- Power Generation, Transmission, & Distribution

- Power Transformer Market

Power Transformer Market Size, Share, and Growth Forecast 2026 - 2033

Power Transformer Market by Core (Closed, Shell, Berry), Insulation (Gas, Oil, Solid, Air), Phase (Single, Three), Application (Residential and Commercial, Utilities, Industrial), and Regional Analysis, 2026 - 2033

Power Transformer Market Size and Trends Analysis

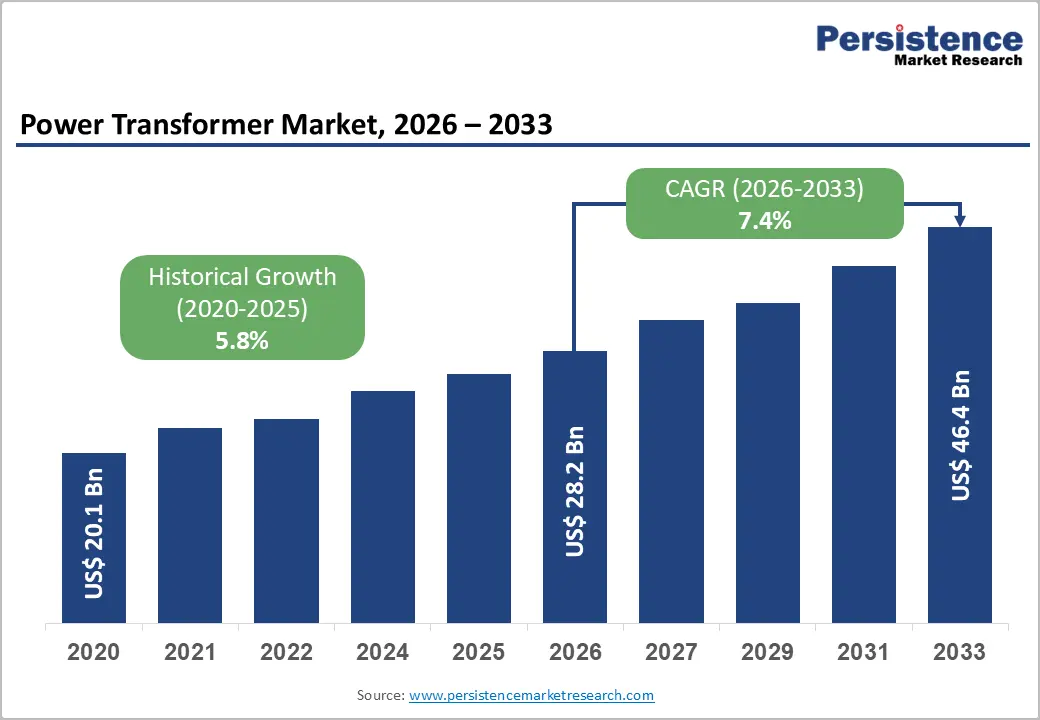

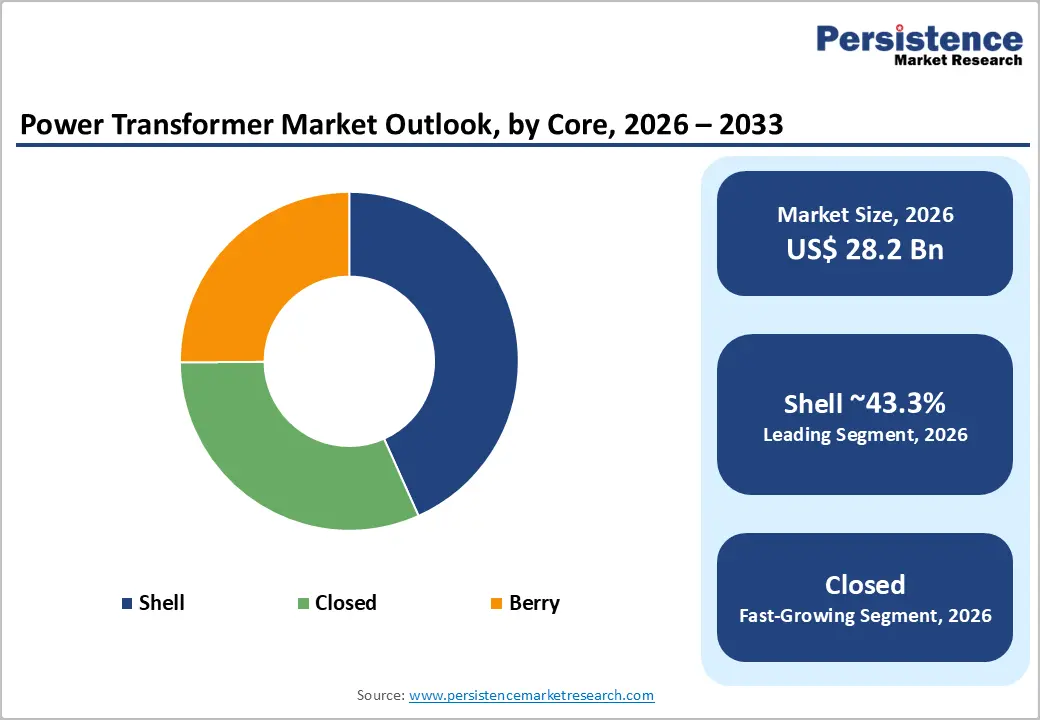

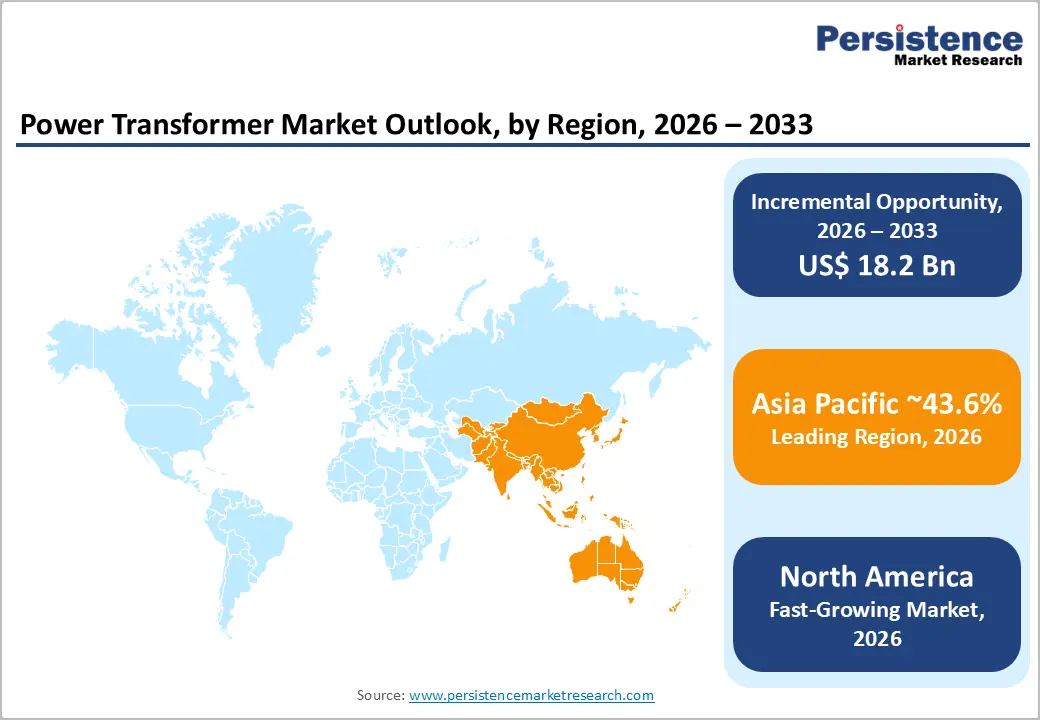

The global power transformer market size is likely to be valued at US$28.2 billion in 2026 and is expected to reach US$46.4 billion by 2033, growing at a CAGR of 7.4% during the forecast period from 2026 to 2033, driven by accelerating grid modernization programs, especially in North America and Europe, where aging transmission infrastructure is being replaced to support high electricity loads.

Key Industry Highlights:

- Leading Core: Shell, approximately 43.3% share in 2026, as it provides high mechanical strength and superior short-circuit resistance.

- Dominant Insulation: Oil, nearly 60.4% in 2026, due to its dual function of effective cooling and electrical insulation.

