- Processed Food

- Sauerkraut Market

Sauerkraut Market Size, Share, and Growth Forecast, 2026 - 2033

Sauerkraut Market by Product Type (Liquid, Solid), Packaging (Jars, Cans, Pouches), Distribution Channel (Supermarkets / Hypermarkets, Departmental Stores, Online, Others), and Regional Analysis for 2026 - 2033

Sauerkraut Market Share and Trends Analysis

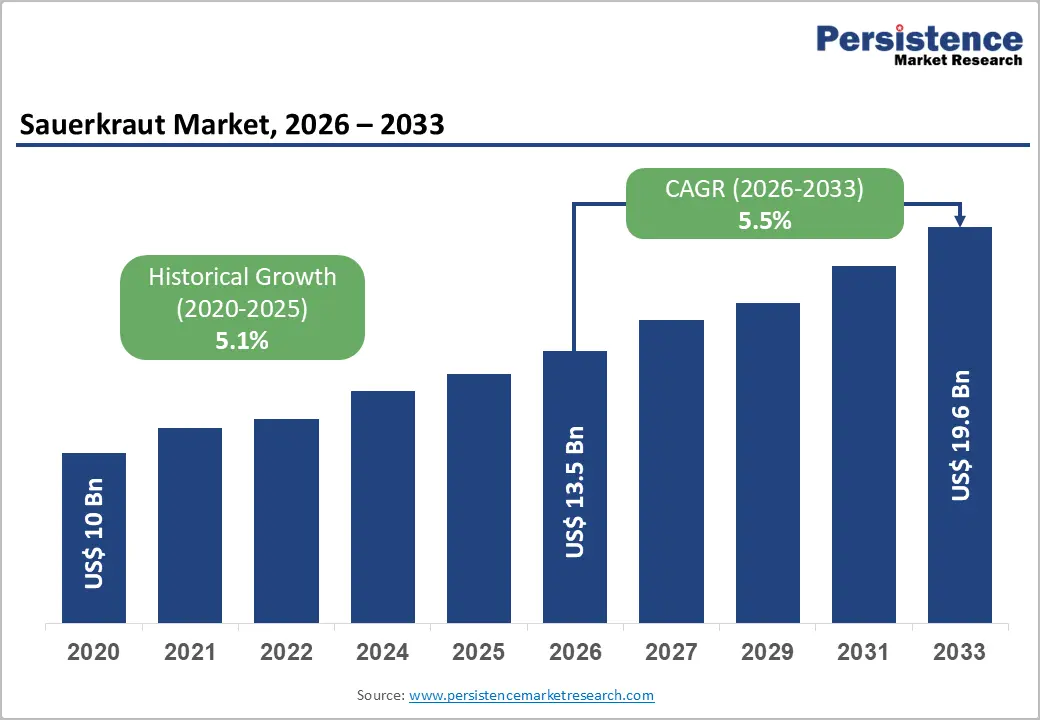

