- Healthcare

- Robotic-Assisted Hip Replacement Market

Robotic-Assisted Hip Replacement Market Size, Share, and Growth Forecast, 2026 - 2033

Robotic-Assisted Hip Replacement Market by Component (Robotic Hardware Systems, Software, Planning Platforms, Consumables, Accessories, Implants, Services), Technology Type (Passive Systems, Semi-active Systems, Active Systems, Autonomous Systems, AI-integrated Robotics, AR-assisted Systems, VR-assisted Systems), End-User (Hospitals, Ambulatory Surgical Centers (ASCs), Orthopedic Clinics, Others), and Regional Analysis for 2026-2033, and Regional Analysis for 2026 - 2033

Robotic-Assisted Hip Replacement Market Share and Trends Analysis

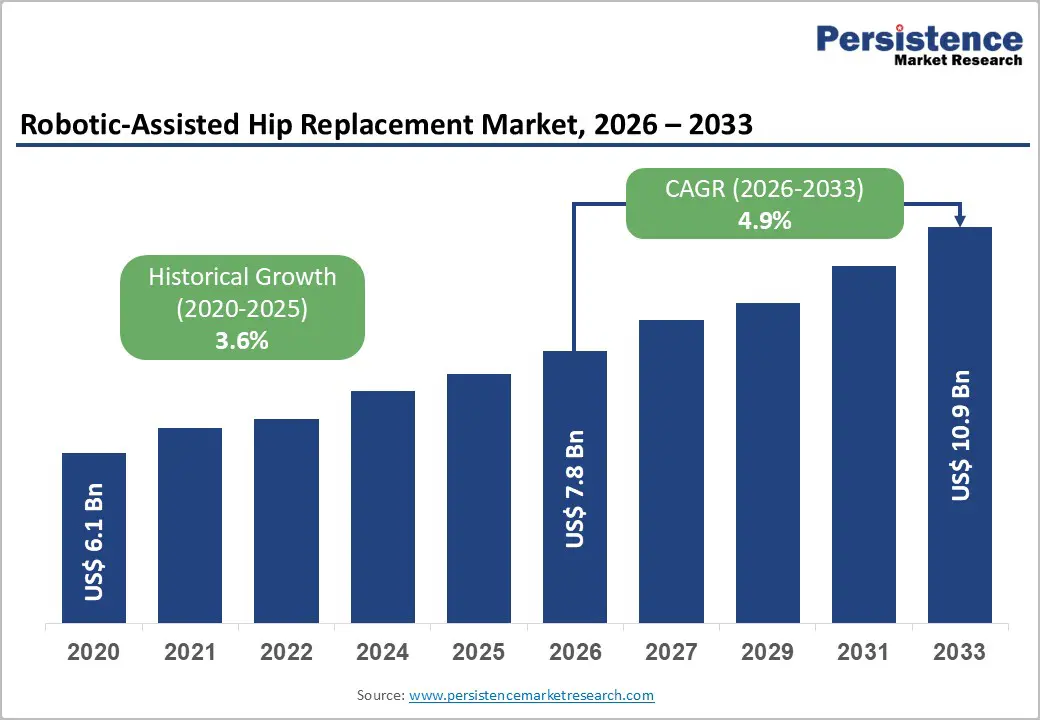

The global robotic-assisted hip replacement market size is likely to be valued at US$ 7.8 billion in 2026, and is projected to reach US$ 10.9 billion by 2033, growing at a CAGR of 4.9% during the forecast period 2026–2033. Market growth is primarily driven by the rising incidence of osteoarthritis and hip fractures, particularly among aging populations, which is significantly increasing the volume of hip replacement procedures worldwide.

The growing preference for minimally invasive and precision-based surgical technologies is further supporting adoption. Healthcare providers are prioritizing improved clinical outcomes, including enhanced implant positioning, shorter recovery times, and reduced revision rates, all of which robotic-assisted systems facilitate. Favorable reimbursement frameworks in developed markets, especially in North America and parts of Europe, are encouraging hospital investments. However, high capital costs, ongoing maintenance expenses, and the need for specialized surgeon training continue to limit widespread adoption in emerging economies.

Key Industry Highlights

- Dominant Components: Robotic hardware systems are set to command around 50% revenue share in 2026, while software and planning platforms are likely to grow the fastest through 2033, driven by increasing adoption of data-driven workflows.

