- Advanced Materials

- Copper-Clad Laminates Market

Copper-Clad Laminates Market Size, Share, and Growth Forecast, 2026 - 2033

Copper-Clad Laminates Market by Product Type (Multi-Layer, High-Frequency, Others), Resin Type (FR-4/Epoxy, High Tg FR-4, Others), Application, and Regional Analysis for 2026 - 2033

Copper-Clad Laminates Market Size and Trends Analysis

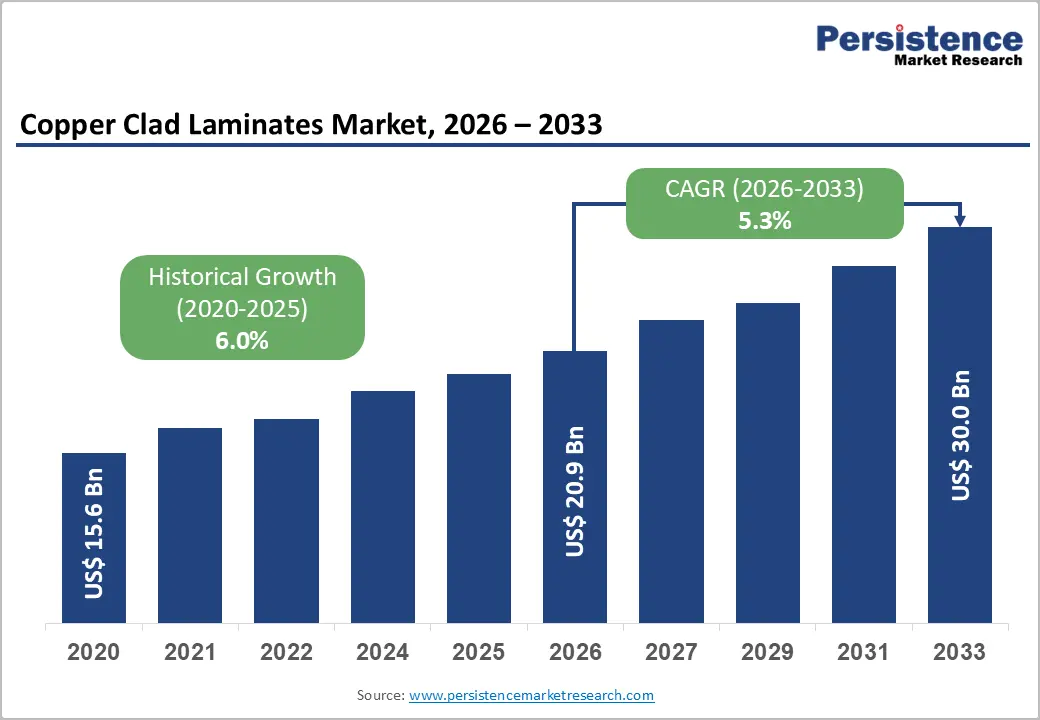

The global copper-clad laminates market size is likely to be valued at US$20.9 billion in 2026 and is expected to reach US$30.0 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033, driven by sustained PCB demand, rapid expansion of 5G infrastructure, and increasing electronics integration in electric vehicles (EVs).

The market is also benefiting from rising adoption of high-speed digital systems and advanced computing architectures, which require low-loss, thermally stable laminate materials. Overall, the industry is transitioning from volume-driven growth to value-driven expansion through high-performance materials.

Key Industry Highlights:

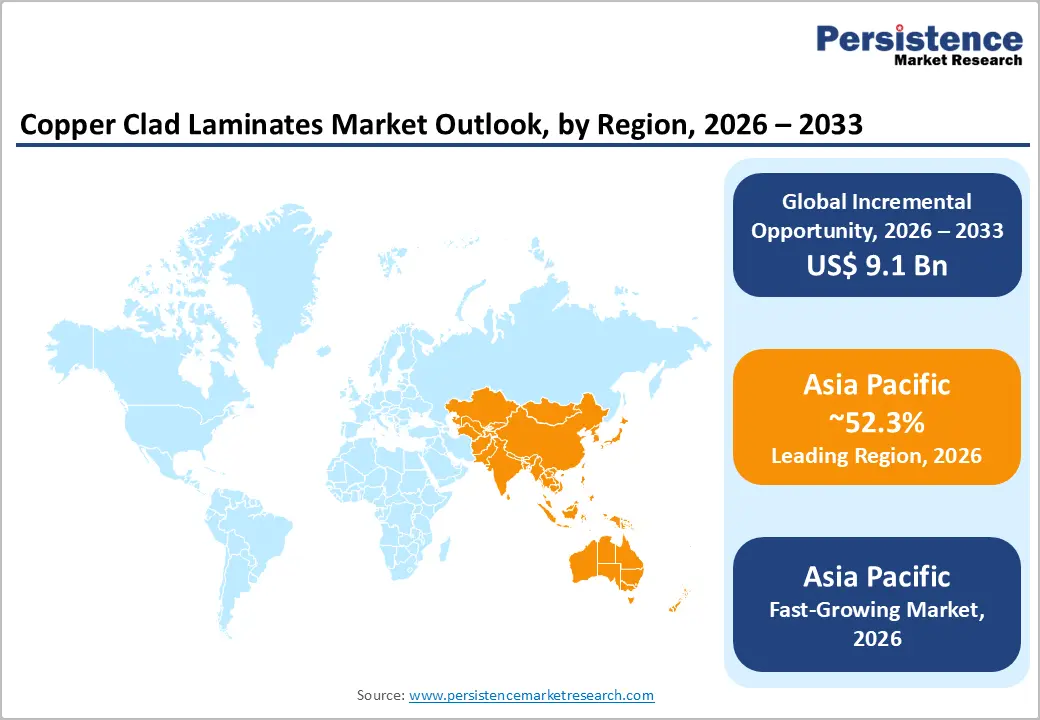

- Leading Region: Asia Pacific is projected to account for approximately 52.3% of the market share, supported by its strong electronics manufacturing ecosystem and integrated PCB supply chains.

- Fastest-growing Region: Asia Pacific is also expected to be the fastest-growing region, driven by rapid expansion in China, India, and Southeast Asia, as well as increasing investment in electronics localization and advanced materials.

- Investment Plans: Significant investments are being directed toward high-performance laminates, semiconductor packaging materials, and localized manufacturing facilities, particularly in the Asia Pacific and North America, to strengthen supply chain resilience and meet rising demand.

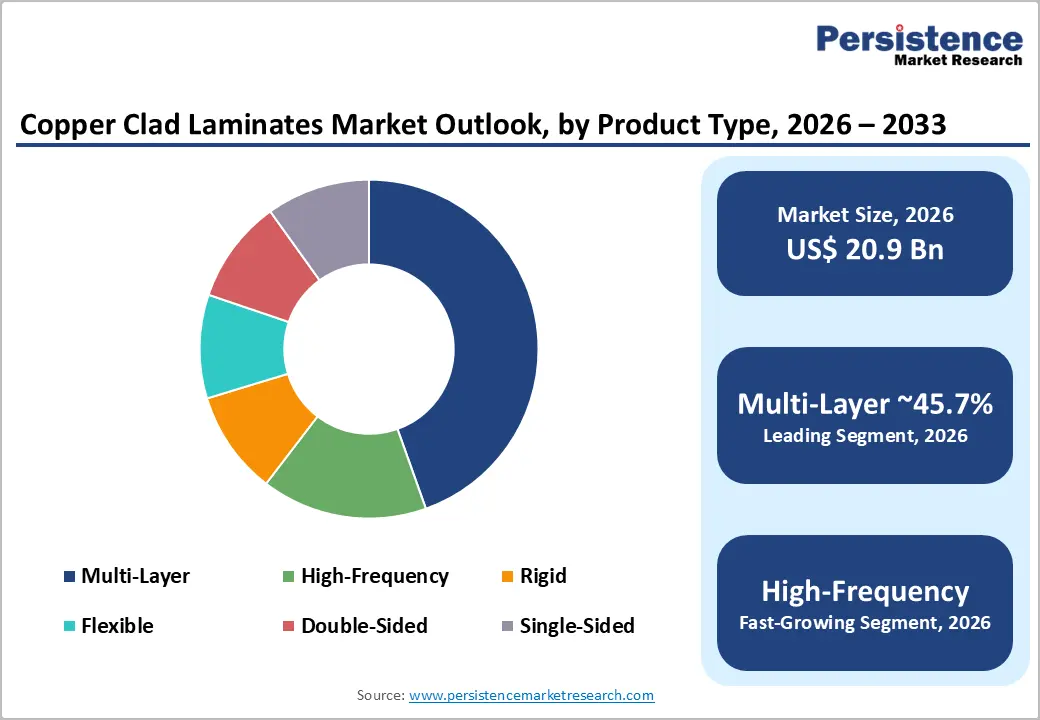

- Dominant Product Type: Multi-layer laminates are anticipated to hold approximately 45.7% of market share, due to their extensive use in high-performance PCBs for telecom, data centers, and automotive electronics.

