- Healthcare

- Platelet Rich Fibrin Market

Platelet Rich Fibrin Market Size, Share, and Growth Forecast, 2026 - 2033

Platelet Rich Fibrin Market by Modality (Membrane Form, Liquid Form, Injectable Form), Process Type (Cell Proliferation, Cell Differentiation, Others), Application (Implant Dentistry, Periodontology, Others), and Regional Analysis 2026 - 2033

Platelet Rich Fibrin Market Size and Trends Analysis

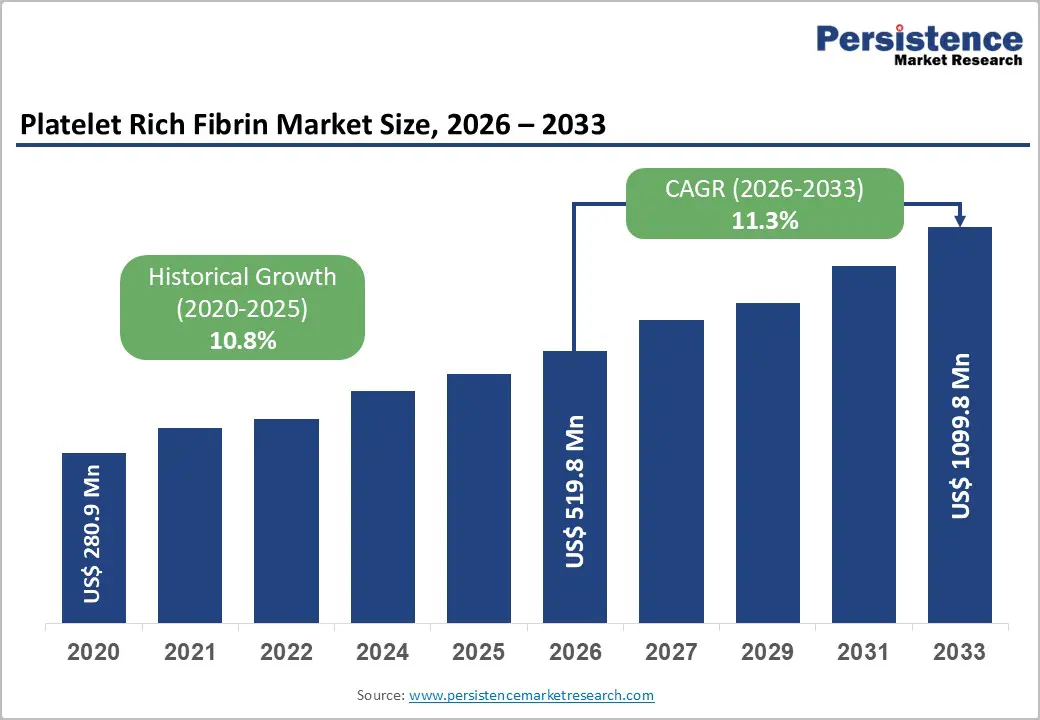

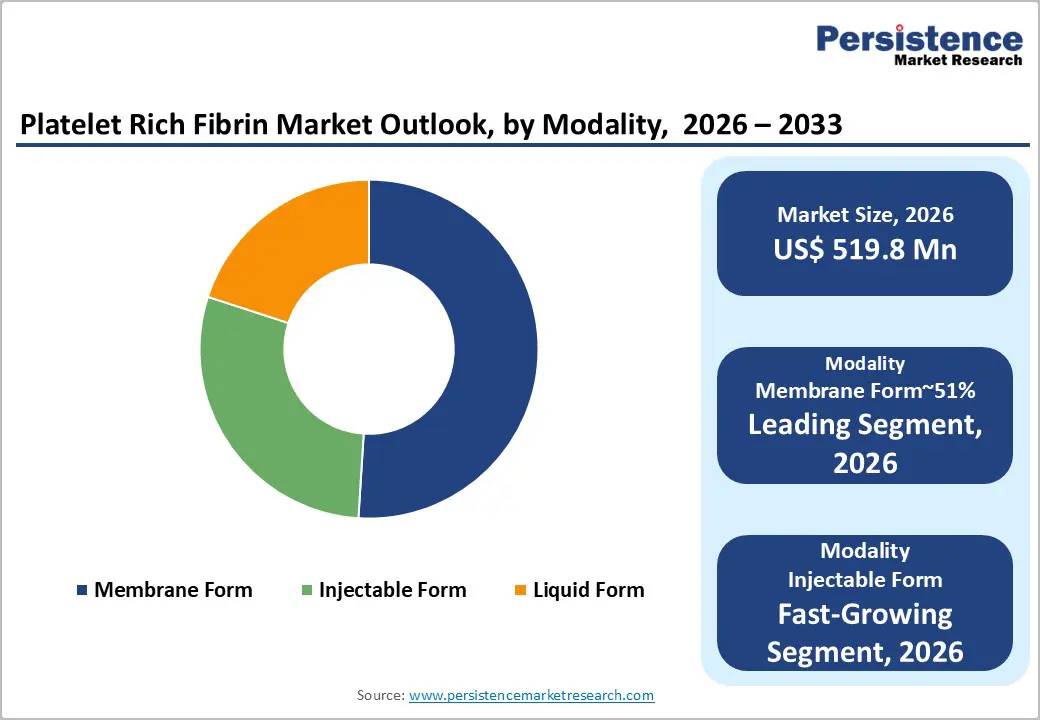

The global platelet rich fibrin market size is likely to be valued at US$519.8 million in 2026 and is expected to reach US$1,099.8 million by 2033, growing at a CAGR of 11.3% during the forecast period from 2026 to 2033, driven by the increasing adoption of biological wound healing solutions in modern surgical settings.

Healthcare professionals are increasingly favoring materials that minimize infection risks during complex procedures, reflecting a broader shift toward natural healing approaches that enhance long-term patient outcomes. Additionally, autologous concentrates offer excellent scaffolding properties that support effective tissue regeneration across a wide range of applications. Ongoing advancements in preparation technologies are further facilitating wider clinical adoption, positioning the market for accelerated growth alongside rising surgical volumes and improved workflow integration.

Key Industry Highlights:

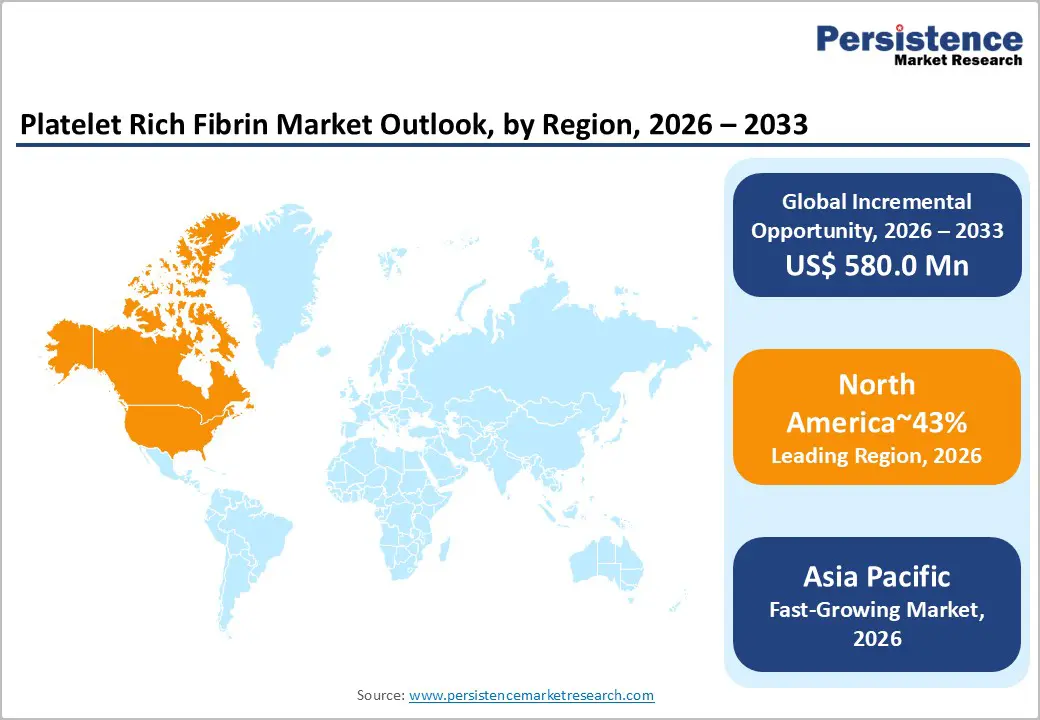

- Leading Region: North America is projected to lead, accounting for approximately 43% share in 2026, supported by high dental implant volumes, robust healthcare infrastructure, and early adoption of advanced regenerative biologics.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest, driven by expanding medical tourism, rising geriatric populations, and increasing investments in specialized dental clinics.

- Leading Modality: Membrane form is expected to lead, accounting for approximately 51% share in 2026, anchored by its critical role as a biological barrier in guided bone regeneration and periodontal surgeries.

- Leading Application: Implant dentistry is anticipated to dominate, accounting for approximately 39% share in 2026, anchored by rising success rates of osseointegration when using fibrin-based scaffolding.

| Key Insights | Details |

|---|---|

|

Platelet Rich Fibrin Market Size (2026E) |

US$519.8 Mn |

|

Market Value Forecast (2033F) |

US$1,099.8 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

11.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

10.8% |

Market Factors - Driver, Restraint, and Opportunity Analysis

Driver Analysis - Autologous Biologic Integration Enhancing Clinical Adoption Dynamics

Regenerative medicine frameworks increasingly prioritize autologous biologic integration to enhance controlled tissue regeneration outcomes. Patient safety considerations are accelerating the substitution away from synthetic graft materials toward biologically compatible alternatives. Utilization of patient-derived blood components eliminates immunogenic rejection risks and cross-contamination concerns. Concentrated growth factors embedded within fibrin matrices significantly enhance localized cellular proliferation and repair efficiency. This biological optimization improves surgical predictability across complex reconstructive and implant-based therapeutic interventions. Regulatory emphasis on biocompatibility further reinforces the adoption of autologous materials within clinical practice standards. Consequently, healthcare providers increasingly integrate fibrin-based solutions into standardized procedural workflows across specialties.

The Intra-Lock L PRF Intraspin System demonstrates strong alignment with these evolving procedural and safety requirements globally. Standardized centrifugation protocols ensure reproducible fibrin architecture and growth factor distribution across clinical applications. Consistency in preparation directly supports procedural reliability and improves graft integration outcomes within surgical environments. Outpatient care settings increasingly adopt such systems due to simplified workflows and reduced infrastructure requirements. Cost efficiency improves as chairside preparation minimizes dependence on external biologic processing facilities. This convergence of clinical reliability, regulatory alignment, and operational efficiency accelerates sustained adoption of fibrin-based regenerative therapies.

Procedural Volume Expansion Driving Autologous Matrix Integration

Rising volumes of implant and periodontal surgeries are structurally increasing demand for autologous healing matrices. Clinical workflows integrate these materials to accelerate tissue integration and reduce postoperative complication incidence. This procedural expansion strengthens reliance on biologics that deliver predictable regenerative performance across elective interventions. Cost structures favor in-clinic preparation as providers reduce dependence on outsourced grafting materials. Regulatory emphasis on patient safety further accelerates substitution toward autologous matrices with minimal contamination risk. Technological advancements in centrifugation and preparation systems enhance consistency, reinforcing clinician confidence in routine applications. Consequently, procurement strategies increasingly prioritize regenerative biomaterials aligned with high-throughput surgical environments.