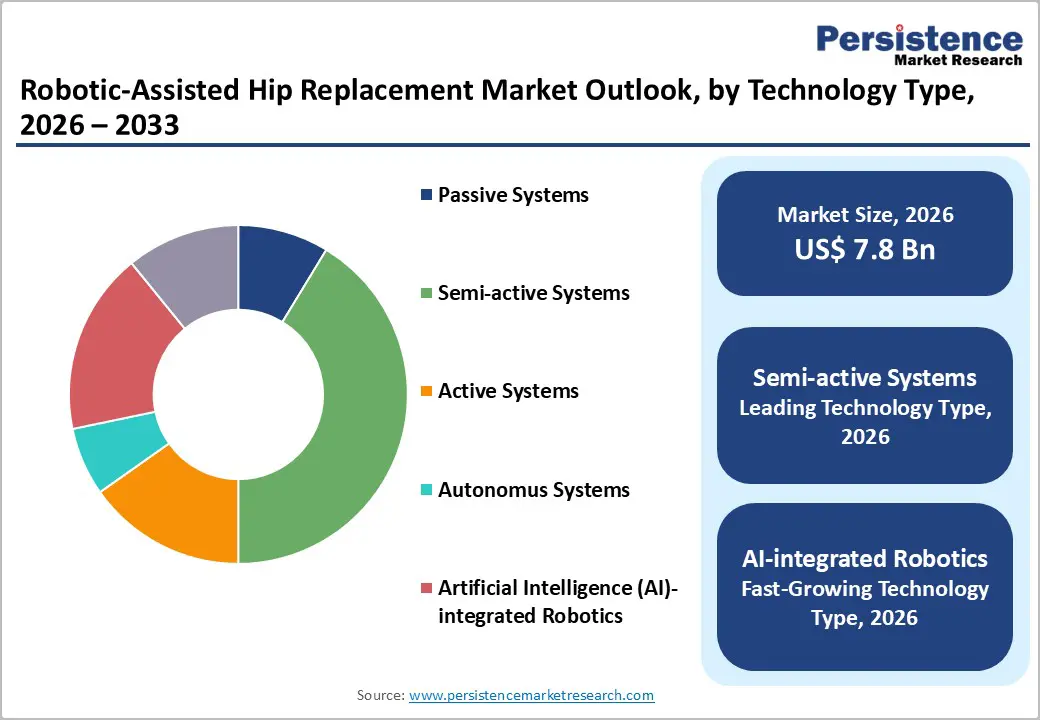

- Leading Technology Types: Semi-active systems are expected to lead with an estimated 38% share in 2026, while AI-integrated robotics are projected to be the fastest-growing at 7.3% CAGR during 2026–2033, reflecting the shift toward precision, automation, and predictive surgical analytics.

- Dominant End-Users: Hospitals are anticipated to account for around 66% of revenue in 2026, while ambulatory surgical centers (ASCs) are likely to be the fastest-growing, supported by the transition toward outpatient and minimally invasive procedures.

