- Non-food Packaging

- Refillable Packaging Market

Refillable Packaging Market Size, Share, and Growth Forecast 2026 - 2033

Refillable Packaging Market by Packaging Type (Pallets & Crates, Bottles & Containers, Intermediate Bulk Containers (IBCs), Drums & Barrels, Boxes & Cartons, Reusable Pouches & Refill Packs, Returnable Transport Packaging (RTP)), Material Type, Application, End-user, and Regional Analysis, 2026 - 2033

Refillable Packaging Market Size and Trend Analysis

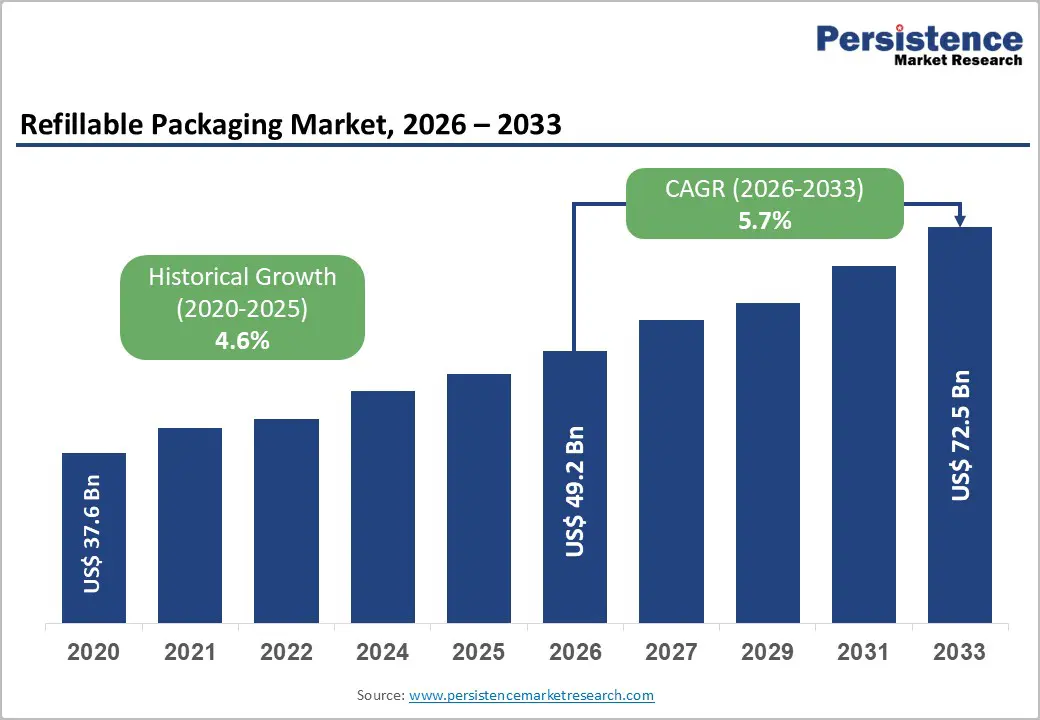

The global refillable packaging market size is likely to be valued at US$ 49.2 billion in 2026 and is expected to reach US$ 72.5 billion by 2033, growing at a CAGR of 5.7% during the forecast period from 2026 to 2033. The refillable packaging market is advancing steadily, propelled by tightening global single-use plastic regulations, growing corporate sustainability commitments, and rising consumer preference for environmentally responsible packaging solutions.

Key Industry Highlights:

