- Bulk Chemicals

- Ready-mix Concrete Market

Ready-mix Concrete Market Size, Share, and Growth Forecast 2026 - 2033

Ready-mix Concrete Market by Product Type (Transit Mixed Concrete, Shrink Mixed Concrete, Central Mixed Concrete), Application (Commercial, Residential, Infrastructure, Industrial), and Regional Analysis, 2026 - 2033

Ready-mix Concrete Market Size and Trend Analysis

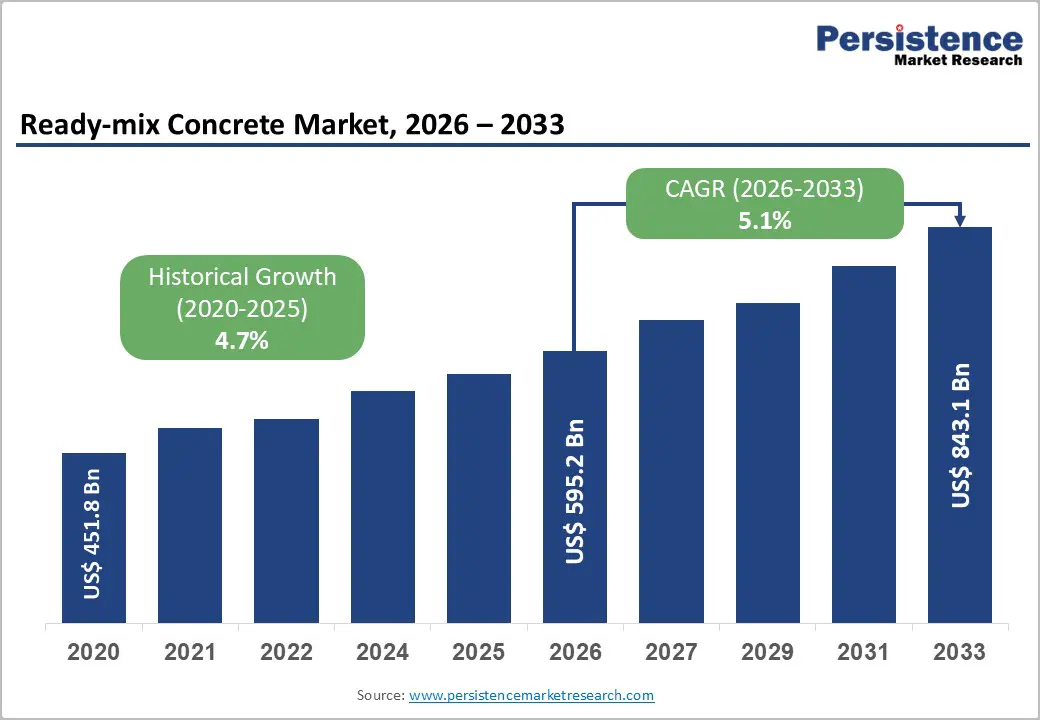

The global Ready-mix Concrete market size is expected to be valued at US$595.2 billion in 2026 and projected to reach US$843.1 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033. Rise in public infrastructure spending, urban housing construction, and industrial development across Asia Pacific, the Middle East, and the Americas, collectively generating structural, non-cyclical demand for pre-batched concrete.

Governments worldwide are investing in capital expenditure at historic levels: India increased infrastructure capex by 11.1% to US$ 133 billion in FY 2024–25; the U.S. construction sector recorded US$ 2.2 trillion in total spending in 2024; and Gulf nations are executing giga-projects aligned with economic diversification strategies. These concurrent demand drivers, reinforced by the shift from on-site concrete mixing to centralized quality-controlled ready-mix production, underpin the market's compound growth trajectory through 2033.

Key Industry Highlights:

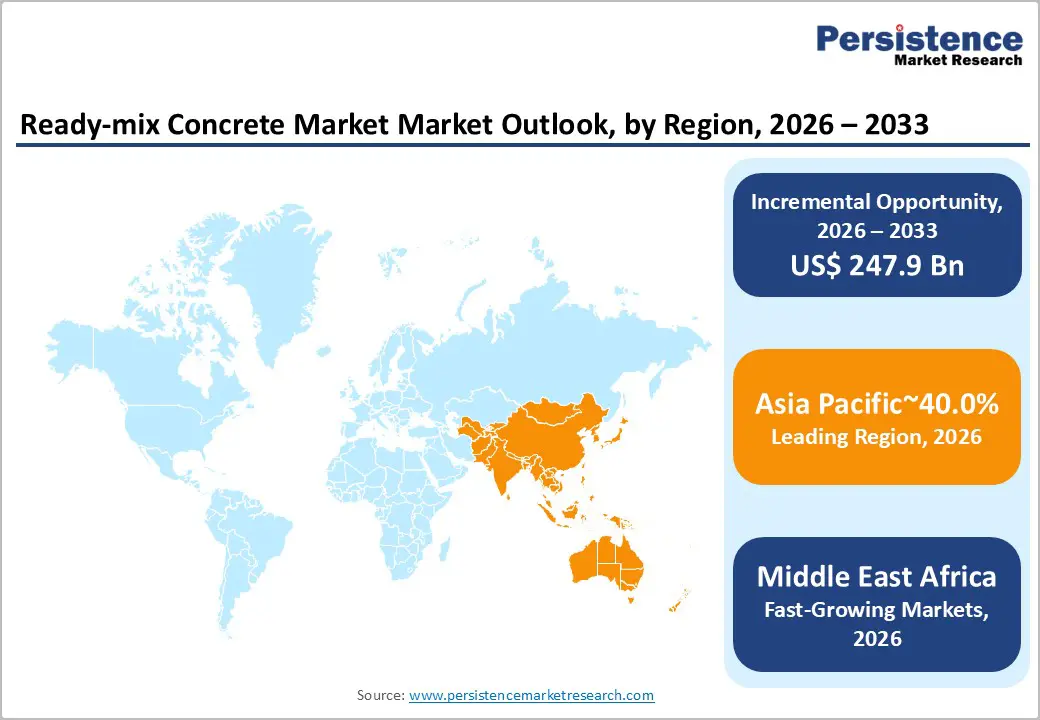

- Leading Region: Asia Pacific dominates the global Ready-mix Concrete market with approximately 40% revenue share in 2025, anchored by China's US$ 117.8 Bn market and India's fast-expanding construction economy driven by US$ 133 billion government capex and a US$ 5.8 trillion real estate projection by 2047.

- Fast-Growing Market: Middle East & Africa is the fastest-growing region through 2033, propelled by GCC giga-projects NEOM, Red Sea Project, Qiddiya, collectively representing over US$ 1 trillion in active construction, with the IMF projecting 4.2% GDP growth for the Middle East in 2025, sustaining construction investment momentum.

