- Bulk Chemicals

- 1-Butene Market

1-Butene Market Size, Share, and Growth Forecast, 2026 - 2033

1-Butene Market by Grade (Polymer-grade 1-butene, Chemical-grade 1-butene), Application (Polyethylene, Others), End-user (Plastics, Chemicals, Pharmaceuticals, Packaging, Automotive Construction, Consumer goods, Electronics), and Regional Analysis for 2026 - 2033

1-Butene Market Share and Trends Analysis

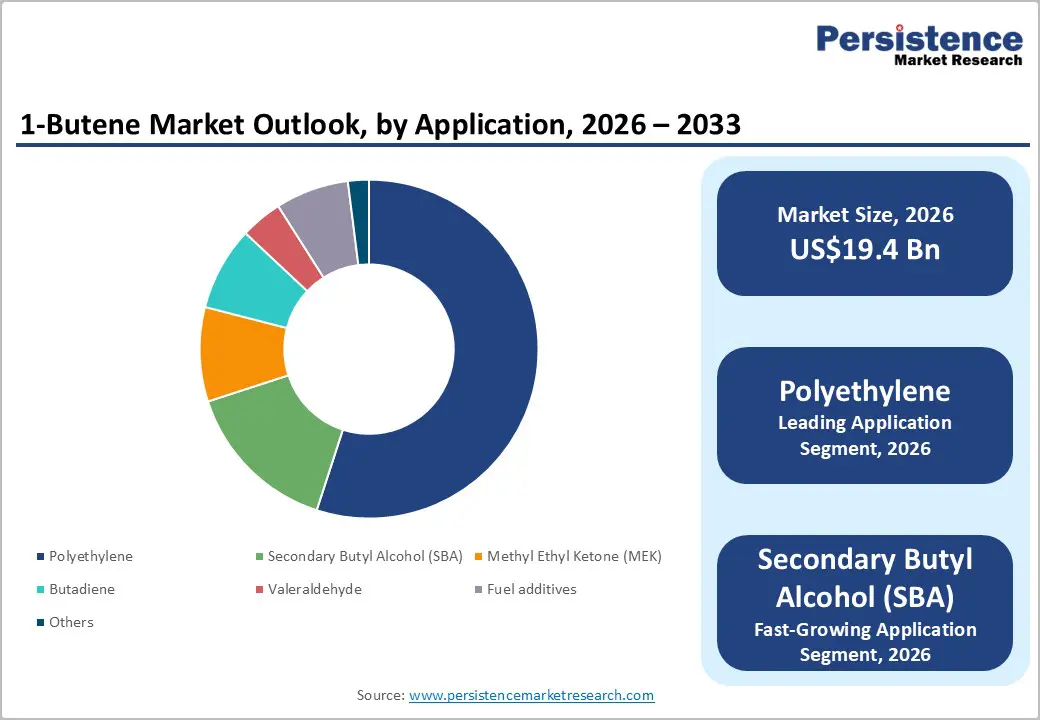

The global 1-butene market size is likely to be valued at US$19.4 billion in 2026 and is expected to reach US$28.2 billion by 2033, growing at a CAGR of 5.5% during the forecast period from 2026 to 2033, driven by increasing urbanization and population growth, which are driving demand for flexible packaging and durable consumer products, thereby boosting the consumption of polyethylene comonomers.

In addition, stringent vehicle emission regulations are encouraging the use of lightweight materials, where 1-butene-based polymers contribute to improved strength-to-weight performance. Advancements in catalytic dimerization technologies are also enhancing production efficiency and enabling manufacturers to achieve higher-purity 1-butene compared to conventional refinery extraction methods.

Key Industry Highlights:

- Leading Grade: Polymer-grade 1-butene is set to hold around 82% revenue share in 2026, driven by its indispensable role as a comonomer in the production of high-strength polyethylene.

- Fastest-Growing Grade: Chemical-grade 1-butene is projected as the fastest-growing segment, supported by the rising demand for specialized industrial solvents and fuel additives.

- Leading Application: Polyethylene is estimated to hold roughly 55% revenue share in 2026, due to its massive consumption in the global flexible packaging and consumer goods industries.

- Fastest-Growing Application: Secondary butyl alcohol (SBA) is forecast to record the fastest growth, driven by its increasing use as an intermediate in pharmaceuticals and cosmetics.

- Regional Leadership: Asia Pacific is projected to lead the market and register the fastest growth through 2033.

- Competitive Environment: The market reflects a moderately consolidated structure, with key players such as Sinopec and Exxon Mobil leveraging integrated supply chains and production scale.