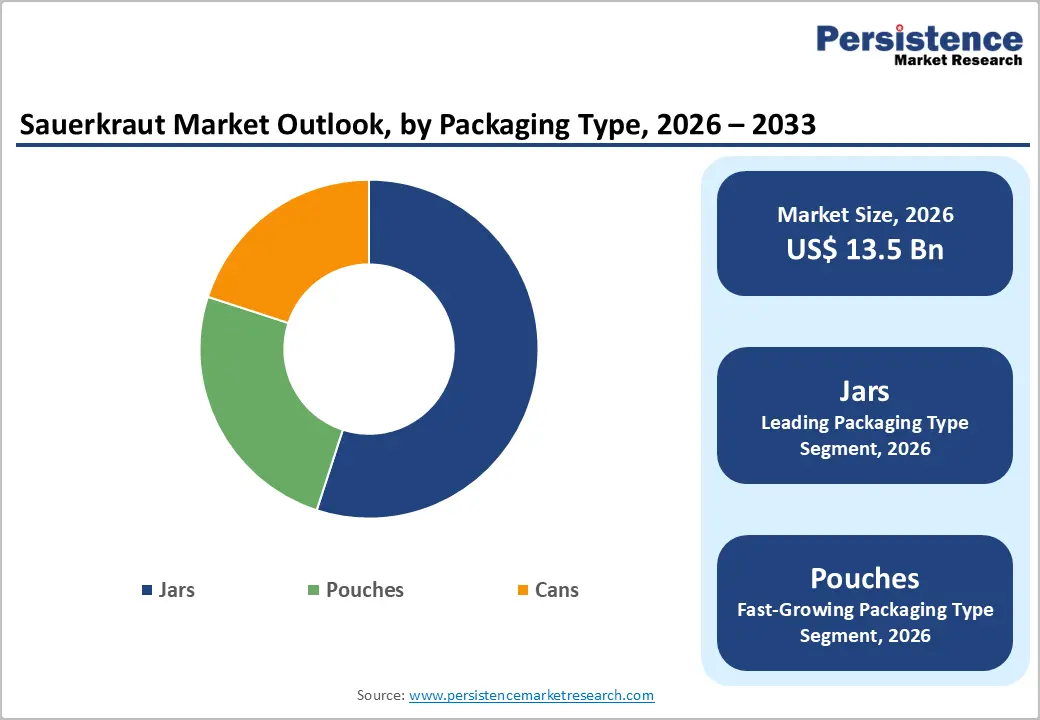

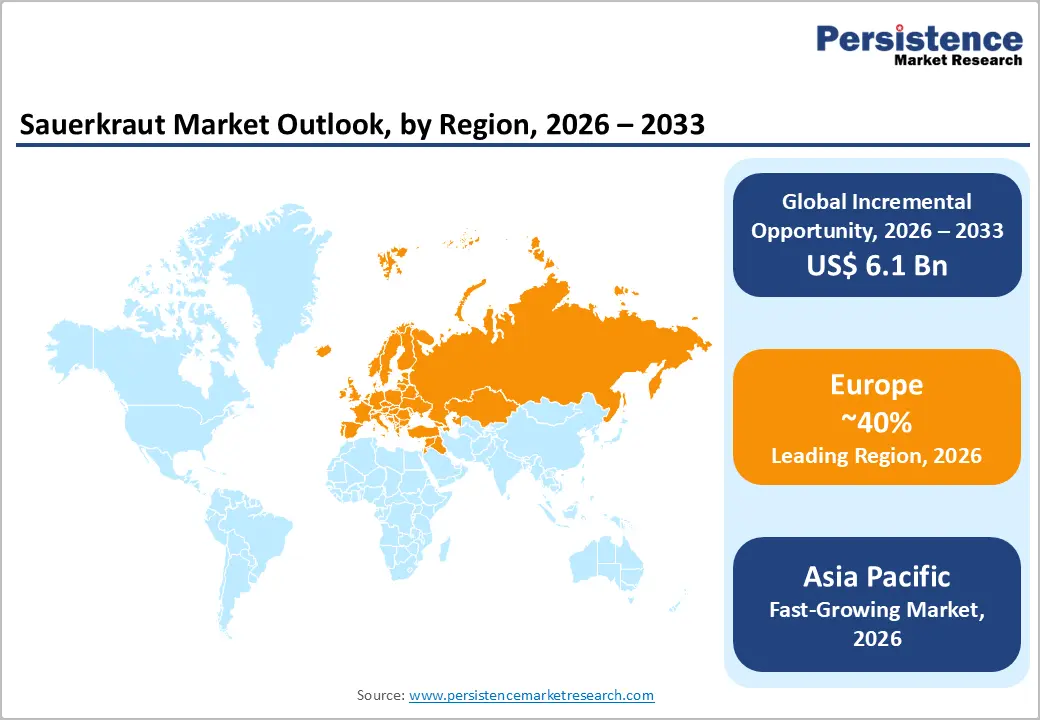

The global sauerkraut market size is likely to be valued at US$13.5 billion in 2026 and is estimated to reach US$19.6 billion by 2033, growing at a CAGR of 5.5% during the forecast period 2026−2033, driven by rising consumer awareness of gut health and increasing demand for probiotic-rich foods.

