- Bulk Chemicals

- Aluminum Sulfate Market

Aluminum Sulfate Market Size, Share and Growth Forecast, 2026 - 2033

Aluminum Sulfate Market by Application (Water Treatment, Pulp & Paper, Textile Processing, Others), Grade Level (Standard Grade, High Purity Grade, Iron-Free Grade, Ferric Grade), Product Form (Liquid, Solid, Powder), and Regional Analysis for 2026 - 2033

Aluminum Sulfate Market Share and Trends Analysis

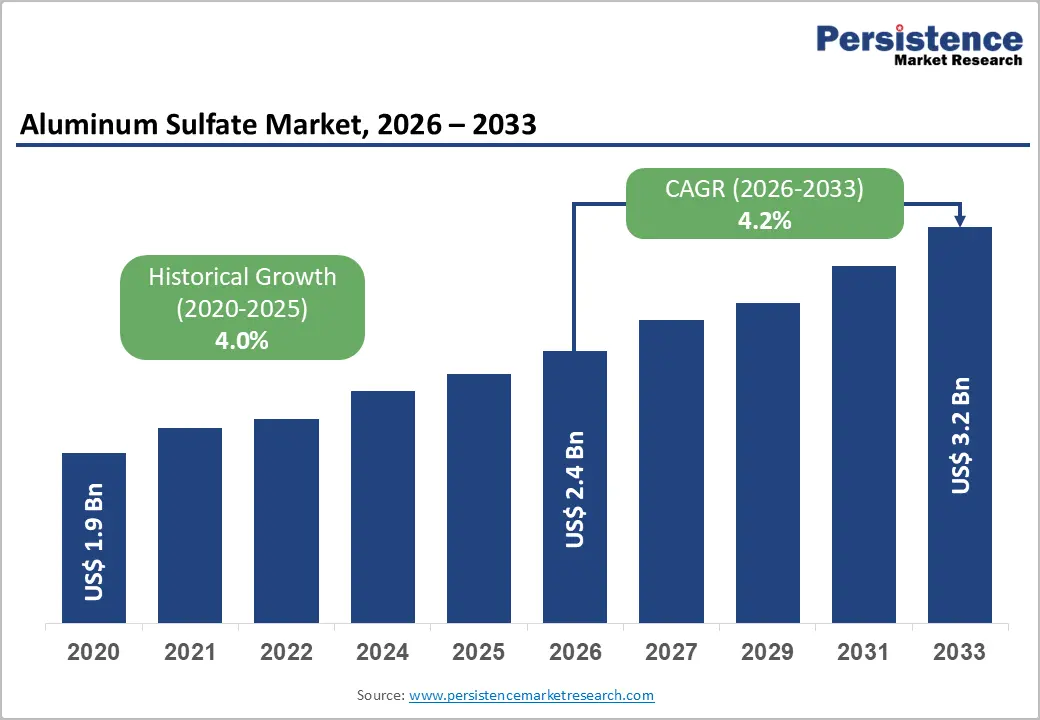

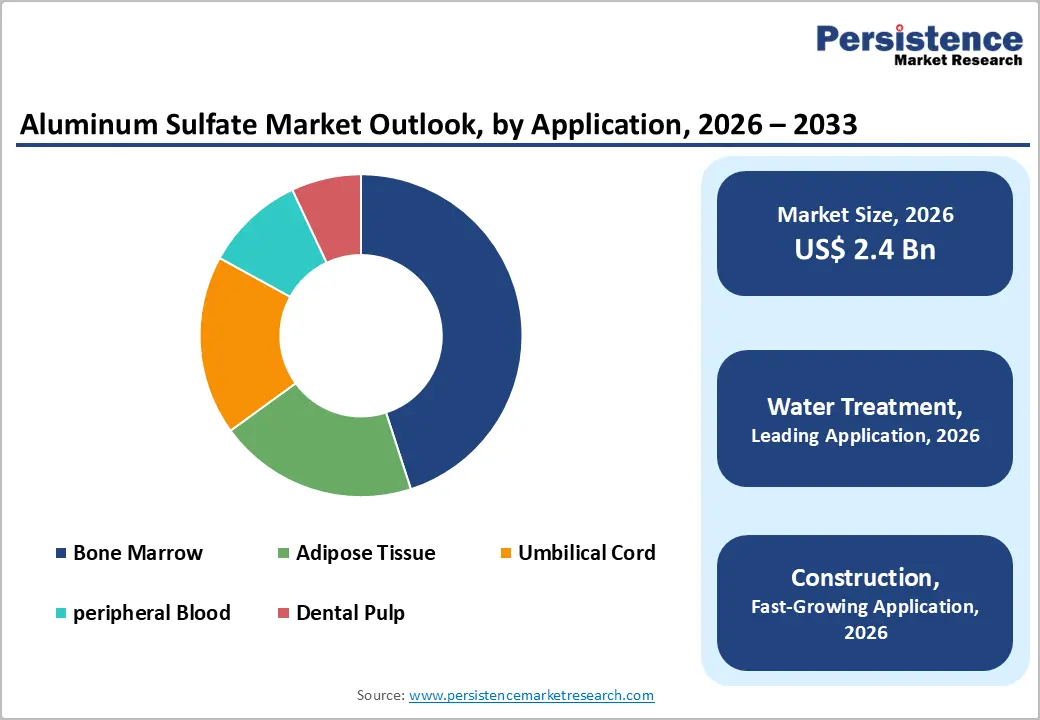

The global aluminum sulfate market size is likely to be valued at US$2.4 billion in 2026 and is projected to reach US$3.2 billion by 2033, growing at a CAGR of 4.2% during the forecast period 2026 - 2033, driven by rising global water treatment demand, supported by increasing urbanization and stricter wastewater regulations.

Industrial consumption across pulp & paper and textiles remains stable, while infrastructure expansion is accelerating usage in construction applications. Regulatory mandates from organizations such as the U.S. Environmental Protection Agency (EPA) and the European Environment Agency (EEA) are reinforcing demand for coagulants such as aluminum sulfate in municipal and industrial water purification systems.

Key Industry Highlights:

- Dominant Applications: Water treatment is set to command around 48% of the revenue share in 2026, while the construction segment is likely to grow the fastest at 4.5% CAGR through 2033, driven by rising infrastructure and urban development investments.

- Leading Grade Levels: Standard grade aluminum sulfate is expected to lead with 52% share in 2026, while high purity grade is projected to be the fastest-growing at 4.7% CAGR during 2026 - 2033, supported by stringent quality requirements in pharmaceuticals and food processing.

- Dominant Product Forms: Liquid aluminum sulfate is anticipated to lead with an estimated 46% share in 2026, while powder form is slated to be the fastest-growing at 4.8% CAGR from 2026 to 2033, driven by logistics efficiency and extended shelf life advantages.

