- Advanced Materials

- Renewable Materials in Construction Market

Renewable Materials in Construction Market Size, Share, and Growth Forecast, 2026 - 2033

Renewable Materials in Construction Market by Product Type (Crop-Based Materials, Non-Crop Based Materials), Application (Exteriors, Interiors, Building Systems, Solar Powers, Structurals, Permeable Pavement), and Regional Analysis for 2026 - 2033

Renewable Materials in Construction Market Size and Trends Analysis

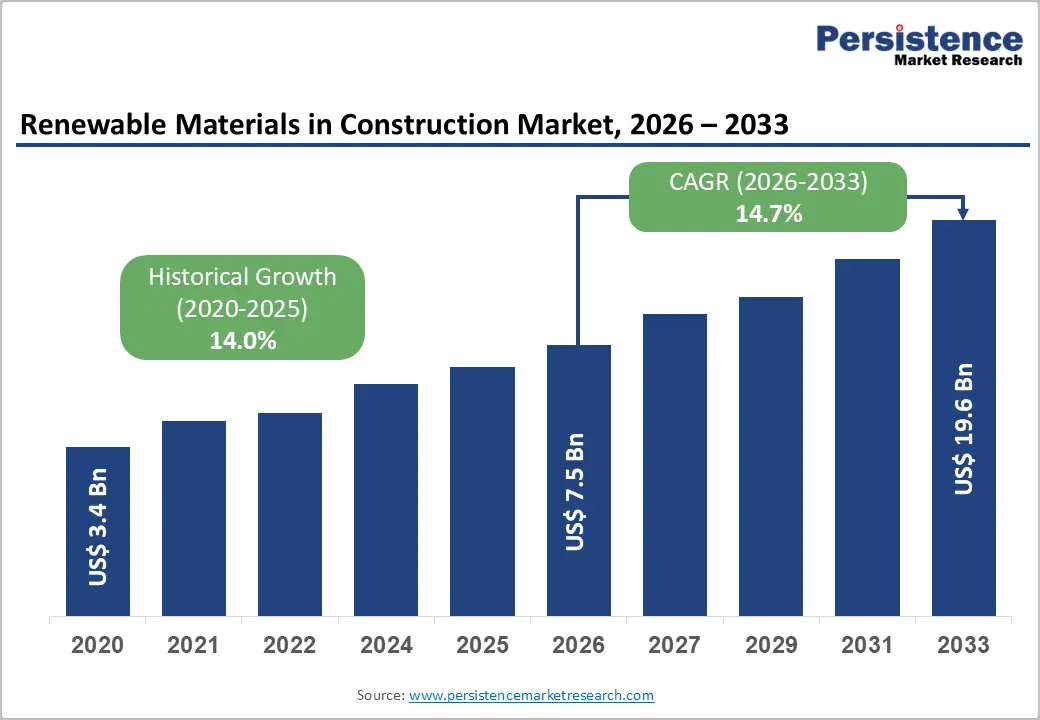

The global renewable materials in construction market size is likely to be valued at US$7.5 billion in 2026, and is expected to reach US$19.6 billion by 2033, growing at a CAGR of 14.7% during the forecast period from 2026 to 2033, driven by the increasing adoption of renewable materials, including bio-based, recycled, and sustainably sourced products such as timber, bamboo, hemp, straw, cork, and mycelium-based composites, which are widely used across structural, interior, exterior, and energy applications. These materials provide reduced carbon footprints, enhanced energy efficiency, and strong alignment with green building standards, positioning them as a critical component of sustainable construction practices.

Key Industry Highlights:

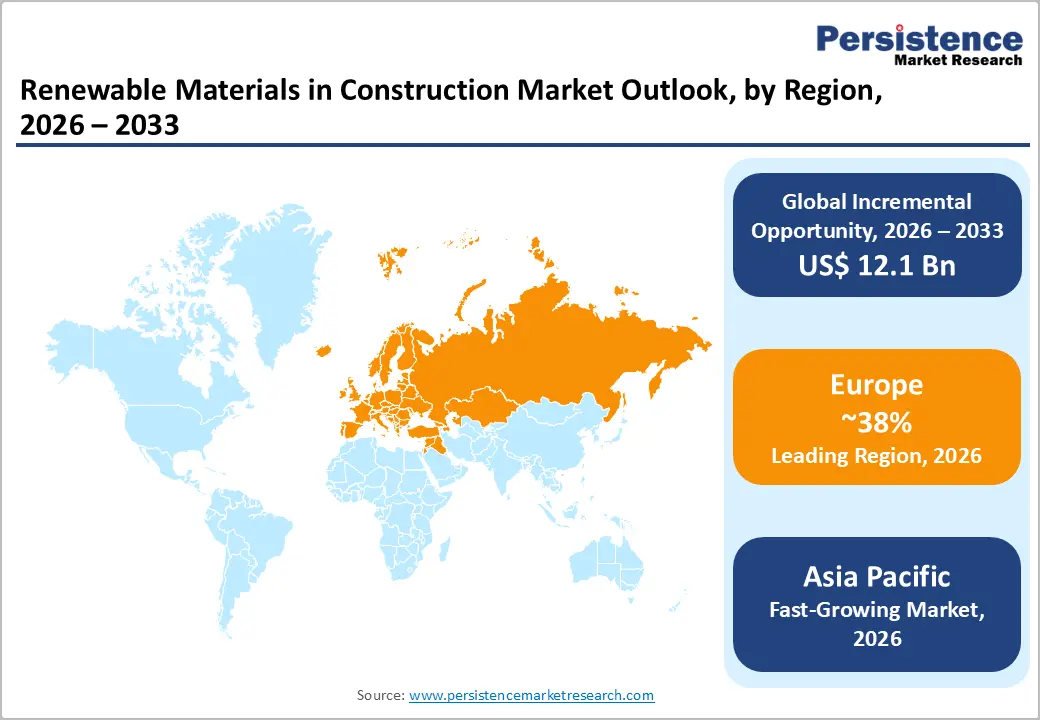

- Dominant Region: Europe is projected to dominate with 38% revenue share in 2026, supported by strict green building regulations and circular economy policies.

- Fastest-growing Region: Asia Pacific is expected to be the fastest-growing region, driven by rapid urbanization and government sustainability initiatives in China and India.

- Dominant Product Type: Crop-based materials are expected to dominate with 62% share in 2026, due to their wide availability and cost-effectiveness.

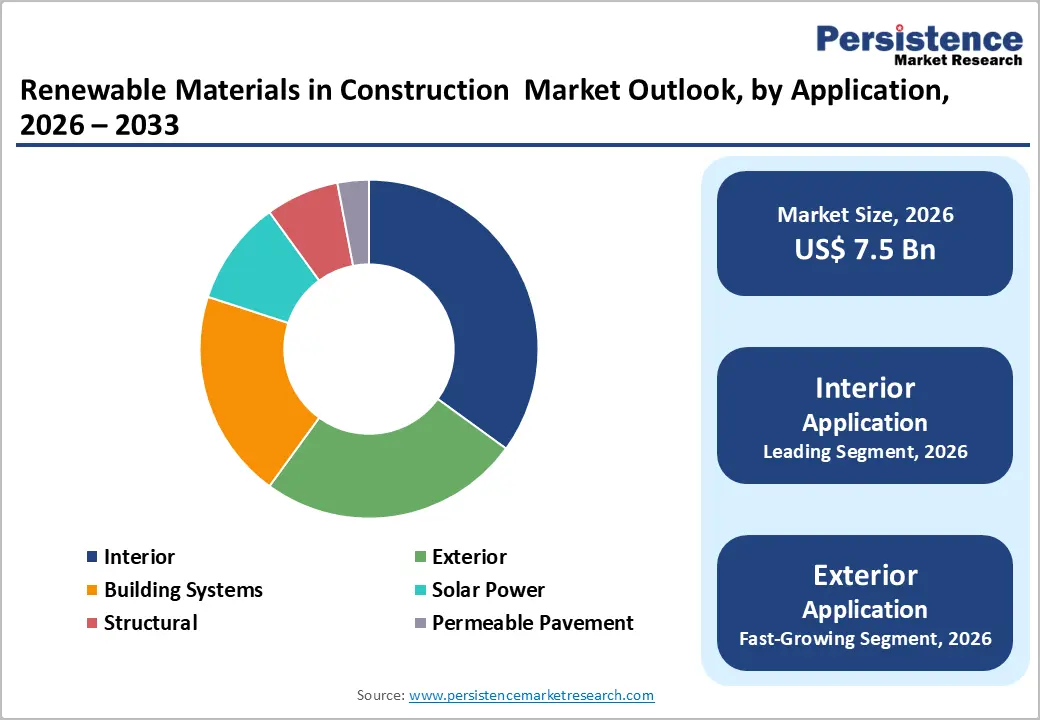

- Leading Application: Interiors are projected to lead with the 35% share, owing to high use of renewable finishes and insulation.

DRO Analysis

Driver - Global Push for Sustainable and Green Building Practices

The global push for sustainable and green building practices has intensified amid escalating climate challenges and urbanization pressures. Driven by stringent regulations, corporate ESG mandates, and rising energy costs, governments worldwide are enforcing energy-efficient building codes, net-zero standards, and circular economy principles that prioritize material reuse and waste minimization.

