- Advanced Materials

- Recycled Carbon Fiber Market

Recycled Carbon Fiber Market Size, Share, and Growth Forecast 2026 - 2033

Recycled Carbon Fiber Market by Product Type (Chopped Fiber, Milled Fiber), Source (Aerospace Scrap, Automotive Scrap, Other), End-Use Industry (Automotive & Transportation, Consumer Goods, Sporting Goods, Industrial, Aerospace & Defense, Marine, Others), and Regional Analysis for 2026 - 2033

Recycled Carbon Fiber Market Size and Trend Analysis

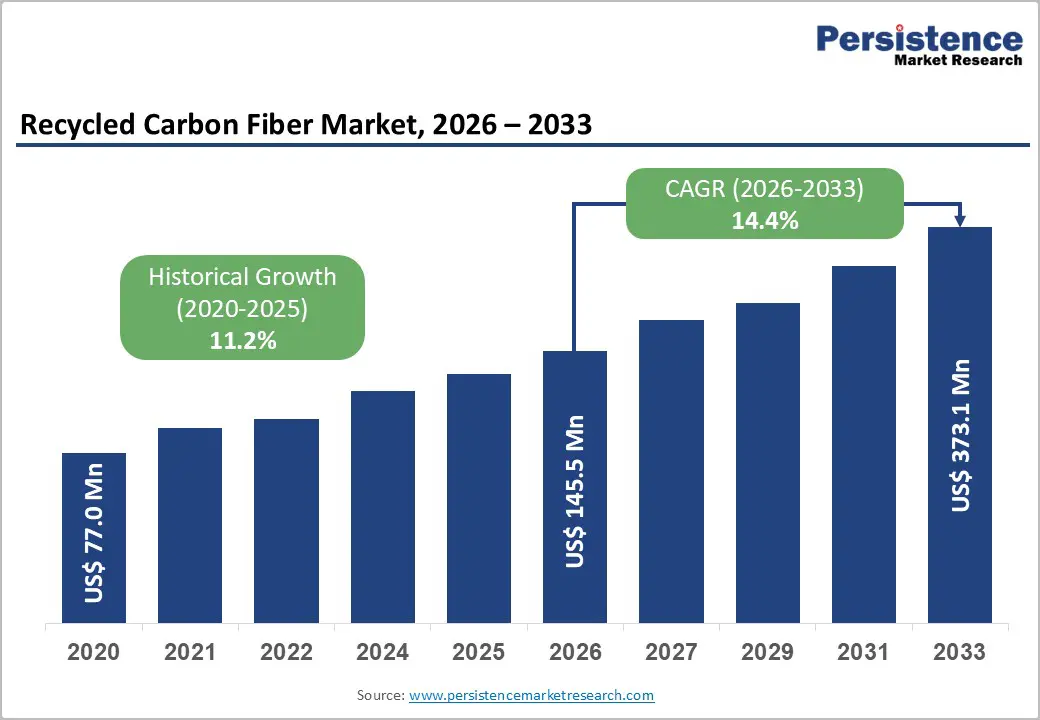

The global recycled carbon fiber market size is valued at US$ 145.5 Mn in 2026 and is projected to reach US$ 373.1 Mn by 2033, growing at a CAGR of 14.4% between 2026 and 2033. This exceptional growth trajectory is anchored by accelerating circular economy mandates, the substantial cost advantage of recycled carbon fiber over virgin grades, and rising demand from automotive lightweighting, aerospace, and sporting goods sectors seeking sustainable, high-performance material inputs.

Regulatory frameworks, including the European Union's End-of-Life Vehicle (ELV) Directive, the EU Green Deal, and corporate net-zero commitments from global OEMs, are structurally expanding feedstock availability and downstream adoption, creating a self-reinforcing demand cycle for recycled carbon fiber through the forecast period.