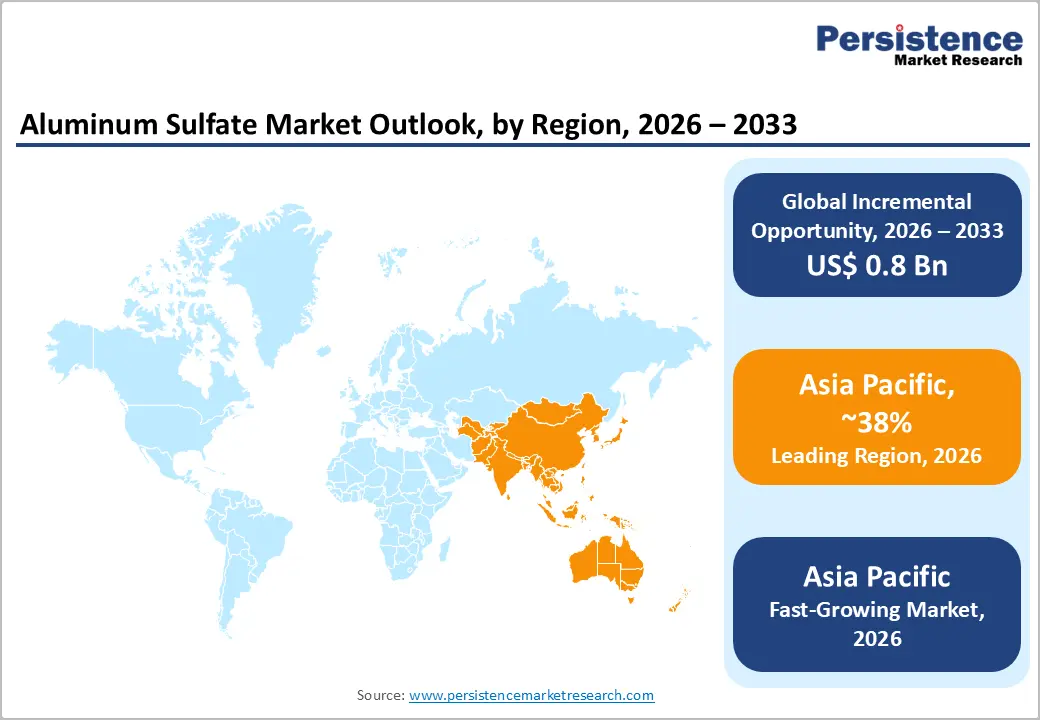

- Regional Leadership: Asia Pacific is poised to dominate with an estimated 38% share in 2026, supported by rapid urbanization and industrial expansion, and is expected to maintain the fastest growth trajectory through 2033.

- Competitive Environment: Competitive dynamics are shaped by capacity expansions, digital dosing innovations, and sustainability-focused solutions, with companies strengthening regional supply chains and enhancing water treatment efficiency.

DRO Analysis

Driver - Rising Global Water Treatment Demand and Regulatory Enforcement

The primary driver for the aluminum sulfate market is the expansion of water treatment infrastructure globally. According to the United Nations World Water Development Report (2025), over 56% of the global population lacks safely managed wastewater treatment, driving government investments exceeding US$320 billion annually in water infrastructure. Aluminum sulfate remains a preferred coagulant chemical due to cost efficiency and effectiveness in removing suspended solids and phosphorus.

Regulatory frameworks such as the U.S. Clean Water Act and the EU Urban Wastewater Treatment Directive mandate strict discharge standards, increasing chemical dosing requirements. Emerging economies, particularly India, under programs such as Jal Jeevan Mission, are scaling municipal treatment capacity, directly boosting demand. This structural dependency positions aluminum sulfate as a critical water treatment chemical, ensuring consistent market expansion.

Restraint: Environmental and Sludge Disposal Challenges

A key restraint impacting the aluminum sulfate market growth is the environmental concern associated with sludge generation. Aluminum-based coagulants produce high volumes of chemical sludge, increasing disposal costs by up to 25-30% of total treatment expenses, as noted by the International Water Association (IWA).

Additionally, tightening environmental regulations regarding landfill use and sludge reuse are increasing compliance costs for utilities and industries. Alternatives such as polyaluminum chloride (PAC) are gaining traction due to lower sludge production, creating competitive pressure. These structural challenges may limit adoption in cost-sensitive regions and encourage substitution in advanced treatment systems.

Opportunity: Expansion in Emerging Economies and Industrial Water Recycling

A significant opportunity exists in emerging markets and industrial water reuse systems. The World Bank (2025) estimates that water reuse investments will exceed US$110 billion by 2030, particularly in Asia Pacific and the Middle East. Aluminum sulfate is widely used in pre-treatment stages for industrial recycling systems.

Rapid industrialization in countries such as India, Vietnam, and Indonesia is increasing demand for industrial wastewater treatment chemicals. Additionally, zero liquid discharge (ZLD) policies in sectors such as textiles and chemicals are driving consistent chemical consumption. This creates a scalable opportunity segment exceeding US$800 million by 2030, positioning aluminum sulfate as a key enabler in sustainable water management systems.

Category-wise Analysis

Application Insights

The water treatment segment is expected to lead the aluminum sulfate market with an estimated 48% share in 2026, anchored in its critical role across municipal and industrial purification systems. Demand remains structurally tied to tightening discharge norms and rising treatment volumes, where aluminum sulfate continues to offer a cost-efficient solution for turbidity and phosphorus removal. Expansion of wastewater infrastructure across developed and emerging economies is expected to sustain consistent consumption levels. In 2025, the U.S. Environmental Protection Agency scaled up funding under national water infrastructure programs, reinforcing chemical demand across treatment facilities.

