissioning before flight operations can commence. Specialist ARFF manufacturers, particularly Oshkosh Airport Products and Rosenbauer with its Panther platform, are best positioned to capture this pipeline, provided they maintain ICAO-compliant certification credentials across evolving aircraft category classifications.

Category-wise Analysis

Vehicle Type Insights

Pumper truck remains the dominant segment in the global fire fighting vehicle market, accounting for 43.2% of total market revenue in 2026. The segment’s leadership is primarily supported by its critical role as the first-response apparatus in firefighting operations across municipal, industrial, and commercial environments. Pumper trucks combine high-capacity water delivery systems exceeding 1,500 gallons per minute with the transportation of hose lines, firefighting equipment, foam systems, and emergency response crews, making them indispensable for urban fire departments worldwide.

Their importance is further reinforced in high-risk industrial facilities such as petrochemical plants, oil terminals, and LNG storage sites, where compatibility with foam injection systems compliant with NFPA 11 standards is essential for suppressing flammable liquid fires. According to the U.S. Fire Administration (USFA), pumper trucks represent the largest category of firefighting apparatus deployed across the country’s nearly 29,705 fire departments, ensuring stable replacement demand and long-term procurement consistency.

Closely linked to rising climate-related disaster risks, the Wildland fire truck is emerging as the fast-growing vehicle type segment in the market. Increasing wildland-urban interface (WUI) fire incidents across North America, Southern Europe, and Australia are driving aggressive government investments in specialized wildfire response fleets.

CAL FIRE alone ordered more than 120 additional Type 3 wildland engines during its 2024–25 procurement cycle to strengthen rapid-response capabilities in wildfire-prone regions. Supporting this trend, Ferrara Fire Apparatus introduced a purpose-built WUI-rated Type 3 platform equipped with compressed-air foam systems (CAFS) and off-road optimized stainless-steel water tanks. Simultaneously, the European Forest Fire Information System (EFFIS) reported above-average burned areas across Southern Europe in 2023, prompting countries such as Spain, Portugal, and Greece to accelerate wildland firefighting vehicle procurement programs through 2028.

Propulsion Insights

Internal Combustion Engine (ICE) propulsion continues to dominate the global fire fighting vehicle market, accounting for approximately 80.2% share in 2026, equivalent to nearly US$ 5.05 Billion in revenue. The segment’s leadership is primarily driven by the unmatched reliability, long operational range, high torque output, and compatibility with existing firefighting infrastructure across municipal and industrial fire departments worldwide. Diesel-powered fire apparatus remains the preferred choice for high-demand emergency operations because they can simultaneously support high-capacity water pumps, aerial ladder hydraulics, and rescue equipment without compromising operational performance.

Major firefighting agencies such as the New York City Fire Department (FDNY), which operates one of the world’s largest diesel-based fleets with over 200 front-line engine companies, continue to rely heavily on ICE-powered vehicles for urban emergency response. In addition, engineering standards such as the SAE International J1834 pump certification framework are currently optimized around diesel power take-off systems, creating a strong technological and infrastructure lock-in for conventional propulsion platforms. The long operational lifespan of firefighting vehicles, typically 15–20 years under NFPA 1901 guidelines, further ensures sustained demand for ICE-powered apparatus, spare parts, and maintenance services through the mid-2040s.

While ICE propulsion maintains market leadership, Battery Electric Vehicle (BEV) propulsion is emerging as the fastest-growing segment, supported by rising net-zero emission targets and stricter environmental regulations. Municipal governments and emergency response agencies are increasingly investing in zero-emission firefighting fleets to reduce operational emissions and fuel dependency. In 2023, Magirus GmbH delivered Europe’s first series-production all-electric aerial ladder truck, the M32L AT Electric, establishing a major milestone for electric fire apparatus commercialization.

The Los Angeles Fire Department incorporated electric vehicle trials into its 2024 fleet modernization strategy in alignment with California’s Advanced Clean Fleets regulation introduced by the California Air Resources Board (CARB), which mandates progressive zero-emission procurement targets for public agencies beginning in 2027. These regulatory developments, combined with advancements in high-voltage chassis systems and battery technologies, are expected to significantly accelerate BEV adoption across the global fire fighting vehicle market during the forecast period.

End-user Insights

Municipal Fire Departments continue to dominate the global fire fighting vehicle market, accounting for 47.7% of total market revenue in 2026, equivalent to nearly US$ 3.01 Billion. The segment’s leadership is primarily driven by the legally mandated nature of municipal fire protection services and the highly structured fleet replacement cycles followed by urban fire authorities worldwide. Major metropolitan departments such as the London Fire Brigade, Tokyo Fire Department, and Chicago Fire Department regularly implement multi-year procurement programs covering pumper trucks, aerial ladder trucks, rescue vehicles, and advanced emergency response apparatus.

