- Healthcare

- Genomic Cancer Testing Market

Genomic Cancer Testing Market Size, Share, and Growth Forecast, 2026 - 2033

Genomic Cancer Testing Market by Test Type (Genomic Profiling Tests, Genetic Testing, Liquid Biopsy Tests, Companion Diagnostic Tests, Pharmacogenomic Tests, Hereditary Cancer Tests, Other Tests), Technology (Next Generation Sequencing (NGS), Polymerase Chain Reaction (PCR), Microarray, Fluorescence In Situ Hybridization (FISH), Immunohistochemistry (IHC), Others), Application (Oncology Diagnostics, Prognostic Testing, Predictive Testing, Targeted Therapy Selection, Disease Monitoring, Risk Assessment, Drug Discovery & Development), and Regional Analysis for 2026 - 2033

Genomic Cancer Testing Market Share and Trends Analysis

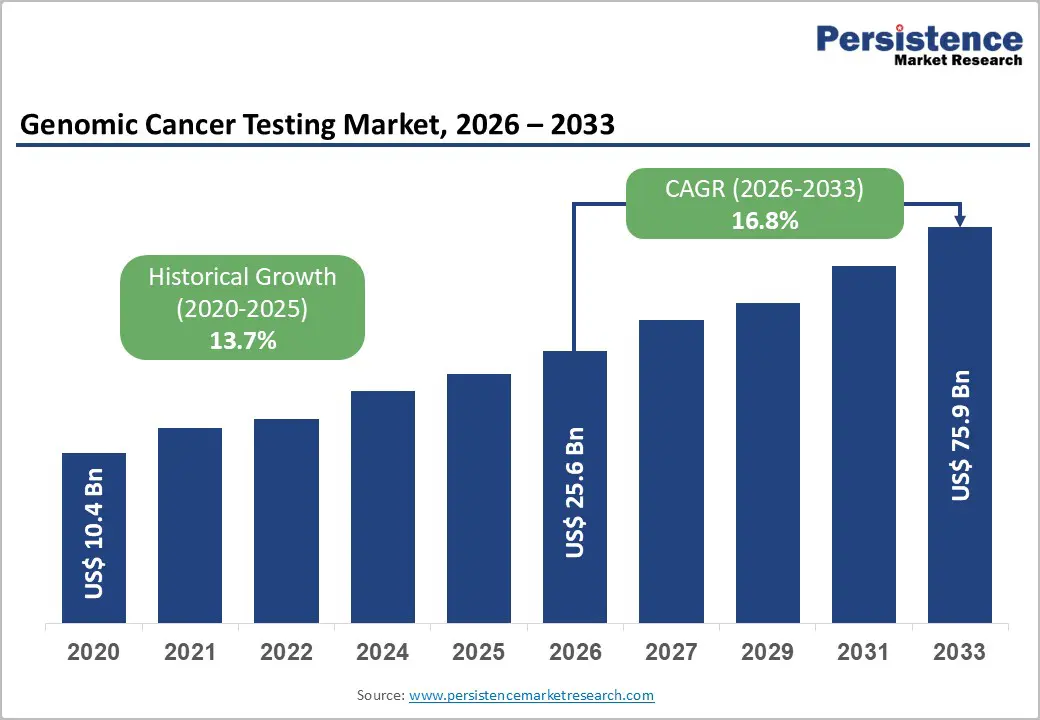

The global genomic cancer testing market size is likely to be valued at US$ 25.6 billion in 2026, and is projected to reach US$ 75.9 billion by 2033, growing at a CAGR of 16.8% during the forecast period 2026−2033. Market expansion is driven by aging populations and the increasing prevalence of cancer, which intensifies demand for precise diagnostic solutions. Rising clinical awareness and adoption of personalized treatment protocols enhance the utility of genomic testing, enabling early detection and improved therapeutic outcomes.

Integration of advanced technologies such as next-generation sequencing and liquid biopsy supports high-throughput, accurate analysis, facilitating broader application across oncology care pathways. Healthcare infrastructure development, including laboratory networks and diagnostic centers, increases accessibility to genomic services, promoting market penetration in urban and emerging regions. Policy initiatives encouraging precision medicine and reimbursement frameworks strengthen affordability and adoption rates.