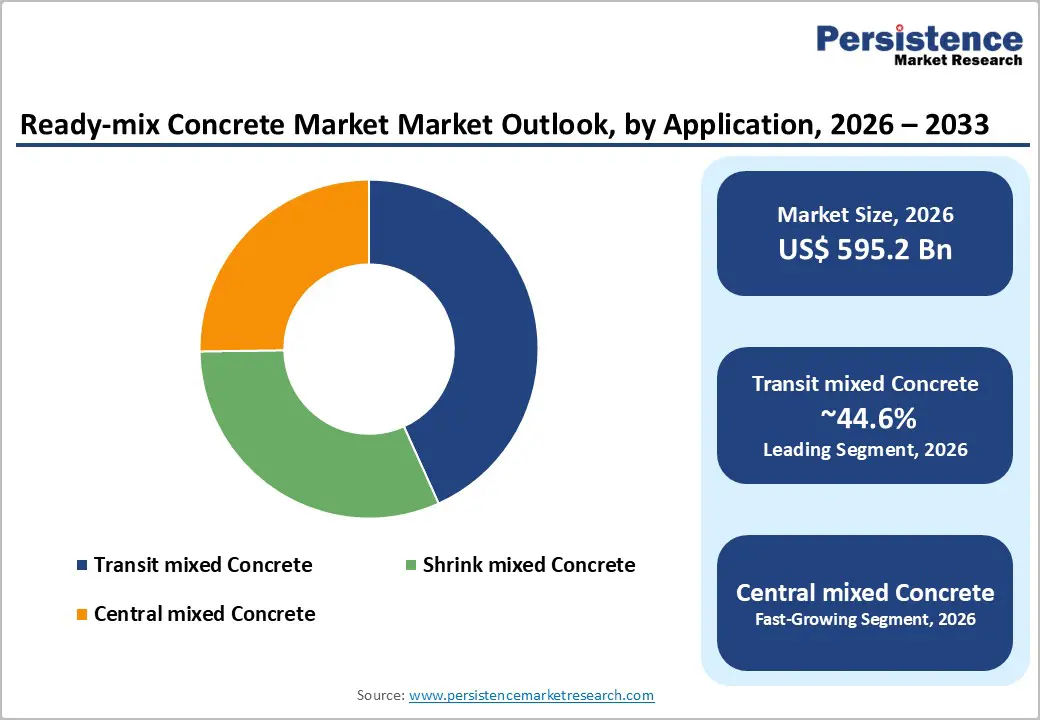

- Leading Concrete Type: Transit mixed concrete leads with approximately 45% share in 2025, reflecting its operational flexibility, extended workability window, and dominance across the broadest range of residential, commercial, and infrastructure construction applications globally.

- Fast-growing Concrete Type: Central mixed concrete is the fastest-growing product type, with a positive CAGR, driven by quality specification mandates in infrastructure contracts, AI-admixture innovations like Lyten's S Cure™ delivering 110% early-strength gains, and growing EPD compliance requirements in public procurement.

- Opportunity: AI-driven operational efficiency platforms exemplified by Master Builders Solutions' MasterAtlas R3 and Lyten's 3D Graphene™ admixture, enabling producers to simultaneously reduce returned concrete waste, lower embodied carbon, and meet LEED and EPD compliance requirements that are becoming standard in public infrastructure tenders.

DRO Analysis

Drivers - Government Infrastructure Capital Expenditure Programs Generating Non-Discretionary Concrete Demand

Large-scale government infrastructure investment programs across major economies are creating durable, policy-mandated demand for ready-mix concrete across highway, bridge, rail, port, and urban transit applications. In the United States, the Infrastructure Investment and Jobs Act (IIJA) committed US$ 1.2 trillion over five years, with US$ 550 billion in new spending specifically directed toward road networks, bridges, and transit systems, which represent the single largest domestic channel for concrete consumption.

India's National Infrastructure Pipeline (NIP) targeting US$ 1.4 trillion in project execution by 2025 and the government's 3.4% of GDP capital expenditure commitment in FY 2024–25 collectively generate concrete procurement across thousands of simultaneous construction sites. Similarly, Gulf Cooperation Council (GCC) nations are executing over US$1 trillion in active construction projects, anchored by NEOM, the Red Sea Project, and Qiddiya in Saudi Arabia, with concrete as the foundational material across all project categories.

Urbanization and Housing Deficits Compelling Structured Residential Construction at Scale

Accelerating urbanization across Asia Pacific, Africa, and Latin America, combined with formal housing program mandates in developed economies, is generating a structurally persistent demand pool for ready-mix concrete in residential construction. The United Nations estimates that 68% of the global population will reside in urban areas by 2050, requiring an estimated 2 billion new urban dwellings globally.

In India, the Pradhan Mantri Awas Yojana-Urban (PMAY-U) program has sanctioned 1.18 crore houses with 86.6 lakh already completed, while India's real estate sector is projected to reach US$ 5.8 trillion by 2047, contributing 15.5% of GDP. In the United States, 1.6 million new homes were constructed in 2024, sustaining residential concrete demand. Ready-mix concrete's advantages over site-mixed alternatives in residential construction, including consistent quality, structural compliance, and faster pour cycles, are compelling adoption across formal housing programs globally.

Restraints - Raw Material Cost Volatility and Supply Chain Disruptions Compressing Producer Margins

Ready-mix concrete production is highly sensitive to the cost and availability of cement, aggregates, and water, three input categories subject to logistics bottlenecks, regional scarcity, and energy-intensive production economics. Cement manufacturing, which accounts for approximately 8% of global CO2 emissions, according to the International Energy Agency (IEA), is subject to rising carbon prices under the EU Emissions Trading System (ETS) and equivalent frameworks, thereby inflating input costs.

Aggregate supply constraints in urbanized markets create local shortages, while fuel cost volatility, which directly impacts ready-mix truck operating economics, compresses margins for producers operating on fixed-price contracts. These input cost dynamics constrain profitability, particularly for independent and regional ready-mix operators.

Environmental Regulations Restricting Traditional Concrete Production and Formulations

Tightening environmental regulations governing concrete production, delivery operations, and washout water management are creating compliance costs that disproportionately burden smaller market participants. The European Union's construction sector experienced a 0.9% decline in annual average output in 2024 (per Eurostat), partly attributable to regulatory cost inflation related to materials compliance.

