- Non-food Packaging

- Fluff Pulp Market

Fluff Pulp Market Size, Share, and Growth Forecast 2026 - 2033

Fluff Pulp Market by Product Type (Southern Softwood Fluff Pulp (SBSK), Northern Softwood Fluff Pulp (NBSK), Hardwood Fluff Pulp, Bleached Fluff Pulp, Unbleached Fluff Pulp), by Fiber Source (Softwood-Based, Hardwood-Based, Blended Fiber), by Application (Baby Diapers, Adult Incontinence Products, Feminine Hygiene Products, Air-Laid Products, Medical Absorbents, Nonwoven Products, Others), End-user, and Regional Analysis, 2026 - 2033

Fluff Pulp Market Size and Trend Analysis

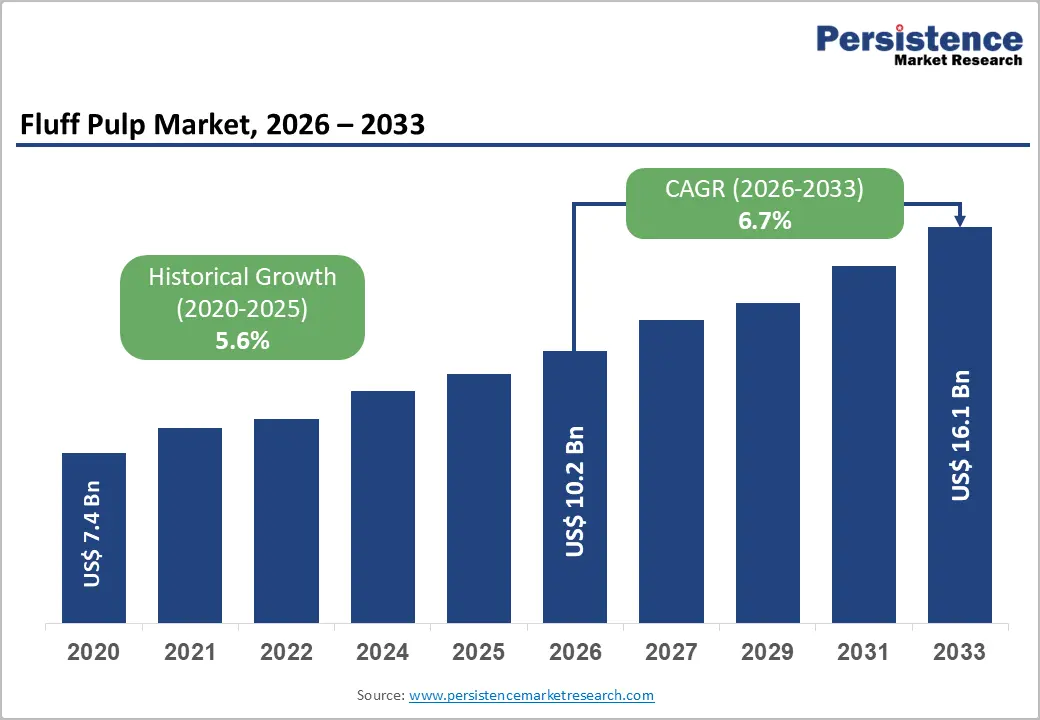