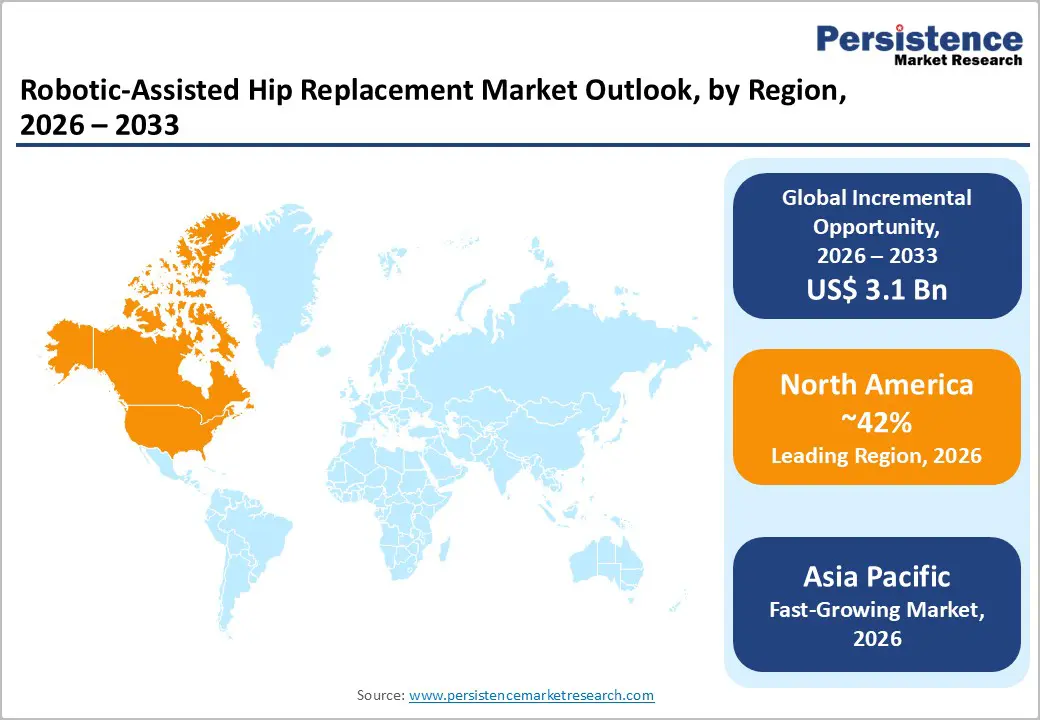

- Regional Leadership: North America is poised to dominate with an estimated 42% share in 2026, while Asia Pacific is projected to register the fastest growth at 6.4% CAGR through 2033, driven by rising procedure volumes in China, India, and Southeast Asia.

- Key Market Trends: Competitive dynamics are increasingly shaped by AI integration, the expansion of outpatient surgical settings, and growing investments in emerging markets, with companies focusing on innovation, cost optimization, and geographic expansion.

| Key Insights | Details |

|---|---|

|

Robotic-Assisted Hip Replacement Market Size (2026E) |

US$ 7.8 Bn |

|

Market Value Forecast (2033F) |

US$ 10.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.6% |

DRO Analysis

Rising Geriatric Population and Increasing Orthopedic Disease Burden

The increasing prevalence of age-related musculoskeletal disorders is a major driver. According to the World Health Organization (WHO), the global population aged 60+ is expected to reach 2.1 billion by 2050, significantly increasing demand for hip replacement procedures. Osteoarthritis alone affects over 528 million people globally, as per the Institute for Health Metrics and Evaluation. In the U.S., the Centers for Disease Control and Prevention (CDC) reports more than 450,000 hip replacements annually, with volumes expected to grow by over 25% by 2030. Robotic-assisted systems enhance surgical accuracy and implant longevity, reducing revision rates by up to 20% and aligning with healthcare systems’ long-term cost-optimization goals.

Recent developments further validate this demand trajectory. In 2025, government-backed hospitals in India, including major public institutions, successfully performed robotic-assisted hip replacements under national health schemes, improving accessibility for elderly patients. Additionally, large-scale public healthcare initiatives are increasingly integrating robotic surgery to address aging-related orthopedic conditions. These real-world implementations highlight how rising disease burden is not only increasing procedure volumes but also accelerating the transition toward precision-driven surgical solutions in both developed and emerging healthcare systems.

Advancements in Robotic Technologies and Expanding Healthcare Investments

The integration of AI, real-time imaging, and data analytics is transforming orthopedic procedures. Robotic systems now offer sub-millimeter accuracy, improving implant positioning and patient-specific surgical planning. The U.S. Food and Drug Administration (FDA) has approved multiple robotic platforms with advanced navigation and haptic feedback systems since 2023. Studies published in The Journal of Arthroplasty in 2024 indicate that robotic-assisted hip surgeries reduce intraoperative errors by approximately 30% compared to conventional methods. These advancements are increasing surgeon confidence and expanding adoption across high-volume surgical centers.

Industry movements in the past years strongly reinforce this technological shift. For instance, the first AI-assisted total hip replacement surgery in the U.S. was successfully performed using advanced planning platforms, demonstrating real-world clinical viability of AI-integrated robotics. Furthermore, national healthcare systems such as the U.K.’s National Health Service (NHS) have announced plans to significantly expand robotic surgery adoption, aiming to have up to 90% of keyhole procedures robot-assisted in the long term. In tandem, hospital networks are investing in robotic infrastructure upgrades and expanding surgical capabilities, signaling sustained capital inflow and institutional commitment toward next-generation orthopedic care.