- Leading Region: Asia Pacific, with about 43.6% share in 2026, owing to large-scale grid expansion programs and sustained investments in ultra-high voltage transmission networks.

- Fast-growing Region: North America, backed by urgent replacement of aging grid infrastructure and rising power demand from data centers.

- Latest Acquisition: In January 2026, RESA Power expanded its transformer services by acquiring Quebec-based Société Générale d'Électrotechnique (SGE). This acquisition would enable the company to focus on the development and maintenance of electrical utilities infrastructure.

DRO Analysis

Driver - Surge in Renewable Energy Connections to the Grid

Solar and wind plants are mostly built far from where electricity is consumed. Getting that power to cities requires step-up transformers at the generation site and converter transformers at grid entry points. This creates a sustained demand. The National Renewable Energy Laboratory projects that the U.S. alone will need to extend transformer stock capacity by 160% to 260% by 2050 to meet electrification goals.

About 25% of renewable energy projects are already being delayed globally due to transformer shortages. HVDC projects add further pressure. The Saudi Arabia-Egypt HVDC interconnection, operational by 2025, is expected to exchange up to 3 GW of electricity across 1,350 km, requiring specialized converter transformers. In 2024, Brazil recorded its largest-ever grid expansion. It added 10.9 GW of capacity and 91% from solar and wind, requiring significant investment in high-voltage transformers to stabilize the network.

Worn-Out Grids and Heavy Replacement Pipelines

Grid infrastructure across North America and Europe is reaching the end of its usable life. According to the U.S. DOE's Large Power Transformer Resilience Report to Congress (July 2024), the average age of large power transformers (LPTs) in North America’s grid is 38 to 40 years. This creates a steady and unavoidable replacement wave. According to a 2025 report, more than half of U.S. distribution transformers, i.e., around 40 million units, are already beyond their expected service life, adding a replacement burden on top of rising new-build requirements.

Demand for power transformers has risen 119% since 2019, while demand for generator step-up units has grown 274%. The Handy-Whitman Index, which tracks utility capital costs, shows that costs of utility line transformers have almost tripled since 2010. Europe is in a similar position, with utilities now tying procurement to strict environmental compliance standards.

Restraint - Heavy Upfront Costs and Long Payback Timelines

Buying and installing a large power transformer is expensive, and the financial returns take years to materialize. This slows procurement decisions, especially for small utilities and emerging-market operators. High interest rates are adding to financial challenges for utilities, raising the cost of debt financing. Combined with rising capital expenditure, this has caused some utilities to become overextended and more susceptible to credit rating downgrades.

During three of the last five years (2020 to 2024), more utilities had their credit ratings downgraded than upgraded. Supply chain pressures compound the issue. Lead times are averaging 128 weeks for power transformers and 144 weeks for generator step-up units as of Q2 2025, with some orders taking up to four years to fulfill. In 2025 alone, U.S. utilities requested US$31 billion in rate increases, with most expecting high capital spending to continue through 2030. For developing economies, this cost barrier is more acute, often delaying grid modernization programs by years.

Opportunity - Electrification of Rail Corridors and Urban Transit Networks

As governments push to decarbonize transport, rail networks are being electrified at a fast pace. Every electric train requires traction transformers to step down the overhead line voltage for propulsion. In January 2025, Hitachi Energy was awarded a contract to supply 360 RESIBLOC Rail traction transformers to Siemens Mobility for the upgrade of Munich's S-Bahn network. India's electrification drive is another key signal.

The country has electrified 94% of its railway network as of early 2024 and continues progressing toward complete electrification. In January 2025, Alstom secured approximately US$155.52 million to supply traction components and maintenance services for 17 Vande Bharat Sleeper trainsets in India. Each new electrified line, metro extension, or high-speed rail corridor directly translates into transformer orders.

Grid Reliability Mandates and the HVDC Buildout

Stringent reliability standards are compelling grid operators to invest in high-performance transformer infrastructure, particularly HVDC converter transformers. These are not optional upgrades, but they are compliance-driven. Significant 525 kV HVDC equipment orders totaling over US$ 36 billion have already been placed to multiple vendors, covering both converter platforms and transmission cables.