Key Market Highlights

- Leading Region: Europe leads the global recycled carbon fiber market, anchored by the EU Circular Economy Action Plan, strong Airbus-driven availability of aerospace scrap, and commercially operating recyclers, including Gen 2 Carbon Limited and SGL Carbon, supported by the Fraunhofer ICT innovation ecosystem.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market, driven by China's MIIT strategic material designations, Japan's NEDO-funded process innovation under its Green Growth Strategy, and India's expanding aerospace and defense composites manufacturing programs under the Make in India initiative.

- Dominant Segment: The Chopped Fiber product type segment dominates with approximately 68% of global market revenue, due to its versatility across injection molding, compression molding, and SMC/BMC processing platforms, and its compatibility with existing manufacturing equipment used by automotive and industrial component producers.

- Fastest-Growing Segment: Automotive & Transportation in the end-use industry category is the fastest-growing demand segment, propelled by EU CO2 fleet targets under Regulation 2019/631, the global EV manufacturing boom with approximately 17 million EV units sold in 2024 per IEA data, and established OEM closed-loop recycling models led by BMW Group.

- Key Market Opportunity: The global wind turbine blade decommissioning wave, with an estimated 50,000 blades due for retirement in the U.S. alone by 2025 and IRENA-projected volumes exceeding 40 million metric tons globally by 2050, offers transformational feedstock supply and downstream re-use opportunities for proactive recycled carbon fiber market participants.

| Key Insights | Details |

|---|---|

| Recycled Carbon Fiber Market Size (2026E) | US$ 145.5 Mn |

| Market Value Forecast (2033F) | US$ 373.1 Mn |

| Projected Growth CAGR (2026 - 2033) | 14.4% |

| Historical Market Growth (2020 - 2025) | 11.2% |

DRO Analysis

Market Growth Drivers

Circular Economy Regulations and Corporate Sustainability Mandates Accelerating Adoption

Stringent regulatory pressure and ESG-driven corporate commitments are the foremost structural catalysts propelling the recycled carbon fiber market. The European Union's Circular Economy Action Plan and the End-of-Life Vehicle (ELV) Directive, which mandates that a minimum of 95% by weight of vehicles must be recoverable, with at least 85% through material reuse or recycling, are compelling automotive OEMs and Tier 1 suppliers to integrate recycled material streams into production processes.

In aerospace, the global fleet of next-generation composite-intensive aircraft, including the Boeing 787 Dreamliner and Airbus A350 XWB, which contain 50% and 53% composites by weight, respectively, is generating substantial volumes of manufacturing scrap and end-of-life panel material. The International Air Transport Association (IATA) projects continued aviation fleet expansion through 2035, thereby amplifying the supply of aerospace carbon fiber scrap available to recyclers. These forces, together, are increasing feedstock availability and policy-backed end-market receptivity simultaneously.

Cost Advantage Over Virgin Carbon Fiber Driving Wider Industrial Adoption

The significant cost differential between recycled and virgin carbon fiber is a powerful commercial driver enabling adoption across cost-sensitive end-use industries. Virgin carbon fiber is priced at approximately US$ 20-30 per kilogram, while recycled carbon fiber, depending on form and grade, is typically available at 50-70% lower cost, rendering it highly attractive for automotive structural panels, consumer goods, sporting equipment, and industrial components where premium performance is required but primary-fiber-grade specifications are not mandatory.

The U.S. Department of Energy (DOE) has consistently noted that reducing carbon fiber costs is critical to achieving mass-market lightweight vehicle targets, and recycled fiber directly contributes to this objective. As primary composite production scales in aerospace and wind energy, with global cumulative end-of-life wind turbine blade volumes projected to exceed 40 million metric tons by 2050 according to the International Renewable Energy Agency (IRENA), the upstream feedstock supply for recycled carbon fiber will become increasingly abundant and economically accessible.

Market Restraints

Inconsistency in Recycled Fiber Properties Limiting High-Performance Application Uptake

The primary technical constraint on the recycled carbon fiber market growth is variability in mechanical properties compared to virgin grades. Thermal recycling processes, most notably pyrolysis, can cause changes in surface chemistry, fiber shortening, and reductions in tensile strength of approximately 10-20% relative to virgin carbon fiber, depending on process parameters and feedstock condition.