High Capital Investment and Ongoing Cost Burden

Robotic-assisted surgical systems require a significant upfront investment, typically US$ 1–2.5 million per unit, along with annual maintenance costs exceeding US$ 100,000. In 2025, several mid-sized hospitals in emerging markets delayed adoption due to budget constraints and uncertain return-on-investment (ROI) timelines. Additionally, consumables and software licensing fees increase procedural costs by 10–20%, limiting affordability for patients in price-sensitive markets. These financial requirements make initial investment decisions highly complex for hospital administrators.

Recent industry developments clearly highlight the financial barriers associated with adoption. In 2026, public hospitals in India required corporate social responsibility (CSR) funding to subsidize robotic surgeries, highlighting affordability challenges to wider patient access. Similarly, healthcare leaders in the U.K. have warned that, without increased capital investment, many hospitals may struggle to adopt robotic systems despite a national push to expand. These examples demonstrate that even advanced healthcare systems face funding gaps, reinforcing cost as a critical constraint to widespread market penetration.

Skilled Workforce Gaps and Integration Complexity

Robotic-assisted procedures require specialized training and workflow restructuring. In 2025, multiple healthcare systems reported delays in implementation due to a shortage of trained orthopedic surgeons and support staff. Learning curves can extend to 20–30 procedures per surgeon, impacting initial efficiency. Furthermore, integration with existing hospital IT systems and imaging infrastructure remains complex, especially in low-resource settings. These factors collectively slow down the transition from conventional to robotic-assisted surgical methods.

Operational challenges are further validated by real-world constraints in healthcare systems. Reports from national health systems indicate that expensive robotic equipment remains underutilized due to staff shortages and a shortage of trained personnel, directly affecting productivity and return on investment. Additionally, policymakers in India have highlighted shortages of specialist doctors and resource limitations as key reasons for the delayed adoption of robotic surgery in public hospitals. These workforce and integration gaps continue to slow implementation timelines and limit the scalability of robotic-assisted surgical programs globally.

Expansion in Emerging Markets and Rising Healthcare Access

Emerging economies such as India, China, and Brazil offer significant growth opportunities. These regions account for over 60% of the global population but have relatively low penetration of robotic surgery systems. In 2025, India witnessed increased investments in robotic surgery platforms across private hospital chains. The addressable market in Asia-Pacific alone is estimated to exceed US$ 3 billion by 2030, driven by rising medical tourism and expanding middle-class populations. Growing patient awareness and demand for high-quality surgical outcomes are encouraging hospitals to adopt these advanced technologies. As a result, robotic systems are becoming an important differentiator for healthcare providers in these regions.

Government-led initiatives are further accelerating adoption. In July 2025, the Government of India rolled out a policy boost for robotic surgery training and funding support, enabling public hospitals to co-fund robotic procedures for underprivileged patients. Similarly, China’s National Health Commission (NHC) announced expanded grants for digital healthcare infrastructure in early 2026, aimed at equipping tertiary hospitals with advanced surgical technologies. These programs are enhancing accessibility, reducing procedure backlogs, and strengthening the overall ecosystem for robotic-assisted orthopedic surgery in emerging markets.

AI Integration and Shift toward Outpatient Surgical Care

AI-driven preoperative planning and intraoperative analytics present a high-value opportunity. In 2025, several companies launched AI-enabled platforms that analyze patient-specific anatomy using CT/MRI data, improving implant fit and reducing complications. The AI-enabled robotics segment is expected to contribute over 25% of total market revenue by 2033, as precision medicine gains traction. At the same time, hospitals and surgical centers are focusing on efficiency, minimizing complications, and personalizing care for patients undergoing hip replacements. These advancements support more predictable outcomes and faster patient recovery.

The shift toward outpatient procedures is also creating demand for compact, modular robotic systems. In 2025, ASCs in the U.S. increased adoption of minimally invasive orthopedic procedures by over 15% year over year. The U.S. Centers for Medicare & Medicaid Services (CMS) expanded reimbursement codes for robotic-assisted outpatient procedures in September 2025, providing financial incentives to hospitals and surgical centers. Additionally, media reports in 2026 highlighted rising patient preference for AI-supported robotic surgeries, driven by improved precision and reduced post-operative discomfort. These factors are driving adoption in both hospital and outpatient settings, opening substantial new revenue streams for robotic surgery providers.