- Leading Resin Type: FR-4/Epoxy is anticipated to lead the resin type segment with an estimated 34.2% market share, driven by its cost-effectiveness and widespread adoption across consumer electronics and industrial applications.

DRO Analysis

Driver - Increasing PCB Complexity across Consumer Electronics and Digital Infrastructure

The growth of the copper-clad laminates market is closely tied to the expansion and increasing complexity of printed circuit boards (PCBs). As consumer electronics, cloud computing infrastructure, and telecommunications networks evolve, PCB designs are becoming denser, thinner, and more performance-intensive. Devices such as smartphones, servers, and networking equipment now require multilayer architectures and advanced signal integrity, directly increasing demand for high-quality laminates.

Industry shipment data indicates continued expansion in PCB production volumes, particularly in high-speed computing and networking segments. From a materials perspective, this shift drives demand for multilayer laminates and low dielectric-loss materials, which offer improved electrical performance. The result is a dual impact on the market: higher consumption volumes and increased average selling prices (ASPs). This transition reinforces long-term demand stability while elevating the importance of innovation in laminate materials.

Electrification of Vehicles and Growth of ADAS Systems

The automotive sector is emerging as a major driver of copper-clad laminate demand, fueled by the rapid adoption of electric vehicles (EVs) and advanced driver-assistance systems (ADAS). Modern vehicles incorporate significantly higher electronic content, including battery management systems, infotainment platforms, radar modules, and power control units.

Global EV adoption has accelerated significantly, with annual sales exceeding 17 million units in 2024, reflecting a structural shift toward electrified mobility. This transformation requires materials that can withstand high temperatures, mechanical stress, and long operational lifecycles, thereby increasing demand for high Tg FR-4, PTFE-based laminates, and low-loss materials.

Unlike consumer electronics, automotive electronics require lengthy qualification cycles and stringent reliability standards, creating high entry barriers and long-term supplier relationships. As a result, the automotive segment is contributing not only to volume growth but also to the premiumization of the CCL market.

Restraint - Raw Material Volatility and High Qualification Costs

One of the primary structural challenges in the copper-clad laminates market is the volatility in raw material costs, particularly copper foil and resin systems. Copper prices are influenced by global commodity cycles, geopolitical factors, and supply-demand imbalances, leading to fluctuating input costs for manufacturers. At the same time, advanced laminates require specialized resins and manufacturing processes, further increasing production expenses.

In addition, industries such as automotive, aerospace, and telecommunications impose stringent qualification requirements, thereby extending product development timelines and increasing upfront costs. These factors limit manufacturers' ability to quickly adjust pricing or switch production strategies. While demand remains robust, profit margins can vary significantly across product categories, with commodity laminates facing greater cost pressures compared to specialized, high-performance materials.

Opportunity - Localization of Electronics Manufacturing in Emerging Markets

Emerging economies, particularly India, are actively promoting domestic electronics manufacturing through policy initiatives and financial incentives. The introduction of component manufacturing schemes and increased government support for localization are creating new demand opportunities for copper-clad laminates.

The establishment of domestic CCL production facilities represents a strategic shift toward reducing import dependency and strengthening local supply chains. This development is expected to benefit industries such as consumer electronics, telecommunications, and industrial equipment by reducing lead times and improving supply reliability. As electronics manufacturing ecosystems mature in these regions, the demand for locally produced laminates is likely to increase, offering long-term growth potential for both domestic and international players.

Growth in High-Performance Laminates for Advanced Applications

The increasing adoption of high-speed communication systems, semiconductor packaging technologies, and miniaturized electronic devices is creating strong demand for advanced laminate materials. Applications such as 5G infrastructure, AI-driven data centers, and millimeter-wave (mmWave) systems require laminates with low dielectric loss, high thermal stability, and minimal warpage.

Recent product developments indicate a clear shift toward low-thermal-expansion laminates and high-frequency materials, which are essential for next-generation electronics. These materials command higher margins and are less susceptible to commoditization. As technology convergence accelerates, this segment is expected to become a key driver of value creation within the market, particularly in high-growth sectors such as semiconductor packaging and automotive radar systems.

Category-wise Analysis

Product Type Insights

Multi-layer laminates are expected to dominate the product type segment and account for approximately 45.7% of the market share in 2026. Their leadership is driven by widespread adoption in high-performance applications such as telecommunications infrastructure, data centers, and automotive electronics. For instance, multi-layer CCLs are extensively used in 5G base station boards, cloud server motherboards, and advanced driver-assistance systems (ADAS), where high circuit density and signal integrity are critical. These laminates enable complex circuit routing, improved electromagnetic interference (EMI) shielding, and enhanced thermal management, making them essential for modern PCB designs.