This inconsistency in fiber length, surface energy, and tensile modulus creates challenges for design engineers seeking to meet certified load-bearing standards in aerospace-grade or structural automotive applications, limiting recycled carbon fiber's addressable market to non-critical and semi-structural component categories. Bridging this performance gap requires further investment in process engineering and surface treatment technologies, which remain an ongoing cost challenge for many smaller recyclers.

Limited Scalability of Recycling Infrastructure and Feedstock Sorting Challenges

Despite strong demand signals, the global recycled carbon fiber industry remains constrained by a fragmented and geographically uneven recycling infrastructure. Carbon fiber reinforced polymer (CFRP) waste requires specialized high-temperature pyrolysis or solvolysis facilities that represent significant capital investment, with industrial pyrolysis plants requiring infrastructure investments typically ranging from US$ 5 Mn to US$ 20 Mn, depending on throughput capacity.

Sorting mixed composite waste streams to segregate carbon fiber from glass fiber, aramid, or hybrid reinforcements poses persistent operational challenges that reduce process efficiency and output quality. The absence of standardized CFRP waste classification protocols and collection networks in developing regions further constrains the reliability of the raw material supply chain, acting as a meaningful drag on market scale-up beyond established recycling hubs in Europe and North America.

Market Opportunities

Wind Energy Sector: A Transformational Feedstock and Demand Opportunity

The global wind energy sector is emerging as both a transformational source of CFRP scrap and a significant new demand channel for recycled carbon fiber materials.

Wind turbine blades, increasingly manufactured using carbon fiber-reinforced composites to enable longer span designs above 80 meters, are beginning to reach end-of-life at scale, with an estimated 50,000 turbine blades due for decommissioning in the United States alone by 2025, according to reporting by Bloomberg NEF. The European Commission has proposed legislation within its Wind Power Action Plan to mandate recyclability standards for turbine blades, further accelerating the flow of recoverable CFRP material into recycling value chains.

The structural push toward carbon-fiber-intensive next-generation blade designs creates a closed-loop opportunity: blade scrap can be processed into chopped or milled recycled carbon fiber for reuse in blade root components, nacelle parts, or automotive structural applications. Companies that establish blade-specific recycling capabilities and downstream re-entry supply chains are well-positioned to capture this high-volume, long-duration demand stream through 2033 and beyond.

Automotive Lightweighting and Electric Vehicle Structural Demand Creating High-Volume Applications

The global automotive industry's accelerating transition to electric vehicles represents a high-growth demand opportunity for recycled carbon fiber materials in structural and semi-structural applications. Battery Electric Vehicles (BEVs) require aggressive weight reduction to extend driving range, and recycled carbon fiber composites, offering approximately 70% of the stiffness of virgin carbon fiber at a fraction of the cost, are attracting serious engineering evaluation for battery enclosures, floor panels, seat frames, bumper beams, and interior structural inserts. According to the International Energy Agency (IEA), global EV sales reached approximately 17 million units in 2024, representing nearly 20% of all new-car sales.

The European Union's CO2 emissions targets for passenger vehicles, mandating fleet-average emissions of 0 g/km by 2035, create a powerful driver for weight-reduction technologies, including recycled-carbon-fiber composites. Automotive OEMs, including BMW Group, which pioneered the use of CFRP in its i3 and i8 platforms and already operates dedicated carbon fiber recycling processes, signal a clear industry direction. This creates a structured demand for high-consistency recycled chopped fiber in injection molding and compression molding automotive applications.

Category-wise Analysis

Product Type Insights

Chopped Fiber is the dominant segment in the product type category, accounting for approximately 68% of the global recycled carbon fiber market revenue. Chopped recycled carbon fiber, produced in lengths typically ranging from 3 mm to 12 mm, is the most versatile and commercially accessible form of recycled carbon fiber, compatible with a broad range of downstream processing technologies, including injection molding, compression molding, sheet molding compound (SMC), and bulk molding compound (BMC) fabrication. Its compatibility with existing thermoplastic and thermoset processing equipment lowers the adoption barrier for automotive, industrial, and consumer goods manufacturers, eliminating the need for capital equipment upgrades.