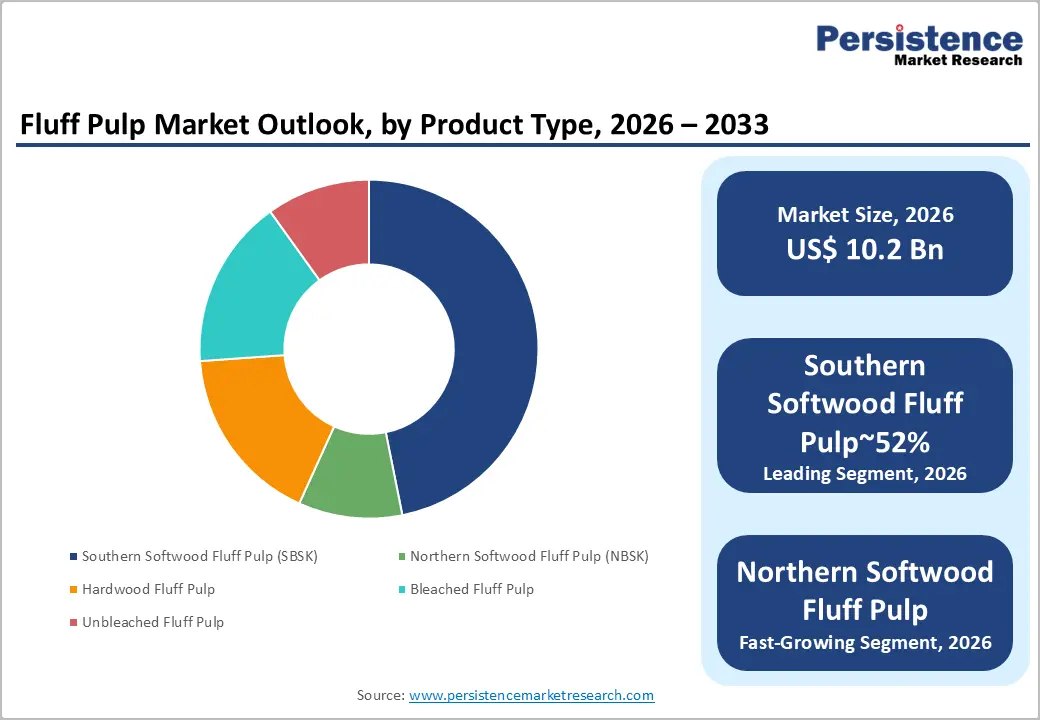

The global fluff pulp market size is likely to be valued at US$10.2 billion in 2026 and is expected to reach US$16.1 billion by 2033, growing at a CAGR of 6.7% during the forecast period from 2026 to 2033.

The market is advancing on robust structural foundations driven by accelerating global demand for absorbent hygiene products, a rapidly aging world population amplifying adult incontinence product consumption, and rising hygiene awareness and disposable income levels in high-growth emerging markets, enabling the transition from reusable to disposable hygiene solutions.