Growth is supported by plant-based diets and fermented vegetable consumption in urban populations. Retail expansion improves access through packaged formats and modern distribution channels. Technology in controlled fermentation improves shelf life and product consistency. Cold chain infrastructure supports wider geographic availability and reduced spoilage. Regulatory support for minimally processed foods strengthens market legitimacy.

Key Industry Highlights:

- Leading Product Type: Solid product type is projected to hold around 67% share in 2026, driven by strong traditional consumption patterns and stable demand across retail supply chains.

- Fastest-growing Product Type: Liquid format is expected to record the fastest growth, supported by functional beverage integration and probiotic wellness adoption.

- Leading Packaging Type: Jar packaging is estimated to account for around 55% share in 2026, driven by preservation efficiency, consumer trust, and strong retail visibility.

- Fastest-growing Packaging Type: Pouch packaging is forecast to be the fastest-growing segment, supported by convenience demand and logistics efficiency improvements.

- Dominant Region: Europe is projected to account for around 40% share in 2026, driven by a strong cultural consumption base, established fermentation practices, and regulatory alignment.

- Fastest-Growing Region: Asia Pacific is forecast to be the fastest-growing region from 2026 to 2033, supported by dietary transition, urbanization, and expanding health awareness.

- Competitive Environment: The market reflects a moderately fragmented structure, with leading participants such as Nestlé and Danone maintaining positioning through scale advantages, distribution integration, and product portfolio diversification.

- Innovation Trends: Advances in controlled fermentation systems, probiotic stabilization technologies, and digital retail expansion are driving product differentiation and accelerating commercial adoption across health-oriented food categories.

DRO Analysis

Driver - Rising Demand for Probiotic Foods driven by Gut Health Awareness

Consumer shift toward preventive nutrition strengthens demand for probiotic-rich foods. Rising awareness of gut microbiome balance increases preference for fermented vegetable products in daily diets. Functional food positioning supports wider acceptance across retail and food service channels. Dietary transition toward plant-based eating patterns enhances the relevance of fermented vegetables as supportive digestive health components. A 2025 update from the United States Department of Health and Human Services reported growing inclusion of gut health-focused dietary patterns in national nutrition surveys, reflecting stronger public attention toward digestive wellness.

Food manufacturers respond through the expansion of controlled fermentation systems and standardized processing methods. This improves product consistency and supports repeat purchase behavior among urban consumers. Retail penetration across supermarkets and online grocery platforms enhances product visibility and availability. Packaging innovations extend shelf stability and reduce distribution losses. Nutrition professionals increasingly reference fermented foods in dietary guidance frameworks, reinforcing structured consumer adoption across preventive health-driven consumption patterns.

Restraint - Low Consumer Familiarity in some Emerging Markets Limits Adoption

Limited consumer exposure in emerging economies restricts the acceptance of fermented vegetable products. Taste preferences in many regions remain centered on fresh, fried, or heavily spiced foods, reducing willingness to trial sour fermented variants. Awareness of probiotic benefits remains low, which weakens perceived functional value during purchase decisions. Retail environments in tier 2 and tier 3 cities show limited shelf presence of specialty health food categories, reducing visibility and impulse demand.

Weak product education from distributors and retailers reduces understanding of fermentation-based nutrition benefits. Cultural food habits influence preference for locally familiar side dishes, limiting substitution with non-native fermented products. Limited culinary integration in regional recipes reduces repeat consumption patterns. Price sensitivity in emerging markets further restricts willingness to adopt premium packaged fermented foods, slowing overall category penetration across mass consumer segments.