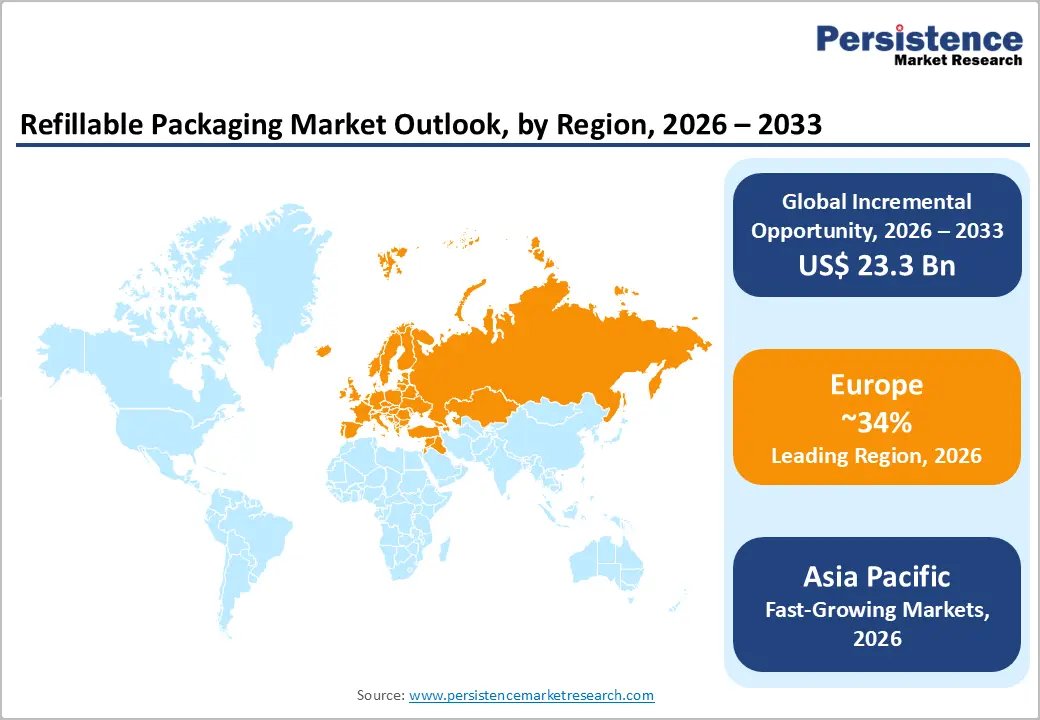

- Leading Region: Europe leads the global refillable packaging market, likely to account for 34% share, driven by the world's most advanced regulatory framework, including the EU PPWR, Germany's Pfand deposit-return system, and France's AGEC Law mandating reusable packaging across key consumer categories.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with a CAGR of 6.9%, with China's circular economy policy, India's Plastic Waste Management Rules, and ASEAN plastic reduction roadmaps collectively accelerating refillable packaging adoption across consumer goods and industrial supply chains.