Key Market Highlights

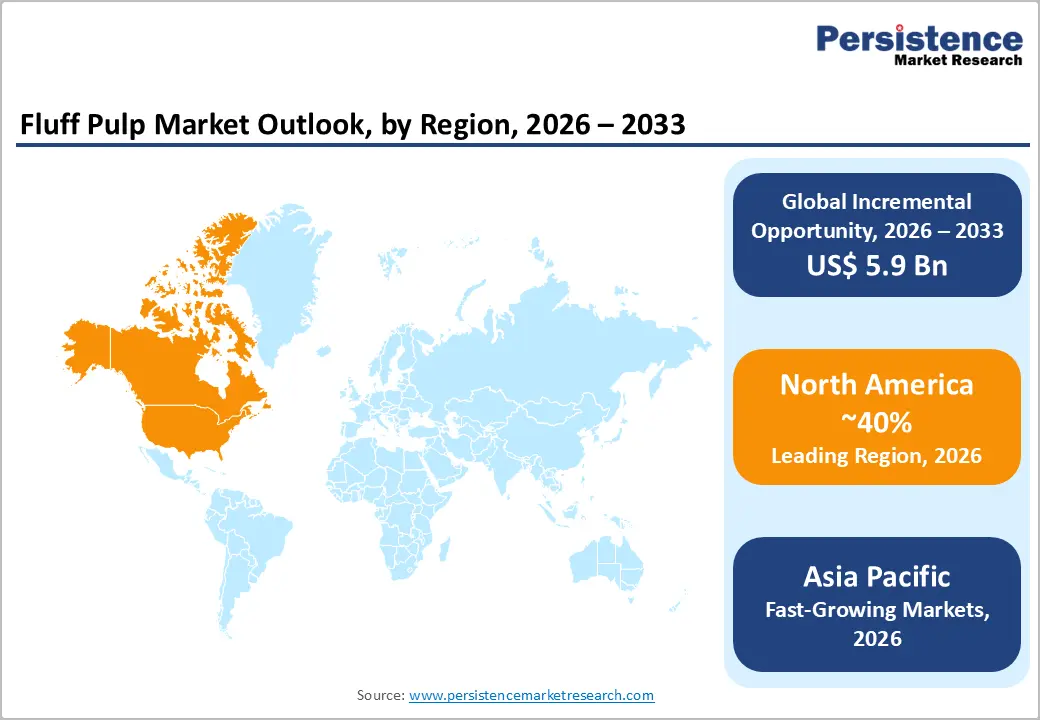

- Leading Region: North America, led by the U.S. South, dominates global fluff pulp production with the world's largest SBSK supply base holding 40% share. The American Forest & Paper Association (AF&PA) confirms the U.S. as the largest global fluff pulp exporter, with major producers International Paper, Georgia-Pacific, and Rayonier Advanced Materials supplying global hygiene brand customers.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market with a rising CAGR of 8.2%, driven by China's rapidly expanding hygiene products converting industry, India's GST-exempt sanitary napkin market expansion, and rising diaper adoption across Southeast Asia as the World Bank's projected 1 billion new middle-class consumers by 2030 enter the hygiene market.

- Dominant Segment: Southern Softwood Bleached Kraft (SBSK) leads the Product Type category with approximately 52% market share, driven by its superior long fiber length, wet tensile strength, and high-bulk absorbent core performance, which are critical for premium baby diaper and adult incontinence product applications globally.

- Fastest Growing Segment: Adult Incontinence Products represent the fastest-growing application segment, fueled by the WHO's projection that the population aged 60+ will double to 2 Billion by 2050, with incontinence affecting 420 million people globally, driving premium, high-fluff-content product demand in North America, Europe, and developed Asia Pacific markets.

- Key Opportunity: Expanding air-laid nonwoven applications, with INDA and EDANA confirming consistent above-average growth in wipes, medical pads, and industrial absorbents utilizing fluff pulp, offer producers a growing demand channel less exposed to thin-core diaper substitution, combined with rising feminine hygiene adoption in South Asia under PMBJP and UNFPA-supported programs

Market Dynamics

Drivers - Surging Global Demand for Disposable Baby Diapers in Emerging Economies

The rapid expansion of the middle class across Asia Pacific, Latin America, and Sub-Saharan Africa is driving a structural and sustained increase in baby diaper adoption rates, with fluff pulp serving as the primary absorbent core fiber. According to UNICEF, approximately 140 Million babies are born globally each year, and diaper penetration rates in emerging markets including India, Indonesia, Nigeria, and Bangladesh remain well below developed market levels, representing a vast addressable growth opportunity.

The World Bank projects the global middle class to expand by approximately 1 Billion people by 2030, primarily in Asia and Africa, directly correlating with increased per-capita hygiene product expenditure. Major global hygiene brands including Procter & Gamble and Kimberly-Clark are actively expanding manufacturing and distribution infrastructure in these high-growth regions, driving proportional increases in fluff pulp procurement from leading suppliers.

Aging Demographics and Rising Adult Incontinence Product Demand

The global demographic transition toward an older population is generating one of the most durable and fast-growing demand pools for fluff pulp in the adult incontinence product category. According to the World Health Organization (WHO), urinary incontinence affects an estimated 420 million people globally, with prevalence rates rising sharply among individuals aged 65 and above.

The population aged 60+ is projected to double to over 2 Billion by 2050, representing an unprecedented and structurally assured expansion in adult diaper and incontinence pad demand. Adult incontinence products typically have higher fluff pulp loading per unit than baby diapers, due to the greater fluid volumes they manage, amplifying the per-unit raw material demand in this fast-growing product category. Leading fluff pulp producers, including International Paper Company, Domtar Corporation, and Suzano S.A., are actively expanding capacity to address this growing market segment.