Intraoral Health PRF Matrix Kit demonstrates integration within standardized implant protocols through consistent clot formation and handling reliability. Regeneris with the Advanced PRF System supports scalability requirements for clinics managing high procedural volumes. These systems enable rapid preparation cycles, aligning with the operational demands of outpatient and chairside surgical settings. Consistency in matrix quality directly improves graft stability and accelerates healing timelines across procedures. Cost efficiency improves through reduced reliance on external biomaterial sourcing and streamlined clinical workflows. This alignment between procedural demand, operational efficiency, and regenerative performance sustains adoption momentum across restorative dentistry practices.

Restraint Analysis - Preparation Standardization Gaps Limiting Clinical Consistency

Variability in centrifugation protocols introduces inconsistencies in fibrin matrix quality across decentralized preparation environments. Clinicians encounter difficulty achieving uniform platelet concentration and fibrin architecture without calibrated equipment and controlled workflows. These inconsistencies elevate procedural variability and increase perceived risk across implant and periodontal interventions. Resource-constrained settings face greater challenges due to limited access to standardized preparation infrastructure and validation protocols. Regulatory expectations for reproducibility further expose gaps in process uniformity across clinical sites. This fragmentation weakens confidence in outcome predictability and restricts the broader scalability of autologous biomaterial utilization. Consequently, adoption remains uneven across regions with varying levels of technical capability and infrastructure maturity.

Intraoral Health PRF Matrix Kit faces scrutiny regarding protocol variability that impacts consistency across different clinical operators and environments. Regeneris, with the Advanced PRF System, encounters similar deployment challenges when scaling across multi-site clinical networks. Inconsistent preparation outcomes complicate clinical validation and reduce the comparability of regenerative performance metrics. Procurement decisions become conservative as providers prioritize systems with proven standardization and reproducibility benchmarks. Operational inefficiencies increase when additional training and calibration are required to maintain acceptable preparation quality. These constraints collectively slow purchasing momentum and limit penetration across emerging and distributed healthcare delivery networks.

Protocol Standardization Complexity Constraining Clinical Validation

Variations in centrifugation speeds generate inconsistent platelet concentration and fibrin architecture across clinical preparations. Absence of universally accepted guidelines complicates cross-study comparisons and limits aggregation of clinical evidence. Device manufacturers apply distinct isolation and activation parameters, creating fragmented procedural standards across systems. These inconsistencies reduce confidence in reproducibility and slow adoption among risk-averse medical specialists. Regulatory bodies require harmonized datasets to validate safety and efficacy across broader clinical indications. Lack of standardized protocols increases validation complexity and prolongs approval timelines for regenerative applications. Consequently, variability in preparation methods constrains scalability and delays integration into mainstream therapeutic pathways.

Silfradent with Medifuge Centrifuge introduces controlled rotation parameters to improve fibrin clot consistency across procedures. Precision engineering supports stabilization of biological outputs, enhancing reliability within defined operating conditions. However, practitioner-dependent techniques continue to introduce variability despite standardized equipment capabilities. Training requirements increase as clinicians must align procedural execution with device-specific operational protocols. Smaller clinics face greater barriers due to limited technical expertise and constrained training resources. This operational complexity elevates entry thresholds and reduces adoption rates among new users. As a result, standardization challenges persist despite technological advancements in centrifugation systems.

Opportunity Analysis – Injectable Formulation Advances Enabling Minimally Invasive Regeneration

Rising demand for minimally invasive procedures is accelerating the development of injectable fibrin matrices for targeted delivery. Syringeable formulations enable precise placement within confined anatomical sites, improving access to deep periodontal defects. This capability reduces dependence on open surgical interventions and shortens procedural recovery timelines significantly. Policy frameworks increasingly favor outpatient care models, reinforcing the adoption of chairside regenerative solutions across practices. Technological progress in formulation stability enhances flow characteristics while preserving growth factor integrity during delivery. These innovations improve therapeutic precision and expand applicability across periodontal and endoscopic treatment pathways. Consequently, injectable platforms create a differentiated opportunity within regenerative workflows requiring controlled biologic placement.