In addition, compliance standards established under NFPA 1901 and accreditation frameworks from the Commission on Fire Accreditation International (CFAI) require departments to continuously evaluate vehicle age, operational reliability, and safety performance, creating a stable and recurring procurement environment for OEM manufacturers. Public funding support further strengthens this segment, with the U.S. Congressional Research Service reporting that federal fire apparatus assistance programs have distributed more than US$ 8 Billion since 2001 to support municipal fleet modernization initiatives.

Closely linked to rising climate-related emergencies, Forestry & Wildland Agencies are emerging as the fastest-growing end-use segment in the market. The increasing frequency and severity of wildfires across North America, Australia, and Southeast Asia are driving substantial investments in specialized wildland firefighting fleets capable of operating in remote and rugged terrains. Supporting this trend, the U.S. Bureau of Land Management introduced a long-term wildfire strategy focused on expanding initial-attack suppression capacity through additional procurement of Type 6 and Type 7 wildland engines.

Simultaneously, Morita Holdings Corporation expanded exports of wildland firefighting vehicles to Southeast Asian forestry agencies, particularly in Indonesia and Malaysia, where governments are strengthening wildfire response infrastructure to combat escalating peat-fire incidents across the region.

Regional Insights

North America Fire Fighting Vehicle Market Trends and Insights

North America accounts for 32% of the global fire fighting vehicle market in 2026, representing US$ 2.02 billion, anchored by the United States' mature but actively refreshing municipal fleet base and Canada's growing wildland apparatus procurement activity. The National Fire Protection Association (NFPA)'s apparatus replacement guidelines and federally funded grant mechanisms create structurally consistent procurement rhythms that insulate the region from severe demand cyclicality.

Canada's Public Safety Canada department increased wildfire preparedness funding by C$ 256 Million in its 2023 budget, channelling a portion toward provincial fire agency fleet expansion, a forward signal that North American regional demand will remain above historical averages through 2028.

United States Fire Fighting Vehicle Market Size

The United States fire fighting vehicle market represents 80.2% of the North America regional market in 2026, equivalent to US$ 1.62 Billion, driven by the combination of one of the world's largest municipal fire department networks and sustained federal apparatus grant disbursements.

Pierce Manufacturing's backlog of apparatus orders reported at over 2,500 units in its 2023 annual disclosures illustrates the depth of structural demand that keeps U.S.-based OEMs operating at near-capacity. Ongoing fleet electrification mandates from California and New York state governments will further reshape the U.S. procurement mix toward hybrid and BEV platforms by the late 2020s.

Europe Fire Fighting Vehicle Market Trends and Insights

Europe accounts for 22.4% of the global fire fighting vehicle market in 2026, representing US$ 1.41 Billion, with demand shaped by the dual pressures of ageing fleet replacement needs and increasingly stringent EU-level emissions regulations targeting public procurement. The European Commission's Clean Vehicles Directive (2019/1161), which requires member states to set minimum procurement thresholds for clean-energy vehicles in public sector tenders, is directly compelling fire departments in Western Europe to evaluate electric and hybrid apparatus configurations.

Southern European governments, particularly Spain and Italy are accelerating aerial and wildland apparatus procurement in direct response to record fire seasons documented by Copernicus Climate Change Service satellite data through 2023, reinforcing the region's above-average CAGR trajectory.

Germany Fire Fighting Vehicle Market Size

The Germany fire fighting vehicle market represents 28.9% of the Europe regional market in 2026, equivalent to US$ 0.41 Billion, driven by Germany's exceptionally dense municipal fire service network of over 1 Million volunteer and professional firefighters organised under 16 state fire services. Albert Ziegler GmbH and Magirus GmbH dominate domestic procurement through entrenched OEM relationships with German municipal procurement authorities. Germany's federal Digitalisation and Emergency Services Modernisation Programme is funding command-and-control vehicle upgrades across Länder-level fire services through 2027, sustaining elevated procurement volumes.

United Kingdom Fire Fighting Vehicle Market Size

The United Kingdom fire fighting vehicle market represents 20.2% of the Europe regional market in 2026, equivalent to US$ 290 msillion, with procurement concentrated among 45 territorial fire and rescue services operating under frameworks set by the Home Office Fire and Rescue Directorate. The UK Government's Net Zero Strategy commits public sector fleet procurement to zero-emission targets, and the London Fire Brigade launched an electric vehicle trialling programme in 2024 that is influencing procurement specifications across other English regional services. This electrification transition will drive incremental vehicle capex as departments acquire new BEV platforms alongside existing ICE fleet maintenance obligations through the early 2030s.