Europe leads with ambitious policies such as the Circular Economy Action Plan, mandating recycled materials in new projects and passive house designs for superior insulation and airtightness. Asia Pacific, particularly China and India, shows rapid adoption fueled by urbanization, air quality concerns, and infrastructure mandates requiring green certifications. Emerging markets leverage low-carbon materials such as sustainable timber and recycled steel to curb emissions from construction, which accounts for nearly 40% of global energy-related CO2.

Restraint - Higher Initial Cost Compared to Conventional Materials

Sustainable materials, such as low-carbon concrete, mass timber, recycled steel, and high-performance insulation, often command premium prices due to specialized manufacturing processes and limited supply chains. These eco-friendly alternatives require advanced production techniques, such as energy-intensive carbon capture in cement or sustainable sourcing for engineered wood, which elevate material expenses compared to readily available conventional options like standard Portland cement or virgin steel.

Additional upfront investments arise from enhanced design complexity, including superior building envelopes for airtightness and energy modeling software to optimize performance. Certification processes for standards such as LEED or passive house compliance demand rigorous testing, documentation, and third-party verification fees. Labor costs also rise as projects necessitate skilled workers trained in green installation methods, such as precise modular prefabrication or biophilic integrations.

Opportunity - Government Incentives and Net-Zero Building Targets

Nations worldwide are accelerating the transition to net-zero buildings through targeted incentives and ambitious policy frameworks. Tax credits, grants, and rebates offset upfront costs for energy-efficient systems like solar panels, heat pumps, and advanced insulation, making sustainable construction financially viable for developers and owners.

Europe's EU Green Deal mandates all new buildings achieve net-zero emissions by 2030, backed by the Renovation Wave initiative funding retrofits and low-carbon materials. The U.S. Inflation Reduction Act provides substantial deductions for zero-energy projects, while China's 14th Five-Year Plan enforces strict carbon quotas, prioritizing passive designs and district heating. In Asia Pacific region, India's state-level benefits include additional Floor Area Ratio (FAR) for certified green structures and subsidies on electricity tariffs. C40 Cities commit to halving embodied emissions in new builds by 2030, promoting zero-emission machinery from 2025.

Category-wise Analysis

Product Type Insights

Crop-based materials are anticipated to dominate with the 62% share in 2026, owing to their abundant global supply from annual harvests, ensuring scalability without deforestation pressures. Lower production costs stem from minimal processing, such as simple baling, shredding, or pressing versus energy-intensive mining for synthetics. IsoHemp is a leading European manufacturer of industrial hemp-based construction blocks (hempcrete), widely used in sustainable building projects.

Non-crop-based materials are likely to be the fastest-growing product type in the renewable materials in construction market. Non-crop materials such as mycelium, algae biocomposites, and recycled polymers surge ahead through rapid innovation, delivering superior fire resistance, carbon-negative sequestration, lightweight strength, and exceptional thermal/acoustic insulation over traditional options. Ecovative develops mycelium-based composites, grown from fungal root structures on organic waste, representing a next-generation alternative to conventional construction and insulation materials.

Application Insights

Interiors are projected to dominate, capturing 35% market share in 2026, fueled by surging demand for sustainable flooring such as cork and bamboo, mycelium wall panels, hemp insulation, and bio-based finishes in residential and commercial spaces. Corticeira Amorim is a global leader in cork-based materials used extensively for flooring, wall panels, and acoustic insulation in residential and commercial interiors.

Exteriors are expected to represent the fastest-growing application segment, supported by robust innovations in bio-based claddings such as mycelium boards, algae-infused roofing tiles, and hemp-fiber facades. These solutions deliver weather resistance, UV stability, and fire retardancy while meeting stringent green certifications, enabling scalable retrofits and new net-zero structures amid urbanization pressures. An example of exterior application is mycelium-based façade panels developed by Ecovative Design. The company has introduced mycelium-grown composite boards that can be used as exterior cladding solutions in buildings.

Regional Insights

North America Renewable Materials in Construction Market Trends

North America is projected to grow at a CAGR of approximately 14.2% through 2033. The region's market development is driven by the convergence of powerful policy incentives, including the U.S. Inflation Reduction Act's low-embodied-carbon material procurement provisions, the USDA BioPreferred Program, and Canada's National Zero-Carbon Building Standard, with a maturing mass timber construction ecosystem and growing developer ESG commitments that are translating into voluntary renewable material adoption across the private commercial and residential development sectors.

In North America's renewable materials in construction market, the U.S. holds the dominant share at approximately 70%, driven by its larger economy and policy support, Canada accounts for 10% share and represents a highly developed secondary market with a strong domestic mass timber manufacturing industry British Columbia-based producers, including Structurlam and Western Archrib, supply both Canadian and U.S. construction projects and national building code provisions for tall mass timber that have supported landmark CLT and mass timber projects including Brock Commons at UBC.