Key Industry Highlights

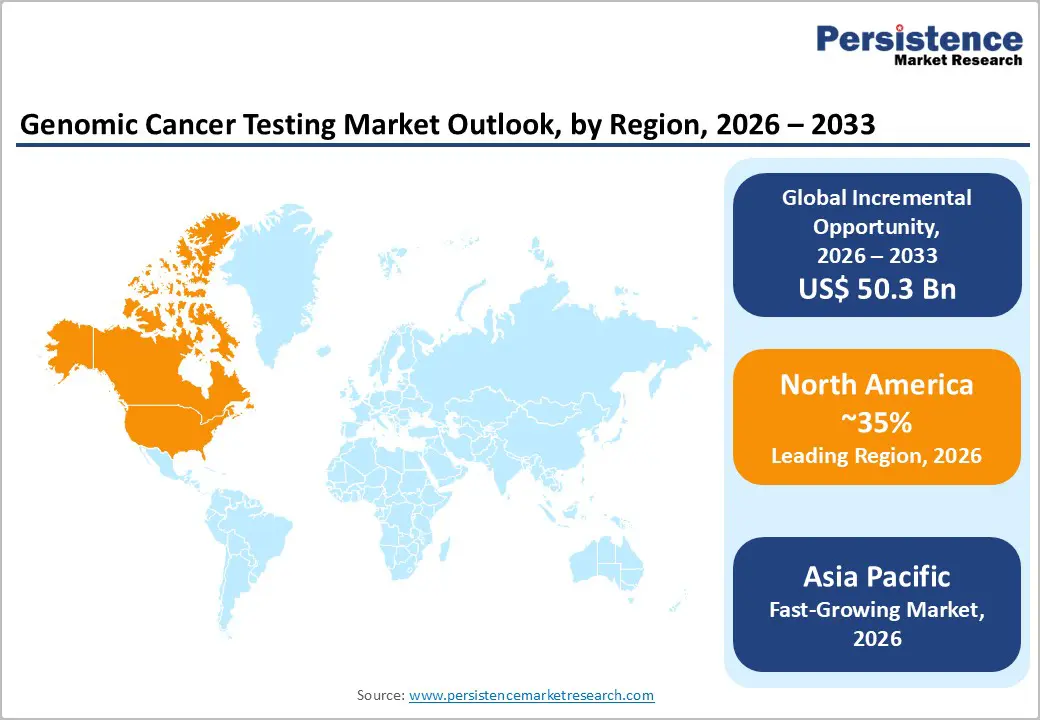

- Dominant Region: North America is expected to dominate with around 35% market share in 2026, driven by infrastructure and precision oncology adoption.

- Fastest-growing Regional Market: Asia Pacific is forecasted as the fastest-growing market between 2026 and 2033, on account of expanding diagnostics and precision oncology adoption.