Opportunity - Growth of Plant-based and Functional Food Categories Supports Expansion of Fermented Products

Plant-based and functional food adoption shifts demand toward nutrient-dense, minimally processed options. Sauerkraut aligns with digestive wellness positioning and fiber-focused diets. Retail innovation in ready-to-eat fermented vegetables improves shelf visibility across premium grocery and convenience channels. Examples include refrigerated probiotic bowls in Whole Foods-style formats and fermented vegetable mixes in European deli sections. Controlled fermentation systems support uniform taste profiles and longer shelf stability for broader distribution.

Market traction strengthens through dietary guidance and institutional nutrition, focusing on plant-forward eating patterns. The 2025 USDA Dietary Guidelines Advisory Committee scientific review identifies plant-forward dietary patterns as a leading preventive nutrition direction in public health frameworks. E-commerce platforms such as Amazon Fresh and BigBasket expand access in non-urban regions. Food manufacturers integrate fermented vegetables into salad kits and functional meal solutions, reinforcing cross-category demand growth in health-oriented retail ecosystems.

Category-wise Analysis

Product Type Insights

Solid format is anticipated to secure the 67% market share in 2026, reflecting strong consumer preference for traditional fermented cabbage texture and culinary versatility. Use in sandwiches, salads, and side dishes supports consistent demand. Packaged jars and cans improve shelf stability and retail distribution across supermarkets and food service outlets. Strong integration into European cuisine traditions and established supply chains further strengthen steady consumption across household and commercial applications.

Liquid format is expected to be the fastest-growing segment, propelled by functional beverage adoption and digestive health trends. Integration into wellness shots and probiotic drinks supports growth. Health cafes and nutraceutical channels expand visibility, while improved fermentation and filtration technologies enhance taste consistency and safety. Rising consumer experimentation with gut health beverages and expanding online wellness retail platforms further accelerate adoption across urban health-focused populations.

Packaging Insights

Jars are poised to dominate with the 55% of the sauerkraut market in 2026, powered by strong retail shelf stability, consumer trust in visible product integrity, and traditional packaging familiarity. Glass jar formats support fermentation preservation and reduce spoilage risk in long storage cycles. Examples include widespread use in European supermarket chains for branded fermented vegetables. Strong adoption across Germany and Poland supports steady household demand. Retail merchandising efficiency and clear product visibility reinforce repeat purchase behavior in household consumption segments.

Pouches are estimated to be the fastest-growing segment, fueled by portability demand and the expansion of convenience-oriented consumption patterns. Lightweight packaging reduces logistics costs and improves supply chain efficiency. Examples include single-serve fermented food pouches introduced in urban convenience stores and health food outlets across Asia and North America. Food service applications increasingly integrate flexible packaging formats for portion control. Sustainability trends promoting reduced plastic usage and lower carbon packaging footprint further accelerate adoption across modern retail channels.

Regional Insights

North America Sauerkraut Market Trends

North America is characterized by rising demand for probiotic-rich and functional food products driven by increasing consumer focus on digestive wellness and preventive nutrition. The U.S. shows strong adoption through brands such as Bubbies and Cleveland Kitchen, while Canada reflects growth across organic retail chains. Supermarkets, specialty stores, and e-commerce platforms ensure wide availability and consistent consumption patterns across urban households.

Growth momentum is reinforced by product innovation in fermented vegetable applications within health beverages, snacks, and fusion cuisine formats. Mexico shows rising integration in urban wellness diets and modern retail outlets. Food service chains include fermented vegetables in salads and plant-based meals. Cold chain logistics support quality stability, while digital grocery platforms expand access to functional probiotic products across diverse consumer segments.

Europe Sauerkraut Market Trends

Europe is expected to lead with an estimated 40% of the sauerkraut market share in 2026, supported by deep fermentation food heritage and high-frequency household consumption patterns. Strong demand is reinforced in Germany, Poland, and France, where sauerkraut is integrated into daily meals such as sausages and ready-to-eat sides. Companies such as Hengstenberg GmbH, Kühne + Sohn GmbH & Co., and Deleeuw Organic influence large-scale retail supply. Established supermarket penetration across REWE and Tesco supports consistent availability and stable consumer turnover.