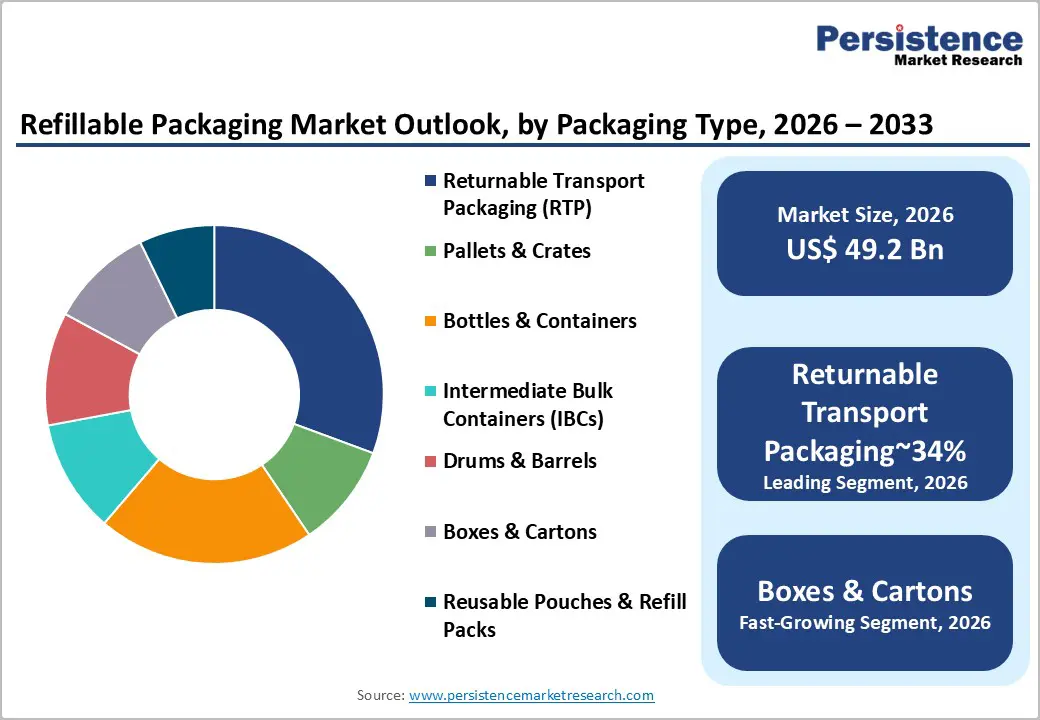

- Dominant Packaging Segment: Returnable Transport Packaging (RTP) dominates with approximately 34% market share, supported by decades of established use across automotive, chemical, and food & beverage supply chains and growing e-commerce logistics adoption.

- Fastest Growing Segment: Cosmetics & personal care is the fastest-growing end-use segment, driven by luxury and mass-market beauty brands launching premium refillable bottle programs and DTC concentrate refill formats to meet consumer sustainability expectations.

- Key Opportunity: E-commerce-enabled DTC refill business models, leveraging concentrated refill pouches, tablets, and subscription formats, represent a high-growth opportunity for packaging manufacturers serving sustainability-driven FMCG brands targeting eco-conscious consumers.

Market Dynamics

Drivers - Stringent Single-Use Plastic Regulations and Circular Economy Mandates

The global regulatory tide against single-use plastics is the most powerful structural driver for the refillable packaging market. The European Union's Single-Use Plastics Directive (SUPD) bans a range of single-use plastic products and mandates that member states establish reuse and refill systems across key product categories.

The EU Packaging and Packaging Waste Regulation (PPWR), finalized in 2024, sets mandatory targets for reusable packaging, requiring that 10% of takeaway food packaging be offered in reusable formats by 2030. The United Nations Environment Program (UNEP) is also advancing a global plastics treaty that is expected to mandate reuse targets across signatory nations. These interlocking regulatory frameworks create a non-discretionary demand environment for refillable packaging solutions, driving manufacturer and brand adoption at scale.

Rising Corporate Sustainability Commitments and ESG-Driven Packaging Strategies

Leading global consumer goods companies are embedding refillable packaging into their core sustainability strategies, generating substantial commercial demand for refillable packaging manufacturers. Unilever, Nestlé, Procter & Gamble, and L'Oréal have all publicly committed to reusable and refillable packaging targets as part of their net-zero and plastic waste reduction roadmaps.

The Ellen MacArthur Foundation's New Plastics Economy Global Commitment, signed by over 500 organizations representing more than 20% of global plastic packaging production, includes specific targets for refill and reuse. These commitments translate directly into long-term, high-volume procurement contracts for refillable packaging suppliers, providing a durable demand foundation beyond regulatory compliance alone.

Restraints - High Initial Capital Investment and Reverse Logistics Complexity

Transitioning from single-use to refillable packaging systems requires significant upfront capital investment in packaging design, washing and sterilization infrastructure, and reverse logistics networks. For small and mid-size brands, establishing cost-effective collection, cleaning, and redistribution systems can be prohibitively expensive.

A World Economic Forum analysis of reuse system economics indicates that refillable models typically require 5–10 reuse cycles to achieve environmental and economic breakeven versus single-use alternatives, depending on geography and logistics density. This capital burden acts as a meaningful adoption barrier, particularly in markets lacking established returns infrastructure.

Consumer Behavior, Inertia and Convenience Preferences

Despite growing environmental awareness, consumer adoption of refillable packaging systems is constrained by the persistent preference for convenience. Studies published in the Journal of Cleaner Production indicate that consumer participation in voluntary refill schemes declines significantly when systems require extra steps, such as carrying return packaging, visiting specific collection points, or pre-planning purchases.

Return rates for voluntary deposit-and-return systems vary widely, from over 90% in mature European markets to below 30% in markets without mandated infrastructure, limiting system economics and environmental impact.