The consistent flow behavior of chopped recycled fiber in melt-processing systems, a key requirement for high-volume automotive injection molding operations, combined with its cost advantage over virgin chopped carbon fiber, makes it the preferred specification for structural and semi-structural component manufacturing. Growing procurement by Tier-1 automotive suppliers and consumer electronics OEMs further consolidates this segment's market leadership through the forecast period.

Source Insights

Aerospace Scrap is the leading source segment, contributing approximately 52% of the total global recycled carbon fiber market revenue. Aerospace remains the most concentrated and highest-purity source of CFRP manufacturing scrap and end-of-life material, owing to the high carbon fiber content specification of modern commercial aircraft structures. The Boeing 787 Dreamliner contains approximately 35,000 kg of carbon fiber per airframe, and Airbus produces composite-intensive widebody aircraft, including the A350 XWB and A220, each generating substantial cutting, trimming, and laminate scrap during production.

Aviation industry data from the International Air Transport Association (IATA) indicates a projected global fleet size exceeding 47,000 aircraft by 2040, with composite content rising in every new aircraft program, ensuring a structurally growing aerospace scrap supply. The relative homogeneity and high quality of aerospace-origin CFRP scrap make it particularly suited to producing premium recycled carbon fiber grades, commanding price premiums in demanding end-use applications.

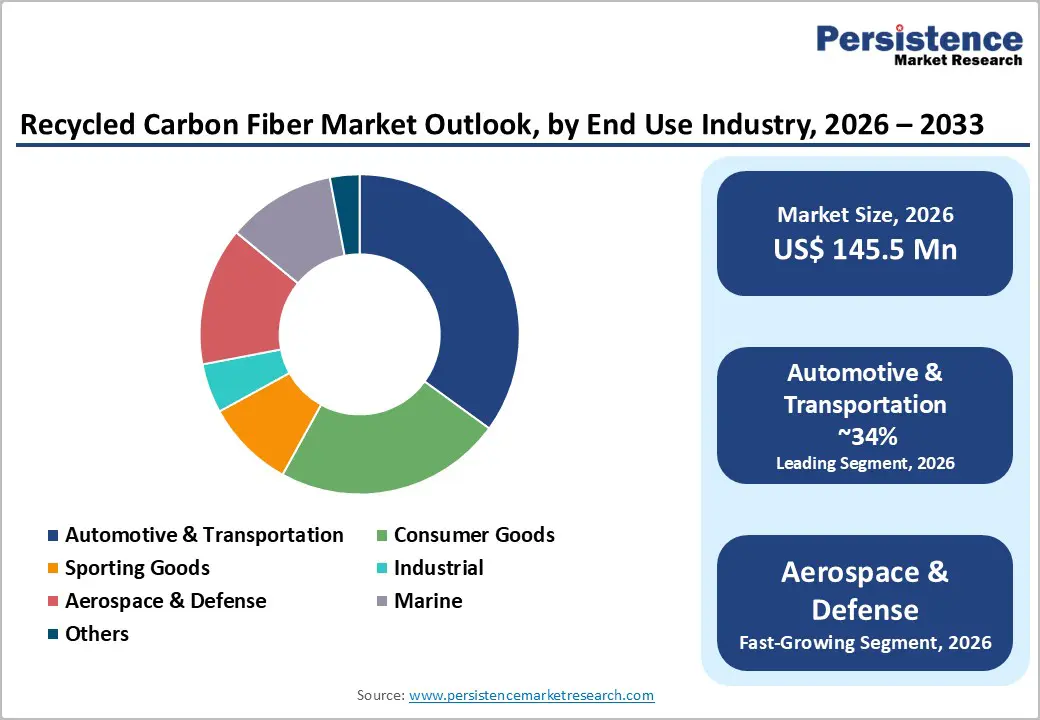

End-Use Industry Insights

The Automotive & Transportation segment leads the end-use industry category, capturing approximately 34% of the global recycled carbon fiber market revenue. This primacy is driven by the automotive industry's dual commitment to cost reduction and regulatory compliance on vehicle weight and emissions performance. Recycled carbon fiber composites are increasingly specified in automotive structural sub-assemblies, including B-pillars, roof reinforcements, underbody panels, and door inners, where carbon fiber properties are required but cost constraints preclude virgin fiber use.