Demand strength is reinforced through culinary integration into deli, bakery, and packaged meal categories across mass retail systems. Production efficiency is strengthened through industrial fermentation facilities operated by Kühne and Bionade-linked supply networks. Export activity within European trade corridors supports cross-border distribution to Italy and Spain. The presence of traditional fermented food consumption in Poland and the Czech Republic sustains repeat demand cycles. Strong retail branding and standardized cold-chain systems enhance product consistency across packaged jar and pouch formats.

Asia Pacific Sauerkraut Market Trends

Asia Pacific is forecast to be the fastest-growing market for sauerkraut, stimulated by rapid dietary diversification, rising functional food adoption, and expanding urban retail infrastructure. China shows increasing incorporation of fermented vegetables within premium health food channels and wellness-focused supermarkets. India demonstrates rising demand from metro city consumers adopting probiotic-rich diets and packaged fermented products through modern retail formats. Japan reflects a strong integration of fermented foods into convenience store ecosystems and aging population nutrition planning. South Korea exhibits growing acceptance of Western fermented vegetable variants through fusion cuisine and café-style food services.

Market acceleration is reinforced through the expansion of cold chain logistics, digital grocery platforms, and premium health retail outlets across metropolitan clusters. Food manufacturers are introducing localized flavor adaptations to align with regional taste profiles and reduce sensory resistance. The rapid growth of e-commerce platforms supports wider product discovery among younger consumers. Investment in food processing technologies improves shelf stability and quality consistency for fermented vegetable products. The rising influence of nutrition labeling systems and wellness-focused branding strengthens consumer confidence across emerging urban dietary segments.

Competitive Landscape

The global sauerkraut market reflects a moderately fragmented structure with the presence of multinational packaged food companies and regional fermented food producers. Nestlé S.A., Danone S.A., and Hain Celestial Group strengthen retail dominance through large-scale distribution networks and branded packaged food portfolios. Market competition remains shaped by product consistency, fermentation standards, and shelf placement efficiency across supermarkets.

Bubbies Fine Foods, Kühne Group, and Eden Foods compete through organic positioning and functional food differentiation strategies. Regional producers focus on artisanal fermentation methods and localized taste preferences. Competitive intensity is influenced by branding strength, cold chain reliability, and regulatory compliance. Innovation in clean label formulations and retail expansion supports differentiation across both premium and mass market segments.

Key Industry Developments:

- In July 2025, Cleveland Kitchen’s sauerkraut was featured in USA TODAY Food as Medicine Special Edition, highlighting fermented vegetables as science-backed functional foods supporting gut health and wellness, strengthening mainstream recognition of probiotic-rich dietary solutions in preventive nutrition programs.

- In April 2025, Bubbies Fine Foods and Wildbrine expanded their fermented product portfolios through new sauerkraut, kimchi, and pickled vegetable launches across Whole Foods Market and other retail channels, strengthening innovation momentum in probiotic-rich food categories.

Companies Covered in Sauerkraut Market

- Hain Celestial Group

- Bubbies Fine Foods

- Kühne Group

- Eden Foods

- Hengstenberg GmbH

- Frank’s Kraut

- Reuben’s Kraut

- Cleveland Kitchen

- Wildbrine

- Alnatura

Frequently Asked Questions

The global sauerkraut market is projected to reach US$13.5 billion in 2026.

Rising demand for probiotic-rich fermented foods, supported by growing digestive health awareness and clean-label dietary preferences, drives the sauerkraut market.

The sauerkraut market is poised to witness a CAGR of 5.5% from 2026 to 2033.

Expansion in plant-based diets, functional food innovation, and increasing retail penetration across emerging markets creates key opportunities for the sauerkraut market.

Some of the key market players include Hain Celestial Group, Bubbies Fine Foods, Kühne Group, and Eden Foods.