Regulations mandating minimum recycled concrete aggregate content, restricting CO2 emissions from cement, and requiring washout water recycling at batch plants are compelling capital investment in equipment upgrades. Restrictions on nighttime concrete delivery in dense urban areas limit operational productivity and increase unit delivery costs, constraining revenue per vehicle in high-density markets.

Opportunities - Central Mixed Concrete Adoption in Quality-Critical Infrastructure and Smart Construction Projects

The Central Mixed Concrete segment, the fastest-growing product type at a projected CAGR of 5% through 2033, presents a significant opportunity for ready-mix producers investing in centralized wet-batch plant infrastructure and advanced quality control systems. Central mixing delivers superior concrete uniformity, precision water-to-cement ratio control, and documented compliance with structural specifications characteristics increasingly mandated by government procurement standards for critical infrastructure, including bridges, nuclear facilities, data centers, and high-rise foundations.

Lyten's launch of S Cure™ in January 2026, a concrete admixture powered by 3D Graphene™ nanomaterials that delivers an over 110% increase in early compressive strength, exemplifies the performance-enhancement technology being commercialized for central-mixed applications. The U.S. IIJA's bridge rehabilitation program and India's NIP expressway network both specify quality-controlled concrete formulations that centralized wet-batch production optimally delivers, positioning this segment for above-market growth among technically capable producers.

AI-Driven Operational Efficiency and Waste Reduction Platforms for Ready-Mix Producers

The integration of artificial intelligence and real-time sensor technology into ready-mix concrete production and delivery operations represents a transformational opportunity for producers to simultaneously reduce waste, lower costs, and meet sustainability commitments. Master Builders Solutions launched the MasterAtlas R3 Returned Concrete Program in January 2026, an AI-driven and admixture-integrated solution enabling ready-mix producers to reuse returned concrete through real-time monitoring and optimized dosing, reducing waste and carbon footprint while improving operational efficiency.

This technology directly addresses one of the industry's most persistent cost and sustainability challenges: returned concrete, which accounts for an estimated 2%–5% of all ready-mix volume globally, represents millions of tonnes of material waste annually. Producers offering verified sustainability credentials, including documented embodied-carbon reductions, recycled-content certification, and digital delivery tracking, are increasingly advantaged in public procurement tenders that require Environmental Product Declarations (EPDs) and LEED-compliant material sourcing.

Category-wise Analysis

Product Type Insights

The transit mixed concrete segment dominates and accounted for ~45% of the share in 2025. Transit mixing, where dry or partially hydrated materials are loaded into truck-mounted drum mixers and fully mixed en route to the job site, has established itself as the default delivery method across the broadest range of construction applications due to its flexibility, extended workability window, and adaptability to variable site conditions. This format allows concrete to be loaded at the central plant and mixed during transport, giving contractors the ability to manage slump and hydration timing in response to site conditions and weather, a critical operational advantage in large-scale residential and commercial projects.

The U.S. construction sector's US$ 2.2 trillion annual spending base is predominantly served by transit mix operations, reinforcing North America's leadership in the segment. However, Central Mixed Concrete is the fastest-growing product type, driven by upgrades to quality specifications in infrastructure contracts.

Application Insights

The infrastructure application segment leads the global ready-mix concrete market, accounting for approximately 38% of total market share in 2025. Infrastructure's dominance reflects the material intensity of road, bridge, tunnel, dam, port, and rail construction project categories, in which ready-mix concrete is the sole structural material choice and procurement volumes per project are orders of magnitude larger than those for residential or commercial projects.

National infrastructure investment programs across every major economy are generating simultaneous demand: the U.S. IIJA, India's NIP, China's continued Belt and Road Initiative (BRI) project execution, and GCC giga-projects collectively represent tens of trillions of dollars in infrastructure capital allocation with concrete as the foundational input material. The Residential application segment is the fastest growing, driven by PMAY-U in India, China's social housing programs, and record U.S. housing starts of 1.6 million units in 2024.

Regional Insights

North America Ready-mix Concrete Market Trends and Insights

North America holds approximately 18% of the global Ready-mix Concrete market revenue in 2025, driven by the U.S. IIJA's unprecedented infrastructure spending mandate, record residential construction activity, and the operational maturity of the region's ready-mix delivery infrastructure. The region is characterized by a concentration of vertically integrated aggregates and concrete producers, including Martin Marietta, Vulcan Materials, CEMEX USA, and Breedon Group, executing strategic acquisitions to secure aggregate supply chains critical for sustained ready-mix production capacity.