The offshore wind buildout is a key catalyst. Several U.S. states, including New York and New Jersey, have required or expressed interest in HVDC transmission systems to connect new offshore wind farms to the onshore grid. In Europe, the Rajasthan HVDC project in India covers 765 kV/400 kV grid connections as part of a prominent renewable energy transmission corridor from Bhadla to Fatehpur. As more cross-border interconnections are planned globally, the demand for specialized HVDC converter transformers will continue rising alongside strict grid performance requirements.

Category-wise Analysis

Core Insights

Shell core is anticipated to dominate with a share of approximately 43.3% in 2026. Shell core transformers deliver an efficient cooling system, design flexibility, high seismic resistance, smooth control of leakage magnetic flux, and superior short-circuit tolerance. As the winding is enclosed within the core, heat dissipation is more uniform. This makes them the preferred choice in high-output and low-voltage applications such as industrial substations and electronic circuits.

The closed core segment will likely remain in the second position in 2026. Closed-core transformers are designed to minimize magnetic flux leakage and core losses, resulting in better voltage regulation and less energy wastage. They also handle the unpredictable and bidirectional power flows that come with solar and wind integration far better than old designs.

Insulation Insights

The oil insulation segment is predicted to lead with a share of nearly 60.4% in 2026. Oil insulation is widely used across industries due to its thermal stability and dielectric strength, while its dielectric properties reduce damage from high voltage. These advantages position oil insulators as the preferred choice among manufacturers. For large transformers above 100 MVA, oil is still the most cost-effective coolant with superior thermal conductivity.

The gas insulation segment is projected to be the fastest-growing in 2026. As cities become denser and space inside urban substations shrinks, Gas-Insulated Transformers (GITs) have become the go-to solution. They are compact, non-flammable, and safe for underground or indoor environments. In Tokyo, for example, over 400 gas-insulated transformers were installed between 2020 and 2023 in underground substations beneath commercial complexes. It was mainly due to their non-flammable nature and compact footprint.

Regional Insights

Asia Pacific Power Transformer Market Trends

In 2026, Asia Pacific is predicted to dominate with a share of nearly 43.6%. It is augmented by the sheer scale of electrification and industrialization underway across the region. The region's focus on integrating renewable energy sources and reducing transmission losses further encourages the adoption of energy-efficient transformer technologies. The region accounts for a majority of newly commissioned high-voltage transmission projects globally. For instance, India's entire 765 kV transmission corridor relies exclusively on three-phase units, with Power Grid Corporation installing 210 such transformers between 2020 and 2023.

China Power Transformer Market Trends

China is the world's largest and most active market for transformers, and its ambitions are only expanding. State Grid Corporation of China's fixed-asset investment rose to a record high of over US$93.2 billion in 2025. The country's west-to-east power transmission strategy is the central force behind transformer demand. China plans to commission 15 new Ultra-High Voltage (UHV) transmission lines between 2026 and 2030. It would enable around 200 GWh per year of renewable power to connect to the grid and boost cross-provincial electricity transmission capacity by 35%.

Indonesia Power Transformer Market Trends

Indonesia presents a compelling long-term opportunity, though it remains more of an emerging market than a top-tier one. The country is still expanding its grid. Large parts of its eastern regions, including Sulawesi, Kalimantan, and Papua, are in active electrification phases. The Eastern part of Indonesia is experiencing high demand for power transformers due to the ongoing development of power plants and substations in these regions. Indonesia's state utility PLN built 4,616 km of additional transmission lines and 16,210 MVA of substation transformer capacity under its expansion programs. The government's push to complete electrification and support industrial growth creates consistent procurement activity.

North America Power Transformer Market Trends

North America is expected to be the fastest-growing region in 2026. Urgent replacement of aging infrastructure, as well as surging new load from AI data centers and EV charging, are pushing the market forward. The U.S. continues to dominate the regional market, fueled by federal investments in grid modernization, rising electrification of transportation, and AI-supported data center expansion. Ongoing shortages have catalyzed domestic production initiatives, pointing to long-term structural growth.

U.S. Power Transformer Market Trends

The U.S. is simultaneously dealing with a supply crisis and an unprecedented demand surge. Demand for generator step-up transformers increased by 274% between 2019 and 2025. During the same period, demand for substation transformers rose by 116%, fueled by AI data center growth and the ongoing transition to electrified transport and industrial manufacturing. The supply side is struggling to keep up. Standard power transformers average 128 weeks for delivery, and generator step-up transformers average 144 weeks. Some specialized orders are extending to four years. Power transformer prices have risen 77% since 2019.