Opportunities - Food & Beverage Sector Adoption of Reusable Bottles and Bulk Refill Stations

The food and beverage sector represents the largest and most rapidly developing opportunity for refillable packaging manufacturers. Grocery retailers and specialty food brands across Europe and North America are rapidly expanding in-store bulk refill stations for liquids, grains, and personal care products. Carrefour, Aldi, and Whole Foods Market have piloted or scaled in-store refill programs.

The Ellen MacArthur Foundation estimates that shifting 20% of beverage packaging to reuse models could eliminate millions of tonnes of plastic waste annually. EU reuse targets under the PPWR mandate refillable options for beverages by 2030, creating a compliance-driven commercial runway for suppliers of refillable bottles, containers, and dispensing equipment across the food and beverage value chain.

E-commerce and Direct-to-Consumer Refill Pack Business Models

The growth of direct-to-consumer (DTC) e-commerce channels is enabling a new generation of refill-at-home packaging models that bypass traditional retail constraints. Brands such as HiBar, Blueland, and Grove Collaborative have built commercially viable businesses around concentrated refill tablets, pouches, and minimal-plastic refill packs delivered directly to consumers.

The U.S. e-commerce market for sustainable consumer goods has grown at double-digit rates, and platforms including Amazon are investing in refillable and subscribe-and-save packaging programs. For packaging manufacturers, this trend creates demand for lightweight, cost-efficient reusable pouches, concentrated refill formats, and DTC-optimized refillable bottles and containers, a high-growth segment where product differentiation and barrier materials innovation offer significant value-creation opportunity.

Category-wise Analysis

By Packaging Type Insights

Returnable Transport Packaging (RTP) is the dominant packaging type segment, accounting for approximately 34% of the global refillable packaging market. RTP, encompassing pallets, crates, IBCs, drums, and bulk containers used across supply chains, has been the most established and commercially mature refillable packaging segment for decades. Industrial users, including automotive, chemicals, and food & beverage manufacturers, rely on RTP to reduce per-trip packaging costs, minimize waste, and comply with supply chain sustainability standards.

The Reusable Packaging Association (RPA) estimates that reusable pallets save over US$ 2 billion annually in U.S. supply chain costs compared to single-use alternatives. Growing e-commerce logistics volumes are further expanding RTP adoption, as third-party logistics operators and retailers seek standardized, cost-effective returnable container systems for their distribution networks.

By Material Type Insights

Plastic remains the dominant material in the refillable packaging market, accounting for approximately 43% of total material consumption. Despite growing environmental concerns about plastic waste, high-density polyethylene (HDPE), polypropylene (PP), and PET continue to dominate refillable packaging applications due to their durability, light weight, chemical resistance, and cost-effectiveness across multiple reuse cycles.

The Plastics Industry Association notes that well-designed rigid plastic refillable containers can achieve 25–50 reuse cycles before replacement, delivering favorable lifecycle environmental and economic performance. Post-consumer recycled (PCR) plastic content integration is further improving the sustainability credentials of plastic refillable packaging, helping manufacturers meet EPR and recycled content mandates while maintaining structural performance across repeated use.

By Application Insights

Liquid packaging is the leading application segment, commanding approximately 38% of the refillable packaging market. The breadth of liquid packaging applications, spanning beverages, personal care, household cleaners, industrial chemicals, and food ingredients, makes this the most commercially significant application category. Refillable bottles, IBCs, and dispensing containers for liquid products are well-established across both consumer and industrial markets.

The beverage sector alone, including returnable glass and PET bottle systems for soft drinks, beer, and water, represents a multi-billion-dollar legacy of refillable packaging. Regulatory mandates in the EU and Asia Pacific for refillable beverage containers are reinforcing and expanding liquid packaging's dominant position across the forecast period.

By End-user Insights

Food & Beverage is the dominant end-use sector, accounting for approximately 32% of the global refillable packaging market revenue. The food and beverage sector has the longest-established history of refillable packaging, from glass milk bottles to returnable PET beverage containers, and is currently undergoing a new wave of refillable adoption driven by regulatory mandates, retailer sustainability commitments, and consumer demand for sustainable packaging.