Regeneris with I- PRF Injectable advances clinical usability through flowable matrices suited for endoscopic and minimally invasive applications. Intraoral Health Liquid PRF Kit supports targeted angiogenesis by enabling localized delivery within complex periodontal environments. These systems align with outpatient procedural models by simplifying preparation and reducing surgical infrastructure requirements. Improved handling characteristics enhance clinician control during application, supporting consistent therapeutic outcomes across varied cases. Cost efficiency benefits emerge through reduced operative time and minimized postoperative management requirements. This strategic focus expands access to underserved regenerative indications and strengthens competitive positioning within evolving treatment paradigms.

Chronic Wound Management Expanding Biologic Dressing Utilization

The rising prevalence of diabetic ulcers is intensifying demand for advanced biologic dressing solutions in clinical care. Fibrin membranes enable sustained cytokine release, supporting tissue regeneration in chronic non-healing wound environments. Hospital settings increasingly integrate these biologics within inpatient protocols for managing complex and refractory cases. Improved healing efficiency reduces recurrence rates and lowers cumulative costs associated with prolonged wound management. Aging populations with higher comorbidity burdens further expand the addressable patient base for regenerative therapies. Regulatory focus on outcome-based care models reinforces the adoption of treatments demonstrating measurable healing improvements. Consequently, chronic wound management emerges as a critical expansion pathway for fibrin-based therapeutic applications.

Geistlich Pharma with BioGide demonstrates potential synergy through integration with autologous fibrin matrices in wound care settings. Combining collagen scaffolds with patient-derived growth factors enhances structural support and accelerates tissue repair processes. Healthcare systems prioritize such approaches to reduce hospitalization duration and optimize resource utilization across care pathways. Clinical investigations focusing on limb salvage strengthen evidence supporting regenerative biomaterial effectiveness in severe cases. However, integration complexity requires alignment between surgical protocols and biologic preparation workflows within institutions. This targeted focus on chronic conditions establishes a stable and scalable demand base for market participants.

Category–wise Analysis

Modality Insights

Membrane form is expected to lead, accounting for approximately 51% share in 2026, anchored by its structural role in surgical scaffolding and guided tissue regeneration. Solid fibrin matrices provide mechanical stability, enabling clot retention and controlled healing within defect environments. Clinical workflows depend on predictable handling characteristics that support suturing and layered placement across complex procedures. Technological refinements in centrifugation and thickness control enhance matrix density and biological performance outcomes. Cost efficiency emerges through chairside preparation, reducing reliance on external grafting materials and processing infrastructure. This convergence of structural stability, workflow integration, and biological efficacy sustains dominance across surgical regeneration settings.

The injectable form is anticipated to be the fastest-growing segment, driven by demand for minimally invasive delivery across periodontal and aesthetic applications. Flowable fibrin formulations enable precise administration into irregular anatomical sites, improving localized growth factor distribution efficiency. Integration with endoscopic and fine needle techniques expands accessibility within confined treatment environments. Reduced procedural trauma lowers recovery time and improves patient throughput in outpatient clinical settings. Advances in centrifugation protocols extend working time, enhancing usability during complex multi-site interventions. These technological and procedural advantages accelerate adoption across diversified minimally invasive treatment pathways.

Application Insights

Implant dentistry is projected to lead, accounting for approximately 39% share in 2026, anchored by rising demand for durable restorative solutions. Fibrin-enhanced protocols improve osseointegration kinetics, supporting faster stabilization and functional recovery across implant procedures. Clinicians integrate these biologics within extraction sockets and sinus elevations to optimize bone regeneration outcomes. Dentsply Sirona Symbios regenerative solutions reinforce adoption through reliable integration within standardized implant workflows. Reduced treatment timelines improve patient throughput and lower cumulative procedural costs within clinical practice settings. Consistent performance in compromised bone conditions strengthens practitioner confidence in fibrin-supported regenerative approaches. This convergence of efficiency, predictability, and clinical necessity sustains dominance within implant-focused applications.