Europe Power Transformer Market Trends

Europe is being boosted by a policy-led, long-term energy transition rather than a short-term spike. The EU's Ecodesign Directive is raising efficiency thresholds, forcing old transformers off the grid. Europe's Ecodesign Directive, complying with Tier 2 standards, sets ecological criteria for power transformers and can unlock energy savings of 16.2 TWh annually, reducing CO2 emissions by 3.7 million tons. Cross-border interconnections are also generating large-scale procurement. Domestic HVDC projects such as the NeuConnect UK-Germany cable are spurring large transformer orders.

Germany Power Transformer Market Trends

Germany is Europe's single largest market. The country's Energiewende, a national policy to transition to renewable energy, is the central driver. Renewable energy sources accounted for around 46% of the country's electricity generation in 2022, bolstering demand for high-performance transformers capable of handling variable energy inputs. Offshore wind capacity in the North Sea is a key contributor to power transformer demand. Siemens Energy's September 2025 decision to invest €220 million (US$240 million) to broaden its century-old Nuremberg transformer plant by 50% further underscores how central Germany is to Europe’s transformer supply.

U.K. Power Transformer Market Trends

The U.K. is growing steadily, mainly spurred by offshore wind expansion. According to the U.K. Department for Energy Security and Net Zero, the country allocated £10 billion (US$13.3 billion) in 2023 to extend its energy infrastructure, including offshore wind farms that require specialized transformers for efficient power transmission. The government's long-term grid blueprint is adding further structural demand. The country’s GBP 58 billion Beyond 2030 blueprint aims to connect 21 GW of additional offshore wind, ensuring multi-year orders for medium- and ultra-high-voltage transformer units.

Competitive Landscape

The global power transformer market is moderately consolidated. Companies such as Hitachi Energy, Siemens Energy, GE Vernova, TBEA, and Hyundai Electric dominate large utility-scale contracts because of their manufacturing capacity, HVDC expertise, and long-standing relationships with grid operators. Competition has shifted away from only pricing and now revolves around manufacturing capacity, delivery timelines, and grid modernization capabilities.

Due to transformer shortages globally, utilities increasingly prioritize suppliers that can guarantee delivery slots rather than only low-cost bids. Hitachi Energy currently holds one of the most prominent competitive positions globally, mainly in HVDC and grid integration transformers. Siemens Energy has strengthened its position through smart-grid and digital transformer technologies.

Key Industry Developments:

- In February 2026, Siemens Energy finalized a US$1 billion investment plan to ramp up manufacturing of gas turbines and power-grid solutions in the U.S. It includes increasing manufacturing capacity for large power transformers and resuming gas turbine manufacturing in Charlotte, North Carolina.

- In February 2026, GE Vernova completed the acquisition of the remaining 50% stake in Prolec GE for US$5.275 billion, bringing full ownership of the transformer manufacturer after a 30-year joint venture. The deal closed following receipt of all regulatory approvals, with Prolec GE now operating in GE Vernova's Electrification segment.

- In January 2026, RESA Power acquired Virginia-based 3MD Power Services LLC. The transaction bolstered the former’s transformer dielectric fluid processing fleet and expanded its operational footprint into the South Atlantic states.

Companies Covered in Power Transformer Market

- ABB Ltd.

- Alstom SA

- Bharat Heavy Electricals Limited

- Crompton Greaves Ltd.

- GE Co.

- Hyosung Power & Industrial Systems Performance Group

- Hyundai Heavy Industries Co. Ltd.

- Mitsubishi Electric Corporation

- Siemens Energy

- Toshiba Corp.

- Others

Frequently Asked Questions

The global power transformer market is projected to be valued at US$28.2 billion in 2026.

The power transformer market is expected to reach US$46.4 billion by 2033.

Key trends include the adoption of digital monitoring systems and the rising demand for transformers suited for renewable integration.

Shell is expected to be the leading core with a share of nearly 43.3% in 2026, backed by its compact design and superior voltage regulation performance.

The power transformer market is expected to grow at a CAGR of 7.4% from 2026 to 2033.

ABB Ltd., Alstom SA, Bharat Heavy Electricals Limited, and Crompton Greaves Ltd. are a few key market players.