Restraints - Substitution Threat from Superabsorbent Polymer (SAP)-Rich Thin-Core Architectures

The progressive trend toward thin-core and coreless diaper architectures that substitute a significant proportion of fluff pulp content with superabsorbent polymer (SAP) to achieve thinner, lighter, and higher-capacity absorbent cores represent challenges to the market. According to the European Disposables and Nonwovens Association (EDANA), the average fluff pulp content per baby diaper has declined meaningfully over the past two decades as SAP concentrations have increased from approximately 15-20 grams per diaper to current levels, reducing per-unit fluff pulp demand even as overall diaper volumes grow. This substitution effect constrains volume growth of fluff pulp despite healthy overall hygiene product market expansion.

Deforestation Concerns and Sustainable Forestry Certification Compliance Costs

Growing consumer, regulatory, and investor scrutiny of deforestation risks associated with wood-based fiber sourcing is increasing compliance and certification costs for fluff pulp producers. The Forest Stewardship Council (FSC) and Program for the Endorsement of Forest Certification (PEFC) certification requirements, while increasingly demanded by hygiene brand manufacturers as supply chain sustainability prerequisites, impose ongoing audit, management, and operational costs on producers.

The European Commission's EU Deforestation Regulation (EUDR), which requires due diligence verification that products, including wood pulp, are not linked to deforestation, is adding regulatory compliance burdens for fluff pulp producers supplying the EU market, potentially disadvantaging producers operating in regions with less developed sustainable forestry infrastructure.

Opportunities - Expanding Air-Laid Nonwoven Applications Driving Incremental Fluff Pulp Demand

Air-laid nonwoven products, including wipes, table napkins, medical absorbent pads, and industrial absorbents, represent a rapidly growing application category for fluff pulp outside the conventional hygiene product sector, creating meaningful diversification of demand for market participants. Air-laid technology uses fluff pulp fibers as a primary structural component, typically in combination with binder fibers and superabsorbent polymers, to produce soft, absorbent nonwoven substrates.

According to the Association of the Nonwoven Fabrics Industry (INDA), the global air-laid nonwovens market has demonstrated consistent above-average growth rates, with hygiene and wipes applications driving the majority of incremental volume. According to the European Nonwoven Fabrics Association (EDANA), the global nonwovens industry consumed approximately 12 million tonnes of raw materials in 2023, with air-laid applications representing a growing share. This application breadth provides fluff pulp producers with opportunities for volume growth that are less exposed to the thin-core diaper substitution trend.

Rising Feminine Hygiene Product Adoption in South and Southeast Asia

The convergence of government menstrual health programs, rising female literacy and workforce participation, and e-commerce-enabled distribution infrastructure is driving accelerating adoption of feminine hygiene products in South Asia and Southeast Asia, creating a high-growth demand frontier for fluff pulp in sanitary napkin and pantyliner absorbent core applications.

According to UNICEF, approximately 500 million women and girls globally lack access to adequate menstrual hygiene facilities and products, with the majority concentrated in South Asia, Sub-Saharan Africa, and Southeast Asia. In India, the abolition of the GST on sanitary napkins in 2018 and the expansion of government distribution through Pradhan Mantri Bhartiya Janaushadhi Pariyojana (PMBJP) have materially increased sanitary napkin penetration rates. With the UN Population Fund (UNFPA) identifying menstrual health as a global development priority, multi-stakeholder programs are creating a durable and expanding demand pipeline for sanitary napkin components, including fluff pulp, through 2033.

Category-wise Analysis

Product Type Insights

Southern Softwood Bleached Kraft (SBSK) Fluff Pulp is the dominant product type segment, accounting for approximately 52% of total global fluff pulp consumption. SBSK pulp, produced primarily in the U.S. South from species including Southern Yellow Pine, offers the optimal combination of long fiber length, superior wet strength, and high absorbent capacity essential for premium diaper and incontinence product absorbent core performance.

According to the American Forest & Paper Association (AF&PA), the U.S. remains the world's largest fluff pulp producer, with southern softwood kraft mills operating at high utilization rates to serve global demand. SBSK's long fibers provide structural integrity to the absorbent core under wet load conditions, preventing gel blocking and maintaining loft, performance characteristics that premium hygiene brand manufacturers prioritize and that are difficult to replicate with shorter hardwood or northern softwood alternatives.