France Fire Fighting Vehicle Market Size

The France fire fighting vehicle market represents 17.9% of the Europe regional market in 2026, around procurement by 99 departmental fire and rescue services (SDIS) coordinated through the Direction Générale de la Sécurité Civile et de la Gestion des Crises (DGSCGC). France's Plan National Forêt et Bois, updated in 2023, includes specific funding allocations for wildland fire apparatus procurement by SDIS in fire-prone southern departments. Gimaex GmbH maintains a strategically important manufacturing and service presence in France, positioning it to capitalise on SDIS tender activity through the forecast period.

Asia Pacific Fire Fighting Vehicle Market Trends and Insights

Asia Pacific is poised for 36.8% of the global fire fighting vehicle market in 2026 making it the world's leading regional market by share and the one experiencing the most structurally broad-based demand expansion. China's urban fire infrastructure investment, Japan's seismic resilience-driven apparatus upgrades, and India's regulatory-mandated fleet build-out are operating simultaneously a convergence of demand forces unmatched in any other region. The Asian Development Bank (ADB)'s urban resilience financing frameworks, which disbursed over US$ 4 Billion in disaster risk reduction investments across the region in 2023, are indirectly accelerating fire infrastructure procurement in ADB borrower countries throughout Southeast Asia.

China Fire Fighting Vehicle Market Size

The China fire fighting vehicle market represents 43.2% of the Asia Pacific regional market in 2026, equivalent to US$ 1.00 Billion, underpinned by the Ministry of Emergency Management of China's mandate to expand urban fire rescue capacity in Tier 1 and Tier 2 cities as part of the 14th Five-Year Plan (2021–2025) for emergency management infrastructure.

Zoomlion Heavy Industry Science & Technology Co., Ltd. leads domestic production of aerial platforms and large-tonnage pumper equivalents, benefiting from import substitution preferences embedded in government procurement policies. China's rollout of smart city fire management systems requiring compatible apparatus fitted with IoT telemetry is creating a new equipment specification layer that will drive incremental procurement activity through 2030.

Japan Fire Fighting Vehicle Market Size

Japan fire fighting vehicle market represents 19.2% of the Asia Pacific regional market in 2026, equivalent to US$ 450 million, shaped by the Fire and Disaster Management Agency (FDMA) of Japan's systematic apparatus replacement programme targeting units exceeding 15 years of service life. Morita Holdings Corporation dominates the domestic OEM landscape, supplying the majority of Japan's approximately 170,000 fire apparatus units through long-standing relationships with municipal fire bureaus. Japan's national Resilience Programme, extended through 2030, allocates dedicated capital for disaster response vehicle upgrades in earthquake-prone prefectures, sustaining predictable near-term procurement volumes.

India Fire Fighting Vehicle Market Size

India fire fighting vehicle market represents 11.1% of the Asia Pacific regional market in 2026, equivalent to US$ 0.26 Billion, at an early but rapidly accelerating stage of formalised apparatus procurement driven by urban growth and new regulatory standards. The Bureau of Indian Standards (BIS) issued updated fire vehicle specifications under IS 950 in 2023, providing a technical procurement baseline that state fire departments are now using to run competitive tender processes for the first time at scale. As India's smart cities mission matures and fire department staffing expands under Home Ministry directives, the country's apparatus import volumes and domestic production capacity are both forecast to scale materially by 2028.

South Korea Fire Fighting Vehicle Market Size

South Korea fire fighting vehicle market represents 11.4% of the Asia Pacific regional market in 2026, equivalent to US$ 260 million, structured around procurement by the National Fire Agency (NFA) of Korea, which manages a nationwide fleet modernisation programme under the government's 119 Emergency Services expansion plan. South Korea's Ministry of the Interior and Safety allocated a record ? 320 Billion to fire service infrastructure in its 2024 budget, including new apparatus for metropolitan fire stations in Seoul, Busan, and Incheon. South Korea's advanced domestic manufacturing base including Doosan and Hyundai industrial vehicle platforms positions the country to develop export-capable fire apparatus within the forecast period.

Competitive Landscape

Market Structure Analysis

The global fire fighting vehicle market operates as a moderately consolidated oligopoly at the premium end, with Rosenbauer International AG, Oshkosh Corporation (through Pierce Manufacturing and Oshkosh Airport Products), and REV Group, Inc. collectively commanding an estimated 40–45% of global revenue, per industry association data from the Fire Apparatus Manufacturers' Association (FAMA). Competition pivots on three dimensions: long-cycle government contract relationships, the breadth of the apparatus type portfolio, and the ability to deliver certified compliance with jurisdiction-specific standards such as NFPA 1901 and EN 1846.