The European Automobile Manufacturers' Association (ACEA) reports that CO2 fleet targets under EU Regulation 2019/631 are compelling manufacturers to invest aggressively in lightweight material substitution programs, with recycled composites representing a cost-viable pathway. BMW Group's established closed-loop CFRP recycling program, which recovers manufacturing waste from its Leipzig facility and reintegrates it into i-series vehicle production, serves as an industry reference model, signaling broad-based automotive-sector commitment to the adoption of recycled carbon fiber.

Regional Analysis

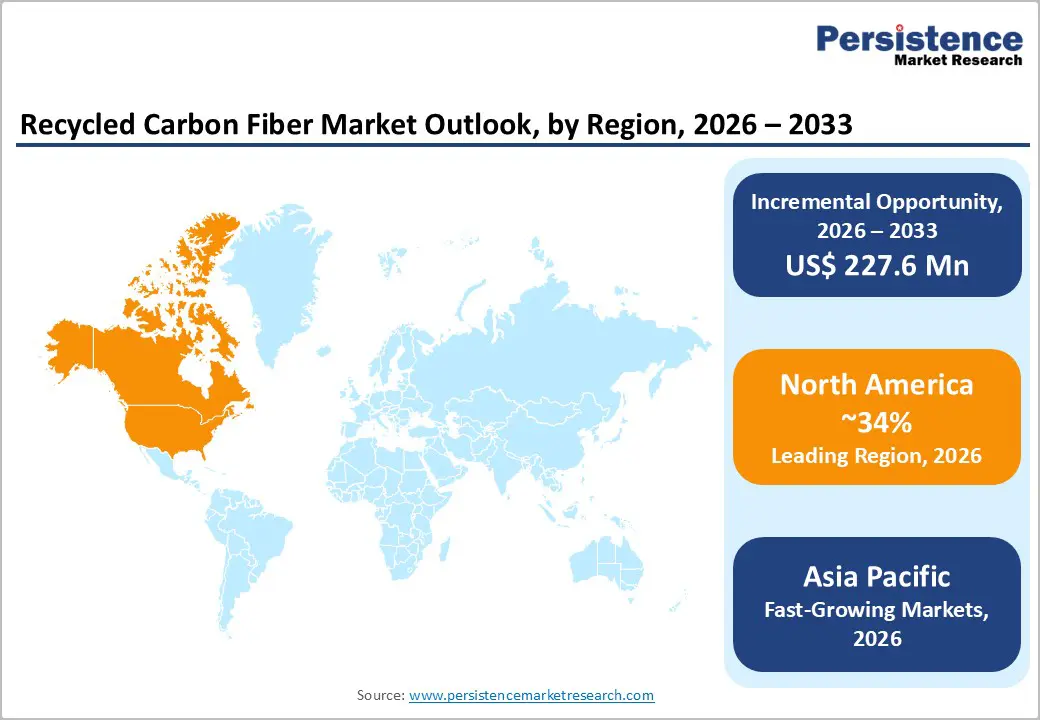

North America Recycled Carbon Fiber Trends & Insights

North America is a leading region in the global recycled carbon fiber market, underpinned by a high concentration of aerospace manufacturing activity, a robust innovation ecosystem, and proactive federal investment in sustainable materials and clean technology. The United States hosts the world's largest commercial aerospace manufacturing base, with Boeing operating major composite manufacturing facilities in Washington, South Carolina, and California, generating substantial volumes of high-quality aerospace CFRP scrap available for the recycled fiber supply chain. The U.S. Department of Energy (DOE) Advanced Manufacturing Office has directed investment toward low-cost carbon fiber and composites recycling technologies, recognizing their strategic importance for both the automotive decarbonization agenda and industrial competitiveness.