- Innovation Trends: The development of bio-based production routes and the implementation of digital process optimization are shaping long-term market sustainability and efficiency.

DRO Analysis

Driver - Expansion of Polyethylene Production Capacity

Global polymer demand continues to increase due to packaging, construction, and automotive applications. According to the U.S. Energy Information Administration (EIA), U.S. refinery utilization exceeded 90.3% in 2024, indicating strong downstream demand. This expansion directly increases the consumption of co-monomers such as 1-butene in linear low-density polyethylene manufacturing processes.

Industrial producers invest in integrated cracker units to improve feedstock utilization efficiency. Increased adoption of flexible packaging materials in urban retail systems drives demand for polyethylene derivatives. Infrastructure projects require durable plastic materials for piping and insulation. This cause-and-effect relationship between polymer demand and co-monomer consumption sustains consistent growth momentum.

Restraint - Feedstock Price Volatility and Margin Pressure

Crude oil price fluctuations directly influence olefin production costs, creating uncertainty in profit margins. Variability in naphtha and natural gas liquids pricing affects production economics. Manufacturers face challenges in maintaining stable pricing strategies, which impacts long-term contract structures and investment planning.

Supply disruptions in upstream hydrocarbon markets constrain production scalability. Sudden cost increases reduce competitiveness against alternative co-monomers. Margin compression limits capital allocation for expansion projects. These constraints create structural challenges for consistent supply growth and profitability.

Opportunity - Adoption of Advanced Catalyst Technologies

Development of high-performance catalysts improves selectivity and yield in olefin production. Companies investing in next-generation catalytic systems achieve higher efficiency and reduced waste generation. This technological shift enables cost-effective production while aligning with environmental compliance standards.

Strategic partnerships between chemical producers and technology providers accelerate innovation adoption. Enhanced catalyst performance reduces energy consumption and operational costs. This pathway supports long-term profitability and sustainability objectives while expanding production capabilities.

Category-wise Analysis

Grade Insights

Polymer-grade 1-butene is anticipated to secure around 82% of the 1-butene market share in 2026, reflecting the massive demand from global polyethylene manufacturers. The production of medical-grade surgical gowns utilizes high-purity resins derived from this grade to ensure barrier protection. High purity levels are essential to prevent catalyst poisoning during the polymerization process.

Chemical-grade 1-butene is expected to be the fastest-growing segment, propelled by increasing utilization in the production of specialized solvents and additives. Manufacturers use this grade to synthesize methyl ethyl ketone for industrial-grade paint thinners. Rising industrial activity in emerging markets supports the steady consumption of this grade.

Application Insights

Polyethylene is poised to dominate with a forecast market share of over 55% in 2026, powered by the global shift toward flexible packaging and durable plastic goods. Heavy-duty geomembranes used in mining operations rely on 1-butene-based Linear Low-Density Polyethylene (LLDPE) for superior chemical resistance. This application remains the primary consumer of the total 1-butene supply.

Secondary butyl alcohol (SBA) is estimated to be the fastest-growing segment, fueled by the expanding pharmaceutical and cosmetics industries. The synthesis of specialized fragrance fixatives frequently employs SBA as a key intermediate. This growth is supported by increasing consumer spending on personal care products.

End-user Insights

Packaging is likely to be the leading segment with a projected 48% of the 1-butene market share in 2026 due to the rapid expansion of global e-commerce and food delivery services. Multi-layer food packaging films utilize 1-butene comonomers to achieve high puncture resistance. This segment benefits from the continuous need for protective and shelf-stable packaging solutions.

The automotive segment is anticipated to be the fastest-growing segment, fueled by the demand for lightweight plastic components in electric vehicles. Modern fuel tank systems are increasingly manufactured using specialized polymers to reduce vehicle weight. This trend aligns with global efforts to improve fuel efficiency and reduce carbon emissions.

Regional Insights

North America 1-Butene Market Trends

North America holds a significant share of the global market, supported by advanced petrochemical infrastructure and integrated refining capacity. The U.S. leads due to shale-based feedstock availability, while Canada emerges as the fastest-growing country, driven by infrastructure investments and the expansion of petrochemical facilities.

U.S. 1-Butene Market Insights

The U.S. market is projected to expand significantly as companies such as Chevron Phillips Chemical capitalize on low-cost ethane feedstocks. A 2025 development involved the completion of a major 1-butene unit on the Gulf Coast to support domestic LLDPE production. Regulatory support for domestic manufacturing through the Inflation Reduction Act incentivizes continued investment.