U.S. Ready-mix Concrete Market Size

The U.S. Ready-mix Concrete market is valued at approximately US$ 101.9 billion in 2025, underpinned by US$ 2.2 trillion in total construction spending, 4.5% of GDP, and a housing market that delivered 1.6 million new homes in 2024. The IIJA's US$ 110 billion road and bridge allocation and US$ 66 billion rail investment are generating multi-year concrete procurement programs that provide revenue visibility for large domestic producers. Martin Marietta's US$2.05 billion acquisition of 20 active aggregate operations in the U.S. Southeast in February 2024 exemplifies the strategic capital deployment underway to secure supply chains that support this demand trajectory.

Europe Ready-mix Concrete Market Trends and Insights

Europe holds approximately 20% of the global ready-mix concrete market revenue in 2025, shaped by divergent national trajectories: Spain, Czechia, and Slovakia recorded double-digit construction output growth in 2024, while Romania, Poland, and Austria contracted sharply (per Eurostat).

The region's transition toward low-carbon concrete formulations, driven by EU ETS carbon pricing and the European Green Deal's embodied carbon reduction targets, is simultaneously compelling product innovation and creating compliance cost pressures for traditional Portland cement-based ready-mix producers.

Germany Ready-mix Concrete Market Size

Germany's Ready-mix Concrete market is valued at approximately US$ 23.8 billion in 2025, reflecting the country's position as Europe's largest construction economy despite a 9% contraction in annual construction output in 2024 (per Eurostat). Germany's Wohnraumoffensive social housing program and sustained public infrastructure investment in road, rail, and energy transition infrastructure maintain structural concrete demand. Heidelberg Materials' domestic production network and CEMEX operations represent the primary large-scale ready-mix supply infrastructure, while the push for recycled aggregate concrete under EU PPWR is reshaping material specifications.

U.K. Ready-mix Concrete Market Size

The U.K. Ready-mix Concrete market is valued at approximately US$13.6 billion in 2025, sustained by the government's National Infrastructure Strategy and the continued execution of major projects including HS2, Hinkley Point C, and the Lower Thames Crossing. Tarmac (CRH Group)'s launch of its ultra-low carbon cement MevoCem pilot in July 2025 signals the UK market's transition toward low-embodied-carbon ready-mix formulations, while the new rail-fed aggregates depot in Rugby reflects investment in supply chain resilience for concrete producers.

Asia Pacific Ready-mix Concrete Market Drivers and Analysis

Asia Pacific dominates the global Ready-mix Concrete market with approximately 40.0% revenue share in 2025, anchored by China's unparalleled construction volume and complemented by rapidly expanding demand from India, Southeast Asia, and Australia.

China remains the world's largest single concrete consumer by volume producing over 2.5 billion tonnes of cement annually (per the China Cement Association) though its construction cycle is transitioning from peak residential volume toward infrastructure and industrial applications. India is the fastest-growing major market in the region, with government capital expenditure growing by 11.1% to US$133 billion in FY 2024–25.

China Ready-mix Concrete Market Size

China's Ready-mix Concrete market is valued at approximately US$117.8 billion in 2025, reflecting the country's position as the world's largest construction economy by volume despite a structural transition away from speculative residential development toward government-directed infrastructure, industrial parks, and social housing programs under the 14th Five-Year Plan.

China's Belt and Road Initiative continues to drive concrete demand for overseas infrastructure projects, while domestic expressway expansion, high-speed rail network extensions, and urban metro systems sustain high-volume transit and central-mix concrete procurement across state-owned construction enterprises.

India Ready-mix Concrete Market Size

India's Ready-mix Concrete market is valued at approximately US$47.6 billion in 2025 and is among the fastest-growing country-level markets globally, driven by the government's US$ 133 billion infrastructure capital expenditure in FY 2024–25, the PMAY-U housing program, and India's real estate sector projected at US$ 5.8 trillion by 2047. India's warehousing market, projected to require 159 million sq. ft. by 2047 at a 4% CAGR, represents an emerging concrete demand vertical, while the National Logistics Policy and dedicated freight corridors are generating large-scale industrial park construction requiring ready-mix at scale.