The North American recycled carbon fiber innovation ecosystem includes pioneering recyclers such as Vartega Inc. and Carbon Conversions Inc., which are advancing solvolysis and pyrolysis process efficiency for automotive and industrial applications. The U.S. National Composites Center and academic programs at institutions such as the University of Tennessee and Oak Ridge National Laboratory (ORNL) are advancing research on fiber reclamation and characterization. Federal manufacturing incentives under the Inflation Reduction Act (IRA) and the CHIPS and Science Act are creating downstream demand conditions that favor domestically sourced recycled composite materials for EV and electronics manufacturing supply chains.

Europe Recycled Carbon Fiber Trends & Insights

Europe is the global epicenter of recycled carbon fiber technology development, policy leadership, and commercial deployment, driven by the European Union's comprehensive circular economy legislative framework and the region's deep industrial base in aerospace, automotive, and wind energy.

Germany leads regional adoption, with automotive OEMs including BMW Group, Volkswagen AG, and Mercedes-Benz Group AG operating established CFRP recycling and re-integration programs supported by research partnerships with the Fraunhofer Institute for Chemical Technology (ICT) and the German Aerospace Center (DLR). The EU's Circular Economy Action Plan, REACH chemical regulations, and the proposed revision to the End-of-Life Vehicle Regulation collectively mandate increased recyclate content and prohibit landfilling of composite waste, providing the strongest policy scaffolding for the recycled carbon fiber market globally.

The United Kingdom hosts several specialist recycled carbon fiber companies, including Gen 2 Carbon Limited, formerly ELG Carbon Fibre, which operates Europe's largest dedicated carbon fiber recycling facility in Coseley, West Midlands, processing aerospace and automotive CFRP scrap into high-quality chopped and milled recycled fiber for global customers.

France contributes through Alpha Recyclage Composites and strong aerospace demand from the Airbus supply chain concentrated in the Toulouse and Bordeaux corridor. Spain's growing wind energy manufacturing sector is adding blade scrap-derived feedstock. The European Clean Aviation initiative and Horizon Europe funding programs are directing significant research investment into closed-loop composite recycling, reinforcing Europe's global technology leadership in this field.

Asia Pacific Recycled Carbon Fiber Trends & Insights

Asia Pacific is the fastest-growing region in the global recycled carbon fiber market, propelled by China's dominant virgin carbon fiber production base and surging downstream composites manufacturing, alongside Japan's deep technical expertise in advanced fiber processing. China is simultaneously the world's largest carbon fiber producer and the most rapidly expanding composites consumer market, with the Ministry of Industry and Information Technology (MIIT) designating carbon fiber composites as a strategic advanced material under successive Five-Year Plans.

China's growing CFRP manufacturing and end-of-life scrap volumes, from wind turbine blades, EVs, and electronics manufacturing, are creating the supply conditions for a domestic recycled carbon fiber industry, with companies including Carbon Fiber Recycling, Inc. and emerging domestic recyclers beginning to scale operations.

Japan has long been the technological heart of the global carbon fiber industry, home to Toray Industries, Teijin Limited, and Mitsubishi Chemical Group, and is actively transitioning these competencies toward recycled fiber processing and bio-circular composite platforms. Japan's New Energy and Industrial Technology Development Organization (NEDO) has funded multiple programs to develop recycled carbon fiber processes aligned with the country's Green Growth Strategy, targeting carbon neutrality by 2050. India is an emerging participant, driven by government-backed expansion of aerospace and defense manufacturing under the Make in India initiative, while ASEAN nations, particularly Malaysia and Vietnam, are building composite manufacturing bases that will generate recycled carbon fiber feedstocks at increasing scale over the forecast period.

Competitive Landscape

The global recycled carbon fiber market is characterized by a highly fragmented competitive structure, comprising a diverse mix of large multinational fiber producers with dedicated recycling divisions, specialist recycling technology companies, and emerging regional processors.

Market differentiation is primarily driven by recycling process technology, pyrolysis versus solvolysis, feedstock quality management, fiber product consistency, and downstream application development capability. Leading players, including Toray Industries, SGL Carbon SE, and Teijin Limited, leverage their virgin fiber expertise and global customer networks to accelerate recycled product commercialization.