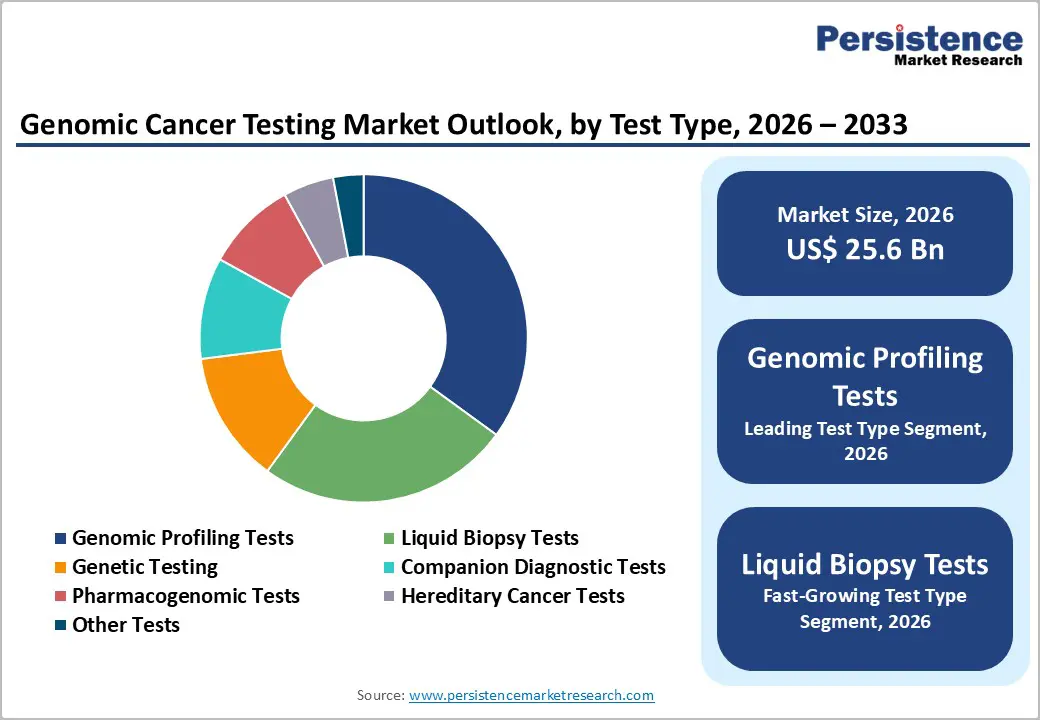

- Leading Test Type: Genomic profiling tests are expected to lead with over 35% revenue share in 2026, supported by comprehensive tumor analysis and targeted therapy selection.

- Fastest-growing Test Type: Liquid biopsy tests are projected to grow fastest between 2026 and 2033, fueled by minimally invasive monitoring.

| Key Insights | Details |

|---|---|

|

Genomic Cancer Testing Market Size (2026E) |

US$ 25.6 Bn |

|

Market Value Forecast (2033F) |

US$ 75.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

16.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

13.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Cancer and Aging Demographics

The increasing burden of cancer reflects both rising incidence rates and extended patient survival, driving demand for precise diagnostic tools. U.S. government estimates project 2,041,910 new cancer cases in 2025, underscoring a persistent disease prevalence. Rising case numbers create pressure on healthcare systems to stratify patients based on tumor characteristics and molecular profiles. Advanced genomic diagnostics allow clinicians to identify actionable mutations, guide personalized treatment plans, and optimize outcomes. Growing patient populations in higher-risk age brackets further elevate the need for efficient, targeted diagnostics that support early detection and clinical decision-making.

Age remains a dominant risk factor for cancer development, with incidence rising sharply among older adults. Median age at diagnosis in the United States is approximately 67 years, and cancer occurrence increases substantially in the aging population. As populations in developed economies age, the proportion of individuals at elevated risk increases. Older adults accumulate genetic mutations over time, underscoring the need for personalized diagnostic approaches to detect disease early. Genomic testing enables the identification of specific alterations, supports tailored therapy selection, and streamlines clinical pathways for efficient patient management.

Increased Healthcare Investment and Funding

Sustained government financing for biomedical research expands infrastructure and technological capability at public institutions and research agencies that underpin clinical innovation. In fiscal year 2025, the United States National Human Genome Research Institute (NHGRI) was allocated US$ 663.7 million to support genomics research, including technology development, biological discovery, and the translation of genomic science into clinical applications. Such appropriation enables long-term investments in advanced sequencing platforms, bioinformatics tools, high-performance computing, and specialized laboratories. Funding also supports the training of specialized scientific talent and provides seed capital that reduces risk for later-stage investment by commercial partners, accelerating innovation and adoption.

Public funding commitments signal priority to industry participants, driving capital flows into diagnostics developers, academic translational centers, and contract research organizations. Agencies establish structured funding mechanisms that lower barriers to entry for exploratory research, foster multidisciplinary collaboration, and support large-cohort clinical studies generating evidence for regulatory acceptance and clinical guideline integration. Stable federal investment reduces uncertainty for private funders, accelerates technology maturation, and shortens the time from discovery to clinical utility. Periods of stagnant or reduced funding illustrate the dependency of innovation cycles on consistent public investment and strategic allocation.