The increasing demand for high-density interconnect (HDI) boards, particularly in smartphones and compact computing devices, further reinforces this segment's dominance. In automotive applications, multi-layer laminates are used in battery management systems and infotainment modules, which require durability and multi-layer signal routing. As digital infrastructure expands globally, multi-layer laminates will continue to serve as the foundation of high-performance electronic systems, ensuring sustained demand.

High-frequency laminates are the fastest-growing segment and are anticipated to witness the highest CAGR during the forecast period, driven by the rapid deployment of 5G networks, IoT devices, and high-speed communication systems. These laminates are specifically engineered to minimize signal loss and maintain performance at higher frequencies, making them critical for applications such as millimeter-wave (mmWave) antennas, radar modules in autonomous vehicles, and satellite communication systems.

For example, telecom equipment manufacturers increasingly rely on high-frequency laminates for massive MIMO antennas and small-cell infrastructure, where signal clarity is crucial. Similarly, automotive radar systems operating at 77 GHz require low-loss materials to ensure accurate sensing. Although smaller in volume compared to standard laminates, this segment offers significantly higher margins due to its specialized nature. As connectivity requirements evolve, high-frequency laminates are expected to play a central role in shaping the future of the CCL market.

Resin Type Insights

FR-4/Epoxy is projected to lead and is anticipated to hold approximately 34.2% market share in 2026. Its widespread adoption is attributed to its balanced performance characteristics, cost-effectiveness, and ease of manufacturing. FR-4 is extensively used in smartphones, laptops, televisions, and industrial control systems, making it the backbone of the laminate industry. It is particularly favored for general-purpose PCBs where moderate thermal and electrical performance is sufficient.

In industrial applications, FR-4 laminates are commonly used in power supplies, control panels, and automation equipment, where reliability and cost efficiency are key considerations. Despite the emergence of advanced materials, FR-4 continues to dominate due to its scalability and compatibility with existing manufacturing processes. Its role as a standard material ensures consistent demand across multiple industries.

High Tg FR-4 is the fastest-growing resin type and is anticipated to continue strong growth as adoption increases in high-temperature applications. This material offers superior thermal resistance, making it suitable for environments where standard FR-4 would degrade. Key applications include electric vehicle power electronics, LED lighting systems, industrial motor drives, and high-performance computing boards.

For example, EV battery management systems and onboard chargers require laminates that can withstand prolonged exposure to elevated temperatures, making high Tg FR-4 a preferred choice. Similarly, in industrial automation, control systems operating under continuous load conditions benefit from enhanced thermal stability. This segment effectively bridges the gap between standard FR-4 and high-performance specialty materials, offering a cost-effective solution for reliability-focused applications. As electronic systems become more complex and heat-intensive, the adoption of high Tg FR-4 is expected to accelerate significantly.

Regional Insights

North America Copper Clad Laminates Market Trends - High-Performance CCL Demand Driven by AI, Data Centers, and Defense Innovation

North America is projected to be a high-value market for copper clad laminates, driven by demand from aerospace, defense, telecommunications, and advanced computing industries. The region benefits from a strong innovation ecosystem and increasing investments in data centers and AI infrastructure, particularly in the U.S.

For example, major hyperscale companies such as Amazon Web Services, Microsoft, and Google continue to expand data center capacity across North America, directly increasing demand for high-performance multilayer PCBs and low-loss laminates used in servers and networking equipment. In parallel, material innovation from companies such as Rogers Corporation and Isola Group supports applications in aerospace radar systems and high-frequency communications.

Regulatory requirements related to environmental compliance, safety standards, and supply chain transparency further shape the market. Policies such as the CHIPS and Science Act are encouraging domestic semiconductor and electronics manufacturing, indirectly boosting demand for advanced laminate materials used in chip packaging and interconnects.

These factors favor established players with strong technical capabilities and compliance expertise. Investment opportunities are concentrated in high-margin segments such as RF laminates, advanced packaging substrates, and defense-grade materials, reinforcing North America’s position as a premium, innovation-driven market.

Europe Copper Clad Laminates Market Trends - Sustainability-Driven CCL Adoption Led by EV and Regulatory Compliance

Europe’s market is characterized by a strong emphasis on regulatory compliance and sustainability, particularly through directives governing hazardous substances in electronic materials such as the RoHS Directive. This regulatory environment is pushing manufacturers toward halogen-free and environmentally compliant laminates, increasing demand for advanced material formulations. The region’s automotive and industrial sectors are driving demand for high-reliability laminates, especially as electrification accelerates.