Strategic trends include capacity expansion investments, establishment of long-term aerospace OEM feedstock supply agreements, technology licensing partnerships, and integration into circular supply chain programs with automotive and wind energy sector partners. IP-protected pyrolysis process innovation and proprietary surface treatment capabilities are emerging as decisive competitive differentiators.

Key Market Developments

- In March 2025, Vartega Inc. announced a strategic partnership with a major U.S. automotive Tier 1 supplier to scale recycled carbon fiber compound supply for injection-molded EV structural components, marking a significant commercial milestone for domestic closed-loop automotive composites supply chains.

- In November 2024, SGL Carbon SE expanded its CFRP recycling processing capacity at its Meitingen, Germany facility, increasing pyrolysis throughput for aerospace scrap-derived chopped and milled recycled carbon fiber to serve growing demand from European automotive and industrial customers.

- In January 2023, Gen 2 Carbon Limited secured long-term supply agreements with Airbus UK for the collection and processing of A350 and A220 manufacturing scrap from UK-based facilities, ensuring feedstock security and reinforcing the company's position as Europe's leading carbon fiber recycler.

Companies Covered in Recycled Carbon Fiber Market

- Toray Industries, Inc.

- SGL Carbon SE

- Gen 2 Carbon Limited

- Carbon Conversions Inc.

- Vartega Inc.

- Procotex Corporation SA

- Mitsubishi Chemical Group Corporation

- Teijin Limited

- Sigmatex Limited

- Hadeg Recycling GmbH

- Alpha Recyclage Composites

- Carbon Fiber Recycling, Inc.

- Karborek Recycling Carbon Fibers

- Shocker Composites LLC

- Adherent Technologies, Inc.

Frequently Asked Questions

The global Recycled Carbon Fiber market is valued at US$ 145.5 Mn in 2026 and is projected to reach US$ 373.1 Mn by 2033, growing at a robust CAGR of 14.4% during the forecast period. This strong momentum is underpinned by circular economy mandates, cost advantages over virgin carbon fiber, and expanding aerospace and automotive composite scrap availability.

The primary demand drivers are the EU's Circular Economy Action Plan and ELV Directive mandating high composite material recovery rates, and the significant cost advantage of recycled carbon fiber, priced 50-70% below virgin grades at approximately US$ 20-30 per kilogram for primary fiber, enabling wider industrial and automotive adoption without compromising lightweight performance requirements.

Chopped Fiber leads the product type category with approximately 68% of global market revenue, driven by its compatibility with widespread injection molding and compression molding platforms, its versatility across automotive, industrial, and consumer goods applications, and its consistent flow behavior in melt-processing systems used by high-volume Tier 1 automotive component manufacturers.

Europe is the dominant regional market for recycled carbon fiber, supported by the EU Circular Economy Action Plan, stringent End-of-Life Vehicle Directive recycling mandates, and the presence of the world's most technically advanced recyclers, including Gen 2 Carbon Limited and SGL Carbon SE, alongside strong aerospace scrap supply from Airbus manufacturing operations across France, Germany, and the United Kingdom.

The wind turbine blade decommissioning wave presents the most transformational opportunity, with IRENA projecting over 40 million metric tons of end-of-life blade material globally by 2050 and an estimated 50,000 blades due for retirement in the U.S. alone by 2025. The European Commission's Wind Power Action Plan further mandates recyclability standards, unlocking large-scale CFRP feedstock supply for closed-loop recycled carbon fiber value chains.

Leading companies in the global Recycled Carbon Fiber market include Toray Industries, Inc., SGL Carbon SE, Teijin Limited, Gen 2 Carbon Limited, Mitsubishi Chemical Group Corporation, Vartega Inc., Carbon Conversions Inc., Procotex Corporation SA, Sigmatex Limited, Alpha Recyclage Composites, Hadeg Recycling GmbH, Karborek Recycling Carbon Fibers, Shocker Composites LLC, and Adherent Technologies, Inc., among others.