Canada 1-Butene Market Insights

The Canada market is forecast to grow as Nova Chemicals expands its polyethylene capacity in Ontario. The development of new C4 extraction facilities enhances the domestic supply of high-purity chemical intermediates. Infrastructure investment in the Alberta Industrial Heartland facilitates the transport of products to international export hubs.

Europe 1-Butene Market Trends

Europe represents a mature market characterized by stringent environmental regulations and advanced manufacturing capabilities. Germany leads due to a strong chemical industry presence, while the U.K. emerges as the fastest-growing country, driven by innovation and sustainability initiatives.

U.K. 1-Butene Market Insights

The U.K. market is projected to grow steadily due to a focus on sustainable chemical production. INEOS announced an investment in low-emission petrochemical processes in 2025. Regulatory frameworks promoting environmental compliance drive the adoption of efficient production technologies and support long-term market development.

Germany 1-Butene Market Insights

The Germany market is projected to maintain leadership due to its advanced industrial infrastructure. BASF expanded specialty chemical production in 2025, strengthening its market position. Strong regulatory support for sustainable manufacturing and innovation enhances competitiveness and supports growth in downstream applications.

Asia Pacific 1-Butene Market Trends

Asia Pacific is expected to lead with an estimated 42% of the 1-butene market share, supported by the massive manufacturing base in China and India. Asia Pacific is also forecast to be the fastest-growing market for the 1-butene market, stimulated by rapid industrialization and a burgeoning packaging sector.

China 1-Butene Market Insights

The China market is driven by the state-led expansion of petrochemical complexes, including significant capacity additions by Sinopec. Recent 2024 developments include the commissioning of integrated refinery units that maximize C4 stream recovery. National policies focused on self-sufficiency in high-end polymers accelerate the adoption of domestic 1-butene production technologies.

India 1-Butene Market Insights

The India market is projected to witness robust growth following Reliance Industries Limited's investment in advanced oligomerization units. Government initiatives such as Make in India promote the development of local chemical value chains. The 2025 expansion of plastic processing hubs in western India creates a consistent demand for high-grade chemical precursors.

Competitive Landscape

The global 1-butene market is moderately consolidated, with 8 players controlling approximately 65% of total shares. Leading manufacturers dominate due to strong production capacity, raw material integration, and energy-efficient product innovation. High entry barriers persist due to capital-intensive manufacturing processes and stringent environmental standards.

Sinopec, Exxon Mobil Corporation, and LyondellBasell Industries lead the competitive landscape with extensive global manufacturing networks. Chevron Phillips Chemical and Evonik Industries maintain strong positions through specialized chemical solutions. These companies leverage capacity expansion, product innovation, and regulatory compliance to sustain market leadership across chemical and industrial sectors.

Key Industry Developments:

- In February 2026, Evonik Industries expanded global hydroxyl-terminated polybutadiene production capacity across Germany and Asia, strengthening the supply of butadiene-derived materials and reinforcing value chain integration.

- In January 2026, Technip Energies secured major contracts from Bharat Petroleum Corporation Limited to develop new polypropylene and butene-1 units at the Bina refinery, strengthening downstream petrochemical capacity and feedstock availability.

- In September 2025, S&P Global Commodity Insights launched a weekly CFR Southeast Asia butene-1 price assessment, enhancing pricing transparency and benchmarking across regional olefins trade flows.

Companies Covered in 1-Butene Market

- Sinopec (China Petrochemical Corporation)

- Exxon Mobil Corporation

- LyondellBasell Industries N.V.

- Chevron Phillips Chemical Company LLC

- Evonik Industries AG

- Reliance Industries Limited

- TPC Group

- Sabic (Saudi Basic Industries Corporation)

- Shell plc

- Mitsui Chemicals, Inc.

- Sumitomo Chemical Co., Ltd.

- INEOS Group

- PetroChina Company Limited

- Lotte Chemical Corporation

- Braskem S.A.

Frequently Asked Questions

The 1-butene market is projected to reach US$19.4 billion in 2026.

Rising polyethylene production for packaging and infrastructure applications drives demand for 1-butene, supported by expanding petrochemical integration and catalyst efficiency improvements.

The 1-butene market is poised to witness a CAGR of 5.5% from 2026 to 2033.

Expansion into specialty chemicals and adoption of sustainable recycling technologies create key growth opportunities for 1-butene utilization.

Some of the key market players include Sinopec, Exxon Mobil Corporation, Chevron Phillips Chemical Company LLC, and LyondellBasell.