Germany's Pfand (deposit-return) system achieves return rates above 97% for refillable PET and glass beverage containers, demonstrating the commercial viability of scaled food & beverage refillable systems. The EU's PPWR reuse targets further mandate the expansion of refillable options across member states, providing sustained regulatory support for this sector.

Regional Insights

North America Refillable Packaging Market Trends & Analysis

North America represents a mature yet accelerating refillable packaging market, supported by regulatory mandates and corporate ESG commitments. The region accounts for approximately 28% of the global market in 2026, translating to nearly USD 13.5 billion. Growth is driven by circular logistics adoption, retailer-led refill systems, and compliance with plastic reduction laws.

- U.S. Refillable Packaging Market Size

The United States dominates North America with an estimated market size of USD 11.0 billion in 2026, growing at around 5.5% CAGR. Expansion is fueled by state-level regulations such as California’s SB 54, strong adoption of reusable transport packaging (RTP), and increasing participation from e-commerce and grocery supply chains.

Europe Refillable Packaging Market Trends, Drivers & Insights

Europe leads globally, contributing approximately 34% of the global market, equating to USD 15.5 billion in 2026. Strong regulatory frameworks such as PPWR and deposit-return systems are key drivers. High consumer awareness and strict reuse mandates position Europe as the most advanced circular packaging ecosystem.

- Germany Refillable Packaging Market Size

Germany is Europe’s largest market, valued at approximately USD 5.0 billion in 2026, expanding at 5.0% CAGR. The well-established Pfand system and VerpackG regulations drive high return rates and widespread adoption of reuse, particularly in the beverage and retail packaging sectors.

- U.K. Refillable Packaging Market Size

The U.K. market is estimated at USD 3.2 billion in 2026, growing at 5.8% CAGR. The implementation of Extended Producer Responsibility (EPR) and increasing retailer-led refill initiatives are accelerating adoption across food, beverage, and household product categories.

- France Refillable Packaging Market Size

France’s market is projected at USD 2.9 billion in 2026, with a 5.6% CAGR. The AGEC law is a key growth catalyst, mandating reuse in foodservice and promoting refill systems. Strong government backing and consumer participation are boosting the penetration of refillable packaging.

Asia Pacific Refillable Packaging Market Drivers & Analysis

Asia Pacific is the fastest-growing region, accounting for approximately 30% of the market and reaching USD 14.7 billion in 2026, with a 6.5% CAGR. Growth is driven by regulatory tightening, industrial expansion, and increasing plastic waste management initiatives across emerging economies.

- China Refillable Packaging Market Size

China leads the region with an estimated USD 6.8 billion market in 2026, growing at 6.8% CAGR. Government policies under the 14th Five-Year Plan and bans on single-use plastics are accelerating adoption across manufacturing, food & beverage, and logistics sectors.

- India Refillable Packaging Market Size

India’s market is valued at approximately USD 3.3 billion in 2026, expanding at a strong 7.5% CAGR. Growth is driven by the Plastic Waste Management Rules, the expansion of FMCG refill models, and rising awareness of sustainable packaging among urban consumers and businesses.

- Japan Refillable Packaging Market Size

Japan’s refillable packaging market is estimated at USD 2.6 billion in 2026, growing at 4.8% CAGR. A mature recycling culture, established deposit-return systems, and widespread adoption of refillable containers in beverages and personal care products support steady market expansion.

Competitive Landscape

The global refillable packaging market is highly fragmented, with a diverse mix of large multinational packaging conglomerates, including Amcor plc, International Paper, and Smurfit Kappa Group, and specialized reusable packaging players such as ORBIS Corporation and Schoeller Allibert. Key differentiators include lifecycle sustainability credentials, material innovation (PCR content, biodegradable alternatives), digital track-and-trace capabilities for closed-loop systems, and supply chain partnership depth.

Emerging business models include packaging-as-a-service (PaaS), pool management platforms, and technology-enabled deposit-return system management. Consolidation is ongoing, with larger players acquiring specialist reusable packaging firms to build circular economy capability and capture EPR-driven market growth.