Fiber Source Insights

Softwood-Based fluff pulp dominates the Fiber Source segment, accounting for approximately 72% of total market volume. Softwood fibers, derived from coniferous species including pine, spruce, and fir, are characterized by long fiber length (2.5-4.5 mm) that imparts superior wet tensile strength, high bulk, and excellent fluid wicking properties to absorbent cores. These mechanical performance attributes are critical in baby diaper, adult incontinence pad, and feminine hygiene product applications where core integrity under saturated conditions directly determines product performance and consumer satisfaction.

According to the Food and Agriculture Organization (FAO), softwood accounts for the majority of global chemical wood pulp production capacity, with major producing regions including the U.S. South, Canada, Scandinavia, and Brazil (via eucalyptus blending programs) sustaining the supply base. Hardwood-based and blended fiber grades are gaining traction in cost-optimized and thin-core applications.

Application Insights

Baby diapers are the dominant application segment, accounting for approximately 42% of global fluff pulp consumption. The baby diaper category is the single largest driver of fluff pulp demand, with the absorbent core of a standard baby diaper containing 8-15 grams of fluff pulp depending on product tier and architecture.

According to UNICEF, approximately 140 Million babies are born annually worldwide, each requiring diaper components for an average of 2-3 years, creating a vast and continuously renewing demand base. While thin-core innovations are progressively reducing per-unit fluff pulp content in premium diaper segments in developed markets, volume growth in Africa, South Asia, and Southeast Asia, where diaper penetration rates remain low and conventional core architectures dominate, is generating substantial offsetting incremental demand, sustaining the baby diaper segment's dominant position through 2033.

End-user Insights

Personal care & hygiene is the dominant end-use segment, accounting for approximately 64% of total Fluff Pulp Market revenue. This segment encompasses the full range of consumer-facing absorbent hygiene products, baby diapers, adult incontinence products, sanitary napkins, pantyliners, and personal wipes, which collectively represent the primary and highest-volume consumption pool for fluff pulp across all geographies.

According to the Procter & Gamble Company, its global baby, feminine, and family care business, entirely dependent on fluff pulp as a critical raw material input, generates revenues exceeding US$20 billion annually, illustrating the enormous scale of the personal care end-use channel. The healthcare end-use segment, encompassing medical absorbents, wound care pads, and surgical drapes, is growing fastest within the end-use category, supported by expanding global healthcare infrastructure investment and a post-COVID-19 rise in healthcare spending.

Regional Insights

North America Fluff Pulp Market Trends & Analysis

North America dominates global fluff pulp production, led by the U.S. South, which serves as the core SBSK manufacturing hub. Strong integration of softwood kraft mills, plantation forestry, and export-oriented supply chains supports large-scale output. The region benefits from certified fiber sourcing (FSC, SFI), robust hygiene demand, and established trade networks supplying Europe and Asia Pacific markets. Canada complements supply with high-quality NBSK grades for premium absorbent applications.

- U.S. Fluff Pulp Market Size

The U.S. is the world’s largest fluff pulp producer and exporter, accounting for an estimated ~25.3% of global supply capacity. The market is driven by strong SBSK production in the Southern states and high demand from hygiene product manufacturers. Large integrated producers supply both domestic diaper and adult incontinence segments and export significant volumes to Asia and Europe, reinforcing its global leadership position.

- Europe Fluff Pulp Market Trends, Drivers & Insights

Europe is primarily a net importer of fluff pulp, relying heavily on North American SBSK and Scandinavian NBSK supply. Demand is driven by a mature hygiene products industry, particularly in Germany, Italy, and the Nordics. Regulatory frameworks such as the EU Deforestation Regulation (EUDR) are reshaping procurement toward traceable, certified fiber. Strong converting infrastructure supports steady consumption across baby diapers, adult incontinence, and air-laid nonwovens.