Countries such as Germany, the U.K., France, and Spain contribute significantly through their manufacturing and engineering capabilities. For instance, leading automotive manufacturers such as Volkswagen and BMW are accelerating EV production, increasing the need for high Tg and thermally stable laminates in battery systems and power electronics. Companies such as Infineon Technologies are also expanding semiconductor production in Europe, which drives demand for advanced substrate materials and high-performance CCLs.

The market is relatively stable, with growth driven by automotive electrification, industrial automation, and compliance-driven material upgrades. Europe remains an important region for premium laminate applications, particularly where reliability, safety, and environmental performance are critical purchasing criteria.

Asia Pacific Copper Clad Laminates Market Trends - Dominant High-Volume CCL Manufacturing Hub with Integrated Supply Chains

Asia Pacific is expected to be the largest and fastest-growing region, growing with a projected CAGR of 6.3%. The region’s dominance is supported by its extensive electronics manufacturing base, well-established PCB supply chains, and cost advantages. Countries such as China, Japan, and Taiwan serve as key production hubs, with major laminate manufacturers including Kingboard Laminates Holdings Ltd., Shengyi Technology Co., Ltd., and Nan Ya Plastics Corporation operating on a large scale. These companies benefit from proximity to PCB manufacturers and OEMs, enabling efficient supply chain integration and cost optimization. China holds the leading position in the market with approximately 66% share, driven by major producers such as Kingboard and Shengyi and by its massive PCB manufacturing capacity.

Recent developments further highlight the region’s leadership. In Japan, Resonac Corporation has introduced advanced low-thermal-expansion laminates for semiconductor packaging, supporting next-generation electronics. In Taiwan, Taiflex Scientific Co., Ltd. has expanded production capacity to meet rising demand for flexible electronics used in smartphones and wearable devices. Meanwhile, in India, Wipro Infrastructure Engineering announced the establishment of a domestic copper-clad laminate manufacturing facility, marking a significant step toward localizing the electronics supply chain.

Southeast Asian countries are also gaining traction as alternative manufacturing hubs due to supply chain diversification strategies. Collectively, these developments strengthen Asia Pacific’s position as a fully integrated value chain, capable of supporting both high-volume production and advanced material innovation, making it the primary driver of global market growth.

Competitive Landscape

The global copper-clad laminates market exhibits a moderately concentrated structure, with leading players collectively accounting for over 45% of the global market share. These companies maintain strong positions in high-performance segments through technological expertise and established customer relationships. At the same time, numerous regional and mid-sized players compete in commodity segments, creating a two-tier competitive environment.

Key players are focusing on innovation, product differentiation, and geographic expansion. Strategies include developing high-performance materials, forming strategic partnerships, and investing in localized manufacturing. Companies are increasingly prioritizing high-margin segments and long-term customer relationships to strengthen their competitive positions.

Key Industry Developments:

- In January 2025, DuPont de Nemours, Inc. showcased its Pyralux flexible circuit laminates and Kapton polyimide films at DesignCon 2025, targeting high-performance applications in AI-driven printed circuit boards, 5G infrastructure, and electric vehicles.

Companies Covered in Copper-Clad Laminates Market

- Kingboard Laminates Holdings Ltd.

- Shengyi Technology Co., Ltd.

- Nan Ya Plastics Corporation

- Resonac Corporation

- Elite Material Co., Ltd.

- ITEQ Corporation

- Panasonic Holdings Corporation

- Doosan Corporation Electro-Materials

- Taiwan Union Technology Corporation

- Isola Group

- AGC Inc.

- Taiflex Scientific Co., Ltd.

- DuPont de Nemours, Inc.

- Rogers Corporation

- Sumitomo Bakelite Co., Ltd.

- Resonac Holdings Corporation

Frequently Asked Questions

The copper clad laminates market is valued at US$20.9 billion in 2026.

The market is projected to reach US$30.0 billion by 2033.

Key trends include the growing adoption of high-frequency and low-loss laminates, rising demand from 5G infrastructure and data centers, increasing use in electric vehicles (EVs) and ADAS systems, and a shift toward high Tg and thermally stable materials.

Multi-layer laminates are the leading segment, accounting for approximately 45.7% of the market share, driven by their extensive use in high-performance PCBs.

The copper clad laminates market is expected to grow at a CAGR of 5.3% from 2026 to 2033.

Major players include Kingboard Laminates Holdings Ltd., Shengyi Technology Co., Ltd., Nan Ya Plastics Corporation, Resonac Corporation, and Rogers Corporation.