Lack of Standardized Testing Guidelines

In the genomic cancer testing market, differences in testing protocols and reporting standards significantly affect clinical adoption. Laboratories use diverse sequencing platforms, bioinformatics pipelines, and sample preparation techniques, producing variable results across institutions. Clinicians face challenges in interpreting results because there are no universally accepted benchmarks for test sensitivity, specificity, and clinical validity. Variations in assay design and result annotation limit comparability and reduce confidence in genomic insights for guiding therapeutic decisions. Regulatory authorities in different regions enforce distinct validation requirements, creating uncertainty for test developers and providers seeking cross-border applicability. Such fragmentation slows integration of testing into oncology workflows.

Inconsistent guidelines also impact training and competency development among laboratory personnel and bioinformaticians. Without uniform standards, establishing proficiency in variant calling, data interpretation, and quality control becomes difficult, increasing the risk of diagnostic errors. Pharmaceutical and diagnostic companies encounter challenges demonstrating clinical utility and regulatory compliance when launching new genomic assays. Clinical trials that rely on genomic stratification experience delays due to methodological inconsistencies, hindering evidence generation for adoption. Divergence in testing practices limits large-scale precision oncology initiatives, hindering the ability to standardize patient care pathways and reduce treatment outcome variability.

Complex Data Interpretation

Interpreting genomic data in cancer testing involves processing massive volumes of information generated from next-generation sequencing (NGS), whole-exome sequencing, and transcriptomic profiling. Each sample produces millions of genetic variants, including single-nucleotide polymorphisms, insertions, deletions, and structural changes. Translating these variants into clinically relevant insights requires advanced bioinformatics tools, specialized knowledge, and constant updates from scientific research. Tumor heterogeneity and sequencing errors increase complexity, demanding integration of multi-omic data with patient history and treatment outcomes.

Data analysis requires significant computational resources and standardized frameworks, which remain limited in many healthcare environments. The scarcity of trained bioinformaticians and molecular pathologists limits adoption and prolongs turnaround times for diagnostic results. Variations in reporting standards across institutions introduce inconsistencies in clinical decision-making, reducing physician confidence and complicating patient management. Artificial intelligence and machine learning offer potential for streamlining interpretation, but require extensive validation and regulatory oversight.

Expansion of Liquid Biopsy and Non-Invasive Diagnostics

Liquid biopsy and other non-invasive diagnostic techniques enable earlier and more frequent assessment of tumor-derived genomic signals. Traditional tissue biopsies require surgical sampling. These procedures are invasive and often limited by tumor location. They cannot be repeated frequently for monitoring. Liquid biopsies detect circulating tumor DNA and other biomarkers in blood or bodily fluids. This approach provides a minimally invasive means of understanding tumor biology. It supports early detection, treatment selection, and monitoring of therapy response or recurrence. Federal research identifies these tests as important for improving cancer detection and patient care.

Circulating tumor DNA can appear years before conventional diagnosis, offering earlier intervention opportunities. Studies show that genetic material released by tumors into the bloodstream can be detected up to 3 years before standard clinical identification. This allows continuous disease monitoring and supports personalized therapy adjustments. It also reduces dependence on invasive procedures. Investment in non-invasive genomic diagnostics aligns with public health goals. It improves patient outcomes through timely intervention and risk stratification.

Development of Companion Diagnostics

Linking targeted therapies with diagnostic tests improves clinical precision. Clinicians can identify patients most likely to respond to specific treatments. Companion diagnostics inform safe and effective use of corresponding drugs. The U.S. Food and Drug Administration (FDA) defines these tests as medical devices that guide therapy decisions. Integration of these diagnostics speeds regulatory review through coordinated evidence. They enhance alignment with clinical guidelines. Embedding molecular insights in decision-making reduces uncertainty for clinicians. Adoption among oncologists increases. Payer confidence strengthens.

Co-developed tests stratify patients by actionable genomic markers. This supports more efficient clinical trial designs. Enriched study populations improve trial success rates. Development timelines for pharmaceutical partners shorten. Payers view these diagnostics as tools to optimize outcomes. Exposure to ineffective treatments decreases. Reimbursement value propositions strengthen. Partnerships between diagnostic developers and drug manufacturers expand the commercial reach of diagnostics. Diagnostic insights are embedded into care standards.