The construction segment, while smaller in base, is projected to register the fastest growth at around 4.5% CAGR through 2033, reflecting its increasing integration into cement chemistry and waterproofing systems. As infrastructure pipelines expand, particularly in transport corridors and urban developments, aluminum sulfate is gaining relevance in enhancing material performance. The shift toward durable and rapid-setting construction materials is further supporting uptake. In 2025, the European Commission continued large-scale infrastructure financing across transport and energy networks, indirectly strengthening demand for construction chemicals, including aluminum sulfate-based additives.

Grade Level Insights

The standard grade segment is expected to hold a leading 52% share in 2026, largely due to its alignment with high-volume, cost-sensitive applications such as water treatment and pulp processing. Its dominance reflects a balance between performance and affordability, making it the default choice across municipal utilities and industrial operations. With global treatment capacity expanding, particularly in regulated markets, demand for standard-grade material is expected to remain structurally stable. In 2025, the Organisation for Economic Co-operation and Development highlighted sustained public investment in water infrastructure, reinforcing reliance on economical treatment chemicals.

At the higher end of the value chain, the high purity grade segment is projected to grow the fastest at approximately 4.7% CAGR through 2033, driven by regulatory tightening in sensitive applications. Industries such as pharmaceuticals, cosmetics, and food processing are increasingly shifting toward refined inputs to meet contamination thresholds and compliance requirements. This transition is particularly visible in developed markets where quality standards continue to evolve. In 2025, the European Medicines Agency updated guidance on excipient quality and impurity limits, a move expected to accelerate the adoption of high-purity aluminum sulfate in regulated manufacturing environments.

Product Form

The liquid segment is expected to account for around 46% of the market in 2026, reflecting its operational advantages in large-scale treatment systems. Its ability to integrate seamlessly with automated dosing infrastructure and deliver consistent performance makes it the preferred format for utilities. As treatment plants continue to modernize, particularly with digital monitoring and precision dosing, liquid formulations are expected to maintain their lead. In 2025, PUB Singapore expanded its smart water management systems with advanced dosing technologies, reinforcing the shift toward liquid coagulants in high-efficiency treatment environments.

The powder segment is anticipated to expand at the fastest pace, with an estimated 4.8% CAGR through 2033, supported by its logistical and storage advantages. Its relevance is growing in decentralized treatment setups and regions where transport infrastructure or storage conditions limit the use of liquid chemicals. The flexibility to deploy powder formulations in smaller or remote systems is driving steady adoption. In 2025, the World Bank increased funding for decentralized water and sanitation programs across developing regions, a shift that is expected to favor powder-based chemical solutions due to ease of distribution and handling.

Regional Insights

North America Aluminum Sulfate Market Trends

North America is estimated to account for 26% of the global aluminum sulfate market in 2026, supported by advanced water treatment infrastructure and stringent regulatory enforcement. Demand is closely linked to the modernization of aging municipal systems, rising wastewater reuse targets, and nutrient removal mandates. Increasing adoption of automated dosing and digital monitoring is further improving chemical efficiency and sustaining steady consumption across utilities.

U.S. Aluminum Sulfate Market Trends

U.S. dominates the region with approximately 78% share, driven by large-scale municipal upgrades and federal funding support. In 2025, the U.S. Environmental Protection Agency finalized new limits on PFAS in drinking water, accelerating upgrades in treatment plants and increasing coagulant demand. This regulatory tightening is expected to sustain aluminum sulfate consumption in advanced purification systems.

Canada Aluminum Sulfate Market Trends

Canada holds close to 14% regional share, with demand shaped by industrial water treatment in mining and energy sectors. In 2025, the Government of Canada announced funding under the Investing in Canada Infrastructure Program to upgrade water and wastewater facilities. These developments are expected to strengthen demand for treatment chemicals, particularly in resource-intensive provinces.

Europe Aluminum Sulfate Market Trends

Europe is projected to hold around 22% of the global market in 2026, driven by strict environmental regulations and circular water management policies. Regulatory harmonization across the EU ensures consistent demand for coagulants in municipal and industrial treatment systems, while sustainability goals are encouraging efficient chemical usage and wastewater reuse practices.

Germany Aluminum Sulfate Market Trends

Germany leads with an estimated 24% share within Europe, supported by its strong industrial base and advanced recycling infrastructure. In 2025, the German Environment Agency advanced national wastewater reuse guidelines to support industrial water efficiency. This is expected to reinforce demand for coagulants in closed-loop treatment systems across manufacturing sectors.