- Germany Fluff Pulp Market Size

Germany is Europe’s largest fluff pulp consumer, accounting for an estimated ~20.5% of regional demand. The market is driven by a highly advanced hygiene manufacturing sector and strong export-oriented production. Germany relies heavily on imported fluff pulp, especially SBSK grades, to support diaper and incontinence product manufacturing. Sustainability compliance and circular economy goals are increasingly influencing sourcing strategies across the German market.

- U.K. Fluff Pulp Market Size

The U.K. represents a moderate but stable demand center, accounting for roughly ~10.2% of European fluff pulp consumption. Demand is driven by healthcare-related hygiene products and retail diaper consumption. The market is import-dependent, sourcing primarily from North America and Scandinavia. Growth is supported by rising adult incontinence demand and increasing focus on sustainable, certified pulp-based hygiene materials in consumer products.

- France Fluff Pulp Market Size

France contributes an estimated ~8.1% of Europe’s fluff pulp demand, supported by a strong personal care and hygiene manufacturing base. Domestic consumption is driven by baby diaper and feminine hygiene product production. The country relies heavily on imports, particularly SBSK pulp from the U.S. and NBSK from Finland/Sweden. Sustainability regulations and consumer preference for eco-friendly hygiene products are shaping procurement decisions.

- Asia Pacific Fluff Pulp Market Size & Share

Asia Pacific is the fastest-growing global fluff pulp market, led by rising hygiene penetration in China, India, and Southeast Asia. Expanding populations, urbanization, and increasing disposable incomes are accelerating demand for diapers and adult incontinence products. The region relies heavily on imports from North America and South America, although Japan and China maintain limited domestic production of specialty grades. Growth is strongly supported by e-commerce and retail expansion.

- China Fluff Pulp Market Size

China is the largest fluff pulp consumer in Asia, accounting for an estimated ~35.4% of regional demand. Rapid expansion of baby diaper and adult incontinence markets drives strong import dependency, primarily from the U.S. and Scandinavia. Domestic producers supply limited volumes, focusing on specialty grades. Rising health awareness and aging population trends are key long-term growth drivers for fluff pulp consumption.

- India Fluff Pulp Market Size

India is an emerging high-growth market, currently representing ~10.2% of the Asia Pacific demand. Growth is fueled by increasing diaper adoption, rising hygiene awareness, and government-led sanitation initiatives. The market is highly import-reliant, sourcing SBSK pulp from North and South America. Expanding middle-class population and retail penetration are expected to significantly accelerate demand over the next decade.

- Japan Fluff Pulp Market Size

Japan accounts for an estimated ~8.1% of Asia Pacific fluff pulp demand. The market is mature and characterized by high per-capita consumption of adult incontinence products driven by an aging population. Domestic producers focus on high-quality specialty fluff pulp grades, while imports supplement supply needs. Demand growth is steady rather than rapid, driven primarily by elderly care and premium hygiene product segments.

Competitive Landscape

The global Fluff Pulp Market is moderately consolidated, with a small number of large-scale producers controlling the majority of global supply. International Paper Company, Domtar Corporation (now part of Paper Excellence), Georgia-Pacific LLC, Rayonier Advanced Materials Inc., and Mercer International Inc. dominate North American SBSK production. Stora Enso Oyj, UPM-Kymmene Corporation, and Sappi Limited are leading European and global suppliers.

Suzano S.A. and Arauco are key southern hemisphere producers growing in global share. Key competitive differentiators include FSC/SFI certification, fiber length and purity specifications, Just-in-Time delivery capabilities, and long-term supply contracts with major hygiene brands. Emerging business model trends include bio-circular production investments and specialty fluff pulp development for ultra-thin core architectures.

Key Market Developments

- April 2025: Suzano S.A. announced expansion of its fluff pulp production capacity at its Cerrado facility in Brazil, targeting growing demand from Asian and European hygiene product manufacturers for eucalyptus-based hardwood and blended fluff pulp grades supporting thin-core diaper architectures.

- January 2024: Rayonier Advanced Materials Inc. completed a performance upgrade at its Jesup, Georgia fluff pulp mill, enhancing SBSK fiber quality and production efficiency to strengthen its competitive position serving premium hygiene brand customers in North America and Asia Pacific.