Category-wise Analysis

Component Insights

Robotic hardware systems are expected to dominate, accounting for approximately 50% of the robotic-assisted hip replacement market revenue share in 2026, driven by their essential role in robotic-assisted hip replacement procedures. These systems, including robotic arms, navigation units, and integrated imaging modules, enhance surgical accuracy, reduce intraoperative variability, and minimize complications. Hospitals prioritize these high-capital investments to improve patient outcomes and procedural efficiency. In 2025, Mount Sinai Health System in New York expanded its robotic hardware for orthopedic procedures, while Fujita Health University Hospital in Japan added next-generation robotic arms in early 2026, reflecting a global focus on upgrading surgical infrastructure to support growing procedure volumes.

Software and planning platforms are projected to grow at a CAGR of 6.2% through 2033, fueled by AI-driven preoperative planning, intraoperative guidance, and cloud-based collaboration tools. These platforms allow surgeons to run simulations, optimize implant placement, and adjust surgical plans in real time. In 2026, the Cleveland Clinic deployed an AI-enhanced planning platform, and Singapore’s Tan Tock Seng Hospital adopted a cloud-based suite in 2025, enabling remote surgical customization and standardization. This software-focused shift is enhancing recurring revenue streams while supporting data-driven, precision-based orthopedic procedures globally.

Technology Type Insights

Semi-active systems are poised to lead with an estimated 38% of the robotic-assisted hip replacement market share in 2026, combining surgeon control with robotic precision. These systems provide haptic feedback and guided assistance, ensuring safety while allowing real-time clinical adjustments. In 2025, Massachusetts General Hospital expanded its semi-active platforms for joint replacements, and in early 2026, Yonsei Severance Hospital in South Korea added semi-active robotics for orthopedic procedures, improving procedural consistency and surgeon confidence. Their balance of control, precision, and regulatory acceptance continues to drive widespread adoption.

AI-integrated robotics is projected to grow at a 7.3% CAGR through 2033, leveraging machine learning and real-time analytics to optimize surgical outcomes and predict intraoperative challenges. In 2025, Tokyo Medical University Hospital successfully deployed an AI-enhanced robotic system, and in March 2026, Alberta Health Services in Canada tested AI-driven platforms for hip replacements, improving alignment accuracy and reducing surgical time. The adoption of these intelligent systems is accelerating as hospitals prioritize precision, efficiency, and personalized patient care.

Regional Insights

North America Robotic-Assisted Hip Replacement Market Trends

North America is expected to capture roughly 42% of the robotic-assisted hip replacement market value in 2026. This leadership is supported by high surgical volumes, advanced hospital infrastructure, and broad reimbursement frameworks that facilitate access to expensive robotic systems. The U.S. continues to lead adoption due to a well-established private healthcare network, high procedure rates for osteoarthritis-related hip replacements, and investments in precision surgical technologies. Canada also contributes to regional growth via public healthcare initiatives that fund advanced surgical equipment.

Recent industry movements confirm this trend. In 2025, the U.S. Department of Veterans Affairs (VA) announced expanded deployment of robotic surgical platforms across VA hospitals to improve orthopedic care for veterans. In early 2026, Mount Sinai Downtown in Miami added an advanced robotic orthopedic suite to improve procedural accuracy and reduce hospital stays, showcasing how major hospital systems are elevating surgical capabilities. These developments reinforce the region’s continued focus on leveraging innovative surgical technologies to enhance patient outcomes and operational efficiency in orthopedic care.

Europe Robotic-Assisted Hip Replacement Market Trends

Europe is a key contributor to the robotic-assisted hip replacement market growth, with strong adoption in Germany, the U.K., France, and Spain. The region benefits from harmonized medical device regulations under the European Union (EU) Medical Device Regulation (MDR), ensuring that advanced robotic systems meet rigorous safety and performance standards. Germany continues to lead in procedure volumes and hospital investment in orthopedic surgical technologies, while the U.K. leverages coordinated NHS funding to expand access to robotic-assisted interventions across major surgical centers. France and Spain are also gradually increasing adoption through hospital modernization initiatives and technology partnerships.