Periodontology is anticipated to be the fastest-growing segment, driven by the increasing prevalence of advanced gum disease requiring regenerative intervention. Biological matrices enable targeted repair of deep periodontal pockets and gingival recession defects across specialized treatments. Salvin Dental Specialties Salvin Regenerative kits support complex procedures through integrated preparation and delivery systems. Patient preference for autologous healing approaches accelerates substitution away from synthetic grafting materials in periodontal care. Minimally invasive surgical techniques improve recovery profiles while maintaining regenerative effectiveness across treatment cycles. Advances in fibrin handling and application enhance precision within delicate periodontal structures. These clinical and technological dynamics sustain rapid expansion across specialized periodontal therapy pathways.

Regional Insights

North America Platelet Rich Fibrin Market Trends

North America is expected to remain the leading regional market, accounting for approximately 43% share in 2026, supported by high dental implant penetration and a robust regulatory environment for biologics. Dense networks of equipped clinics drive consistent procurement. Reimbursement structures reinforce technology uptake. The region's dominance is anchored in a mature healthcare infrastructure that facilitates the early adoption of advanced regenerative materials. Large-scale dental service organizations are expected to remain key drivers of procurement as they standardize biological protocols across multiple locations. Favorable reimbursement policies for certain surgical components are anticipated to sustain demand for high-quality fibrin processing systems.

The US is expected to anchor regional momentum through significant investments in research and development for autologous blood concentrates. Stringent FDA oversight ensures high safety standards, which reinforces clinician confidence in using advanced centrifugation devices. Bio-Horizons with L-PRF Cotton Matrix is expected to benefit from a well-established distribution network across American dental schools and private practices. Zimmer Biomet, with Platelet Rich Fibrin Kit, benefits from localization strategies enhancing supply chain resilience. Growing consumer awareness regarding natural healing benefits is projected to increase the adoption of fibrin-based treatments in outpatient settings.

Asia Pacific Platelet Rich Fibrin Market Trends

Asia Pacific is expected to register the fastest growth trajectory, as expanding medical infrastructure and rising disposable incomes accelerate market expansion across emerging economies. The region's growth is anchored in the rapid development of specialized dental tourism hubs that prioritize cost-effective but high-quality regenerative treatments. Increasing awareness of oral hygiene and aesthetic dental procedures is expected to broaden the potential patient base for fibrin therapies. Local manufacturers are anticipated to introduce competitive processing kits, making the technology more accessible to mid-tier clinics.

India anchors this acceleration through government-backed dental infrastructure initiatives and private clinic scaling. Regulatory approvals for import kits spur investments in periodontology. Procedure volume surges sustain momentum. China is expected to remain a primary growth engine for the region due to its massive population and increasing government focus on advanced medical technologies. Rapid urbanization and the proliferation of private dental chains are anticipated to drive high volumes of equipment procurement. Dentsply Sirona, with Symbios regenerative solutions, is expected to leverage its global brand equity to capture expanding market share in major Chinese cities. Strategic partnerships between international vendors and local distributors are projected to enhance the availability of specialized fibrin modalities.

Europe Platelet Rich Fibrin Market Trends

Europe is expected to remain a mature and structurally stable regional market, with demand primarily anchored in high standards of clinical education and established surgical traditions. European practitioners have been at the forefront of developing the low-speed centrifugation concept that defines modern PRF preparation. The region's market is expected to remain characterized by a strong preference for evidence-based biological solutions in periodontology and maxillofacial surgery. Public health systems are anticipated to gradually integrate these autologous therapies into specialized hospital departments to improve wound healing outcomes. Established standards mandate biomaterial integration for maxillofacial repairs.