- October 2023: Stora Enso Oyj announced a strategic review of its pulp production assets, including evaluation of capacity optimization for specialty fluff pulp grades, as part of a broader portfolio realignment targeting high-value fiber applications in hygiene and medical absorbent markets globally.

Fluff Pulp Market- Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 7.4 Bn |

| Current Market Value (2026) | US$ 10.2 Bn |

| Projected Market Value (2033) | US$ 16.1 Bn |

| CAGR (2026 - 2033) | 6.7% |

| Leading Region | North America, 40% share |

| Dominant Product Type | Southern Softwood Fluff Pulp (SBSK), 52% share |

| Top-ranking Fiber Source | Softwood-Based, 72% |

| Incremental Opportunity | US$ 5.9 Bn |

Companies Covered in Fluff Pulp Market

- International Paper Company

- Domtar Corporation

- Suzano S.A.

- Stora Enso Oyj

- UPM-Kymmene Corporation

- WestRock Company

- Georgia-Pacific LLC

- Sappi Limited

- Nippon Paper Industries Co., Ltd.

- Resolute Forest Products Inc.

- Mondi Group

- Rayonier Advanced Materials Inc.

- Oji Holdings Corporation

- Arauco

- Mercer International Inc.

- Paper Excellence Group

- Canfor Corporation

- Clearwater Paper Corporation

Frequently Asked Questions

The global Fluff Pulp Market is projected to reach US$ 16.1 Billion by 2033, growing at a CAGR of 6.7% during the forecast period 2026 - 2033, from an estimated US$ 10.2 Billion in 2026. The market recorded a historical CAGR of 5.6% between 2020 and 2025, driven by global population growth toward the UN's projected 9.7 Billion by 2050 and the WHO's documented ageing demographic trend amplifying adult incontinence product demand.

The primary drivers are global population growth, with approximately 140 Million babies born annually per UNICEF sustaining baby diaper demand, and the ageing demographic transition, with the WHO projecting the global population aged 60+ to double to 2 Billion by 2050 while urinary incontinence affects 420 Million people today, driving adult incontinence product demand and fluff pulp consumption in high-load absorbent core applications.

Southern Softwood Bleached Kraft (SBSK) leads the Product Type segment with approximately 52% market share. Its dominance reflects superior long fiber characteristics, exceptional wet tensile strength, and high-bulk absorbent core performance demanded by premium hygiene brand manufacturers. The American Forest & Paper Association (AF&PA) confirms the U.S. South as the world's largest producing region for SBSK, with major producers including International Paper, Georgia-Pacific, and Rayonier Advanced Materials supplying global markets.

North America, led by the United States, is the dominant fluff pulp producing and exporting region globally. The U.S. South hosts the world's largest concentration of SBSK fluff pulp mills, with the AF&PA confirming U.S. status as the largest global fluff pulp exporter. Major producers including International Paper Company, Georgia-Pacific LLC, and Rayonier Advanced Materials Inc. supply hygiene brand customers in Europe, Asia Pacific, and Latin America.

The fastest-growing opportunity lies in rising feminine hygiene adoption in South Asia and Southeast Asia, supported by India's GST exemption on sanitary napkins, PMBJP distribution programs, and UNFPA-backed menstrual health initiatives targeting the 500 Million women globally lacking adequate hygiene access per UNICEF. Combined with growing air-laid nonwoven applications confirmed by INDA and EDANA, these channels provide fluff pulp producers diversified demand growth less sensitive to thin-core diaper substitution trends.

Key market participants include International Paper Company, Domtar Corporation, Suzano S.A., Stora Enso Oyj, UPM-Kymmene Corporation, WestRock Company, Georgia-Pacific LLC, Sappi Limited, Nippon Paper Industries Co., Ltd., Resolute Forest Products Inc., Mondi Group, Rayonier Advanced Materials Inc., Oji Holdings Corporation, Arauco, and Mercer International Inc., alongside growing producers Paper Excellence Group and Canfor Corporation.