In mid-2025, Spain’s University Hospital La Paz introduced a new robotic OR suite specifically for joint replacement procedures, improving surgical workflow and patient throughput (hospital-lapaz.es). Additionally, France’s Assistance Publique–Hôpitaux de Paris (AP-HP) expanded robotic surgical programs at multiple facilities in early 2026 to reduce recovery times and optimize outcomes. While cost pressures remain in public health systems, these strategic investments underscore Europe’s focus on value-based surgical care, driving robotics adoption to improve clinical precision and reduce long-term complications.

Asia Pacific Robotic-Assisted Hip Replacement Market Trends

Asia Pacific is projected to be the fastest-growing market for robotics-assisted hip replacement procedures, with a CAGR of around 6.4% through 2033. Key markets include China, Japan, and India. China is scaling domestic production of robotic components and supporting hospital adoption through targeted healthcare investments. Japan remains a technology leader with widespread use of advanced robotic systems in surgical centers. India’s rapidly expanding private healthcare sector and rising medical tourism are major growth catalysts, while ASEAN nations are gradually adopting robotics as health infrastructure improves.

Recent advancements highlight this momentum. In late 2025, Singapore’s National University Hospital reported the launch of a dedicated orthopedic robotic OR to support high-volume joint replacement procedures, raising procedural precision and reducing stay durations. In early 2026, China’s Zhejiang Provincial People’s Hospital inaugurated a center for robotic surgery training and implementation, reflecting government-supported expansion of surgical robotics into provincial healthcare networks. These developments, combined with rising patient awareness and cost-effective care models, are driving robust regional growth and positioning the Asia Pacific as a rapidly emerging market for robotic-assisted hip replacements.

Competitive Landscape

The global robotic-assisted hip replacement market structure is moderately consolidated, with leading players such as Stryker, Johnson & Johnson (DePuy Synthes), Smith+Nephew, and Zimmer Biomet collectively controlling over 50% of total market revenue. These established companies leverage extensive hospital networks, clinical partnerships, and integrated hardware-software platforms to maintain market leadership. They also invest heavily in R&D, focusing on AI-driven surgical planning, enhanced robotic precision, haptic feedback technologies, and modular system development to strengthen competitive advantage.

Regional and niche players such as Medtronic and Globus Medical are concentrating on specialized segments, including outpatient surgical systems and semi-active robotics, while expanding in targeted geographies. High capital requirements, regulatory approvals, and complex integration with hospital IT and imaging infrastructure continue to pose entry barriers. However, digitalization and AI integration are enabling software-centric vendors to collaborate through cloud-based surgical planning platforms. Market consolidation is expected to continue gradually, as leading global firms acquire smaller vendors to expand geographically and technologically, while innovation partnerships between robotics and software providers accelerate adoption in advanced healthcare facilities.

Key Industry Developments

- In January 2026, Smith & Nephew completed the acquisition of Integrity Orthopaedics for US$ 450 million, strengthening its shoulder repair portfolio and integrating soft tissue repair with its handheld robotics under the “RISE” growth strategy;

- In October 2025, Zimmer Biomet acquired Monogram Technologies for US$ 177 million, adding AI-driven semi- and fully autonomous robotics to its ROSA platform to enhance precision in joint replacement.

- In October 2025, Johnson & Johnson announced plans to spin off DePuy Synthes into a standalone orthopedics entity with US$ 9.2 billion in annual sales, enabling J&J to focus on surgical robotics and other high-growth areas.

Companies Covered in Robotic-Assisted Hip Replacement Market

- Stryker Corporation

- Zimmer Biomet Holdings, Inc.

- Smith & Nephew plc

- Johnson & Johnson

- Medtronic plc

- Globus Medical, Inc.

- THINK Surgical, Inc.

- Intuitive Surgical, Inc.

- MicroPort Scientific Corporation

- Corin Group

- OMNIlife Science

- Curexo, Inc.

- Renishaw plc

Frequently Asked Questions

The global robotic-assisted hip replacement market is projected to reach US$ 7.8 billion in 2026.

Rising osteoarthritis incidence, aging population, and adoption of precision robotic surgical technologies are driving market growth.

The market is poised to witness a CAGR of 4.9% from 2026 to 2033.

Expansion in emerging markets, AI-enabled surgical platforms, and growth of outpatient surgical centers are creating new market opportunities.

Stryker, Johnson & Johnson (DePuy Synthes), Zimmer Biomet, Smith+Nephew, and Medtronic are some of the key players in the market.