Germany is expected to drive European market stability through its leadership in medical device engineering and clinical research. The country's dense network of specialized dental clinics is anticipated to accelerate the replacement of older centrifugation units with modern, programmable systems. Silfradent with Medifuge Centrifuge is set to maintain a strong presence due to its alignment with German precision standards and quality certifications. Straumann, with Emdogain PRF, aligns with local manufacturing to meet precision demands. Compliance tightening forecasts steady utilization growth. Regulatory updates under the Medical Device Regulation (MDR) are projected to consolidate the market toward established vendors with robust clinical data.

Competitive Landscape

The global platelet rich fibrin market is fragmented, with leadership concentrated among specialized biotechnology firms and diversified medical device manufacturers. This structure reflects varied clinical applications requiring tailored preparation protocols and device-specific validation pathways. Leading players shape procedural standards through clinical validation, influencing practitioner trust and procurement decision frameworks. Procurement behavior remains closely linked to device performance, training ecosystems, and reproducibility under complex surgical conditions. This combination reinforces structured vendor preference patterns across high-precision regenerative treatment settings.

Competitive positioning emphasizes differentiation through integrated systems combining centrifuges, biologic kits, and procedural tools. Premium vendors focus on ecosystem cohesion, while value providers target accessibility across emerging practice environments. Industry dynamics reflect increasing consolidation through acquisitions of niche technology providers with specialized preparation capabilities. Platform evolution incorporates automation and software guidance, improving consistency across multi-operator clinical settings. Competitive intensity shifts toward integrated solutions supporting broader applications, including orthopedics and chronic wound care. These dynamics reinforce a transition toward standardized, technology-enabled regenerative workflows across global healthcare systems.

Key Industry Developments:

- In March 2026, Scientific reports confirm that Alb-PRF (Albumin-PRF) outperforms traditional PRP and H-PRF in endothelial function. This finding validates "next-generation" PRF variants, pushing manufacturers to develop systems capable of producing these specific high-performance concentrates for better wound healing. The superior performance of Alb-PRF validates a shift toward "next-generation" biological concentrates, forcing the market to evolve from simple blood separation to precision bio-engineering systems that offer longer-lasting and more potent healing.

- In February 2026, Zimmer Biomet unveils new regenerative data and highlights at the AAOS Annual Meeting. By integrating regenerative biologics data into major orthopedic forums, Zimmer Biomet strengthens its position against pure-play biotech firms in the surgical recovery space. Zimmer Biomet's integration of clinical data with regenerative biologics validates platelet-rich fibrin (PRF) as a standardized, data-backed pillar within the expanding global platelet-rich plasma market.

Companies Covered in Platelet Rich Fibrin Market

- Zimmer Biomet

- Straumann Group

- Dentsply Sirona

- BioHorizons

- Baxter International

- Geistlich Pharma

- Intra-Lock

- Regeneris

- Intraoral Health

- Silfradent

- Mectron

- Salvin Dental Specialties

- BTI Biotechnology Institute

- RegenLab

Frequently Asked Questions

The global platelet rich fibrin market is projected to reach US$519.8 million in 2026. It is expected to expand to US$1,099.8 million by 2033. This growth reflects rising regenerative demand.

Regenerative procedure expansion in implant dentistry drives primary growth. Dental clinics adopt chairside systems for workflow efficiency. Periodontal applications further accelerate uptake.

The forecast CAGR stands at 11.3% from 2026 to 2033. This rate builds on historical 10.8% momentum. Structural demand sustains this trajectory.

North America leads with approximately 43% share in 2026. Advanced infrastructure supports this position. Reimbursement aids consistent procurement.

Key players include Zimmer Biomet, Straumann Group, Dentsply Sirona, BioHorizons, Baxter International, Geistlich Pharma, Intra-Lock, and Regeneris. Baxter and Intra-Lock focus on advanced formulations.