Key Developments:

- February, 2025: Amcor plc announced the commercial launch of its AmLite Ultra Recyclable refillable pouch range, designed for personal care and household care refill-at-home applications, targeting FMCG brands with EU PPWR reuse compliance requirements.

- October, 2024: Smurfit Kappa Group unveiled its fully circular returnable corrugated transit packaging system for e-commerce fulfillment, achieving over 20 reuse cycles per unit and targeting major European online retail and logistics operators.

- April, 2023: ORBIS Corporation expanded its North American reusable plastic container and pallet pooling service for food & beverage supply chains, adding new regional depots to reduce reverse logistics costs and improve closed-loop system economics for retail customers.

Global Refillable Packaging Market - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 37.6 Bn |

|

Current Market Value (2026) |

US$ 49.2 Bn |

|

Projected Market Value (2033) |

US$ 72.5 Bn |

|

CAGR (2026-2033) |

5.7% |

|

Leading Region |

Europe, 34% share |

|

Dominant Packaging Type |

Returnable Transport Packaging (RTP), 34% share |

|

Top-ranking End Use |

Food & Beverage, 32% |

|

Incremental Opportunity |

US$ 23.3 Bn |

Companies Covered in Refillable Packaging Market

- Amcor plc

- Greiner Packaging

- ORBIS Corporation

- Plastipak Industries Inc.

- RPC Group

- Reynolds Group

- Sem Plastik

- Double H Plastics

- Tek Pak

- Sanpaca

- Schoeller Allibert

- International Paper

- Mondi plc

- Smurfit Kappa Group

- Nefab Group

- DS Smith plc

- Mauser Packaging Solutions

- Brambles Limited

Frequently Asked Questions

The global Refillable Packaging market is valued at US$ 49.2 Billion in 2026 and is projected to reach US$ 72.5 Billion by 2033, at a CAGR of 5.7% over the forecast period. Historically, the market grew at a CAGR of 4.6% from 2020 to 2025, driven by tightening single-use plastic regulations, rising corporate ESG commitments, and growing consumer preference for sustainable packaging alternatives.

The primary demand drivers are stringent regulatory mandates, notably the EU Packaging and Packaging Waste Regulation (PPWR) with mandatory reuse targets, and rising corporate sustainability commitments from global FMCG leaders including Unilever, Nestlé, and Procter & Gamble. The Ellen MacArthur Foundation's New Plastics Economy Global Commitment, signed by over 500 organizations, further institutionalizes demand for refillable packaging solutions across the consumer goods industry.

Returnable Transport Packaging (RTP) is the dominant segment with approximately 34% market share. RTP encompasses pallets, crates, IBCs, and bulk containers used across industrial supply chains, and represents the most commercially mature refillable packaging category. The Reusable Packaging Association estimates that reusable pallets save over US$ 2 billion annually in U.S. supply chain costs, underscoring RTP's proven economic and environmental value.

Europe is the global leader in refillable packaging adoption, underpinned by the world's most comprehensive regulatory framework including the EU PPWR, Germany's Pfand deposit-return system, France's AGEC Law, and national EPR frameworks across member states. Germany achieves beverage container return rates above 97%, demonstrating the commercial viability and environmental effectiveness of mature, mandated refillable packaging systems.

The most significant growth opportunities are in the food & beverage sector's expansion of in-store and DTC bulk refill programs, driven by EU PPWR reuse mandates, and in the emerging e-commerce refill-at-home market, where brands leveraging concentrated refill pouches, tablets, and subscription packaging formats are capturing rapidly growing consumer demand for convenient sustainable consumption.

Leading companies in the global Refillable Packaging market include Amcor plc, Greiner Packaging, ORBIS Corporation, Plastipak Industries Inc., RPC Group, Reynolds Group, Schoeller Allibert, International Paper, Mondi plc, Smurfit Kappa Group, Nefab Group, DS Smith plc, Mauser Packaging Solutions, and Brambles Limited (CHEP), among others.