Europe Renewable Materials in Construction Market Trends

Europe is projected to dominate, growing at a CAGR of approximately 13.8% through 2033. The region's market leadership reflects the combination of the world's most advanced regulatory framework for sustainable construction encompassing the EU Green Deal, EU Taxonomy, EPBD recast, and France's RE2020 with the world's most mature mass timber manufacturing industry concentrated in Austria, Germany, and the Nordic countries, and a strong tradition of bio-based natural building material use across Northern and Central European construction practice.

Germany is projected to command approximately 40% share, fueled by its leadership in timber engineering and bio-based insulations under stringent EU Green Deal mandates. The U.K. holds around 20-25%, driven by net-zero retrofit programs and demand for sustainable cladding. France benefits from RE2020's direct embodied carbon and biogenic carbon sequestration accounting requirements that create the world's most prescriptive direct mandate for bio-based and renewable material adoption in new residential construction.

Asia Pacific Renewable Materials in Construction Market Trends

Asia Pacific is likely to be the fastest-growing regional market for renewable materials, with a projected CAGR of 16.2% from 2026 to 2033, driven primarily by China, India, Japan, and Southeast Asia. Rapid urbanization, government mandates for green buildings, and increasing investment in sustainable infrastructure are accelerating the adoption of crop-based and innovative renewable materials across the region.

China accounts for approximately 50% market share in Asia Pacific, driven by massive infrastructure investments and green building mandates. China's Dual Carbon goals, carbon peak by 2030 and carbon neutrality by 2060, have been operationalized through building energy codes, green building certification standards (China Green Star), and national industrial policy that is directing substantial investments into bio-based building material manufacturing, mass timber processing capacity, and building-integrated solar technology. India holds 20% share, driven by the government's ambitious green building program. India's Green Building Council has certified over 10.27 billion square feet of green building space, national energy efficiency building codes under the Energy Conservation Building Code (ECBC), and growing private developer commitment to LEED and GRIHA certified construction that specifies renewable and low-embodied-carbon materials.

Competitive Landscape

The global renewable materials in construction market features a competitive landscape spanning large multinational specialty chemicals and construction materials corporations, dedicated mass timber manufacturers, bio-based insulation specialists, and innovative sustainable building product companies that collectively address the full spectrum of renewable material applications across the construction value chain. BASF and DowDuPont represent the global specialty chemicals dimension of the market, with both companies investing significantly in bio-based polymer systems, next-generation insulation formulations, and building envelope material innovations that incorporate renewable feedstocks and recycled-content inputs to meet growing regulatory and customer demand for lower-embodied-carbon product alternatives.

BASF's Neopor and Styrodur low-carbon insulation product lines, alongside its investments in bio-based polyurethane precursors, reflect the company's strategic commitment to repositioning its construction materials portfolio toward renewable and circular economy credentials. Sika and Cemex contribute advanced material formulation expertise to the market, with Sika's bio-based admixture and waterproofing systems and Cemex's sustainable concrete and permeable pavement innovations addressing the renewable content and low-carbon dimensions of the structural and civil construction material segments.

Key Industry Developments:

- In March 2026, International Finance Corporation, Global Buildings Performance Network, and Smarter Dharma collaborated to launch the Marketplace for Green Equipment and Materials (MGEM), a digital platform aimed at accelerating sustainable construction in India. The platform enabled developers and builders to discover, compare, and verify green materials through structured data on performance, cost, and availability, while also linking procurement with access to green financing.

- In October 2024, CRH Ventures, the venture capital arm of CRH, announced the launch of its latest accelerator, Sustainable Building Materials.

Companies Covered in Renewable Materials in Construction Market

- BASF

- Alumasc Group

- Binderholz

- Bauder

- DowDuPont

- Forbo

- Kingspan Group

- Cold Mix Manufacturing

- Cemex

- Sika

Frequently Asked Questions

The global renewable materials in construction market is projected to reach US$7.5 billion in 2026.

The renewable materials in construction market are primarily driven by stringent green building regulations, rising demand for low-carbon materials, and global efforts to achieve net-zero construction targets.

The renewable materials in construction market are poised to witness a CAGR of 14.7% from 2026 to 2033.

Key opportunities in the renewable materials in construction market include innovation in high-performance bio-based composites, expansion in emerging economies, and integration into net-zero and energy-positive building projects.

Key players in the renewable materials in construction market include BASF, Alumasc Group, Binderholz, Bauder, DowDuPont, Forbo, Kingspan Group, Cold Mix Manufacturing, Cemex, and Sika.