Category-wise Analysis

Test Type Insights

Genomic profiling tests are likely to be the leading segment with over 35% revenue share in 2026, due to their ability to provide comprehensive molecular characterization of tumors. These tests facilitate targeted therapy selection and enable personalized treatment planning. Hospitals and specialty oncology centers prefer these tests for complex cases where multiple biomarkers inform therapeutic decisions. High clinical acceptance, demonstrated utility in prognostic evaluation, and integration into electronic health records enhance adoption. Accessibility improvements through central laboratories and referral networks support broader implementation.

Liquid biopsy tests are expected to witness the fastest growth between 2026 and 2033, as they offer minimally invasive alternatives for tumor detection and monitoring. Clinicians increasingly favor liquid biopsies for real-time assessment of treatment response and early relapse detection. Ease of sample collection and patient compliance drives adoption in outpatient settings. Technological advancements in circulating tumor DNA (ctDNA) detection and high-sensitivity sequencing expand the clinical utility of ctDNA testing. Integration with digital reporting platforms and AI-assisted interpretation enhances efficiency and scalability. Rising awareness among patients and providers regarding early detection supports rapid segment expansion.

Technology Insights

NGS is poised to lead, with a forecasted over 40% share of the genomic cancer testing market revenue in 2026, owing to its high-throughput capabilities and comprehensive genomic coverage. Healthcare providers rely on NGS for multi-gene panels, enabling simultaneous assessment of numerous cancer-related genes. Accuracy, reproducibility, and integration with bioinformatics platforms enhance clinical confidence. Hospitals and diagnostic networks adopt NGS for standardized workflows and actionable insights. Platform scalability supports centralized testing models, improving operational efficiency and turnaround times.

PCR is anticipated to be the fastest-growing segment between 2026 and 2033, driven by rapid turnaround times, affordability, and adaptability across various sample types. High sensitivity and specificity enable the detection of low-abundance mutations and the monitoring of minimal residual disease. Adoption increases in community hospitals, diagnostic laboratories, and point-of-care settings. Integration with digital reporting tools and automation streamlines interpretation and reduces operational burden. Cultural acceptance of molecular diagnostics and rising preventive healthcare initiatives further stimulate growth.

Regional Insights

North America Genomic Cancer Testing Market Trends

North America is expected to dominate with an estimated 35% share of the genomic cancer testing market value in 2026, reflecting the concentration of clinical, research, and reimbursement frameworks supporting advanced diagnostics such as next-generation sequencing and molecular profiling. Strong healthcare infrastructure in the United States enables high-throughput genomic laboratories and routine use of precision diagnostics in major cancer centers. Federal programs such as the National Institutes of Health (NIH)’s All of Us Research Program generate large genomic datasets and encourage integration of genomics into clinical decision-making. Canada’s national health initiatives expand diagnostic applications from basic screening to molecular stratification, increasing test volumes and supporting the adoption of precision oncology practices.

Key factors driving dominance include established reimbursement policies that encourage providers and payers to adopt complex assays and that reduce financial barriers to genomic profiling. Extensive clinical research networks in the United States and Canada support rapid validation of novel biomarkers and tests. The presence of major biotech and diagnostic technology firms fosters innovation in bioinformatics, automated workflows, and laboratory services. Rising cancer incidence reinforces demand for precision tools to guide targeted therapies. Integration into treatment planning improves outcomes and positions the region at the forefront of genomic oncology diagnostics.

Europe Genomic Cancer Testing Market Trends

Europe is expected to maintain a significant position in the genomic cancer testing market, driven by robust healthcare systems and strong regulatory frameworks. Germany is expanding access to molecular diagnostics through national precision medicine initiatives. France emphasizes integrating genomic profiling into standard oncology protocols to support early detection and treatment personalization. The United Kingdom is advancing digital pathology and bioinformatics platforms to enhance genomic interpretation. Italy is investing in public health programs that promote cancer screening and molecular testing. Established clinical networks and research institutions facilitate rapid adoption of next-generation sequencing and companion diagnostics, supporting demand from hospitals and specialized cancer centers.