The most significant disruptive dynamic right now is electrification Magirus GmbH and Rosenbauer are executing first-mover strategies with commercial electric platforms, while North American incumbents including E-ONE Inc. and Spartan Emergency Response are accelerating hybrid-electric chassis programmes to avoid ceding specification leadership in the upcoming zero-emission procurement cycle.

Key Market Developments

- In 2026, the Indian Army signed a procurement contract with Swadeshi Empresa Pvt. Ltd. under the Innovation for Defence Excellence (iDEX) initiative to acquire advanced unmanned firefighting vehicles, enhancing autonomous disaster-response capabilities and hazardous combat-zone fire suppression operations for defense applications.

- In 2025, Mercedes-Benz Special Trucks showcased advanced all-terrain firefighting and rescue vehicles, including the Unimog tank fire truck and Atego HLF 10, highlighting increasing demand for high-mobility emergency response solutions in disaster management and rescue operations.

- In 2025, Bokaro Steel Plant inaugurated a state-of-the-art firefighting facility equipped with advanced fire response vehicles and emergency infrastructure, strengthening industrial safety standards and improving emergency preparedness across large-scale steel manufacturing operations in India.

- In 2024, Rosenbauer International AG announced the series production of its RT electric fire truck platform for European municipal customers following successful operational validation trials conducted with the Vienna Fire Brigade.

- In 2024, Oshkosh Corporation secured a multi-year contract with the U.S. Department of Defense for next-generation P-19R aircraft rescue and firefighting vehicles, aimed at replacing ageing P-19 units across multiple Air Force bases worldwide.

- In 2023, REV Group, Inc. completed a manufacturing capacity expansion at its E-ONE facility in Ocala, Florida, adding a dedicated stainless-steel pumper truck production line to address an order backlog exceeding 18 months.

Companies Covered in Fire Fighting Vehicle Market

- Rosenbauer International AG

- Oshkosh Corporation (Pierce Manufacturing)

- REV Group, Inc.

- Magirus GmbH

- Morita Holdings Corporation

- Albert Ziegler GmbH

- Bronto Skylift Oy Ab

- E-ONE Inc.

- Ferrara Fire Apparatus

- Spartan Emergency Response

- NAFFCO

- Gimaex GmbH

- W.S. Darley & Co.

- TATRA TRUCKS a.s.

- Zoomlion Heavy Industry Science & Technology Co., Ltd.

Frequently Asked Questions

The global fire fighting vehicle market is valued at US$ 6.30 Billion in 2026 and is projected to reach US$ 9.85 Billion by 2033, expanding at a CAGR of 6.6%. The primary growth catalyst is accelerating municipal fleet replacement activity funded by government grant mechanisms such as FEMA's Assistance to Firefighters Grant programme and regulatory mandates requiring apparatus upgrades across urban and wildland fire agencies globally.

Two structural drivers dominate: first, escalating wildfire frequency and WUI expansion compelling government agencies to procure purpose-built wildland apparatus at volumes not seen in prior decades; second, the International Civil Aviation Organization (ICAO)'s non-discretionary ARFF fleet certification requirements tied to over 220 new airport openings projected globally by 2030, ensuring sustained specialist vehicle procurement independent of broader public sector budget constraints.

Pumper Trucks hold the largest share at 43.2% of the global market in 2026, driven by their universal deployment as the primary first-response apparatus across all department sizes and their dual capability for structural firefighting water delivery and crew transport. This segment faces minimal disruption risk through 2033 because NFPA 1901 apparatus standards institutionalise the pumper truck's role in department deployment protocols, and the 15–20 year asset life cycle generates predictable replacement demand regardless of macroeconomic conditions.

Asia Pacific leads the global fire fighting vehicle market with 36.8% share and US$ 2.32 Billion in revenue in 2026, driven by China's 14th Five-Year Plan emergency management infrastructure investment and Japan's systematic apparatus replacement programme managed by the Fire and Disaster Management Agency (FDMA). India's newly mandated fire apparatus procurement standards and South Korea's record ₩ 320 Billion fire service budget for 2024 ensure the region's dominance will strengthen, not moderate, through 2033.

Fleet electrification represents the highest-value structural opportunity, with OEMs that establish certified BEV fire apparatus platforms before 2027 positioned to capture specification advantages as metropolitan governments in California and the EU execute zero-emission procurement mandates. The enabling condition is battery energy density reaching thresholds sufficient to sustain 8–10 hours of pumping and aerial operations a milestone that Magirus GmbH and Rosenbauer International AG are actively engineering toward with their current commercial electric platform programmes.