Competitive Landscape

The global ready-mix concrete market exhibits a moderately consolidated structure at the tier-1 level, with multinational construction materials groups including Holcim Group, Heidelberg Materials, CEMEX, CRH plc, Martin Marietta Materials, and Vulcan Materials commanding significant combined revenue share through vertically integrated aggregates-to-concrete operations. However, the market remains substantially fragmented at regional and local levels, where thousands of independent batch plant operators serve geographically defined delivery radii.

Strategic differentiation among market leaders centers on aggregate reserve security, low-carbon concrete formulations, AI-powered operational platforms, and vertical integration spanning quarrying through delivery. The most impactful recent strategic trend is accelerated M&A activity targeting aggregate supply chain consolidation, as demonstrated by Martin Marietta, Heidelberg Materials, Breedon Group, and Rogers Group, reflecting the structural link between reserve ownership and ready-mix competitive positioning.

Key Developments:

- In January 2026, Lyten announced expansion into the global concrete market with the launch of S Cure™, a high-performance concrete admixture powered by nanomaterials, including 3D Graphene™, delivering over 110% increase in early compressive strength, improved long-term durability, and faster construction timelines, while being compatible with ready-mix concrete production without requiring changes to existing processes.

- In February, 2025, Nuvoco Vistas Corp. Ltd. launched its second ready-mix concrete (RMX) plant in Nagpur with a production capacity of 90 Cum/hour, enhancing regional supply capabilities and supporting growing demand across industrial, commercial, and residential construction projects with a wide range of value-added concrete solutions.

Global Ready-mix Concrete Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 451.8 Billion |

|

Current Market Value (2026) |

US$ 595.2 Billion |

|

Projected Market Value (2033) |

US$ 843.1 Billion |

|

CAGR (2026–2033) |

5.1% |

|

Leading Region |

Asia Pacific, ~40% market share (2025) |

|

Dominant Product Type |

Transit Mixed Concrete, ~45% market share (2025) |

|

Leading Application |

Infrastructure, ~38% market share (2025) |

|

Incremental Opportunity (2026–2033) |

~US$ 247.9 Billion |

Companies Covered in Ready-mix Concrete Market

- Holcim Group

- Heidelberg Materials AG

- CEMEX S.A.B. de C.V.

- CRH plc / Tarmac

- Martin Marietta Materials Inc.

- Vulcan Materials Company

- Breedon Group plc

- Rogers Group Inc.

- Summit Materials

- Taiheiyo Cement / CalPortland

- LSR Group

- Master Builders Solutions

- Siam Cement Group

- UltraTech Cement Ltd.

- ACC Limited

- China Resources Cement Holdings

Frequently Asked Questions

The global Ready-mix Concrete market is valued at US$595.2 billion in 2026, driven by infrastructure investment programs, urbanisation, and residential construction demand across Asia Pacific, North America, and the Middle East.

The two primary drivers are government infrastructure capital expenditure programs, including the U.S. IIJA committing US$ 1.2 trillion over five years, India's NIP targeting US$ 1.4 trillion, and GCC giga-projects exceeding US$ 1 trillion in active construction and structural urbanisation-driven housing demand, with the UN estimating 68% of the global population will be urban by 2050, requiring approximately 2 billion new urban dwellings and associated concrete infrastructure.

Asia Pacific leads with approximately 40% revenue share in 2025, anchored by China's US$117.8 billion market, and India's US$47.6 billion fast-growing market sustained by US$ 133 billion in government infrastructure capex in FY 2024–25 and a real estate sector projected at US$ 5.8 trillion by 2047.

The convergence of AI-driven operational efficiency platforms and sustainable concrete formulations represents the most significant commercial opportunity. Master Builders Solutions' MasterAtlas R3 and Lyten's S Cure™ 3D Graphene admixture, both launched in January 2026, exemplify the technology investment frontier enabling producers to reduce returned concrete waste, lower embodied carbon, and meet mandatory EPD and LEED compliance requirements increasingly required in public infrastructure tenders across North America, Europe, and the Middle East.

The market is led by Holcim Group, Heidelberg Materials AG, CEMEX, CRH plc/Tarmac, Martin Marietta Materials, and Vulcan Materials, which collectively dominate through vertically integrated aggregates-to-concrete operations, large reserve holdings, and expansive geographic presence. Recent strategic consolidation, including Martin Marietta's US$ 2.05 billion Southeast aggregates acquisition, Breedon Group's acquisition of BMC Enterprises and Lionmark, and the Summit Materials-Quikrete US$ 11.5 billion merger is reshaping the competitive hierarchy across North American and European markets.