Key growth drivers include well-defined reimbursement policies that reduce financial barriers for advanced diagnostics. Collaboration between biotech firms, academic institutions, and healthcare providers accelerates the development and clinical validation of novel assays. Rising prevalence of cancers such as colorectal, breast, and lung increases demand for precision testing. Expansion of high-throughput laboratory capacity and integration of artificial intelligence for data analysis improve turnaround times and diagnostic accuracy. Increasing focus on real-world evidence and value-based healthcare encourages adoption of tests that optimize therapy selection and improve patient outcomes. Technological innovation, combined with supportive policy frameworks, strengthens market positioning and enables sustained growth in clinical and research applications.

Asia Pacific Genomic Cancer Testing Market Trends

Asia Pacific is forecasted to be the fastest-growing market for genomic cancer testing between 2026 and 2033, stimulated by rising investment in healthcare infrastructure and adoption of advanced diagnostics. China has implemented large-scale genomic initiatives that support precision medicine integration in oncology. India is expanding sequencing laboratories and increasing access to molecular diagnostics in urban and semi-urban hospitals. Japan is modernizing cancer care pathways to include biomarker-driven therapy selection. South Korea is investing in national precision oncology programs and digital health platforms. Growing demand for personalized treatment solutions and early detection tools is driving test adoption across clinical and research settings.

Key factors supporting rapid growth include government policies promoting genomics research and public health programs that expand access to molecular testing. Collaboration between local healthcare providers and international biotech firms enhances technical capabilities and introduces novel sequencing platforms. Increasing cancer incidence in populations reinforces need for accurate and actionable diagnostic data. Adoption of liquid biopsy and next-generation sequencing technologies improves the efficiency of testing. Expansion of insurance coverage for molecular assays strengthens affordability.

Competitive Landscape

The global genomic cancer testing market demonstrates a moderately consolidated structure, with leading players capturing approximately 60% of revenue in 2026. Key participants include Thermo Fisher Scientific, Illumina, Qiagen, F. Hoffmann-La Roche, Bio-Rad Laboratories, and Myriad Genetics. These companies leverage extensive product portfolios, advanced sequencing technologies, and validated diagnostic platforms. Collaborations with hospitals and research institutions strengthen adoption. Economies of scale in production and distribution enhance efficiency and market influence.

Innovation and technological differentiation remain central to maintaining market share. Illumina and Thermo Fisher Scientific focus on next-generation sequencing platforms. Qiagen and Bio-Rad Laboratories emphasize molecular assay development. F. Hoffmann-La Roche integrates companion diagnostics with therapies. Myriad Genetics specializes in predictive testing. Strategic partnerships, licensing, and continuous enhancement of test capabilities ensure leadership. Investment in bioinformatics and AI-driven analysis supports rapid interpretation of complex genomic data.

Key Industry Developments

- In March 2026, Lucence, DxD Hub, and the National Cancer Centre Singapore launched a $6 million UNITED 2.0 collaboration to develop an advanced AI-driven genomic cancer profiling test for improved precision diagnostics and treatment selection.

- In November 2025, the Tamil Nadu government announced plans to establish a state-of-the-art genomic testing laboratory aimed at improving cancer treatment and offering targeted therapy services in government hospitals.

- In October 2025, Nucleome Informatics launched the DrSeq 4 Power Biomarkers WGS-HiFi genomics test, an advanced long-read sequencing solution designed to improve detection of complex cancer mutations and support precision oncology.

Companies Covered in Genomic Cancer Testing Market

- Thermo Fisher Scientific

- Illumina Inc.

- Qiagen

- F. Hoffmann-La Roche Ltd

- Bio-Rad Laboratories Inc.

- Myriad Genetics Inc.

- Pacific Biosciences of California Inc.

- Veracyte

- Natera Inc.

- Agilent Technologies Inc.

- Astronics Company

- Personal Genome Diagnostics Inc.

Frequently Asked Questions

The global genomic cancer testing market is projected to reach US$ 25.6 billion in 2026.

Rising cancer incidence, growing adoption of precision medicine, and advancements in next-generation sequencing technologies are driving the market.

The market is poised to witness a CAGR of 16.8% from 2026 to 2033.

Expansion of companion diagnostics, increasing adoption of liquid biopsy, and integration of AI-driven genomic analysis present key market opportunities.

Some of the key market players include Thermo Fisher Scientific, Illumina, Qiagen, F. Hoffmann-La Roche, Bio-Rad Laboratories, and Myriad Genetics.