U.K. Aluminum Sulfate Market Trends

The U.K. is expected to account for approximately 18% regional share, driven by ongoing investments in wastewater infrastructure under regulatory cycles. In 2025, Ofwat approved major funding allocations under the PR24 price review, enabling utilities to expand treatment capacity and improve nutrient removal. This is expected to sustain demand for aluminum sulfate in municipal systems.

Asia Pacific Aluminum Sulfate Market Trends

Asia Pacific is expected to dominate with approximately 38% of the global aluminum sulfate market in 2026, supported by rapid urbanization, industrial expansion, and large-scale water infrastructure investments. The region benefits from cost-efficient production and strong government-backed initiatives to expand treatment capacity, positioning it as the fastest-growing market globally.

China Aluminum Sulfate Market Trends

China leads the region with an estimated 42% share, driven by strict industrial wastewater regulations and large municipal treatment networks. In 2025, the Ministry of Ecology and Environment of China expanded enforcement of wastewater discharge standards under its national pollution control program. This is expected to increase demand for coagulants across industrial and municipal treatment facilities.

Japan Aluminum Sulfate Market Trends

Japan holds around 12% regional share, supported by advanced treatment technologies and high-quality chemical usage. In 2025, the Ministry of Land, Infrastructure, Transport, and Tourism expanded investments in resilient water infrastructure to address climate-related risks. These upgrades are expected to sustain demand for high-performance coagulants, including aluminum sulfate, in precision treatment systems.

Competitive Landscape

The global aluminum sulfate market structure is moderately fragmented, with leading players such as Kemira Oyj, Chemtrade Logistics Inc., GEO Specialty Chemicals, and USALCO LLC collectively accounting for a significant share of global revenues. These companies leverage strong relationships with municipal utilities and industrial clients, supported by established distribution networks and long-term supply agreements. Their competitive edge lies in cost-efficient production, consistent product quality, and integrated water treatment solutions, with increasing investments in process optimization and environmental compliance.

Regional and niche manufacturers such as Gujarat Alkalies and Chemicals Ltd. and Nippon Light Metal Holdings are strengthening their presence through localized production and supply chain advantages. Entry barriers remain moderate due to raw material accessibility, regulatory requirements, and logistics constraints, particularly in water treatment applications. However, evolving trends in sustainable water management and digital dosing technologies are opening avenues for differentiation. Market consolidation is expected to progress gradually, with established players focusing on capacity expansion and regional penetration, while smaller firms compete through pricing strategies and proximity to end-use industries.

Key Industry Developments:

- In November 2025, Chemtrade announced the US$150 million acquisition, expanding its footprint in municipal and food-processing water treatment markets across North America. The deal aligns with its Vision 2030 strategy, strengthening its specialty chemical portfolio and enhancing its turnkey water solutions capabilities.

- In 2025, Kemira completed the acquisition of Thatcher Group’s iron sulfate coagulant business in April 2025 and Water Engineering, Inc. in October, 2025, for US$150 million to strengthen its water treatment portfolio. These moves enhance Kemira’s position in industrial water treatment and coagulant chemicals, particularly across the Eastern U.S. and boiler/cooling water treatment segments.

Companies Covered in Aluminum Sulfate Market

- Chemtrade Logistics Inc.

- Kemira Oyj

- GEO Specialty Chemicals

- USALCO LLC

- Holland Company Inc.

- Affinity Chemical LLC

- Nippon Light Metal Holdings

- BASF SE

- Solvay SA

- Aditya Birla Chemicals

- Gujarat Alkalies and Chemicals Ltd.

- NALCO

- C&S Chemicals

- Summit Chemical Specialty Products

Frequently Asked Questions

The global aluminum sulfate market is projected to reach US$2.4 billion in 2026.

The aluminum sulfate market grows due to rising demand for water treatment chemicals, supported by regulatory compliance and expanding wastewater infrastructure.

The aluminum sulfate market is expected to grow at a 4.2% CAGR from 2026 to 2033.

Key opportunities include expansion in industrial water recycling, emerging market infrastructure, and high-purity chemical applications.

Key players include Kemira Oyj, Chemtrade Logistics Inc., GEO Specialty Chemicals, USALCO LLC, and Gujarat Alkalies and Chemicals Ltd.